Answering the Question: When to Sell a Stock-Part 1A

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIntroduction

I’m going to start this article with the same opening statement that I utilized in two previous articles I wrote on knowing when to sell a stock. The most common complaint that I have heard from investors over my 49+ years in the financial services industry is as follows: “Everyone wants to tell me what to buy and when, but no one ever tells me when to sell.” Consequently, it seems to me that whether you are a novice investor or a grizzled old veteran, the decision as to when to sell a stock is considered one of the most difficult decisions investors must make.

Therefore, not only do I consider this a legitimate complaint, I also consider it an extremely important investing principle that investors constantly face and must deal with. Knowing when it’s the appropriate time to sell a stock can be a very challenging task. But perhaps most importantly, the prudent investor must simultaneously recognize and accept that it can rarely, if ever, be done with perfect precision. In other words, as another old saying goes: “they do not ring a bell at market tops or bottoms on Wall Street.” Consequently, we are prudent when we accept that the best that an investor can expect to accomplish is to make sound and rational sell decisions.

However, before I go any farther, I want to clarify my position. This article on when to sell a stock is based on how I believe a rational prudent long-term investor might consider behaving. In other words, this article may not be of value to active traders or speculators. Personally, my investment philosophy is based on the long-term ownership of attractive businesses that I want to be a long-term shareholder partner of. Consequently, I have little or no experience that might be of value to the more active trader or speculator. Therefore, I also have little knowledge about how that type of individual might or should rationally behave. For that reason, I will offer no comments or advice on short-term trading which is something that I know very little about.

When To Sell a Stock?

I have long held that equity investors are faced with the challenge of correctly answering three important questions:

- What to invest in? I believe the individual security selection is vital to long-term success.

- When to invest? I believe you must not pay too much for even the best companies.

- When to sell? Even the best choices can, from time to time, become dangerously overvalued or experience a permanent deterioration of their fundamentals.

I have written extensively in the past about correctly answering the first two questions. However, I must admit to being somewhat negligent regarding answering the important question, number 3. Part of my negligence stems from the fact that I tend to agree with legendary investor Philip Fisher and what he wrote in his great book “Common Stocks and Uncommon Profits.” In chapter 6 in his book, (which I enthusiastically endorse to anyone who has money invested in common stocks), was simply titled: When to Sell and When Not To. I quote the last sentence of chapter 6 as follows: “If the job has been correctly done when a common stock is purchased, the time to sell it is-almost never.”

I consider Philip Fisher one of my most revered mentors even though I never met him personally. However, I feel that I learned as much or more from reading him than any other teacher I have come across. Consequently, when he states that the best time to sell is almost never, I take his words to heart. Therefore, my first and perhaps best advice regarding when to sell a stock is to engage in this activity as little and as seldom as possible. This is aligned with one of my favorite old adages: “a portfolio is like a bar soap, the more you handle it the smaller it gets.”

Nevertheless, and with great reverence to my teacher Phil Fisher, I have developed a selling philosophy that may be a little less strict than Philip Fisher would agree with, but one that has served me well over the years. Therefore, I have two primary reasons for why I might consider selling a wonderful business that I have thoroughly researched and invested in. However, I also have a few secondary reasons, but they are not investment related. Let’s look at the secondary reasons first because they are easy and straightforward.

My Secondary Reasons for Selling A Stock

There can be many good reasons why an investor might decide to sell common stocks that are not investment related. For example, it might be to fund an important purchase such as building or buying a new home, or funding a child’s education, or to pay for a catastrophic illness, etc. However, since these reasons are not investment related, they are not the subject matter of this article. On the other hand, I do believe that if the investor needing money for a good reason is required to sell some of their common stocks, I do recommend that considerations about valuation and portfolio balance be included in their decision process.

Furthermore, the issues regarding maintaining balance in your equity portfolio (which is investment related) can represent another secondary reason for selling a common stock. This could be the subject matter of a separate article in its own right. Nevertheless, to summarize, if one position performs so well that it becomes a disproportionate portion of your overall portfolio, you might trim in order to keep your portfolio balanced. The stocks relative valuation would have a bearing on precisely how much, if any, you should trim.

(Note: the following examples are intended to illustrate the important principle of rebalancing a portfolio. Although these examples are real-life, they are not offered to boast. Because frankly, I have also owned some real duds.)

How Apple Inc. Became an Overweight

The following example is on Apple Inc. (AAPL), one of several companies that I’ve been required to trim because its performance was so good that it became a disproportionate overweight of client portfolios. Utilizing the calculator function of FAST Graphs, you can see that Apple increased almost six-fold in value since it was purchased in 2010.

The following transaction summary is on an actual portfolio that we manage. On May 14, 2010 we purchased 7000 shares of Apple at a cost of $253,990. On June 28, 2019, Apple became a serious overweight, therefore, in order to balance the Apple position, we sold 3000 shares for $593,760. Therefore, we were de-risking the portfolio by taking more than twice our original investment out of the position. Nevertheless, we still hold shares worth more than 3 times our original investment. Most importantly, this was not a sale that was initiated because we believed that Apple was dangerously overvalued, therefore, it continues to be a long-term hold.

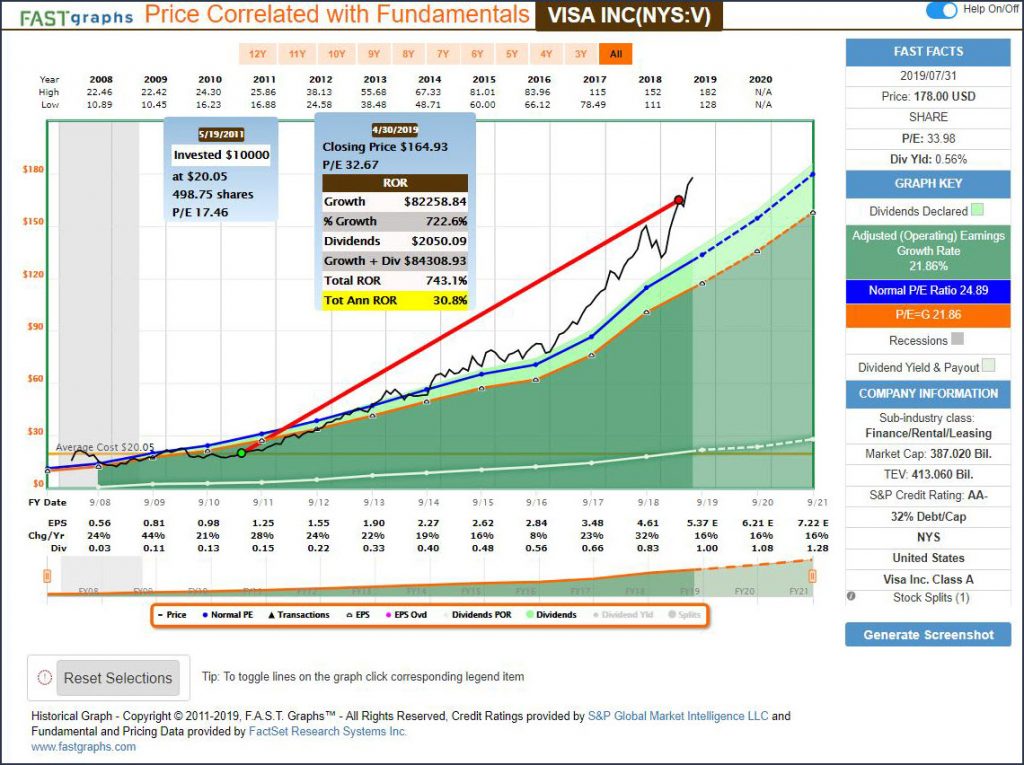

Visa Inc. An Overweight and Dangerously Overvalued Trim

My second example is on Visa Inc. (V) which represents another portfolio holding from a different client account that has been trimmed in order to balance the portfolio. However, with this example it is also on our “sell watch list” as a great business that we believe has entered dangerous overvaluation territory. Consequently, we are prudently trimming while simultaneously not ignoring the momentum that this company continues to enjoy.

Nevertheless, we see that Visa was purchased when its valuation was exceptionally attractive. Consequently, to me at least, the good news bad news is that the company has done extremely well but its price has done even better. Therefore, we not only trimmed to balance the portfolio, we also are trimming based on our belief that Visa is now dangerously overvalued. I will be discussing dangerous overvaluation in more detail later in the article. However, this is a classic example of how even though our decision was prudent, our timing was as would be expected not perfect.

Dangerous Overvaluation

In my previous article published on December 18, 2013 titled “How Do I Know When To Sell A Stock” I presented dangerous overvaluation as my second primary reason for selling a stock. However, I attempted to make a distinction between simple or moderate overvaluation and dangerous overvaluation. Also, many times in the past, I discussed fair value from the perspective of making an initial purchase. Although I will not buy a stock that I consider even moderately overvalued, moderate overvaluation will not automatically initiate a sell. I make a distinction between a buy, sell or hold decision.

Dangerous overvaluation on the other hand is an entirely different matter. Investors should always recognize that Mr. Market can be quite irrational at times. The key is recognizing extremely irrational overvaluation when it is occurring.

Consequently, my second primary reason for selling a stock is when valuation becomes extreme enough to be what I consider dangerous. The idea that overvaluation has become dangerous is an important distinction. The prudent long-term holder of blue-chip companies, especially dividend paying blue chips, must accept that short-term volatility with stock price is a certainty.

As a result, they should also be willing to accept the reality that moderate overvaluation will often manifest. However, since the exact timing and duration is unpredictable, I suggest that the prudent long-term investor be willing to ride these moderate overvaluation situations out. This is especially relevant to blue-chip dividend paying stocks possessing a long legacy of increasing their dividends each year.

Moreover, the concept of fair value is not as precise a calculation as many would like it to be. In truth, there are often many shades of gray that prudent investors would be wise to consider. For example, there are certain companies that are often afforded a quality premium valuation by the market. This piece of information might be given consideration by some investors and rejected by others. At the end of the day, whether it’s wise to pay a quality premium for a given company comes down to the individual investor’s own judgments.

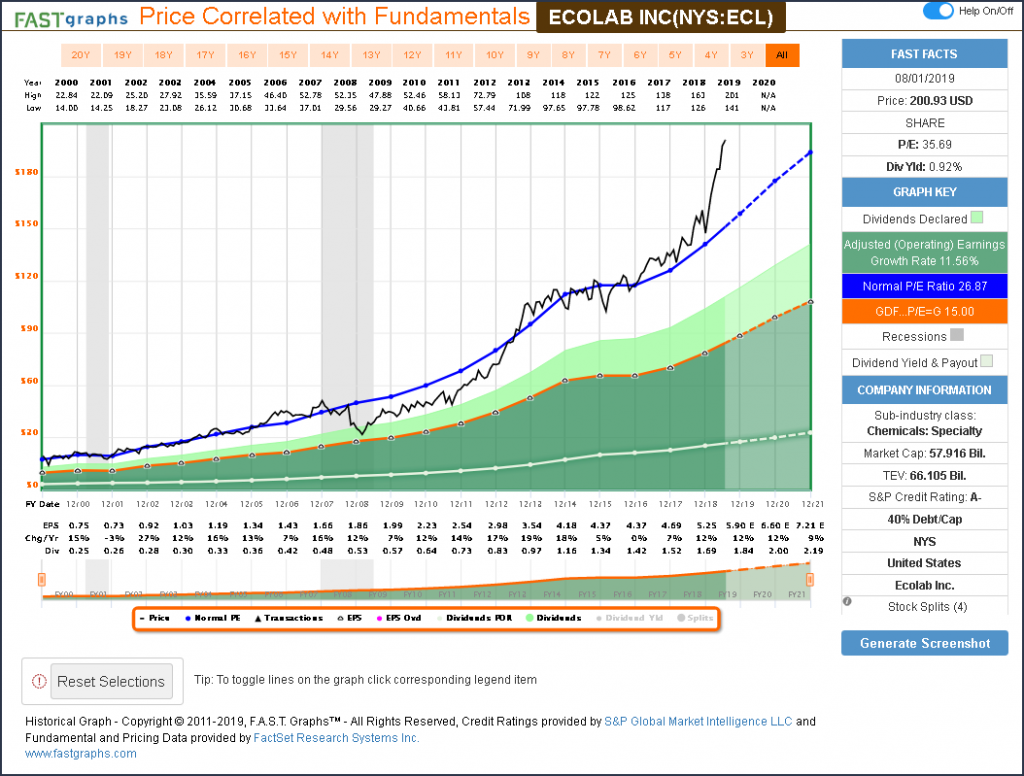

Ecolab Inc.: A Quality Premium Valuation Case in Point

The following earnings and price correlated graph on Ecolab (ECL) clearly illustrates that the market has chronically and consistently applied a premium P/E ratio multiple in excess of 25 (the blue P/E ratio valuation reference line on the graph is a multiple of 26.87). Nevertheless, it should also be clear that Ecolab’s stock price has clearly disconnected from even that historically normal rich valuation.

Nevertheless, based on what the graph above reveals, we see clear evidence of the historical quality premium valuation referenced above. However, the real question is what do we do with this information, or more relevantly, how do we interpret it in order to make a sound buy, sell or hold decision? This is where the “tool to think with” concept or individual judgment comes into play.

One investor might conclude that it makes sense to pay a quality premium when investing in Ecolab based on the evidence revealed. Conversely, another investor who’s more of a stickler for only being willing to invest when fair value exists (such as yours truly) might reject paying a quality premium. Nevertheless, it is clear from the graphical evidence that paying a quality premium for the blue-chip Ecolab has not worked out so badly. However, let me remind you that current valuation is far above historical norms.

My own personal definition of “dangerous overvaluation” is simple and straightforward. Once a company’s market price deviates from my calculation of True Worth™ to the magnitude that it is more than two years ahead of its earnings justified price, I will flag the company as a potential sell. To be clear, I do not mechanically or immediately sell it when this occurs. Instead, I put it on a potential sell list and monitor the stock very closely.

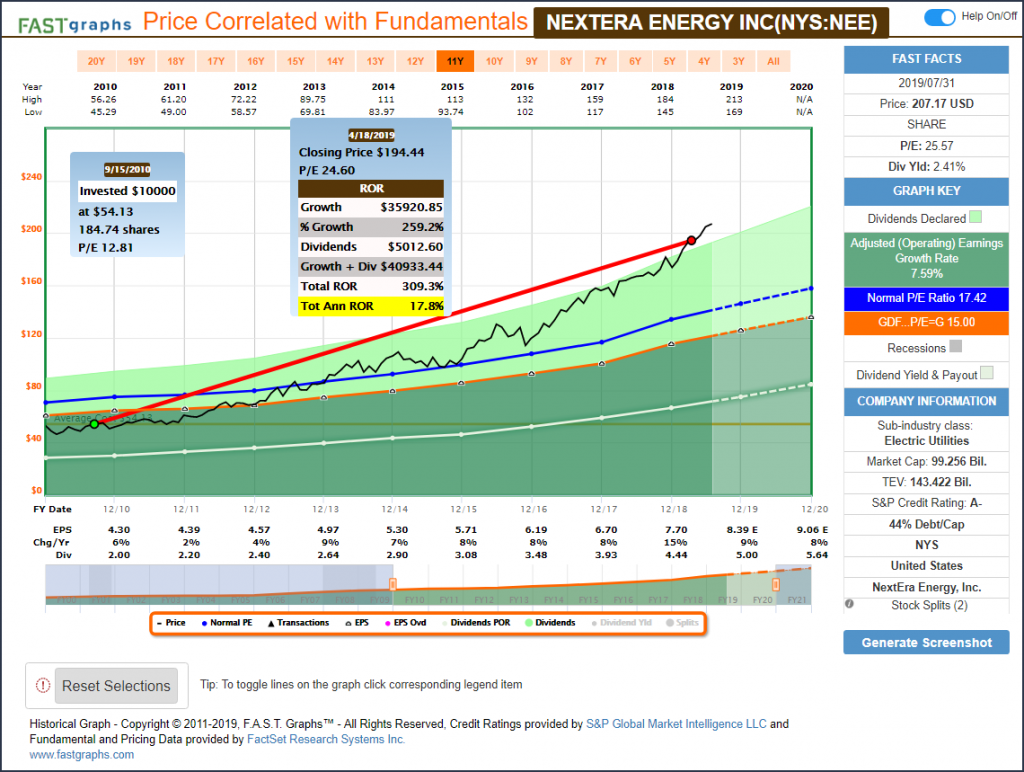

NextEra Energy More Than 3 Years Ahead of Fair Valuation

The following forecasting calculator on NextEra Energy (NEE) shows that the company’s current valuation is more than three years ahead of the earnings justified fair value calculation (the dark orange line on the graph). Consequently, the company has been placed on our “sell watch list” since August 2017.

However, on April 18, 2019 we made the decision to sell out of our holding. Once again, we obviously did not sell at a perfect top. On the other hand, we are totally confident that our decision to sell was both prudent and sound. Furthermore, we ended up making significantly more profit and a much higher annualized rate of return than we originally anticipated when we first purchased the stock even though we considered it significantly undervalued at the time.

A Clear Perspective Of The Danger Of Overvaluation

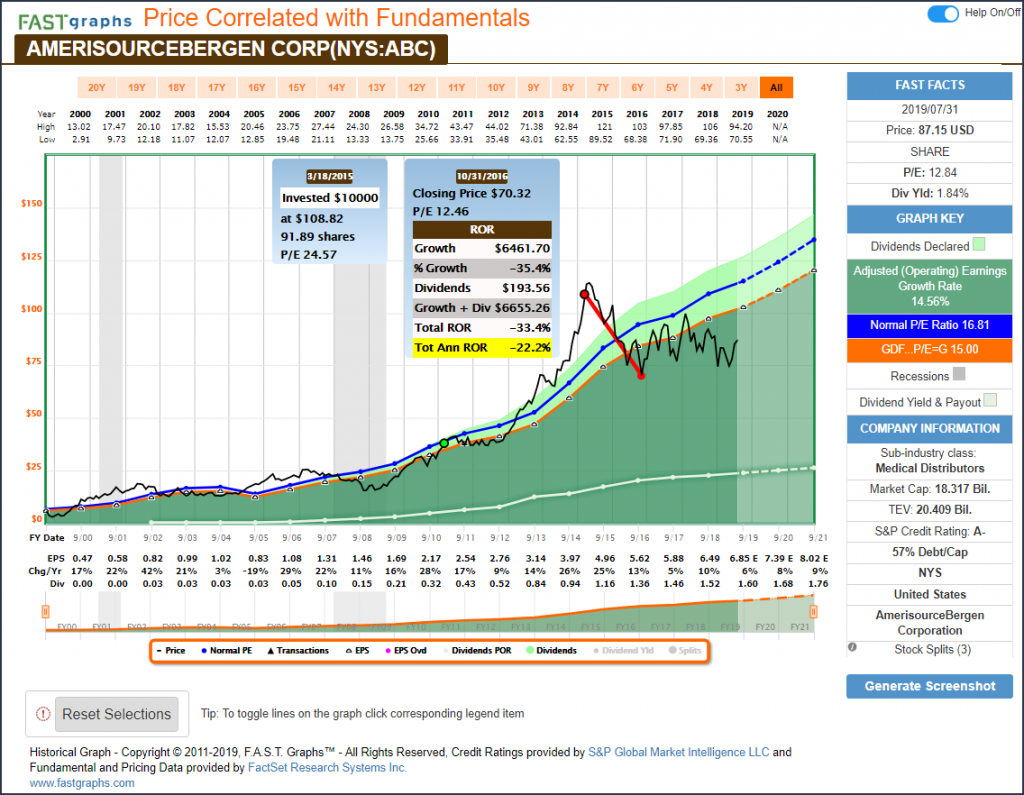

With these next three examples I am illustrating the mathematical reality of dangerous overvaluation under real-world conditions. These are three real-life over valuation sell decisions that we made in order to protect client capital. With each example, I have measured the impact of each of the stocks reverting to the mean when they were obviously significantly overvalued. My goal was to inform the reader of just how dangerous overvaluation could be with real mathematical results.

AmerisourceBergin (ABC)

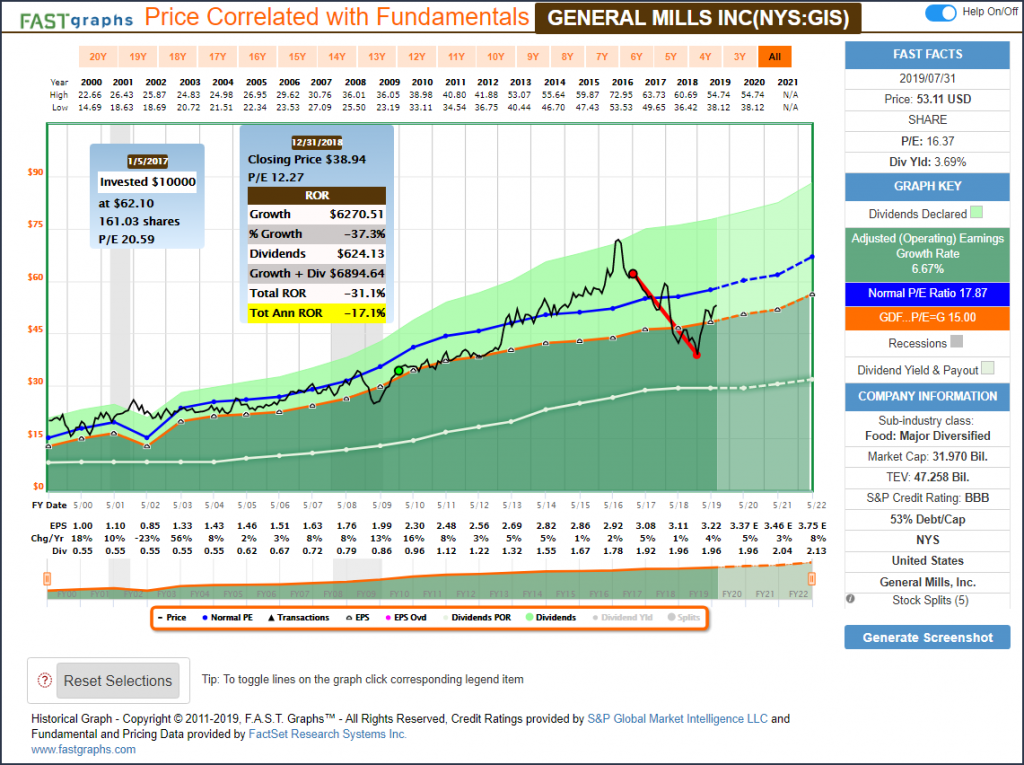

General Mills (GIS)

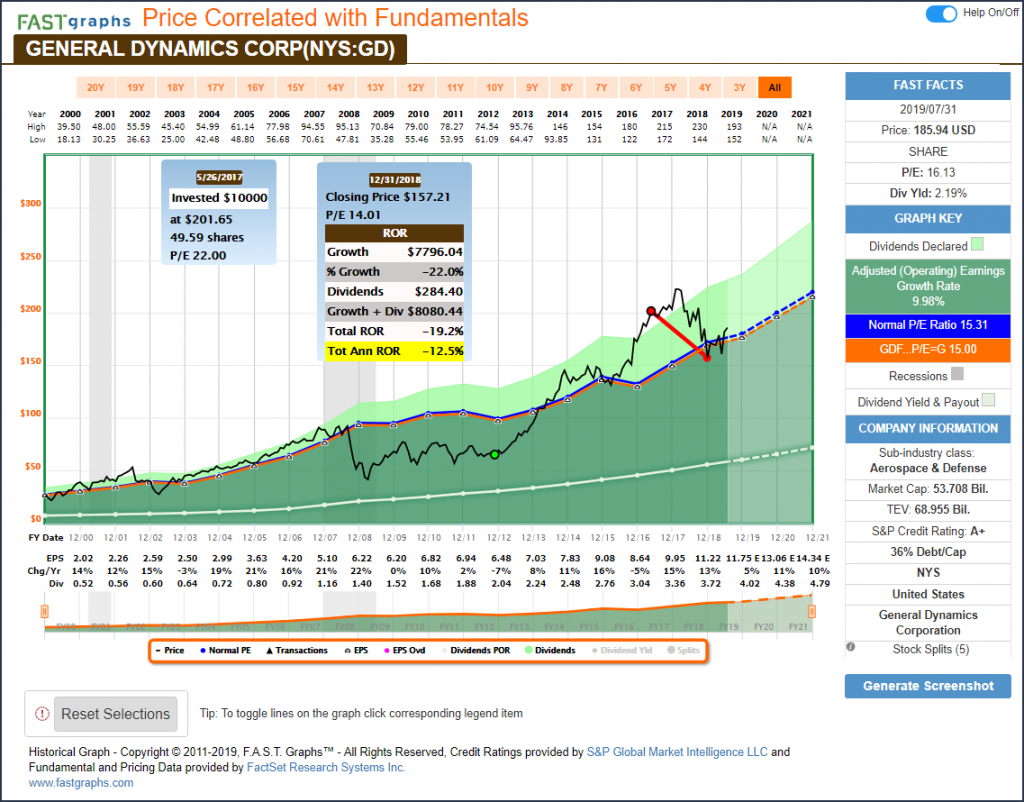

General Dynamics Corp (GD)

The bottom line is that dangerous overvaluation can result in dead money and/or negative returns over extended periods of time. Furthermore, dangerous overvaluation represents an obvious mistake that can and should be avoided. On the other hand, since a precise calculation of fair value is impossible, moderate over valuation, full valuation or slight overvaluation can and should be ignored. Finally, each of the companies represented in the above examples are currently on my dividend growth stock buy lists.

FAST Graph analyze Out Loud Video Detailing The Risk Of Dangerous Overvaluation

With this analyze out loud video I will provide a more comprehensive look and analysis of what the risks of dangerous overvaluation really mean to investors.

Permanent Fundamental Deterioration

Moreover, as investors we are human, and being human means that we can make mistakes, and often we do. Consequently, my other primary reason for selling a stock is when I recognize that I made a mistake. Translated into English, this means that the fundamental performance that I expected didn’t happen. Stated differently again, the fundamentals I expected deteriorated to the extent that the company was no longer an excellent investment.

Comprehensive research and due diligence go a long way towards keeping mistakes at a minimum. Nevertheless, mistakes will be made. The mistake I’m referring to here is investing in the wrong company. Sometimes what once was the right company suddenly becomes the wrong company. This is what I refer to as permanent fundamental deterioration. The respected investor Marty Whitman of the Third Avenue Value Fund put it this way:

“Unrealized Market Depreciation occurs when the market price of a publicly traded security declines. Permanent impairment of capital occurs when the Fundamental values of a business are dissipated with the consequent long-term adverse consequences.”

For that reason, my primary reason for selling a stock is once I have determined that a permanent deterioration in the company’s fundamentals is potentially leading to a permanent impairment of capital. The classic metaphor goes something like this: you wouldn’t want to invest in even the best buggy whip manufacturer after Henry Ford came along. Of course, there are other reasons for fundamental deterioration than creative destruction. But my point is, if you come to believe that a company no longer possesses the salient fundamental characteristics that you originally believed, it is time to sell.

Fortunately, if you’ve done your homework correctly in the first place, this primary reason for selling only comes around rarely, if ever. On the other hand, I believe it is an integral and critical part of a proper due diligence effort.

To summarize the rationale underpinning fundamental deterioration as a primary reason to sell, I will again turn to Philip Fisher and his book “Common Stocks And Uncommon Profits” as follows:

“This is when a mistake has been made in the original purchase and it becomes increasingly clear that the factual background of the particular company is, by a significant margin, less favorable than originally believed. The proper handling of this type of situation is largely a matter of emotional self-control. To some degree it also depends upon the investor’s ability to be honest with himself.”

When a company’s fundamentals are truly deteriorating, it becomes a critical mistake to expect the company’s price to go back to what you originally paid for it so you can break even. When this is happening, your first loss is usually your best loss. Regardless, once you are absolutely certain that a mistake has been made, my suggestion is to immediately cut your future losses and get out.

Teva Pharmaceutical Industries: How I Almost Followed My Own Advice But Didn’t

In January 2005 I confidently purchased Teva Pharmaceutical Industries (TEVA) for client accounts. On July 29, 2010, I even more confidently added to my positions because even though my second purchase price was higher, I believed the valuation opportunity was more compelling. Furthermore, fundamentals over the next 2 or 3 years told me that my decisions were correct. However, earnings growth weakened in 2013, moderately recovered in 2014 and then weakened again in 2015. At this point, my confidence in the company waned and I sold half my position. This was my mistake, because I should have sold it all.

Fundamentals continued to get worse, but I ignored the signs. Finally, in October 2018 I liquidated all remaining shares. At the end of the day, I came close to breaking even on the combination of capital appreciation and dividend income. Nevertheless, my almost 8-year run with the company proved to be a rather poor investment. Lesson learned.

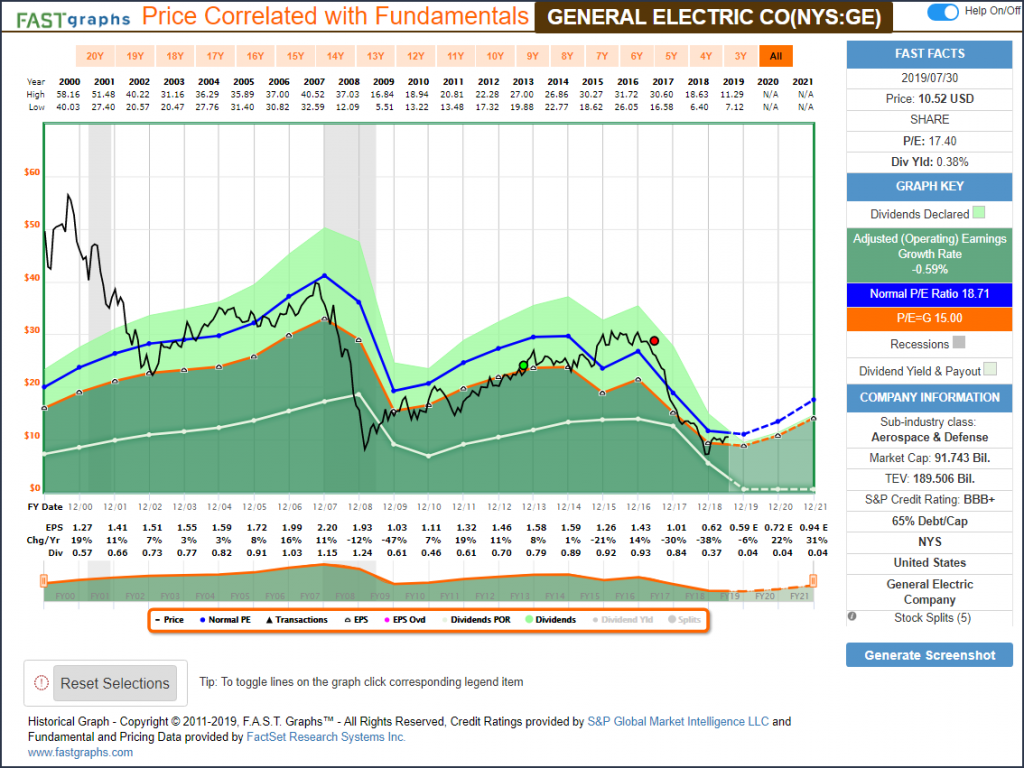

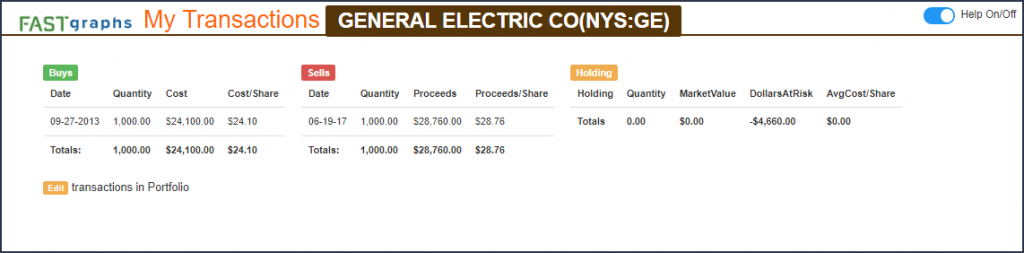

General Electric Company: Another Mistake But I Did A Little Better

My General Electric (GE) experience provides another excellent, and for me and my clients, better example of selling once fundamentals deteriorate. I originally purchased the stock at fair value at the time, watched earnings growth began to falter, experienced a modest dividend cut which motivated me to get out. Although we did just a little better than break even over the 3+ years that we owned General Electric, we thankfully avoided a huge 75% collapse that occurred after we sold from June 2017 to November 30, 2018. Clearly, General Electric represents a clear and undeniable real-life historical example of the dangers of fundamental deterioration.

The Power and Protection of Fair Value

Personally, I believe the sell decision is difficult for most investors because of the natural emotional response that motivates them to feel they must do something, especially during turbulent times. In other words, when they are experiencing volatility within their portfolio holdings, they feel a strong desire or even a need to act. However, more often than not, the best action for investors during volatile markets is to sit tight and do nothing. But the innate “fight or flight response” that is embedded in virtually every living thing is often impossible to resist.

However, if we check in with some of the best investment minds that ever walked the planet, we find that they have disciplined themselves to take a different approach. For example, in the 1996 Berkshire Hathaway Annual Report Warren Buffett stated: “inactivity strikes us as intelligent behavior.”

A quote I included earlier in the article is worth repeating: from legendary investor Philip Fisher’s excellent book “Common Stocks and Uncommon Profits” in chapter 6 titled “When to Sell and When Not To” Philip Fisher gave us this nugget of wisdom: “If the job has been correctly done when a common stock is purchased, the time to sell it is-almost never.”

Both legendary investors are suggesting avoiding the temptation to do something because they believe that the best course of action is usually to sit tight. At this point, it’s important to not overlook the importance of doing the job correctly when the stock is initially purchased. Positioning yourself as a shareholder/owner of an excellent business purchased at a fair valuation is a tried-and-true successful investing strategy.

To my way of thinking, doing the job right implies identifying a great business through research and due diligence and then exercising the discipline to only purchase it when valuation is sound, or better yet, at a bargain level. Doing this puts you in the position to be able to walk through turbulent waters with a minimum of risk to your long-term financial future. Of course, this statement is predicated on the fundamentals of the business continuing to be strong.

However, in addition to doing the job right in the first place, it’s also important that investors possess a realistic understanding of how stock prices work in an auction market. In financial parlance, stock charts are often referred to as “mountain charts.” The reason is because just like a mountain, a stock price chart that is ascending upward will contain numerous peaks and valleys in between.

Consequently, I have coined a metaphor suggesting that great investors and great mountain climbers share a common understanding. Both recognize and accept the reality that in order to get to the highest peaks you must be willing to traverse the occasional valleys along the way. Therefore, in order to be a successful long-term investor, you must accept the unavoidable reality that there will be short-term periods where your performance will be negative. Even more importantly, the precise timing of these periods of negative performance are unpredictable.

However, there is a caveat with this allegory that relates to doing the job right in the first-place part. Once you have been climbing the mountain for a while and are looking for the next higher peaks, it’s important to know that you’re on the right mountain. However, it is one thing to walk down a valley while on your way to a next higher peak, and it’s another thing altogether to walk all the way back down to the bottom because you’re on the wrong mountain.

Summary

In this and previous articles I wrote discussing when to sell a stock, I reviewed several aspects that were not specifically related to investing decisions. For example, I talked about selling stocks to fund an important purchase such as paying for a child’s education, etc. I also talked about selling a stock in order to rebalance your portfolio or to take advantage of an uncommon opportunity that you might have come across. However, I have recently been asked about the sell decision from purely an investment perspective. Therefore, with this article, I tried to present my views on selling a stock purely as an investment decision.

However, if people are looking for advice on the perfect time to sell a stock, I respectfully submit that no such advice exists. You can never – and should never – expect to sell a stock with perfect timing. In fact, I would suggest that the best you can hope for is to make a prudent and sound decision. What I’m suggesting is that more often than not if you do sell an overvalued stock that has momentum, it is likely to continue rising for a period of time after it is sold. Overvaluation often occurs as a result of popularity that is unsupported by sound fundamentals.

This reality often reminds me of a rather profound definition of appreciation that a colleague once shared with me. He asked me if I knew what appreciation was, and of course I gave him the classic definition from the financial lexicon. However, he corrected me by offering that the real definition of appreciation was when the other person appreciated what you owned more than you did. So be careful, when a stock is popular, because it’s important to come to grips with the fact that someone else out there might appreciate it more than you do.

As a rule, stocks become overvalued because they become popular – or hot, as some people like to say. This type of price action is based on sentiment, and sentiment is virtually unquantifiable. You can make guesses, but you can never predict with perfect accuracy how high is up, or how low is low for that matter.

Conclusions

As I indicated throughout this article, there are valid reasons to sell a stock. However, these reasons are typically only relevant under extreme conditions. I adhere to the investment strategy of being a long-term owner of a wonderful business purchased at a sound valuation. Long-term oriented investors recognize that time in the investment is more profitable than attempting to time your investments. Buy-and-hold is a proven strategy and produces solid long-term results. However, at times it requires patience and courage to implement the strategy successfully.

So in closing, I submit that if you’ve done your homework correctly, that the best time to sell a good stock is never. On the other hand, like all rules, there are always exceptions. This especially applies during aberrantly high or extraordinary bull markets like the one we have been in since the Great Recession. As the old saying goes, extraordinary times require extraordinary measures. Dangerously excessive overvaluation is a classic example of an extraordinary event. Therefore, it logically requires the extraordinary measure of selling to protect your future results.

And a permanent deterioration of business fundamentals is another extraordinary event that requires action. But at the end of the day, it’s important to fight the temptation of being too active with your portfolios. Once again, as the old Wall Street adage goes: “a portfolio is like a bar soap, the more you handle it, the smaller it gets.” Consequently, my personal approach to investing in a stock is to become a permanent shareholder partner in a fine business that I admire, and most importantly, that I rationally expect to meet my personal goals and objectives. As a result, I expect to own this business permanently, or at least for a very, very long time.

Finally, an article on when to sell would not be complete without discussing when not to sell. Therefore, I will be supplementing this article with a part B that discusses the worst time to sell a stock. Although everyone wants to know when to sell, I believe it is equally, if not even more, important to know when not to sell. Therefore, I will supplement this article with a follow-up Part 1B titled “The Worst Reasons to Sell A Stock.”

Disclosure: Long AAPL, V, TEVA, NEE, ABC, GIS, GD.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits