On Tuesday of this week we wrote about the four possible scenarios the Fed could adopt in their Wednesday policy decision. In order of most hawkish to most dovish, those scenarios were:

- Fed does not cut rates and signals that a rate cut may be appropriate later in the year (read the September meeting). Balance sheet policy remains unchanged.

- This is the most hawkish of the likely outcomes. The financial markets would likely read this as too hawkish, causing long bond yields and equities to fall as a further slowing of economic growth is discounted.

- Fed does not cut rates, but instead signals a rate cut of 25bps is likely in the near term (read the July meeting). Balance sheet policy remains unchanged.

- This too is a somewhat hawkish outcome since the first rate cut is typically the largest rate cut. The long end of the bond market is likely to rally (lower yields) as the market views the move as less than what is needed to arrest the slowdown. Impact on equities would be small.

- Fed does not cut rates, but instead signals a rate cut of 50bps is likely in the near term (read the July meeting). Balance sheet policy remains unchanged.

- Now we are getting somewhere, and even though this is a somewhat dovish scenario long bond yields are likely to fall in sympathy with short rates, though perhaps not as much as short rates. Equities would likely rally.

- Fed does not cut rates, but instead signals a rate cut of 50bps is likely in the near term (read the July meeting). Balance sheet runoff stops tomorrow and the Fed opens up the possibility of more QE down the road.

- This is the least likely outcome and also the most dovish. Short rates may fall while the long end would likely selloff, steepening the yield curve and ushering in a risk on environment. In this dovish case, equities are likely to do quite well as a reflation trade takes hold, a la QE2.

Well, it turns out the Fed indicated they will walk through door number 2 in July, but opened up the possibility of actually walking through door number 3 if enough voting members get on board with a 50bps rate cut. The market’s reaction to this news was pretty much as expected so far, though two days of trading is hardly enough to identify a lasting trend. The S&P 500 is higher by 1.1% (good but not great) and Treasury bond yields are lower by a bit in aggregate. Gold of course is in the midst of a major breakout above $1400/oz while the US dollar is under pressure. So far so good.

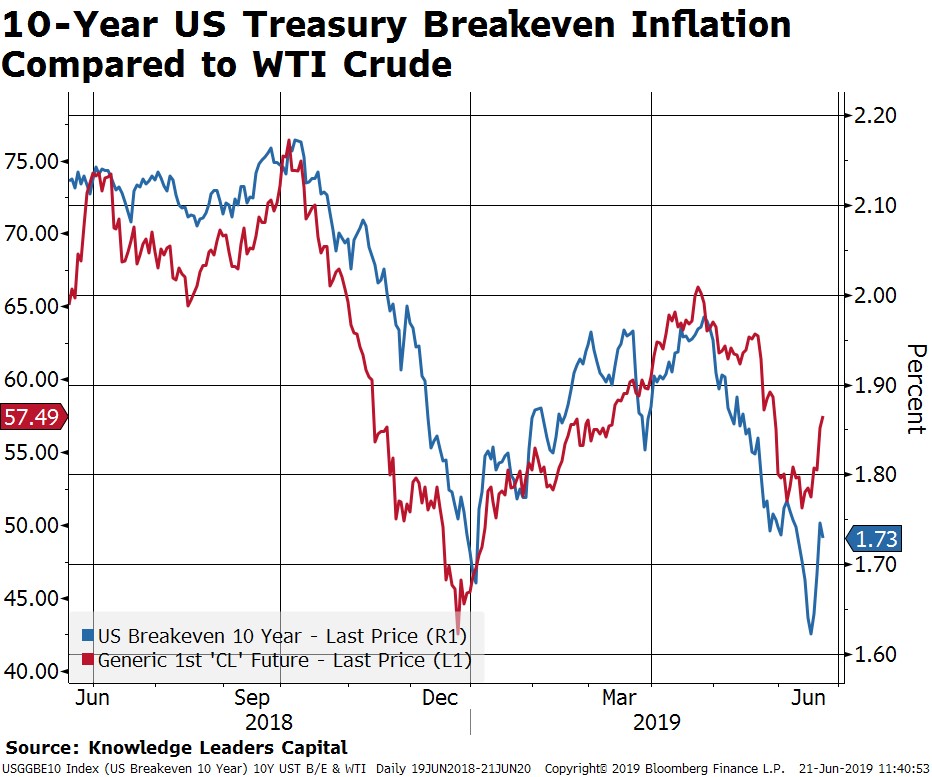

But, things are more interesting than those surface numbers portray, especially so in bonds. In aggregate, 10Y yields fell modestly from about 2.10% to about 2.06% as of this writing since the Fed’s announcement. However, growth expectations fell by a whopping 15bps while the inflation expectations component of the yield actually rose by 11bps. The bulk of the the rise in the inflation component of the yield is due to oil prices ratcheting higher by 12% since Tuesday, partly in response to geopolitical goings on. Therefore, but for the sharp rise in oil prices, the 10Y bond yield would be lower by 26bps since the Fed’s decision.