An article on when to sell a stock would not be complete without some discussion about what I consider to be the worst reason to sell a stock. Ironically, this reason may be the one that is most commonly implemented by investors. Personally, I will rarely, if ever, sell a stock just because the price has fallen. If I’ve done my initial homework correctly, then a falling stock price would represent a great buying opportunity, not a rational reason to sell. If I buy a stock at $20 per share that I believe is worth at least $20 per share or more, then it seems logical to me that I should love it at $15 or even $10 per share. Of course, this is only true if the fundamentals remain solidly intact.

I believe that if fundamentals remain strong, a price drop is more likely to initiate a buy decision than it is a sell decision. I believe this is important, because in my anecdotal experience most investors are inclined to sell a stock if the price drops below the price they paid. Admittedly, averaging down doesn’t always work out as expected. However, I have seen more people take unnecessary losses by selling a perfectly good stock than I have seen people losing more from averaging down into a sound and growing business.

Avoid Selling Just Because the Price Drops: Cognizant Technology Solutions a Textbook Example

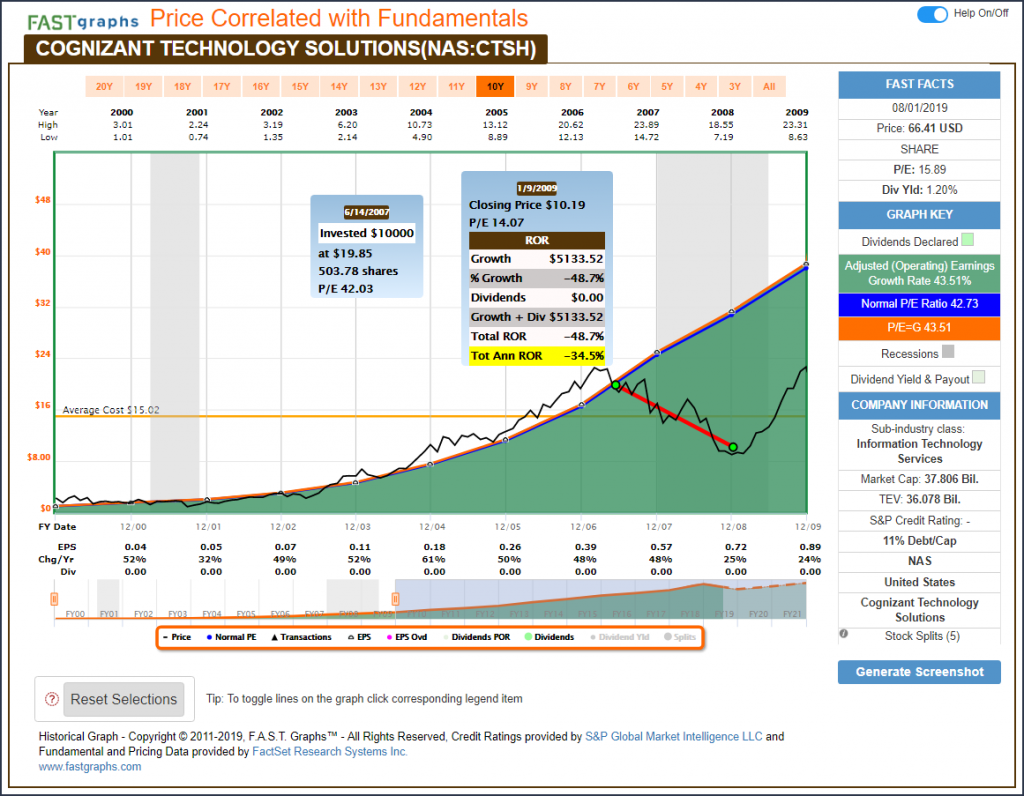

In June 2007, prior to the Great Recession, I initiated a position in the growth stock Cognizant Technology Solutions (CTSH) for my total return portfolios. Note by the green dot on the graph that I purchased the company at a P/E ratio of 42, which indicated fair value based on its earnings growth rate of 43.5% (P/E ratio equal to earnings growth rate). From that point forward, the stock went on a freefall and by January 2009 right in the throes of the Great Recession, the price of this great growth stock was nearly cut in half from $19.85 when it was first purchased to $10.19.

However, as I stated in the introduction, since I loved the stock at $20, I was crazy about it at $10. Therefore, considering that earnings continued to grow at a very high rate over this timeframe, instead of panicking, I enthusiastically doubled down on the stock. Note by doing so, I lowered my cost basis from $19.85 to $15.02. Although my timing actually turned out to be almost perfect, it was actually a combination of luck and good analysis.

The lucky part was simply fortuitous timing that was technically unpredictable. In other words, I didn’t know the stock had bottomed out, but my analysis suggested that fundamentals continue to be strong and therefore I saw the stock available at ½ off sale.

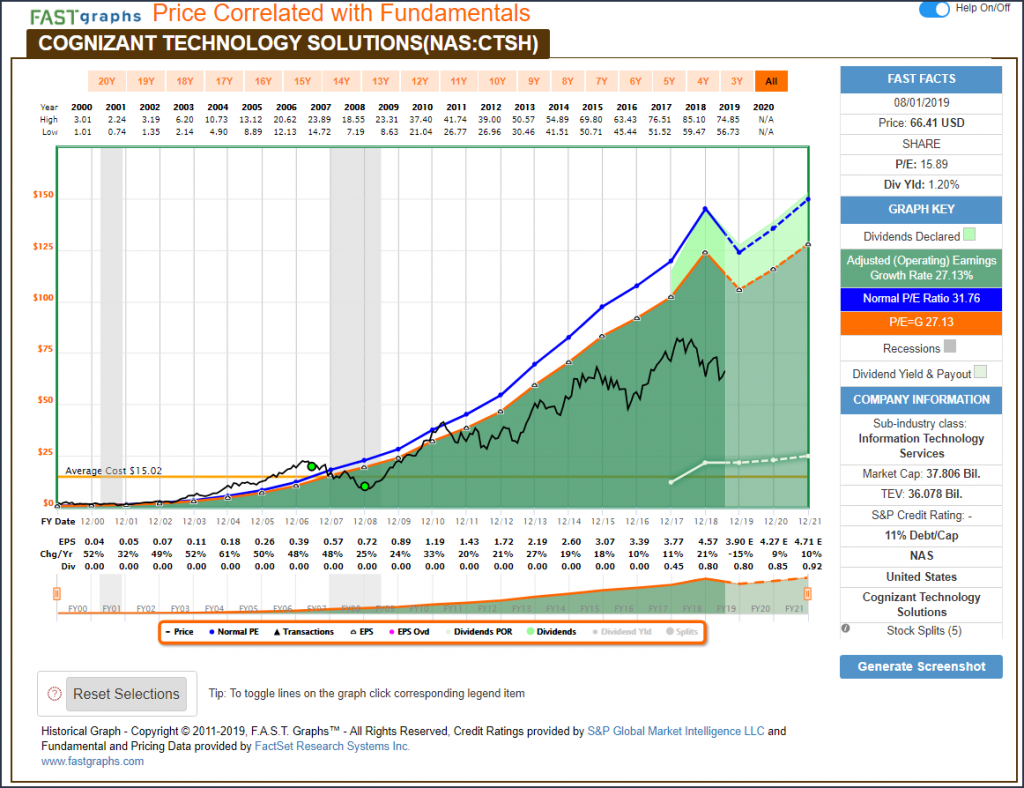

As you can clearly see, the company’s earnings growth continued and the stock price followed. Consequently, this holding has turned out to be one of the best performing stocks we have ever invested in. Imagine the cost to us if we had panicked and sold out just because the price had dropped even though fundamentals were as strong as ever. Therefore, I believe the worst reason to sell is because the price drops. But once again, that statement is predicated on the fundamentals remaining strong – or at least intact. In the long run, fundamentals matter more than price volatility.

When reviewing the transactions it becomes clear that the decision to buy more Cognizant was a lot smarter than had we panicked and sold out. Once again, as I did in part 1 A of this article series, this is a real-life account and real-life results of one of our clients in Cognizant Technologies.

FAST Graphs Analyze Out Loud Video Cognizant Technology Solutions

Summary and Conclusions

Consequently, for the above reasons and more, I personally eschew strategies based exclusively on short-term price action. I especially shun mechanical strategies such as stop losses. For starters, I believe it is never wise or prudent to sell an asset for less than its True Worth™. Therefore, if I bought a stock at its true fundamental value or less, I would hardly be motivated to let someone take it from me at a lower price. I feel this way because I have great confidence in the notion that a stock gets its value from the earnings and cash flows that it generates on behalf of its stakeholders.

Moreover, I believe that True Worth™ is something that the discerning investor can calculate within a reasonable range of accuracy. In contrast, guessing what short-term price action might or might not do is simply too unpredictable. To me, volatility is simply the price investors must be willing to pay for the liquidity that owning a common stock provides. Therefore, when I see one of my wonderful businesses selling for less than my calculation of its True Worth™ I do not see this as a loss, instead I at first see it as a currently, and temporarily, illiquid holding. But more importantly, I see this as a great opportunity to buy more at a better price and valuation.

In summary, I believe it is never wise to sell a great business for less than it is truly worth or simply react to short-term price action. We must always remember that the stock market is an auction. Therefore, over the short run, emotions (sentiment) tend to rule. However, in the long run fundamentals matter most. Therefore, I trust fundamentals over emotions. Consequently, I believe that one of the worst reasons to sell a stock is simply because the price fell. If the fundamentals are deteriorating, then I agree the stock should be sold. Furthermore, if the stock is dramatically overvalued it might also be wise to sell. However, if the stock is fairly valued, or even undervalued, then by selling you are simply allowing others to take advantage of your emotional reaction.

Disclosure: Long CTSH.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.