I have held AbbVie (ABBV) since it was originally spun off from Abbott Labs. Moreover, I have been aggressively adding to my position for clients needing current income and dividend growth. All in all, it has been an excellent performer in spite of the fact that it is being ridiculously undervalued by Mr. Market. No matter what widely-accepted valuation measurement I look at, AbbVie appears insanely cheap.

As of yesterday’s close (June 24, 2019) AbbVie was trading at a blended P/E ratio based on adjusted operating earnings of 9.4 offering a dividend yield of 5.5%. This represents a significant discount to its historical normal P/E ratio of 14.5 and its intrinsic value P/E ratio of 15.

Furthermore, as of yesterday’s close, AbbVie was also trading at a price to EBITDA of 7.8 which is a significant discount to its normal price to EBITDA of 10.9. Additionally, and I consider this important since AbbVie is a dividend growth stock, AbbVie’s normal price to operating cash flow was 9.3 compared to its normal price to operating cash flow of 13.4 and its fair value price to operating cash flow of 15.

AbbVie was also trading at its lowest price to sales ratio of 3.66 since it was spun off and was available to investors at attractive double-digit earnings yields and cash flow yields. But most importantly, all these incredible valuations were supported by strong above-average historical growth and expectations for continued future growth in each of the above metrics.

On June 20, 2019 AbbVie also maintained its $1.07 per share quarterly dividend which is in line to be a significant increase over last year’s $3.95 dividend per share. Which by the way, is also well covered by both operating cash flow and free cash flow. Furthermore, according to Argus research in May of this year, AbbVie updated its adjusted earnings 2019 guidance to $8.73 to $8.83 which was up from its prior guidance of $8.65 to $8.75. (Note: I will be elaborating on all these metrics and more later in the FAST Graphs analyze out loud video).

Why Are AbbVie’s Valuations So Low?

Anyone who has been following AbbVie realizes that the company generates more than half its revenues from its flagship drug Humira which lost its patent protection outside of the US and faces competition from several recently launched biosimilars. However, Humira does not face greater competition from biosimilars in the US until 2023. Nevertheless, according to Argus research, Humira sales fell 23% to $1.23 billion outside the United States. This was in line with company guidance and they also project a 30% decline in Humira sales outside the US in all of 2019.

Humira sales growth in the United States increased 7.1% to $3.2 billion. However, although this is still strong growth, US sales growth has slowed from double digit rates in previous quarters. AbbVie has been fighting back with the recent approval of Skyrizi in both the US and Japan for treatment of moderate-to-severe psoriasis which clinical trials showed it to be superior to Humira. Skyrizi is also on track for approval in Europe. However, this is only one of many candidates in AbbVie’s pipeline. The following description of AbbVie Inc. courtesy of the Wall Street Journal illustrates the diversity of their pipeline:

“AbbVie, Inc. is a research-based biopharmaceutical company, which engages in the development and sale of pharmaceutical products. It focuses on treating conditions such as chronic autoimmune diseases in rheumatology, gastroenterology and dermatology; oncology, including blood cancers; virology, including hepatitis C virus (HCV) and human immunodeficiency virus (HIV); neurological disorders, such as as well as Parkinson’s disease; metabolic diseases, comprising thyroid disease and complications associated with cystic fibrosis; pain associated with endometriosis; and other serious health conditions. The company was founded on January 1, 2013, and is headquartered in North Chicago, IL.”

Nevertheless, AbbVie’s valuation has been clearly impacted by people’s fear of the potential loss of sales for Humira in the not so distant future. However, I think it’s important to recognize that this future is still unknown, while AbbVie’s current operating results remain excellent, and there is potential in AbbVie’s pipeline to not only replace Humira sales but continue growing sales far into the future. Consequently, I am choosing to follow Warren Buffett’s suggestion to be “greedy when others are fearful.”

Although there is always risk in evaluating the pipeline of any pharmaceutical company, AbbVie clearly has a strong pipeline with numerous candidates in phase 3 and several recent approvals. For those who would like to take a deeper look at AbbVie’s pipeline here’s a link on their website.

“But That Was Yesterday And Yesterday’s Gone”

As the English duo Chad and Jeremy so aptly put it in their 1963 hit: “but that was yesterday and yesterday’s gone.” The preceding was the beginning of my article on AbbVie where I was planning on building the case that AbbVie’s fundamentals were significantly stronger than their stock price. Nevertheless, today’s announcement that AbbVie was acquiring Allergan (AGN) solidified and even enhanced my view on this blue-chip dividend growth stock.

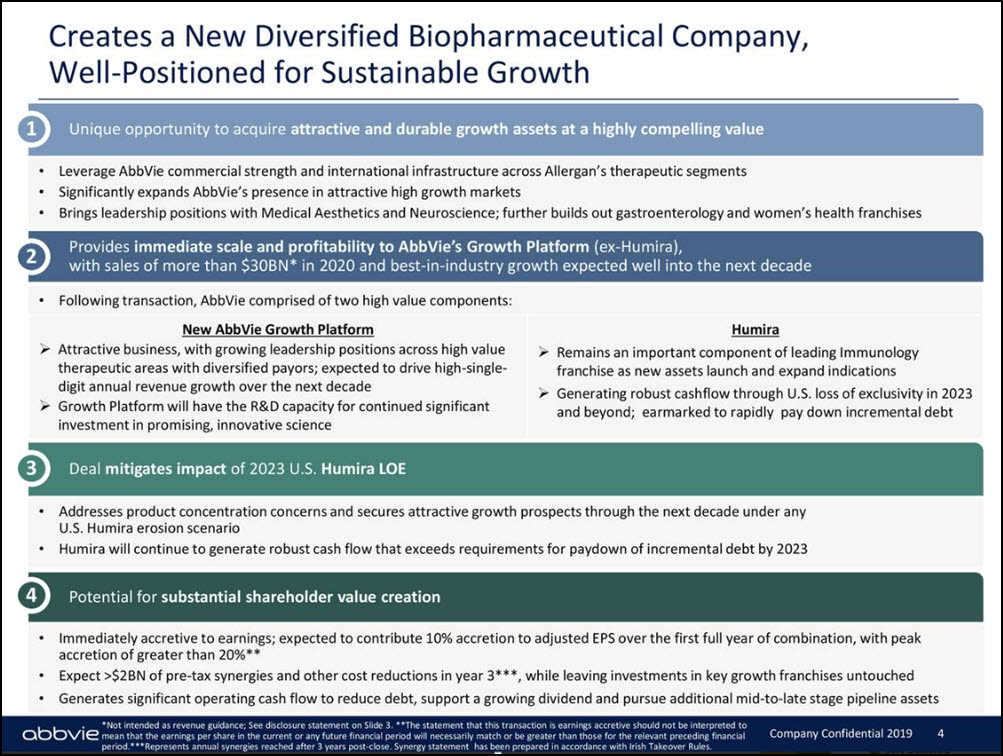

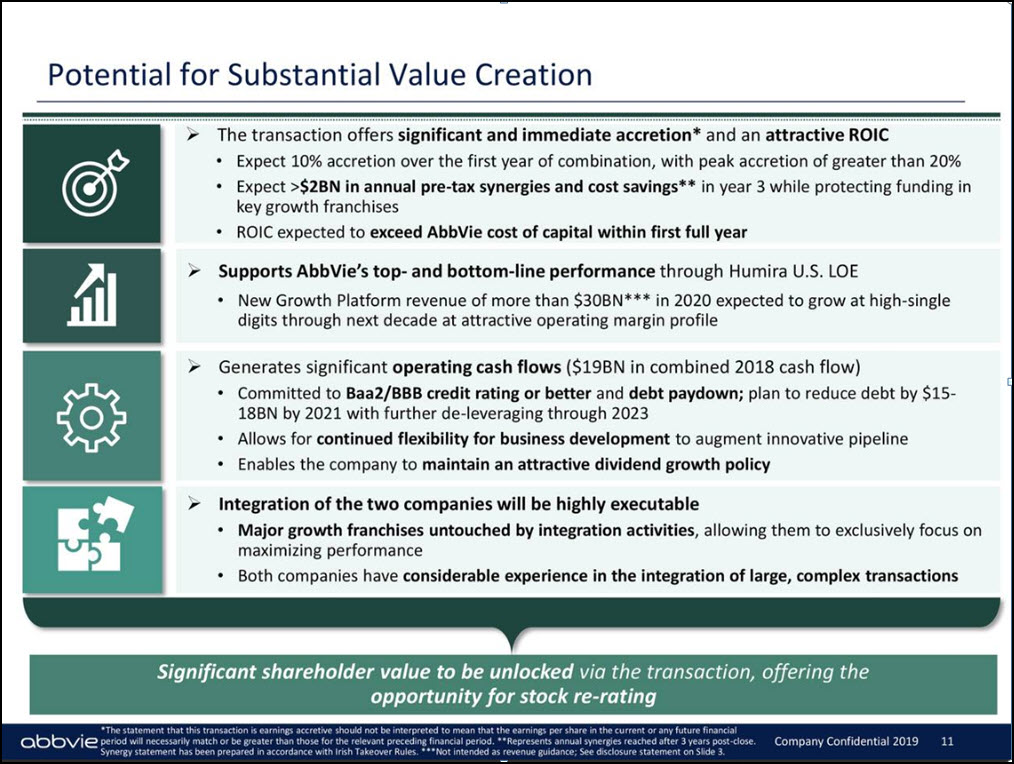

Suffice it to say that I agree with and even support management’s decision to acquire Allergan. I agree with AbbVie’s management that this transaction represented a “unique opportunity to acquire attractive and durable growth assets at a highly compelling value.” Furthermore, I agree with the additional three highlights that AbbVie’s management believes the Allergan transaction offers as depicted on the following slide:

The rest of the slideshow which highlights AbbVie’s positions on why they think this is an excellent transaction is worth looking at closely and can be found here.

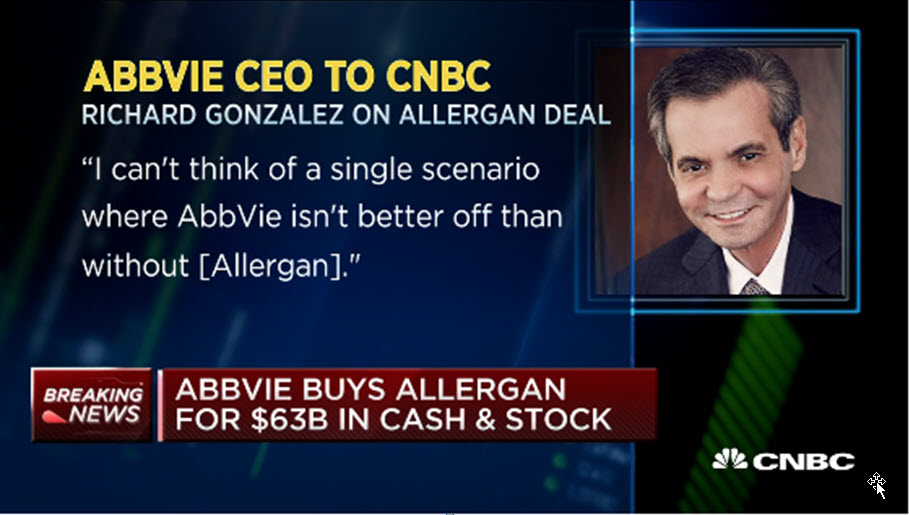

AbbVie’s CEO Richard Gonzales provided his views on why he believes the purchase of Allergan makes good sense for AbbVie and its shareholders. The following excerpts from the video played on CNBC found here highlights his views:

Allergan Cheap Before the AbbVie Acquisition- Still Cheap Afterwards

AbbVie’s $63 billion purchase of Allergan is essentially equal to the company’s current total enterprise value (TEV) of $65.3 billion. On a per-share basis the transaction works out to approximately $188 a share which is approximately a 45% premium to Allergan’s closing price on July 24, 2019. For Allergan shareholders the deal consists of $120.30 of cash and .8660 shares of the combined company.

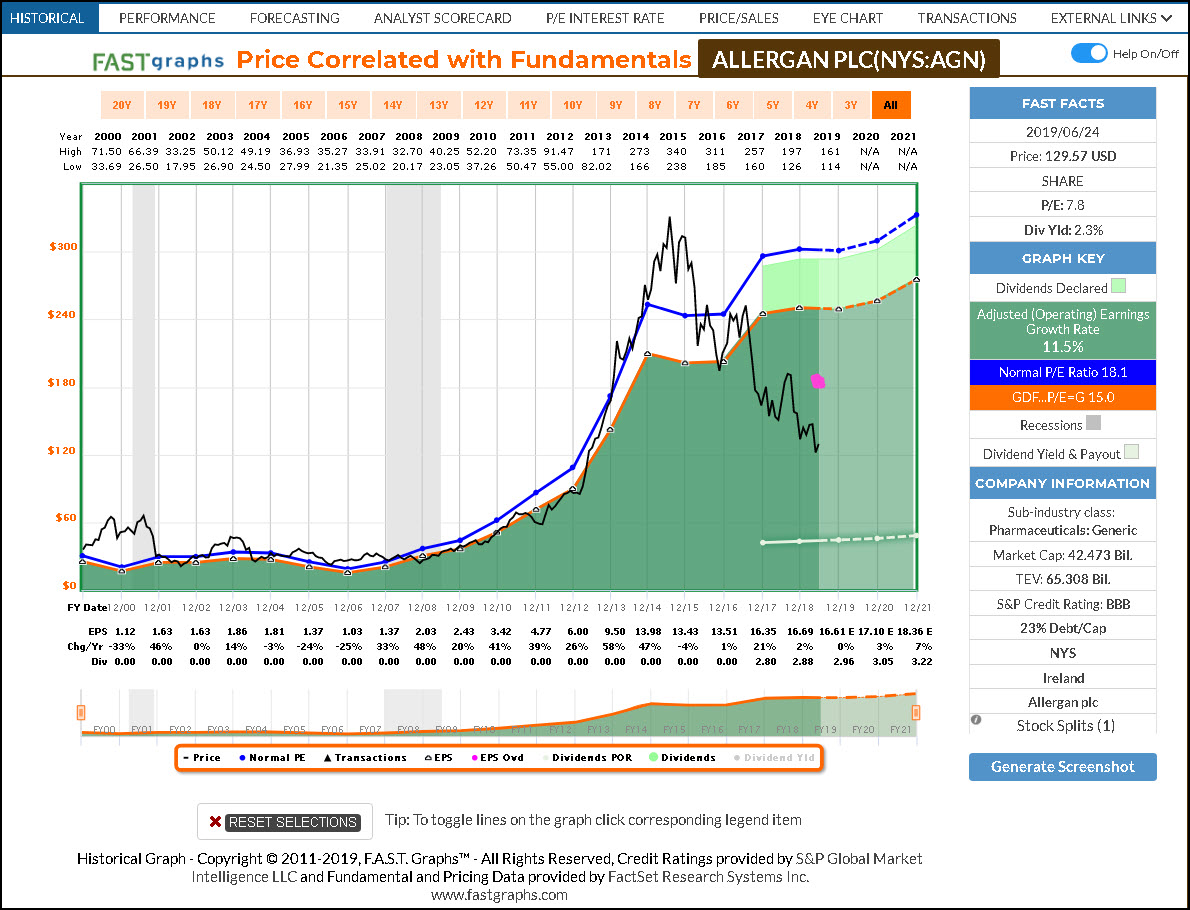

To put this transaction into perspective I offer the following earnings and price correlated graph on Allergan where I put a magenta dot on the graph approximately indicating the price that AbbVie is acquiring Allergan at. The important takeaway is that AbbVie is purchasing Allergan shares at a discount to the company’s intrinsic valuation and historical normal valuations.

Furthermore, I think the reader should note that Allergan was significantly overvalued in 2015 before earnings weakened. However, the reader should also note that the price reaction in 2018 and thus far in 2019 are clearly significant overreactions to a flattening of the company’s operating earnings. Stated differently, Allergan remained a very profitable business where earnings growth merely slowed while stock price collapsed. Again, I believe that was a significant overreaction by the market that appears quite clear when viewing the graphic.

AbbVie Was Already Cheap But Just Got Cheaper

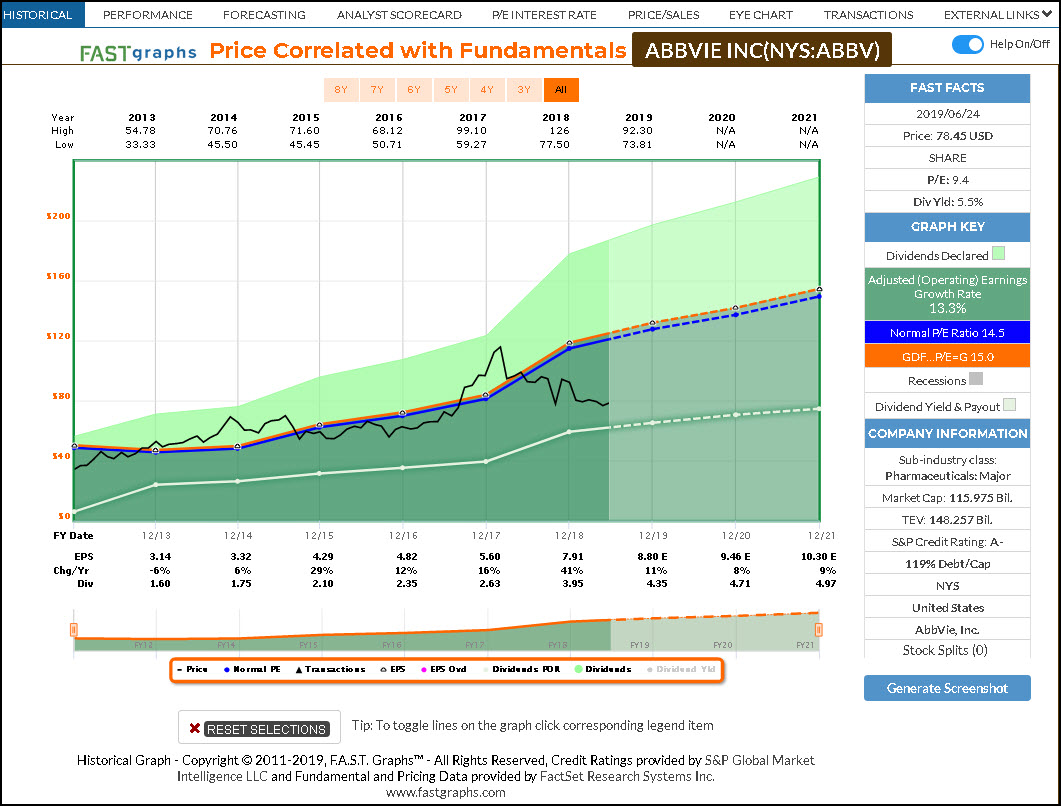

As I indicated in my intro, as of yesterday’s close (June 24, 2019) AbbVie was already extremely undervalued based on past, present and expected future operating performance. Furthermore, this was supported by virtually every widely-used valuation metric. The following adjusted operating earnings and price correlated graph clearly tells that story. As the reader should note, earnings are expected to grow approximately 11% in 2019 which is the midpoint of company guidance as well as the consensus of leading analysts following the company. Furthermore, the reader should also note that earnings beyond 2019 were also expected to increase by 8% and 9% respectively for fiscal years 2020 and 2021.

Most importantly, the earnings expectations on the above graphic represent AbbVie’s management and consensus leading analyst expectations for the company prior to the announced acquisition. As the following slide depicts, AbbVie’s management expects those numbers to be exceeded as a result of the Allergan purchase. Consequently, AbbVie has become even more valuable today than it was yesterday considering the significant price drop coupled with the higher expected future growth.

MorningStar stock analyst note 9:50 AM June 25, 2019

MorningStar published a stock analyst note this morning on the AbbVie transaction titled “AbbVie’s Acquisition of Allergan Looks Opportunistic and Offers Diversification From Humira” In the analyst note MorningStar suggested that Allergan’s portfolio of branded drugs should strengthen AbbVie’s moat and that Allergan’s pipeline and Botox entrenchment did not seem to be fully factored in Allergan’s price. Consequently, they suggested that many of the fears over Humira biosimilar competition would be partially alleviated. Therefore, they continue to believe that AbbVie is undervalued. MorningStar also believes that the $2 billion in annual savings projected by AbbVie’s management seems reasonable.

Barron’s

At 2:05 PM June 25, 2019 Barron’s magazine reported that AbbVie shareholders will get no vote on the purchase of Allergan. They did suggest that even though shareholders of Allergan will vote on the sale they believe it’s unlikely that it will face opposition considering the stock has increased over 26% thus far today.

FAST Graph Analyze Out Loud Video: AbbVie by the Numbers (Allergan included)

Summary and Conclusions

Although it is very difficult for many investors to accept the idea that the market often mis-appraises the market value of publicly traded stocks, my personal experience tells me that it often does. Consequently, I have learned over the many years I’ve been doing this to trust fundamentals more than I do short-term price volatility. Moreover, my personal experience also tells me that short-term market price behavior has a very insidious nature. Unfortunately, investors tend to trust and/or believe more in significant levels of overvaluation, than they do significant levels of undervaluation.

To clarify further, investors will ignore the enormous danger of overvaluation and flee like rats from a burning building from the incredible opportunity of significant undervaluation. In other words, investors want to buy when they should sell and sell when they should buy. Therefore, it has never been a surprise to me that so few people make long-term money investing in stocks. Stocks rarely recover from massive overvaluation, and almost always recover from significant undervaluation. Nevertheless, when emotions rule reason goes out the window.

Today’s reaction to AbbVie’s announcement that they were purchasing Allergan represents a quintessential case in point. Prior to the announcement, investors were fearful that AbbVie was going to suffer from the potential competition facing their flagship drug Humira. However, when management announced this transaction that in addition to other benefits should partially mitigate the potential reduction of future Humira sales, the market reacts negatively instead of the more logical positively. Oh, the peculiar illogic of Wall Street!

Personally, I have believed and continue to believe that AbbVie has a bright and profitable long-term future ahead of it. After today’s announcement, my belief is both solidified and enhanced. Furthermore, my beliefs are primarily based on the actual results that AbbVie is producing, and to a lesser extent on the company’s future potential. Common sense suggests that all pharmaceutical companies face pipeline risks and AbbVie is no different. On the other hand, recent successes coupled with several drugs already in phase 3 and notwithstanding the Allergan pipeline suggests my confidence is not without justification.

Nevertheless, there are risks that the Allergan transaction will not go through. If that does happen, I still believe that AbbVie possesses the potential future growth that I showcased in the beginning of this article. Consequently, I believe that the Allergan opportunity represents potential icing on that cake. All stock investments possess risks, and AbbVie is certainly no exception. On the other hand, it is very rare to find a stock that possesses all the attributes and the incredible long-term return opportunity that AbbVie currently does. The combination of an extremely high and fast-growing current dividend yield coupled with incredible capital appreciation potential make this a risk worth taking. At least in my humble opinion. But with that said, I have elected to let the market digest this news before I add to my positions, which I eventually intend to do. Caveat emptor.

Disclosure: Long ABBV

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.