So, last Monday (6-3-19) at 10:30 a.m. we issued this Trading Flash:

“First, spell check changed one of the words in this morning’s Strategy Report. It should have read “the venerable firm of Raymond James,” not “venereal.” Since I no longer have editors I just plain missed it. Second, the mutual fund outflows mentioned in today’s letter rival those of December 2018 and January 2016, both of which were downside inflection points that launched good rallies. Likewise, the Put to Call Ratio mentioned today is also suggestive of a trading bottom. Third, we had a multi-swing morning between plus and minus on the S&P 500. Such action is how bottoms are made. I do not know what the rest of the session will bring, but I think there is a good change we are making a bottom. Indeed, the SPX held support at our designated levels and rebounded. All of this is developing as the bullish retracement we target at the early-May’s “energy peak” that we advised was a downside “polarity flip” since the stock market’s internal energy was TOTALLY used up; and, we said so! As stated, our internal energy models are now fully recharged with our models suggesting 2800 – 2850 should be our first target for the SPX.”

At the time the S&P 500 (SPX/2873.34) was trading around 2729. Over the next few sessions it would climb to 2843. So again, last Thursday our models suggested the equity markets were likely to “stall” into mid-month and we issued another Trading Flash that read:

“Well, with the D-J Industrial down some 200-points on Monday morning we issued a Trading Flash stating a bottom was being formed. The S&P 500 was changing hands at ~2729 and we were bullish on a trading basis. Now, the SPX is roughly 100-points higher and the short-term oversold condition has been corrected and our models are suggesting that the SPX has traveled into overhead resistance and is likely to stall here into the often mention mid/late-June timeframe.”

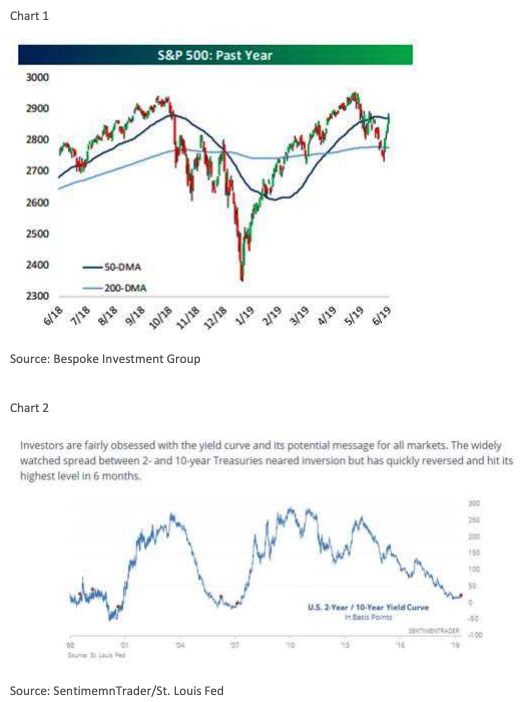

Oops; as the stock market’s fore-reach carried the SPX some 50-points higher into Friday’s session. For you non-nautical types, when you pull the power off on a power boat the vessel stops almost immediately. However, when you pull the power off on the much sleeker sailboat, the boat keeps traveling forward for a much longer time than one would expect . . . aka, fore-reach. In this case, the SPX tagged ~2884 on its intraday high last Friday (chart 1). And don’t look now, but the SPX looks like it has traced out a reverse head-and-shoulders bullish chart pattern. Regrettably, our models are not always right, nothing is, but they are right a lot more than they are wrong. And as often stated in these missives, in out flying days, when you had zero visibility, you had to depend on your instruments. In the stock market it is much the same.

Over the decades we have come to trust our “instruments” (models) even though they are not right all of the time. The problem this time was our models had no idea rumors would circulate that the tariffs on Mexico might be delayed. Nor did they know that a number on Federal Reserve folks were going to wax dovish on Thursday and Friday. Moreover, they did not glean the much softer than anticipated employment report on Friday. Said report dramatically increased the odds of a Fed interest rate cut in the weeks ahead. If so, stock market pundits will have to recalibrate their price earnings (PEs) assumptions, even though S&P 500 estimates have fallen from $173 for 2019 to roughly $168 currently. Candidly, we think they have been reduced too much. Nevertheless, our models suggest, if the 10-year T’note trades below a yield of 2%, it implies a fair PE multiple for the S&P 500 of 19x earnings. Given that assumption, it implies a price target above 3100 for the SPX, a target we have long embraced.

The “yield curve” discussion came back to the fore last week as we continue to argue the yield curve du jour seems to be the 2-year T’note to the 10-year T’note. We have argued that this is NOT the correct yield curve despite what the internet shows. Still, there is this myopic focus on that curve. However, the real yield curve has/is/and will always be the 90-day T’bill yield to the 30-year T’bond yield. In our system-wide conference calls with the brainy Ned Davis this topic has often been discussed and Ned agrees that 90-day to 30-year is the correct yield curve. That said, our pal Jason Goepfert (the invaluable SentimenTrader Report) wrote last week:

“Investors are fairly obsessed with the yield curve and its potential message for all markets. The widely watched spread between 2- and 10-year Treasuries neared inversion but has quickly reversed and hit its highest level in 6 months. The steepening is often what causes trouble, but when this curve has gone from less than 25 basis points to a 6-month high (chart 2), returns in stocks (and bonds) were not consistently different than random.”

Then there was this from market wizard Leon Tuey:

“Sentiment is a contrarian indicator. Excessive pessimism/fear is witnessed at the bottom of a correction/bear market and excessive optimism is seen at market tops. As the market corrects, bullish sentiment subsides, and bearish sentiment rises and at the bottom of a correction, fear surges. Conversely, as the market rallies, bullish sentiment rises, and bearish sentiment subsides. At the top of the rally, bearish sentiment hits a low ebb and optimism becomes excessive. Great news, Folks! The latest AAII Investor Sentiment Survey showed the BULLS plunged below 25% for the third week which shows extreme pessimism Also, BEARS rose to 42.6% outnumbering BULLS by a substantial margin. Also encouraging is that the CNN Fear & Greed Index has moved from Greed to Fear and further market weakness will drive it to Extreme Fear. On Friday, May 31, it did close at 21 showing extreme fear.”

Leon goes on to write:

“As mentioned, the market's short-term direction is driven by technical and sentiment factors. All other reasons given, even after the fact, there is no way of proving whether they are correct. When the market is overbought, momentum deteriorates, and optimism becomes excessive, the market will consolidate/correct (a la October, 2018 and April, 2019). Conversely, when the market is oversold, momentum improves, and pessimism becomes excessive (December, 2018 and late May, 2019), the market will rally. All can be objectively quantified; no need to guess or waffle. As you know, most don't understand the market's logic and they have no idea what drives the market's short-term direction. Consequently, they react to the headlines and the market gyrations which is irrational and no way to invest. Note that the recent rally is greeted with universal skepticism. The consensus is that the market will range bound. They are talking about the S&P, of course, and not ‘the market’. When the market is oversold and pessimism is pervasive, the market doesn't range bound, it rallies until an overbought condition is reached, then, it corrects.”

Given our bullish “call,” we have been asked what stock ideas we are using. It was a few weeks ago, in a meeting with a portfolio manager who manages $40 billion, who told us his two biggest positions were Ford (F/$9.76) and GE (GE/$9.98). Both of those stocks popped over 10% on better than expected earnings’ reports but have subsequently come back down in the charts and close those upside chart gaps. They are worth your consideration. Further, we have been asked to share some of the ideas gleaned from portfolio managers on our recent NYC tour. Some of the names that make sense to us, and that screen well on our models, include: Fair Isaac (FICO/$313.15), Planet Fitness (PLNT/$77.96), Boot Barn Holdings (BOOT/$28.92) who makes all kinds of boots. But, the boot that is really driving their business is they have the preferred boot for oilfield workers, Heico (HEI/$127.95), and Guardant Health (GH/$90.85).

The call for this week: The SPX has rallied ~5.7% from our bullish Trading Flash of last Monday morning (10:30 a.m.). That rally caused one major investment bank to scribe a report to “Sell the Rip.” Another major firm’s strategist reiterated his call that we are in a bear market, a call he has had for a few years. As Leon Tuey wrote, “As you know, most don't understand the market's logic and they have no idea what drives the market's short-term direction. Consequently, they react to the headlines and the market gyrations which is irrational and no way to invest.” We agree and would remind folks that our Trading Flashes are just that, short-term “trading calls.” Longer-term we have NEVER wavered. We are in a secular bull market that has years left to run. This morning our energy models still suggest a stall for a few sessions, but then a run to new all-time highs. “Fate whispers to the warrior, 'You cannot withstand the storm.' The warrior whispers back, 'I am the storm.'” -- Author Unknown.

Investing/trading involves substantial risk. The author and Saut Strategy do not guarantee or otherwise promise as to any results that may be obtained from using this report. Past performance should not be considered indicative of future performance. No reader should make any investment decision without first consulting his or her own personal financial advisor and conducting his or her own research and due diligence, including carefully reviewing any prospectus and other public filings of the issuer. These commentaries, analyses, opinions, and recommendations represent the personal and subjective views of the author, and are subject to change at any time without notice. The information provided in this report is obtained from sources which the author believes to be reliable.

© Saut Strategy

[email protected]

Read more commentaries by Saut Strategy