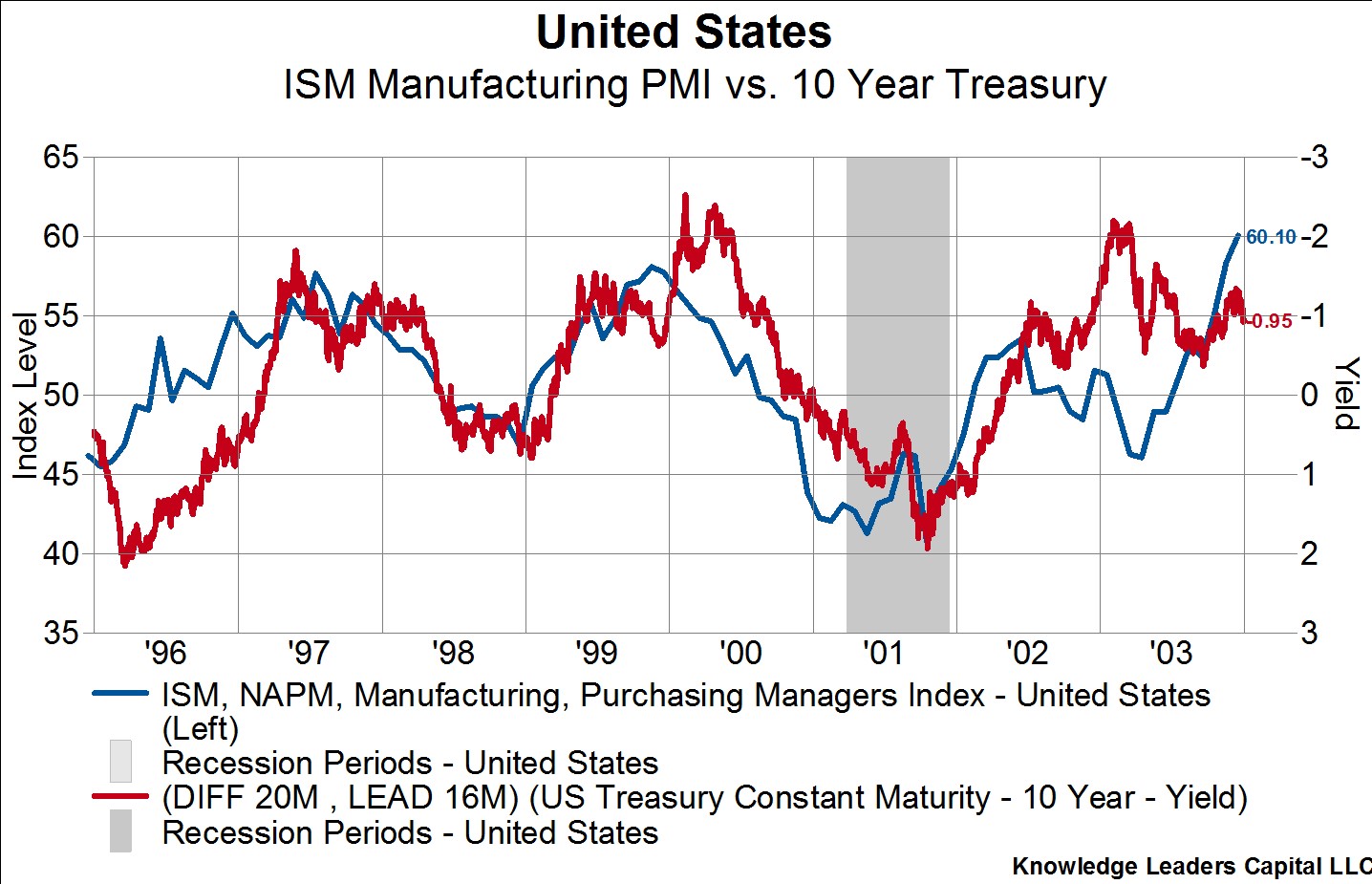

Here’s Why the 1998-99 Melt Up in Stocks is Not an Appropriate Analog

As expectations for a Fed easing cycle have gained momentum, we’ve seen an abundance of comparisons between the current period and the late 1990s. In that period the Fed cut rates and stocks simultaneously levitated into the stratosphere. If we are to follow the logic that the rate cuts in 1998 caused the stock market to rise, then it follows that rate cuts today will cause the stock market to rise. We think that comparison is dangerously off base and will explain why in this post.

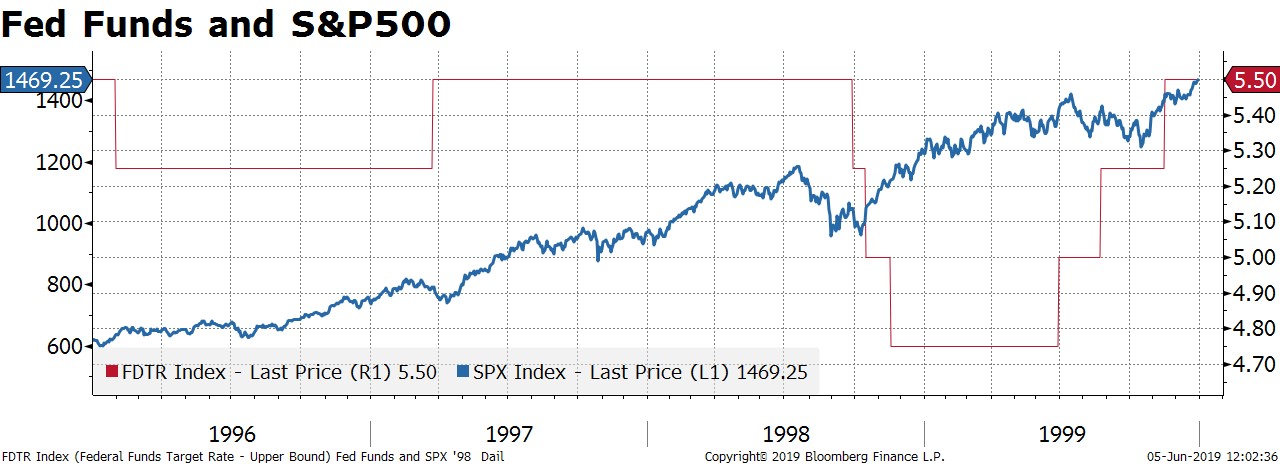

1997 and 1998 was a busy time for financial market news flow. Over that period the Asian financial crisis was unfolding full steam ahead, Russia had defaulted on its debt and the ruble lost 70% of its value, and in September of 1998 Long Term Capital Management (LTCM) failed, requiring a bailout from private lenders. Amid all that turmoil US stocks lost 19% of their value between July and October of 1998. LTCM was the last straw for the Fed and they began cutting the Fed Funds rate at the end of September. Stocks bottomed two weeks later and then staged a 48% rally into the summer of 1999. Economic activity was extremely strong over the period.

Linking the Fed Funds rate cuts in 1998 to the improvement in the economy and equity markets is appealing. It presumes US stocks can blastoff from current levels and a few Fed rate cuts will cause economic growth to improve materially. If only it were true. Below is a short list of key differences between now and 1998 that indicate this time is likely to be significantly different:

-

- Fed Funds rates were roughly flat for 2.5 years leading into the cuts in 1998. Recently, the Fed raised policy rates for 2 years leading into 2019, and the lagged affects of that action is yet to be fully felt.

- M1 and M2 money supply were growing strongly in 1998 and were barely affected by the exogenous factors at play. Today, M1 and M2 money supply figures are headed toward zero and some of the lowest levels we’ve seen since the Financial Crisis.

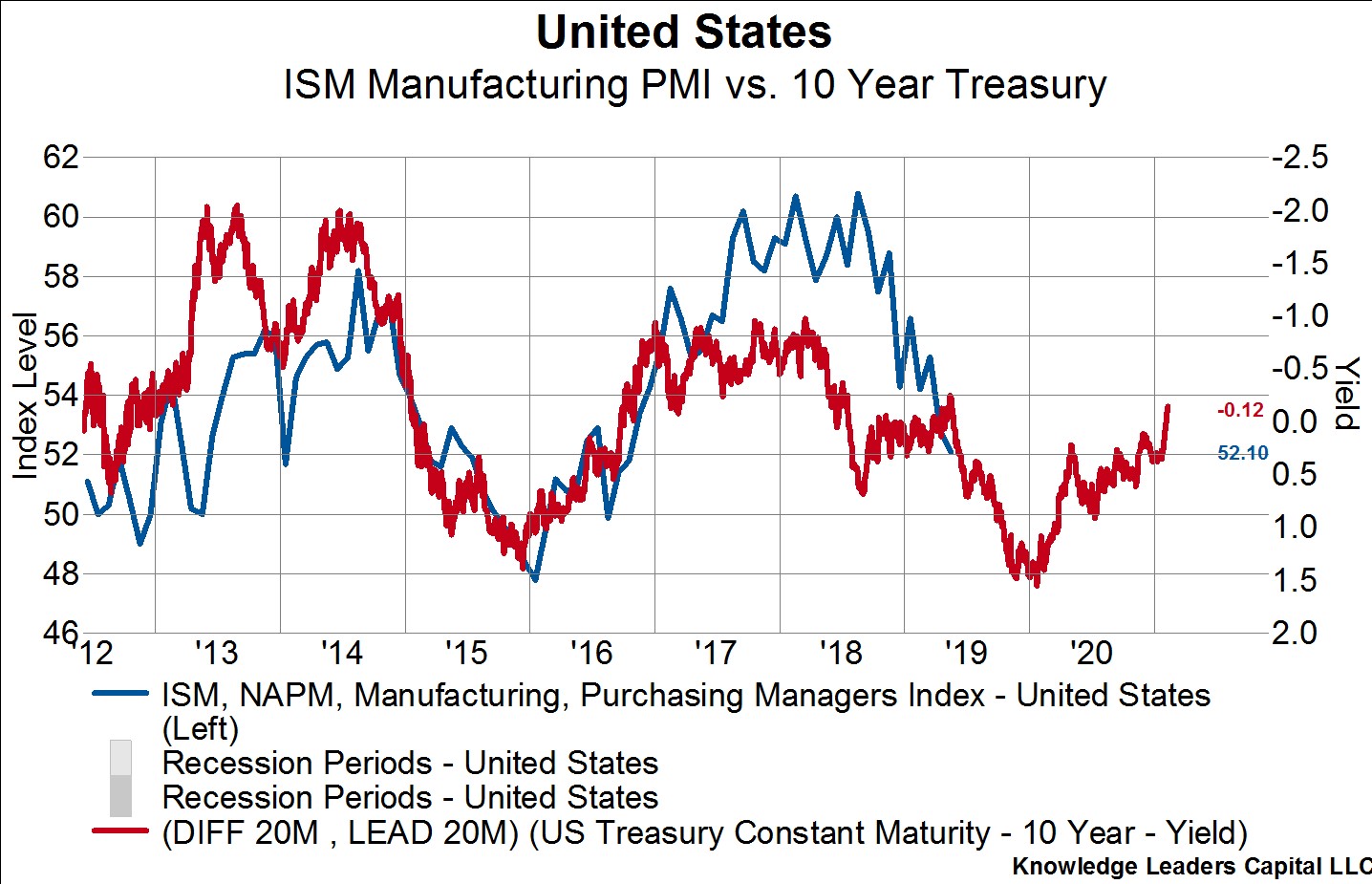

- In 1998 the yield curve flattened, but did not invert at the important 10Y-3M spread. Today, the yield curve is squarely inverted between the 10Y and 3M periods.

- There was no fiscal tightening in the offing in 1998. We face 77bps of fiscal tightening as a % of GDP next year.

- Tariffs were not at play in 1998. Today, we face a hit to growth of between .2% of GDP and 1% of GDP in 2019 and 2020 depending on how the trade war evolves.