Valuation Is More Important Than Politics or Interest Rates: And Most Stocks Are Overvalued Today

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIntroduction

My personal investing strategy is based on the simple logic and reality that great businesses are by definition, better than average. Therefore, to my way of thinking, it logically follows that the best investment returns would be achieved by investing in the best businesses that you could identify. Moreover, it is also important to make sure that you are purchasing great businesses only when their valuation is sound, or better yet – low based on fundamentals. This is important, because you want to fully participate in the business results of the company you are investing in. Consequently, because of my commonsense strategy, I rarely worry too much about the level of the markets in general.

I have often written about this in the past, and what follows is a repost of an article I wrote in July 2017 titled “Should You Care That The Market Is Overvalued – It Depends”:

Most investors suffer from what I believe is an unhealthy (unprofitable) obsession with the stock market. Financial writers and professional investors never tire about offering up their opinion on what the market will do next – especially short term. Individual investors also are deeply concerned with how the markets are doing on a daily basis. To me this only makes sense if you specifically own the “stock market” i.e., an index fund. Otherwise, only what you specifically own should be of any concern to you.

Since I have been in the investment business (since 1970), I have emphatically stated that I do not believe in investing in the stock market, never have and never will. Since people know that I manage stock portfolios, this always conjures up bewilderment. You can see it in their eyes, asking how I can make such an outlandish statement. Well, I can because it’s the truth. I invest in individual companies and build portfolios one business at a time. The so-called “stock market” is only the store at which I shop to buy what I want to own. Just like any other market; grocery stores, drug stores, clothing stores, etc., once I buy what I desire, the store no longer matters.

The stock market, in all its iterations, whether the Dow or the S&P 500 or any number of other indices are averages. Therefore, by definition, “average” is simply a middle number. Consequently, the logical conclusion dictates that within the average are above-average and below-average companies as well. To carry this thought further, you can also say that logically there are most likely way above-average companies, way below-average companies – and everything in between.

Mind Your Owned Business!

Therefore, in response to the question should you care that the market’s overvalued – my simple answer is no. Instead, I believe you should mind your owned businesses. In other words, quit worrying about the overall market average, and place your attention on the companies (stocks) that you specifically own.

I find it odd that we revere the greatest investors such as Warren Buffett, Peter Lynch, Ben Graham and Marty Whitman, yet we mostly ignore their sage advice. Nowhere is this more evident than how most investors think about stock prices compared to how the masters do. Warren Buffett has lamented “For some reason people take their cues from price action, rather than from values.” Here he is telling us that the business value is more important than the short-term market appraisal. In ‘One Up On Wall Street’ Peter Lynch said “What makes stocks valuable in the long run isn’t the market, it’s the profitability of the shares in the companies you own.“Peter’s advising you to mind your businesses’ operating results, not its price. And of course, the famous Ben Graham, teacher to them all, offers his priceless metaphor, “In the short run the market is a voting machine, but in the long run it’s a weighing machine.” Ben is pointing out that intrinsic value (weight) is the true worth of the company you own, while short-term market price can mis-appraise.

Don’t get me wrong, I really don’t blame people for failing to get this critical point. Other than these masters there are few support groups to help them. Most charting tools are focused solely on price. Therefore, investors have scant resources that calculate intrinsic value. As a result, all they have to judge value on is the current price offered by an auction market. This is what I mean when I say that measuring performance without simultaneously measuring valuation is a job half done.

Marty Whitman has said “Unrealized Market Depreciation occurs when the market price of a publically traded security declines. Permanent impairment of capital occurs when the fundamental values of a business are dissipated with the consequent long-term adverse consequences.” Marty is advising to not sell a business for less than it is worth just because the price is temporarily weak. The FAST Graphs (Fundamentals Analyzer Software Tool) I use to chart stocks focuses first and foremost on true worth values and then measures stock price in relation to those values.

Knowledge truly is power. Ignorance can be very costly when investing money. In modern times herd mentality is mostly emotional – not rational. Over the past two decades, either fear, now greed, has dominated the financial markets. Volatility is often too extreme to be sensible. As I have said before – the reality of running with the herd is that your ultimate destination is the slaughterhouse.

It’s a Market Of Stocks Not A Stock Market

The primary message that I am attempting to convey with this article is to suggest that investors pay close attention to what they specifically own, and less attention to generalities such as the stock market. This also ties into another mantra that I have chanted many times: it’s a market of stocks not a stock market. The essence of this phrase lies in the understanding that the individual companies that make up the so-called stock market are unique to themselves. Not all stocks are the same, and in many cases the disparities are enormous. Consequently, when investors are generalizing about the stock market, they are in effect denying the unique attributes that individual companies possess.

This concept also applies to valuation. Within the large universe of stocks that make up the market, there will always and inevitably be overvalued, undervalued and fairly valued individual stocks to be found. Obviously, long-running bull markets like we are currently in will produce a greater number of overvalued stocks, and bear markets will produce a greater number of undervalued stocks. However, regardless of the market we are in, there will always be some of each.

Fast Forward to August 2019: “Wall Street Climbs A Wall of Worry”

Although the words I posted above were originally written in 2017, they still aptly apply today. We currently are seeing a lot of conversation about the overvalued market, the potential for recession, and/or political and interest rate risks. I get that these are highly charged subjects that most people are concerned about. However, and at the same time, I believe that the actual risks and influences that factors such as politics and interest rates have on my portfolio are significantly less connected than people are led to believe.

To be clear, I am not suggesting that neither politics nor interest rates have any effect at all. Instead, I am simply suggesting that they each are but one of many other factors that investors need to consider. But more pertinent to the point, I am emphatically suggesting that there are significantly more important factors that drive stock values that are unfortunately too often ignored. As I pointed out in the introduction, the market is made up of above-average, average and below-average companies. Therefore, when you think about it, you realize that each of these types of companies exist in all market and economic environments.

Moreover, as I also stated in my first sentence, I am most interested in above-average companies when I can purchase them at sound or attractive valuations. Furthermore, I consider a company above average when its business grows at above-average rates. The most common way to measure this is earnings growth. Because stated succinctly, earnings determine market price in the long run, always have and always will. Emotions may determine market price over the short run, but the short run always gives way to the long run, which is nothing more than a long series of short runs.

The Stock Market: Politics vs Earnings vs Interest Rates vs Valuation

Furthermore, I get very tired of the litany of discussion especially in social media about how this President is better than that President – or vice versa. It also frustrates me when people attempt to give too much credit or blame to a sitting President, Senate or Congress for that matter. Frankly, I contend that people fail to understand that the private sector, businesses large and small coupled with serving the consumer are what ultimately drives our economies and our markets.

Additionally, I believe we overestimate the influence that government and/or macroeconomic factors such as interest rates have on business results. In truth and fact, I do believe that government policies can make it easier or more difficult to do business. Also, I do believe that a higher interest rate environment might be more challenging than a lower interest rate environment. However, I also believe that either of those things are simply items on the expense side of the profit loss statement that management is challenged to deal with. And frankly, one of the factors that determines a great business over a mediocre business is a skilled, honest and competent management team. In other words, I strive to invest in companies where I believe management will be able to successfully navigate the many business challenges that the company will inevitably face.

To illustrate and support my above statements, I offer the following exercise where I evaluate the stock market (the S&P 500), the bluest of all blue-chip dividend growth stocks Johnson & Johnson (JNJ), a widely known but mediocre business General Electric (GE) and a leading REIT Simon Property (SPG). In each case, I have put together a presentation that illustrates the effect of politics, valuation, earnings growth and interest rates against the backdrop of each of their long-term results.

What I hope you will find interesting is that each case provides different perspectives and evidence regarding the influence that politics, earnings, interest rates and valuation play relative to the specific results of each company or entity. I hope you find it both interesting and enjoyable, but most of all enlightening.

With my first screenshot I offer the earnings and price correlated graph on the S&P 500 going back to the beginning of 2000 (as far as I can go) and I have added the sitting presidents for each time period. On the graph itself, I am showing earnings growth (the orange line), monthly closing stock prices (the black line) and valuation depicted as high when price is above the orange line, just right when it touches the orange line and low when it is below the orange line.

These are the observations and conclusions I draw from what I am seeing. We don’t have much time to show regarding the Clinton administration, but we do see that the valuation of the S&P 500 was very high in calendar 2000 (referred to as the irrational exuberant period).

Then under the Bush administration, we do see two recessions, but we also see a period of strong growth from 2002 through 2006 with stock price tracking that growth. The Great Recession brought both falling earnings and falling stock prices but only lasted for about 18 months or so.

Under the Obama administration, we start out with attractive valuation and good earnings growth through 2014. Additionally, the markets’ valuation was very high in 2014, 2015, 2016, 2017 followed by a sharp drop in 2018. Market prices flattened as we saw down earnings in 2015 and a very moderate (6%) growth rate in 2016.

So far under the Trump administration we have seen strong double-digit growth and a very strong market with valuation remaining high. However, what I find most interesting is that the market truly did generally “climb a wall of worry” for the most part regardless of which party was in control. But perhaps most importantly, as I will develop further in a minute, valuation trumped everything.

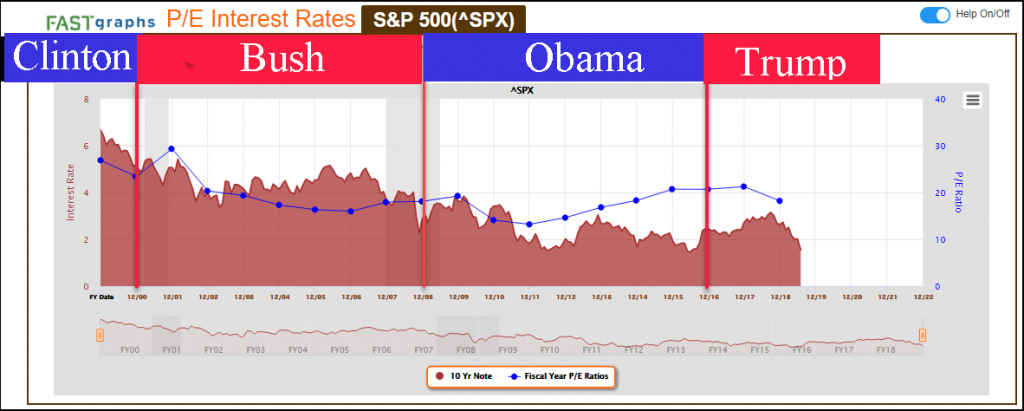

With this next screenshot I am also looking at the relationship between price earnings ratios and interest rates over each of the last four sitting Presidents. Now to clarify why I’m showing this, conventional wisdom suggests that stock valuations would rise during periods of falling interest rates and fall during periods of rising interest rates. The central idea is that fixed income becomes more competitive to equities when interest rates are high, and less competitive when interest rates are low. Consequently, low interest rates would drive up the demand for equities and vice versa. However, for the most part what we see since calendar year 2000 defies this conventional wisdom.

P/E ratios (stock market valuations) depicted by the dark blue line on the graph fell in direct proportion to falling interest rates for the Clinton administration, the entire Bush administration, and for the first three years of the Obama administration. If conventional wisdom was correct, P/E ratios would have risen in an inverse relationship to falling interest rates. Instead, we see in the opposite with interest rates and P/E ratios falling in tandem.

A quick glance back at the first graph illustrates that valuation got in the way of conventional wisdom. During the last 5 years of the Obama administration we did see the expected relationship with P/E ratios (stock valuations) rising as interest rates fell. However, we should also note that market valuations were rational (following the orange line) during that timeframe.

So far during the Trump administration we did see P/E ratios rising modestly during the first year, and then fell during his second year even though interest rates continued to rise. Interestingly, interest rates have fallen thus far in 2019 while valuations appear to be following suit. Once again, defying conventional wisdom. My primary takeaway is that although politics plays a role, and so do interest rates, earnings growth and valuation remain the primary drivers of long-term results. But perhaps most importantly, good above-average businesses thrive under all political and interest rate environments. I believe the evidence as presented is clear in that regard.

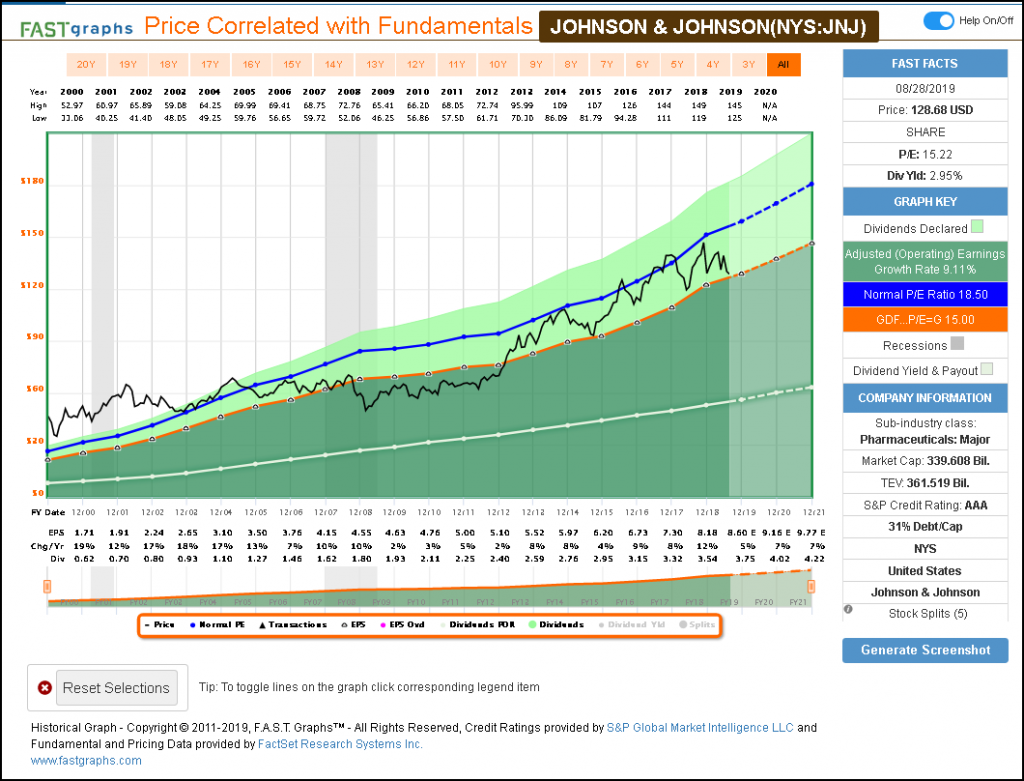

Well, so much for the general stock market as it relates to politics, earnings growth, valuation and interest rates. Next let’s look at the AAA rated blue-chip dividend growth stock Johnson & Johnson and see how these factors impacted its returns.

For starters, we see that Johnson & Johnson performed beautifully as an operating business regardless of which political party held the Presidency. In other words, this company consistently grew its business despite politics. However, we also see that valuation played a significant role on shareholder returns. Johnson & Johnson was significantly overvalued for the better part of calendar year 2000 through 2006. During this timeframe investors fared poorly even though the company did well.

By calendar year 2007 Johnson & Johnson’s stock price became aligned with fair valuation and shareholders did quite well over the next several years. Moreover, when stock price was aligned with fair value as it has been since the beginning of 2008 (despite the Great Recession) Johnson & Johnson shareholders earned a rate of return including dividends that almost perfectly mirrored the operating results of the business. Valuation in conjunction with earnings growth were once again the primary drivers of return.

What’s really interesting about the Johnson & Johnson example is how P/E ratios (valuation) and interest rates both fell in tandem. Once again, this defies conventional wisdom that suggests that P/E ratios should rise when interest rates fall. Of course, the culprit was very high valuations in 2000. From observing the below graphic, it’s hard to argue that interest rates had any effect at all on Johnson & Johnson’s stock price valuation.

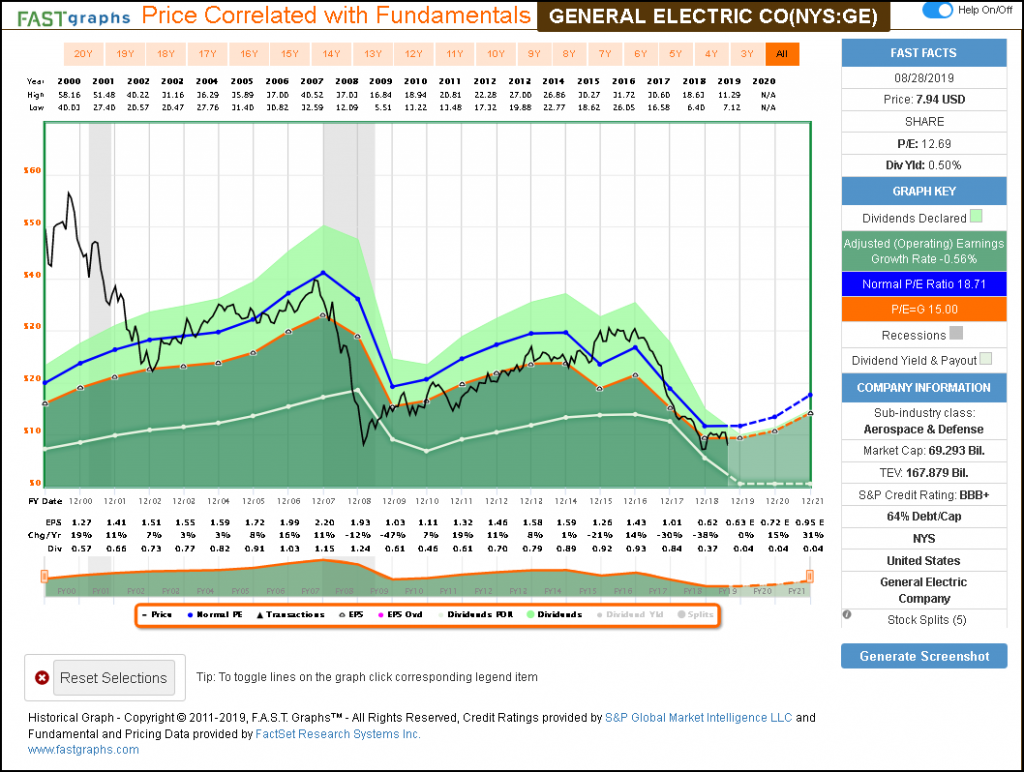

Turning to General Electric, my example of a company with less-than-stellar operating performance and history, we see extremely high valuation coming into the 2001 recession then we see price following earnings up to and through the Great Recession, and this has continued to current time.

Now, we might argue that politics played a crucial role here because of loose lending practices which are primarily attributed to instigating the Great Recession. Add the fact that General Electric moved away from being a premier appliance manufacturer to a financial services company, and we can argue that poor management decisions were more relevant than politics. Nevertheless, General Electric’s results were directly proportionate to how General Electric performed as a business.

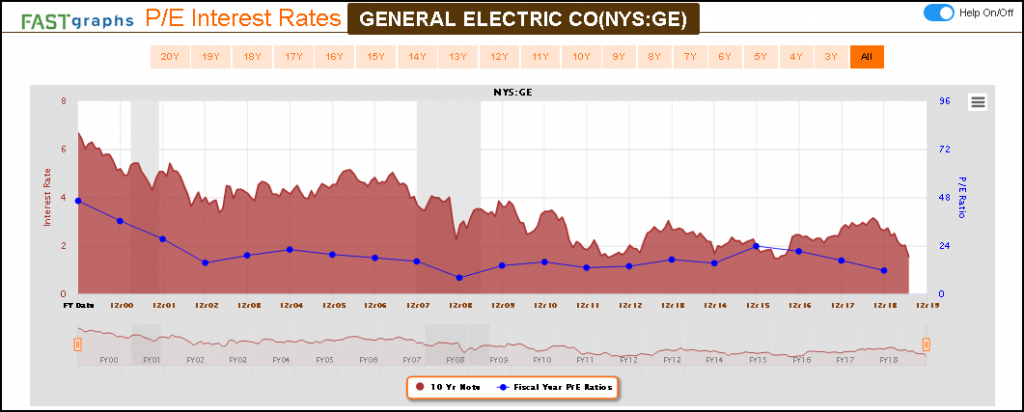

Regarding interest rates, in a similar fashion that we saw with Johnson & Johnson, General Electric’s valuation fell simultaneously with interest rates for most of the timeframe. However, with what we saw with the previous graph, valuation and operating results were more significant and relevant than politics, or interest rates.

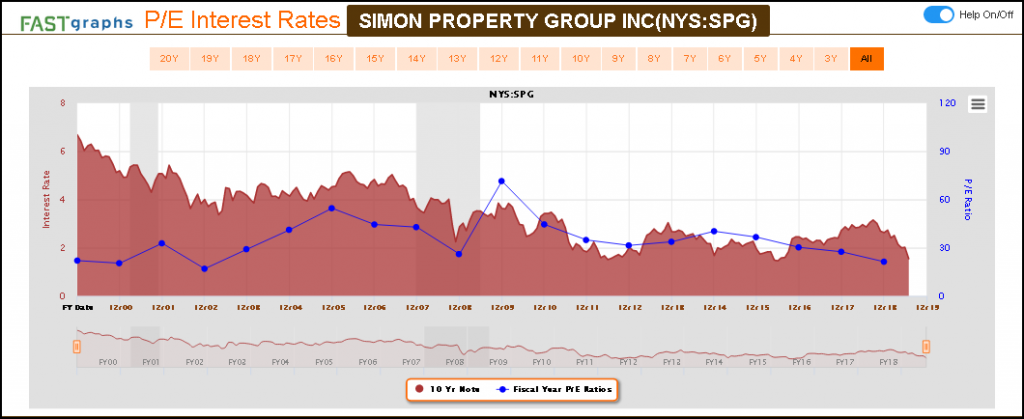

Next I would like to evaluate Simon Property Group, one of the most highly regarded and high-quality REITs. Once again, conventional wisdom suggests that REITs are very sensitive to interest rates. However, from the below graph we discover that Simon performed well as an operating entity in various interest rate and political environments. But most importantly, we also see several examples of how valuation was more relevant than politics or interest rates as it relates to shareholder returns and success.

When we actually examine Simon’s valuation relative to interest rates, we at first see the classic conventional wisdom relationship discussed above. From calendar year 2000 through calendar year 2005, Simon’s valuation moved inversely to interest rates. As interest rates were falling, Simon’s valuation trended upwards.

However, when we look at Simon post the Great Recession, we once again see the unconventional situation where both valuations and interest rates fell in tandem. Nevertheless, if we go back and examine the valuation of Simon over this timeframe, we discover that this high-quality REIT was generally overvalued. Consequently, the benefit of falling interest rates was counteracted by the excessive valuation the REIT was trading at over this timeframe.

The S&P 500: A FAST Graphs™ Video Analysis

In the following video I provide specific evidence of the assertions I presented with this article. I will clearly illustrate how unique different companies are that make up the market (S&P 500) truly are. I will also provide greater insights into the relevance of politics and interest rates in comparison to operating results and valuation.

Summary and Conclusions

My dear mother always taught me – mind your own business. Little did she know that her lesson also applies to my investing career. I never really worry about what the market is likely to do, what the Federal Reserve is likely to do, who’s the President or which political party is in charge – or any other broad macro concept. Instead, I mind my owned businesses. I pay careful attention to the specific businesses I own, their valuations and prospects for future growth. I built my portfolio one company at a time, and I manage my portfolio one company at a time. To me this really simplifies the investment process and offers the side effect of less to worry about.

Disclosure: Long JNJ,SPG

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits