The Northern Trust Economics team shares its outlook for U.S. economic growth, inflation, unemployment and interest rates.

Labor Day weekend marked the functional end of a long, hot summer; the season ahead might be a little cooler for U.S. consumers and businesses. The U.S. administration stepped up tariffs on over $100 billion of Chinese imports of various consumer goods. Beijing retaliated with its own increased tariffs on several American products, including cars. Though the economy continues to show resilience, a few cracks are appearing in the façade. Manufacturing activity and consumer sentiment have both declined from multi-year highs.

Although formal talks between China and the United States are set to resume next month, we are not hopeful for a breakthrough. The continuing uncertainty has led us to reduce our growth projections for the U.S. economy. Recession is not imminent, but risks will rise if the trade war continues to escalate.

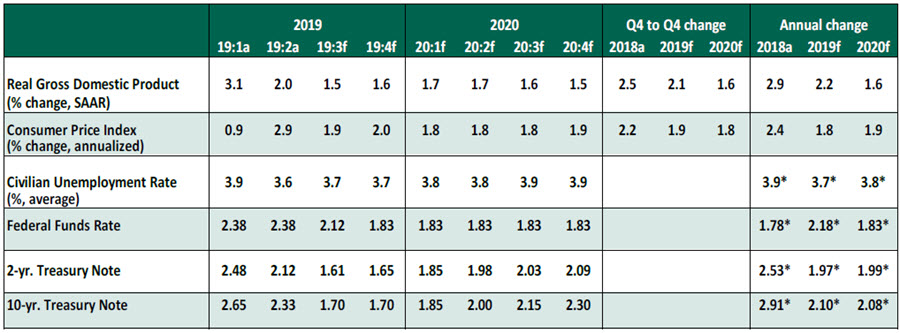

Key Economic Indicators

Influences on the Forecast

- American consumers continue to remain a solid pillar of the U.S. economy. Sturdy labor market conditions continue to support gains in personal spending. But the drop in the University of Michigan Consumer Sentiment Index to a nearly three-year low shows consumers are becoming somewhat more concerned about the economy’s prospects.

- The manufacturing sector continues to struggle with tightening trade policy. The Institute for Supply Management Purchasing Managers’ Index fell further to 49.1 in August (indicating contraction), the lowest reading in more than three years. New export orders also slowed for the second consecutive month to their lowest reading since April 2009. Readings on the service sector remain encouraging.

- Despite the further increase in tariffs, the U.S. and China have agreed (yet again) to go back to the negotiating table, cheering investors hoping for a possible truce. As recent history suggests, the optimism is likely to be short-lived, as the talks are unlikely to achieve any substantial headway. We expect trade tensions to remain elevated through the forecast horizon.

- Uncertainty is likely to keep the demand for U.S. Treasuries high and yields suppressed. We have consequently reduced our expectations for long-term yields.

- The August employment report was a mixed bag. Alongside downward revisions to the July numbers, the payroll increase was modest, but not abysmal. The unemployment rate held steady at 3.7% in August, and wages continued to grow at an annual rate above 3%. Overall, the U.S. labor market remains healthy, but employment growth has likely peaked.

- Second-quarter real gross domestic product (GDP) growth was revised downward by one-tenth to an annualized rate of 2.0%. Downward revisions to government spending and residential investment were partially offset by an upward revision to consumer spending. We expect GDP growth to continue to decelerate and remain below potential, but not start a downturn. Elevated trade uncertainty, deteriorating global growth prospects and reduced fiscal thrust will continue to weigh on business investments.

- Inflationary pressures remained tame in July, with the deflator on personal consumption expenditures (PCE) edging up marginally to 1.4% year-over-year, while core PCE inflation remained stable at 1.6%, well below the Federal Reserve’s 2% benchmark.

- The Fed is caught in the crossfire of the escalating U.S.-China trade tensions. Fed Chair Jerome Powell acknowledged the rise in geopolitical tensions at his speech at Jackson Hole, reiterating the central bank’s commitment to “act as appropriate to sustain the expansion.” While the Fed does not want to enable the trade conflicts, it could be forced to ease further to offset the negative impact on the economy.

For now, we maintain our prediction of one additional 25bps “insurance” rate cut in September, with further reductions only if the U.S. economy takes a noticeable turn for the worst. Given our growth forecast, which is similar to the Fed’s most recent projections, more aggressive easing does not yet seem warranted.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

More Alternative Investments Topics >