Ignore Political and Economic Forecasts: Mind Your Owned Businesses

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIntroduction

In his Berkshire Hathaway 1994 annual report Warren Buffett said ignore political and economic forecasts. I considered this one of the more profound pieces of investment advice and wisdom that I ever came across. It has been my opinion prior to and since I read this advice that investors spend way too much time and energy worrying about things that really don’t – and shouldn’t – matter. I have learned that it is futile to attempt to predict future political, economic or market directions and magnitudes. Nevertheless, most investors seem almost obsessed with trying to do it.

Additionally, it is my humble opinion that investors also place too much importance on evaluating their portfolios based solely on what the current market price shows. Market value is only one of many ways to evaluate how your portfolio is performing. Furthermore, I believe that most of the other ways are more important. Current market value and the intrinsic value of your portfolios are often quite different. To my way of thinking, current market value tells you more about your current liquidity than it does the true value of what you own.

Stated differently, market value often either overstates or understates the true value of the businesses that you own. Consequently, I consider it significantly more important and intelligent to assess the value of your businesses based on sound principles of business, economics and accounting (fundamental values). Therefore, by knowing the true worth of your holdings, you can make more intelligent decisions as to whether you should be buying more, selling, or holding in relation to the market value. To clarify, I do not believe in paying more for a business than it is worth, nor do I believe in selling a business for less than it’s worth. Current market price rarely gives me the whole picture.

In addition to market price and the associated volatility, I also prefer to consider the operating results, which include the growth of earnings, cash flows and dividends. To clarify, if earnings and dividends are growing and market price is inexplicably falling, I see this as a bargain. On the other hand, if I see market values excessively high and fundamentals do not justify the lofty levels, I see risk and potential loss. To summarize, I trust fundamentals more than I do emotionally-charged market behavior.

Nevertheless, the vast majority of investors that I have talked to see only the bottom line with little consideration, regard or concern about how well their businesses are performing. Consequently, they tend to be inclined to want to sell when they should buy – and vice versa. Additionally, most investors tend to worry about macroeconomic forecasts that are for the most part unpredictable, and rarely turn out to be accurate.

This is a soapbox that I have been standing on for many years (actually decades) with little success. However, I consider it extremely important and therefore will never tire of singing the song of prudence and fundamental valuations. In August 2011, I authored an article discussing these very issues. With this article I am revisiting the message I delivered in 2011. It’s important to recognize that this was a period of time where investors were still traumatized by the great recession of 2008. The markets and the fundamentals were behaving quite positively, but investors were having trouble believing that the future could possibly be bright. Yet, despite all these concerns, stock market performance since the spring of 2009 has been one of the best on record.

My Original Article Posted on 2011-08-10 With Edits and Updates Included

There’s certainly no shortage of pundits, prognosticators and even self-proclaimed prophets ready and willing to bombard us with dire forecasts about our future. We get a day in the market like Monday, August 8, 2011, and “Chicken Little” shows up everywhere to include radio, television, newspapers, magazines and the Internet. Yet somehow, we survive it all. But no matter how often our so-called experts get it wrong, they remain steadfast in their desire to forecast our doom with their gloom.

It’s been more than 40 years ago when I first entered the investment business that many friends and family admonished me to reconsider my career path. Their reasoning was simple. There is simply no possible way that the US economy could survive and prosper under the weight of our enormous national debt. In 1970, the year I entered the business, our national debt sat somewhere between $370 and $380 billion. Of course, today our national debt hovers somewhere around $13 trillion and growing.

Before I go any farther, I want to clarify one important matter. Nothing I’ve already written or am about to write is meant to trivialize our serious national debt issue. The amount of debt that our government has piled up in the last 40-plus years is egregious and needs to be addressed. On the other hand, a great motivating factor for authoring this article is to attempt to separate government and the economy.

From my perspective, I clearly see government as a major expense item on our economic profit and loss statement. However, I reject the notion that the government either runs the economy or is responsible for its health. Would it not be true, that if our government ran our economy, that we would be at best a socialistic state, or at worst a communistic state. But in truth, we are a democracy, and our economy is one built on free enterprise and consequently is market driven.

Therefore, our free market-based economy is run and driven by the economic forces of supply and demand. On this basis, what matters most is the attitude of the businesses, consumers and other important components of our economic decision-making processes. In other words, how we feel about our economy has a great deal to do with how we behave, which can have a large impact on our economic growth and health over the short run. In other words, if we all believe our economy is weak, it can easily turn into a self-fulfilling prophecy. On the other hand, when our confidence is high our economy tends to be healthier.

Therefore, it’s really important to understand what drives our economy and what doesn’t. I believe that the overall level of productivity is a major contributing factor to the continuation of economic growth. Essential in this regard would be the primary factors of production, which are land labor and capital. Additional important factors would include research and development and other paths to innovation that promise to increase productivity. But most importantly, government is not a factor of production, as previously stated – it’s an expense.

Warren Buffett’s Sage Advice in 1994

In the Berkshire Hathaway 1994 annual report, Warren Buffett wrote something that had a major impact on me at the time, and it has continued to contribute to my general thinking about investing to this day. Consequently, I consider it one of my favorite Warren Buffett quotes, as well as one of the most important lessons he ever offered the general investing public. I’m going to present the entire quote in this article; however, I am going to break it down into shorter snippets in order to elaborate its important message. But before I do that, I offer this lament: How can people ignore the following aphorism to the point of not even considering its important lesson?

The first sentence of this important Warren Buffett quote establishes its message: “We will continue to ignore political and economic forecasts which are an expensive distraction for many investors and businessmen.” With his first sentence, Warren Buffett is telling us that he considers politics and economic forecasts an expensive distraction. In other words, he is in effect imploring us, as will become more evident later, to focus precisely on what we own, rather than generalities that may or may not impact us in the long run.

The point I am attempting to make here is a simple one. Routinely, I talk to many people that can tell me in precise detail not only what the politicians in the United States are arguing about, but also what’s going on in politics in other nations all over the world. They get this information from the daily bombarding of negative and scary headlines offered by the mass media. Yet ironically, if I asked them questions about their precise holdings, they cannot answer them. For example, if I asked them whether the companies that they own had a good quarterly earnings report, or how many of their companies raised their dividends or announced stock buybacks, et cetera, they usually have no clue.

In other words, I believe investors obsess about things that although scary, do not have a direct long-term impact on their specific portfolios, but only their short-term attitudes about them. The next line in the Warren Buffett quote speaks to my point: “Thirty years ago, no one could have foreseen the huge expansion of the Vietnam War, wage and price controls, two oil shocks, the resignation of a president, the dissolution of the Soviet Union, a one-day drop in the Dow of 508 points, or treasury bill yields fluctuating between 2.8% and 17.4%.” What these important words tell us is that with investing, there is always something to worry about, keep in mind these words were written in 1994.

However, perhaps the most important lesson that this, my favorite Warren Buffett quote can teach us, is found in the next phrase as follows: “But surprise-none of these blockbuster events may even the slightest dent in Ben Graham’s investment principles. Nor did they render unsound the negotiated purchases of fine businesses at sensible prices.” Here Mr. Buffett is telling us that the prospects and rewards of owning good businesses are often independent of the general political and economic environment we find ourselves in. He is also speaking to the importance of investing in good businesses at sound valuations. Finally, we believe he is telling us that it’s more important for us to focus precisely on what we own, because this is where our true long-term rewards or losses will come from.

The final three sentences in this profound Warren Buffett advice are most relevant to the purpose of this article: “Imagine the cost to us, if we had let a fear of unknowns cause us to defer or alter the deployment of capital. Indeed, we have usually made our best purchases when apprehensions about some macro event were at a peak. Fear is the foe of the faddist, but the friend of the fundamentalist.”

Once again, I believe Mr. Buffett is advising us to focus on our precise holdings and their unique fundamental strengths and worry less about what’s going on in more general terms. An old Wall Street adage summarizes my point: “Wall Street climbs a wall of worry.” Of course, the most important lesson here is not to let fear overcome reason. As promised, what follows is the Warren Buffett quote in its entirety:

“We will continue to ignore political and economic forecasts which are an expensive distraction for many investors and businessmen. Thirty years ago, no one could have foreseen the huge expansion of the Vietnam War, wage and price controls, two oil shocks, the resignation of a president, the dissolution of the Soviet Union, a one-day drop in the Dow of 508 points, or treasury bill yields fluctuating between 2.8% and 17.4%. But surprise-none of these blockbuster events made even the slightest dent in Ben Graham’s investment principles. Nor did they render unsound the negotiated purchases of fine businesses at sensible prices. Imagine the cost to us, if we had let a fear of unknowns cause us to defer or alter the deployment of capital. Indeed, we have usually made our best purchases when apprehensions about some macro event were at a peak. Fear is the foe of the faddist, but the friend of the fundamentalist.”

A Few Real-World Examples of Warren Buffett’s Wisdom

What comes next are four real-life examples looked at through the lens of our F.A.S.T. Graphs™ research tool. Admittedly these four selections are hand-picked, because the theme of this article relates to focusing on precisely what you own and carefully researching them before you buy them. My first two examples will look at what I consider to be pure unadulterated growth stocks. My third and fourth example will look at two blue-chip dividend growth stocks.

Two Powerful Growth Stocks Unaffected by the Great Recession

Cognizant Technologies Inc. (CTSH)

My first example is Cognizant Technology Solutions (CTSH). “Headquartered in Teaneck, New Jersey, Cognizant (NASDAQ: CTSH) is a leading provider of information technology, consulting, and business process outsourcing services, dedicated to helping the world’s leading companies build stronger businesses…”

The focal point of the following graph is the plotting of each year’s earnings since calendar year 2004 as represented by the orange line with white triangles. Notice how during the great recession this well-managed company, with no debt on the balance sheet at the time, generated powerful earnings advances despite the economic crisis.

Powerful Operating Performance Right Through the Recession

Furthermore, also consider that the significant drop in stock price from 2007 to 2008 of $22.35 per share to a low of approximately $9 a share was unjustified based on operating results. Perhaps even more importantly, notice how the stock price had recovered to a high of over $41 a share by spring of 2011.

The performance results associated with the above graph illustrate how powerful the rewards can be when the focus is on the specific business results of the company instead of on general economic conditions. The total annualized rate of return for this non-dividend paying growth stock was in excess of 22% per annum at a time when the general market produced very weak results.

Apple Inc. (AAPL)

My second example looks at one of today’s most highly recognized growth stocks, Apple Inc. (AAPL). Thanks to the significant innovations that this company has developed in recent years, their earnings growth has been nothing short of spectacular. Nevertheless, even with this outstanding operating performance, Apple’s stock price was more than cut in half during the great recession. Of course, the subsequent recovery in their stock price has also been nothing short of outstanding.

Strong Recession Resistant Performance Results

The associated performance results for Apple from fiscal year 2004 through their fiscal year ending in September 2010, are truly remarkable. And, as this article is designed to point out, the more than 60% compounded rate of return that Apple generated for shareholders was achieved independent of the economic or political environment that prevailed during this time.

Two Blue-Chip Dividend Growth Stocks Unaffected by the Great Recession

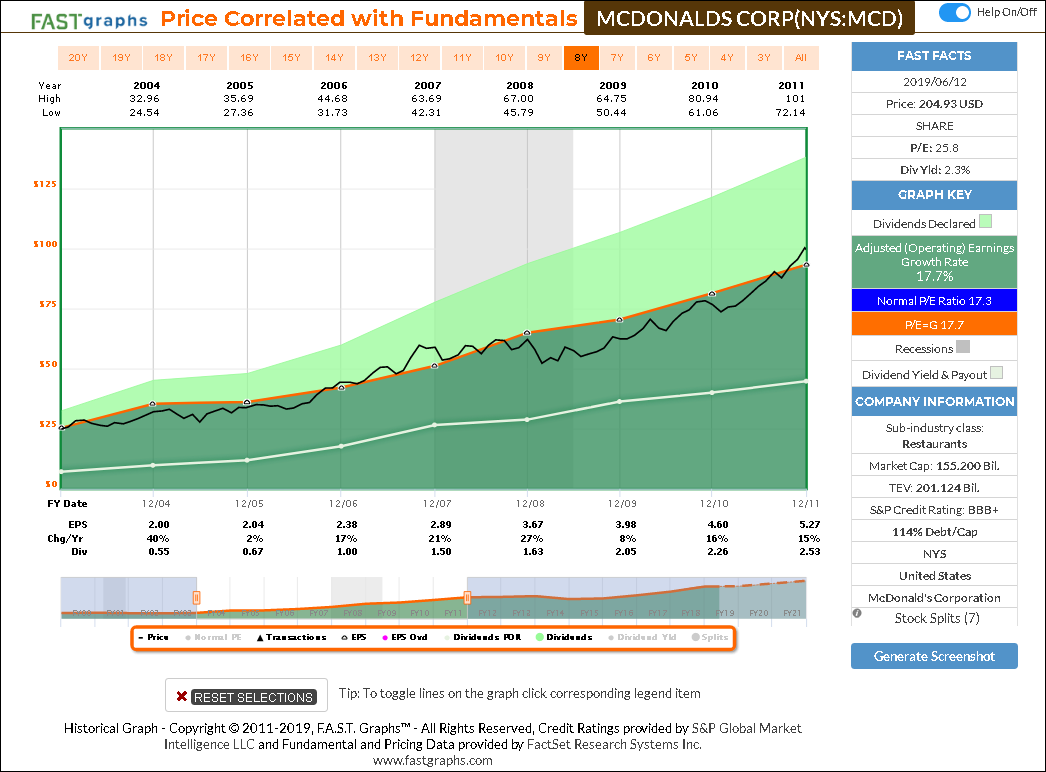

McDonald’s Corp. (MCD)

When looking at dividend growth stocks like my first example, McDonald’s Corp., the focus on the orange earnings line is still very important. However, the light green shaded area on the following graph depicts dividends paid out of earnings. What is clear from the graph is how McDonald’s stock price tracked its consistent earnings growth record of over 17.7% per annum. For the dividend growth investor, they can still face day-to-day stock price volatility, but the advantage of carefully selected dividend growth stocks is the consistent reward from the increasing dividend.

At the bottom of the McDonald’s graph, we can see that the dividend increased from $.55 per share to $2.53 per share for calendar year 2011. Since dividend growth investors tend to be long-term owners focused on the dividends, they were rewarded even during the great recession of 2008 by the growing dividend representing an annual increase in pay.

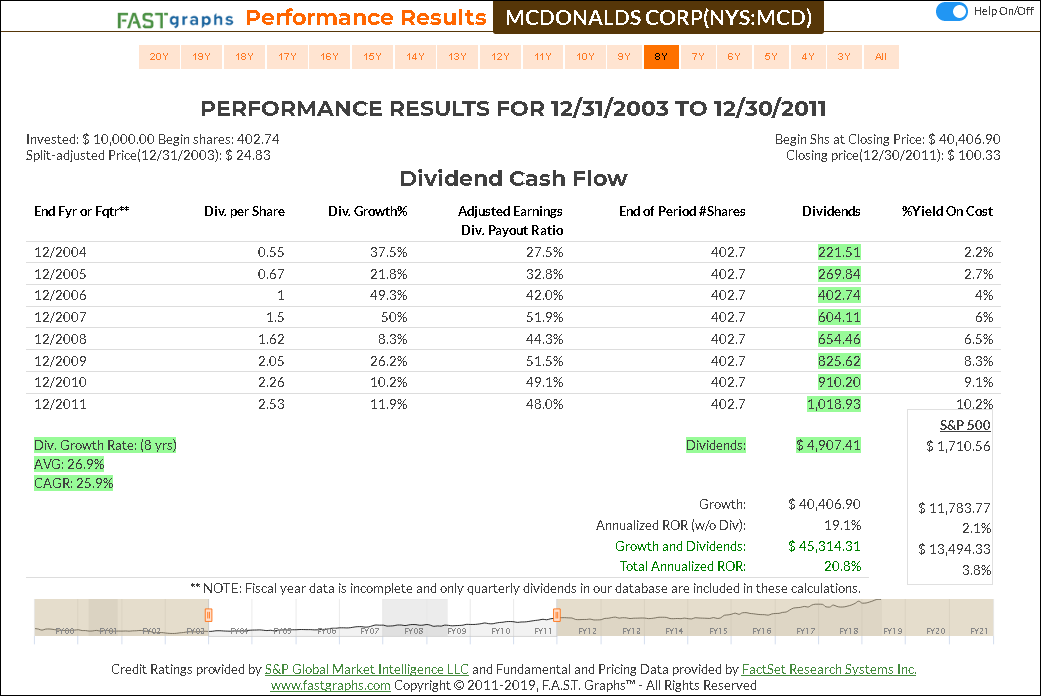

A Growing Dividend Every Year

With the performance results associated with the above graph, we find that McDonald’s was an exceptional investment prior to and during the great recession of 2008. As stated above, the most important attribute to focus on here is the rapidly growing dividend record of this recession-resistant company.

Johnson & Johnson (JNJ)

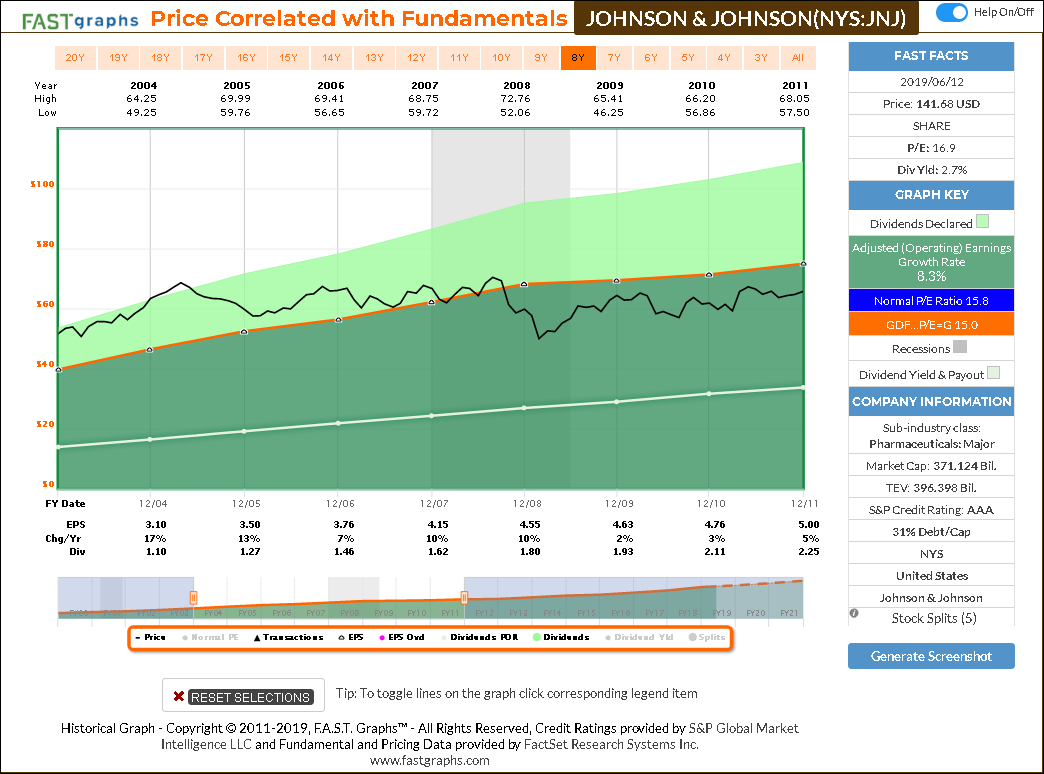

My fourth and final example looks at Johnson & Johnson, a company whose AAA credit rating was even higher than the US Government over this timeframe, at least according to one rating agency. Once again, we see an example of a very consistent earnings growth rate through the recession. However, the recession did cause their earnings growth rate to slow, but not fall. This graph also shows that Johnson & Johnson has typically commanded a premium price earnings ratio relative to its earnings growth. However, for a couple years post the great recession of 2008 this extremely high-quality company traded at a discount to its earnings justified valuation (the orange line).

Shareholders Get a Dividend Increase Every Year

As was the case with McDonald’s, when looking at the associated performance results with the above graph we once again see an example in Johnson & Johnson where they were able to raise their dividend every year since calendar year 2004. Although the growth rate was not as fast as we saw with McDonald’s, the dividend yield was 3.4% by the end of 2010, thanks to its low valuation following the great recession. Consequently, the great recession created an intriguing purchase opportunity of this bluest of blue chips at a bargain basement valuation. Possibly for the first time ever, Johnson & Johnson offered investors a starting dividend yield that was more than they could earn on a 30-year treasury bond. It’s also important to mention that a high starting valuation was the major contributing factor to Johnson & Johnson’s modest returns over this timeframe.

Conclusions

This article is about casting a light of reason on the longer-term perspective, in contrast to what is typically an emotionally-charged attitude about short-term volatility. It is understandably human nature to judge the performance of our portfolios based primarily on their closing stock price for any given day, week, month, or even quarter. The point I am trying to make here is that it is not the most important factor, unless you were literally planning to sell on the day you measure it. Otherwise, the intrinsic value derived from the operating results that your companies generate is, beyond a shadow of a doubt, more important than price volatility, in the longer run.

Part of the problem lies in the complexity that most investors face when attempting to evaluate their specific portfolios beyond price alone. The media only speaks to generalities about the stock market, the economy or politics. Therefore, the everyday investor can only judge their holdings, outside of stock price, against the backdrop of what is generally happening. On the other hand, there are ways that investors could organize the information they receive to focus more on their actual specific holdings. By doing this, they could keep track of their earnings and dividend records, as well as other important news relating specifically to their portfolio holdings. This is precisely why I developed FAST Graphs, the fundamentals analyzer software tool.

Warren Buffett’s timeless quote, along with the four examples cited in this article, provide prima facie evidence that supports our thesis. Leave the broader economic issues to all the pundits who relish the opportunity to predict the unpredictable. Regarding your own financial futures, place your attention precisely on what you personally own and focus specifically on the performances of the businesses behind your investments. There is no place in investing for allowing emotions to interfere with sound judgments. If others are selling because they’re afraid, you can ignore that based on the confidence you have in what you specifically own. I will summarize and conclude this article with another related Warren Buffett quote:

“If we find a company we like, the level of the market will not really impact our decisions. We will decide company by company. We spend essentially no time thinking about macroeconomic factors. In other words, if someone handed us a prediction by the most revered intellectual on the planet, with figures for unemployment or interest rates, or whatever it might be for the next two years, we would not pay any attention to it. We simply try to focus on businesses that we think we understand and where we like the price and management.”

Disclosure: Long CTSH, AAPL, MCD and JNJ at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits