Nonfarm payrolls rose more than expected in the initial estimate for June. The news sent equity futures lower, bond yields higher, and reduced the odds of more aggressive Fed policy action later this month. However, the payroll data are noisy. The underlying trend is private-sector job growth is slower this year, but it’s still relatively strong. The job market is tightening further. Wage growth has remained moderate, but there is scope for improvement for those who had missed out on much of the economic recovery.

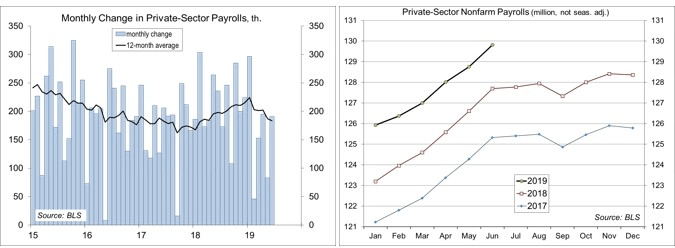

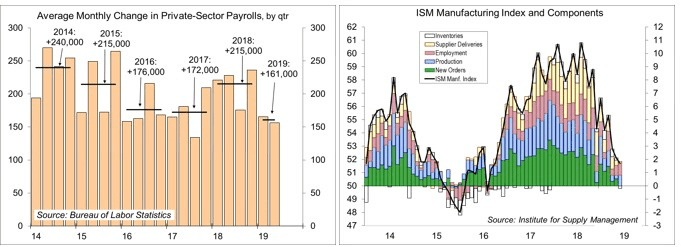

Nonfarm payrolls rose by 224,000 in the initial estimate for June, while the two previous months were revised a net 11,000 lower. The financial press and market participants react to the headline number, but these figures are choppy. There is statistical noise and seasonal adjustment is difficult. However, the noise will cancel itself out over time. That’s why one should never focus too much on any particular month and look at the underlying trend. That underlying trend has slowed this year. Private-sector payrolls averaged a 156,000 monthly gain in 2Q19 (vs. +165,000 in 1Q19 and +215,000 in 2018). We need less than 100,000 net new jobs per month to absorb new entrants into the labor force, so we’re still well beyond a long-term sustainable pace. Some of the slowing could reflect the tightness in job market conditions. Firms continue to report difficulties in finding qualified workers. However, slower job growth also reflects slower economic growth – and in turn, slower job growth would imply slower growth in consumer spending and in the overall economy.

Click here to enlarge

Prior to seasonal adjustment, job gains are strongest through the spring. The U.S. economy added 3.9 million jobs between January and June this year, down from 4.5 million over the same period last year and 4.1 million in 2017. Growth in manufacturing jobs has slowed this year, reflecting weakness in the factory sector. Bricks-and-mortar retail continued to lose jobs (department store jobs down 3.1% y/y), partly offset by job gains in couriers (+5.4%) and warehousing (+4.7%). Demographic changes (an aging population) continued to drive growth in healthcare jobs (+2.5% y/y).

Average hourly earnings rose 0.2% in June, up 3.1% y/y (the 2Q19 average was up 3.2% y/y, with production workers up 3.4%). Wage increases are not distributed evenly. Some workers are not keeping pace with inflation (cough, cough), while others are seeing stronger gains. Those at the low end of the income scale have seen the strongest gains more recently, but that comes from a very low level (entry-level wages were held down during the recession and gradual recovery).

In the Chicago Fed conference on monetary policy in early June, Fed officials heard from academics, but also from community leaders. In his June 19 press conference, Fed Chair Powell noted that there are “communities that are being brought into the benefits of this expansion that hadn’t been earlier.” He added, “we’re 10 years deep into this, and that’s something we heard quite a lot at the conference.” This, in turn, contributed to the FOMC’s focus on “sustaining the expansion,” according to Powell. Wage gains have been moderate overall, but a number of Fed officials would like to see further improvement at the lower end of the range.

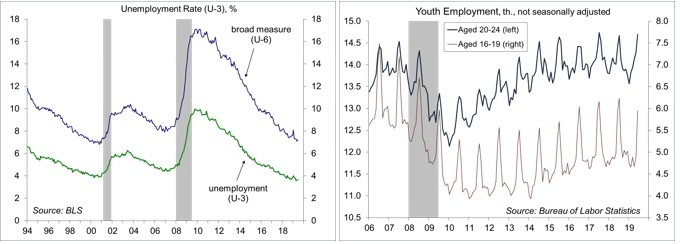

The unemployment rate edged up slightly to 3.7% in June (3.67% before rounding, vs. 3.620% in May) – not a statistically significant change (the unemployment rate is reported accurate to ±0.2%). The broader U-6 unemployment measure, which includes those working part time who would prefer full-time employment and those who have dropped out of the labor force but would take a job if offered, has continued to trend lower, consistent with tighter labor market conditions. The employment/population ratio, at 60.6% remains well below the prerecession level (62.7%), but the ratio for those aged 25-54 is back to where it was (79.7%).

Click here to enlarge

While the overall unemployment rate was little changed in June, the rate for young adults fell sharply (from 7.0% to 6.3%). Part of that may reflect seasonal adjustment issues, but the report showed a larger-than-usual seasonal gain in unadjusted jobs for young adults. That is consistent with tighter labor market conditions in general.

For the Fed, the June payroll figure is welcome news, but officials will focus on the underlying trend, which is moderate. Wage pressures do not appear to be too excessive, and there are further gains to be made for those at the lower end of the wage scale. Still, financial market participants had gotten ahead of the Fed in their monetary policy outlooks. While a July 30 rate cut is factored in, the market odds of a 50-bp move have evaporated. The June payroll figure is a lousy excuse to reset those expectations, but here we are. Look for Chair Powell to restate the Fed’s outlook in his monetary policy testimony to Congress this week.

Data Recap – Financial market participants have been focused largely on trade policy and the prospects for easier monetary policy. A trade truce between the U.S. and China was viewed positively, although it failed to resolve ongoing uncertainty. An upside surprise in the June nonfarm payroll figure dampened prospects for a Fed rate cut (a July 30 ease is still factored in, according the federal funds futures market, but the odds of a 50-bp move have fallen sharply).

The U.S. and China reached a Trade Truce following the G-20 meeting of President Trump and Chinese President Xi. The two agreed to restart trade negotiations. China will import more U.S. agricultural products. The U.S. will lift some restrictions on Huawei. Additional tariffs will not be imposed for the time being, but previous tariffs were not rolled back and trade policy uncertainty will continue.

The June Employment Report was mixed. Nonfarm payrolls rose by 224,000 in the initial estimate, with a net downward revision of 11,000 to the two previous months. Private-sector payrolls averaged a 156,000 monthly gain in 2Q19 (vs. 165,000 in 1Q19 and 215,000 in 2018). The unemployment rate edged up to 3.7%, although the increase was not statistically significant. Summer job gains for teenagers and young adults jumped. Average hourly earnings rose 0.2%, up 3.1% y/y.

Click here to enlarge

The ISM Manufacturing Index slipped to 51.7 in June, vs. 52.1 in May and 52.8 in April. Growth in new orders fell to 50.0. Production rose moderately. Employment growth edged higher. Order backlogs fell for the second consecutive month (not good). Input price pressures retreated. While the new orders figure, at 50.0, was at the breakeven level, it will subtract 0.11 from the Conference Board’s June Index of Leading Economic Indicators (due July 18).

The ISM Non-Manufacturing Index fell to 55.1 in June, vs. 56.9 in May and 55.5 in April. Growth in business activity and new orders slowed (still relatively strong). Employment growth slowed. Input price pressures picked up. The report noted that “comments from the respondents reflect mixed sentiment about business conditions and the overall economy,” with uncertainty due to trade and tariffs.

Click here to enlarge

Unit Motor Vehicle Sales edged down to a 17.3 million seasonally adjusted annual rate in June, vs. 17.4 million in May and 17.2 a year ago. The 2Q19 average was 17.0 million (annual rate), vs. 16.8 million in 1Q19 and 17.2 million in 2Q18, implying that vehicle sales will make a small addition to GDP growth.

The U.S. Trade Deficit widened to $55.5 billion in May, vs. $51.2 billion in April (revised from $50.8 billion). The data suggest that net exports will make a moderate subtraction from 2Q19 GDP growth (advance estimate due July 26).

The ADP Estimate of private-sector payrolls rose by 102,000 in the initial estimate for June, vs. +41,000 in May (revised from +27,000). Construction jobs fell. Weakness remained concentrated in small firms.

The Challenger Job-Cuts Report showed announced corporate layoff intentions falling to 41,977 in June (the figures are not seasonally adjusted and normally dip in the second quarter). The total for the first six months was the highest since 2009, up 35% from the first half of 2018, but still relatively low by historical standards.

Factory Orders fell 0.7% in May (-1.2% y/y), reflecting a 28.2% drop in civilian aircraft orders (-65.7% y/y). Durable goods orders fell 1.3% (unrevised from the previous week). Orders for nondefense capital goods ex-aircraft rose 0.5% (+1.4% y/y), with shipments up 0.6% (+4.0% y/y) – a 1.5% annual rate for the first two months of the quarter (vs. +4.0% in 1Q19). Unfilled orders fell further (0.5% overall and -0.2% ex-transportation) – not a good sign. Inventories rose 0.2% (durables +0.5%, nondurables -0.2% on lower petroleum prices).

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

More Fixed Income Topics >