“Overbought?”

The definition of the term “overbought” is:

“Overbought means an extended price move to the upside; oversold to the downside. When price reaches these extreme levels, a reversal is possible. The Relative Strength Index (RSI) can be used to confirm a reversal.”

And overbought was the question du jour here in Washington D.C. as in, “Hey Jeff, is the stock market overbought?” Our response has been, “Of course it is.” Indeed, since our bottoming call of June 3, 2019 the S&P 500 (SPX/2941.76) has leaped from its June 3 low of ~2729 to its June 21 intraday high of ~2964 in a relatively short 15 trading sessions. As Leon Tuey writes:

“As mentioned in my recent comments, every time the market stalls, anxiety sky rockets and each time the market drops 100 points or more, investors fear that it's the beginning of a bear market. Clearly, investors are still haunted by the last two bear markets and their fear has been reinforced by the two panics in 2018 and by the daily bombardment of ‘bad news’. This week, nervously, many are wondering why the market is stalling. Simple. The market is overbought, which is not surprising as from its December low to the June high, the S&P gained a whopping 26.32%. But as shown below, momentum peaked in April (and some in February). At the June high, however, momentum failed. Another reason is that bullish sentiment rose, but not excessively so. These reasons and this week's G20 meeting with all eyes glued on President Trump and Xi meeting on Saturday help kept investors at bay. Bears do not dare go short and investors are leery of committing new funds. Make no mistake, the pause is nothing more than a normal reaction to an overbought condition. Once rectified, record highs lie ahead. Despite this week's consolidation/correction, the market is showing sub-surface improvement as Advances outnumbered Declines for the past three days. In fact, if today's positive breadth is maintained at the close, the Advance-Decline Lines may well hit record highs again. Stayed focused on the major factors (which continue to give bullish readings) and do not be distracted by the ‘noise’.”

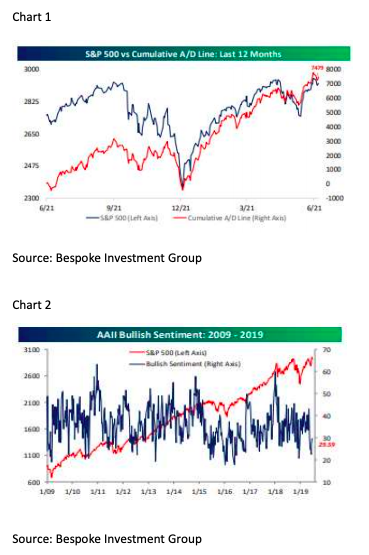

We believed the SPX was going to stall around the 2856 level, but the fore-reach of the market carried it higher than we thought. The stall, however, began on June 21 and extended into last Friday. Still, the primary trend of the stock market is bullish, and the breadth remains strong (chart 1). As Lowry’s writes, “On June 20th, the NYSE all-issues and our OCO Adv-Dec Lines reached new all-time highs together for the first time since May 3rd.” Surprisingly, despite a move to a new all-time high investor sentiment remains subdued (chart 2). Meanwhile, we are entering another earnings season and stock analysts are negative. To be sure, over the past month analysts have reduced estimates on a little more than 17% of the companies in the S&P 1500. Of course, we have seen this act before only to have earnings come in better than the reduced estimates. Still, the reductions have brought into question stock market valuations. Given the current estimates the SPX trades at 19.3x trailing EPS, which is expensive based on historic valuation metrics. However, it trades at 16.8x 12-month forward estimates. In past missives we have argued that in the current interest rate environment our work suggests the fair market price earnings multiple should around 19x.

We have not commented on Dow Theory in a while but have recently been getting questions about it given the under performance of the D-J Transportation Average (TRAN/10461.98). The question was best framed by the astute Lowry’s Research Company over the weekend. To wit:

“When forecasting major market tops, the Dow Theory focuses on the DJ Industrials and DJ Transports. In a healthy bull market, the two Averages confirm one another in recording new highs. The first warning sign of potential trouble for the market occurs when the DJI and DJT diverge. For example, although the DJI recently climbed above its late Apr. 2019 rally high, the DJT remains well below its Apr. high, setting up a potential divergence between the two Averages. According to the Dow Theory, the final step in completing a market top would be a close below a recent important intermediate-term low in each Average – most likely the June 3rd, 2019 reaction low, although some theorists would argue that a close below the Dec. 2018 low is more appropriate in signaling an end to the bull market.”

So, while the D-J Industrial Average (INDU/26599.96) has traded out to a new all-time closing high the Trannies have not and remain well below their respective all-time high. This is what a Dow Theorist terms a non-confirmation. Last week, however. The Transports started to pick up and are on the verge of bettering their recent intraday high. If that occurs, it will certainly be a step in the right direction. Remember, Dow Theory only uses closing prices and intraday highs/lows do not count.

Over the weekend all eyes turned toward the G-20 meeting. For those of you who don’t know we lived in and around the D.C. Beltway for years and consequently continue to have pretty good contacts here. What those sources are telling me late Sunday night is that the Chinese trade talks are going okay. Not great, but okay. They do not expect any formal agreement next week. Of course, those same contacts thought Mueller would indict some folks on Russian collusion (I think just about everyone had that one wrong). Evidently, China will purchase more U.S. agriculture stuff and America will not impose additional tariffs while the talks continue. I was told China made a large soybean purchase from the U.S. recently. I was also told DJT made a concession on Huawei.

The call for this week: The U.S. equity indices were mixed last week for as Leon Tuey points out – stocks have stalled since June 21. The stall could continue as participants await this quarter’s earning’s reports, geopolitics, Fed talk, and other economic data. As investors awaited second-quarter earnings reports, sentiment appeared to be dominated by geopolitical concerns (Middle East tensions, Trade war) and remarks from Fed officials which proved less dovish than some had hoped. Last week’s economic data generally missed expectations. Our stock market internal energy model is being rebuilt, but while the markets may continue to stall there is NOTHING bearish going on here by our work. We did hear a very interesting story on a company called Zymeworks (ZYME/$22.00). According to their website:

“Zymeworks Inc. is a publicly listed (TSX/NYSE: ZYME), clinical-stage, biopharmaceutical company dedicated to the discovery, development, and commercialization of next-generation multifunctional biotherapeutics, initially focused on the treatment of cancer.”

We were told they have found the “magic bullet.”

This morning the preopening futures are sharply higher on hope of a trade deal.

Investing/trading involves substantial risk. The author and Saut Strategy do not guarantee or otherwise promise as to any results that may be obtained from using this report. Past performance should not be considered indicative of future performance. No reader should make any investment decision without first consulting his or her own personal financial advisor and conducting his or her own research and due diligence, including carefully reviewing any prospectus and other public filings of the issuer. These commentaries, analyses, opinions, and recommendations represent the personal and subjective views of the author, and are subject to change at any time without notice. The information provided in this report is obtained from sources which the author believes to be reliable.

© Saut Strategy

[email protected]

Read more commentaries by Saut Strategy