Avon’s Historical Operating Results and Price Action

Since 2008 Avon’s earnings have continuously eroded and its stock price has followed. Moreover, after its dividend grew for many years, the company cut it by 18 ½% for 2012, slashed it an additional 68% in 2013 and then eliminated their dividend altogether in 2016. As a result, investing in Avon has been a significant losing proposition for more than a decade.

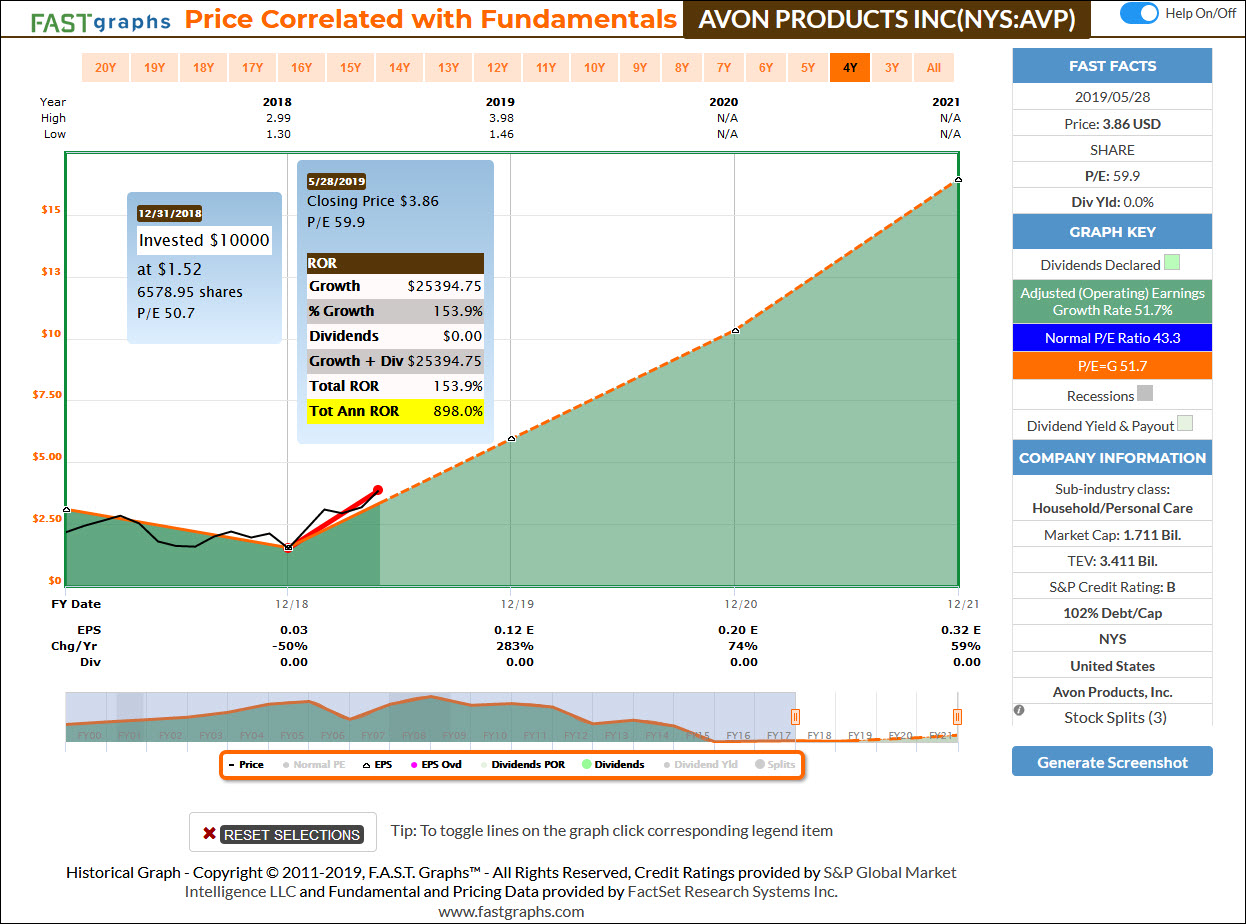

Avon From Value Trap to Growth Stock: Future Earnings Estimates

However, that has changed dramatically thus far in fiscal and calendar year 2019. Year-to-date Avon’s stock has appreciated over 153% from $1.52 per share on December 31, 2018 to $3.86 at the close on May 28. Additionally, per share earnings are forecast to approximately triple from $0.03 a share in 2018 to an estimate of $0.12 a share in 2019.

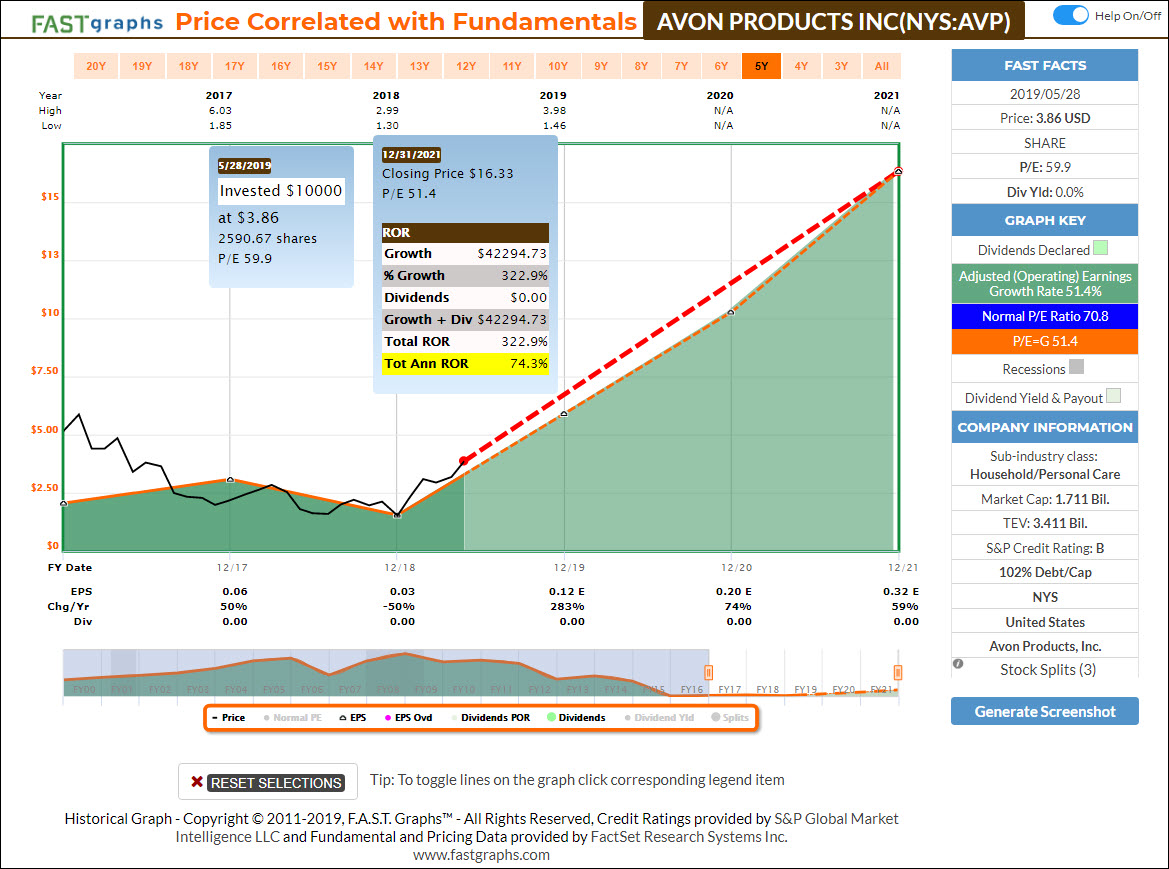

Furthermore, earnings are forecast to grow at an average rate of 51.7% out to 2021. Consequently, at first glance we may apparently be seeing the beginning of a classic value trap morphing into a classic growth stock. If Avon’s earnings were to grow as forecast going forward, courageous investors could reap the extraordinary reward in excess of a 74% total annualized rate of return out to 2021.

However, appearances can be misleading because Natura &Co has announced a pending buyout of Avon at what appears to be a 28% premium over current value. The following announcement summarizes the potential transaction:

“Natura &Co and Avon join forces to create a Direct-to-Consumer global beauty leader

Company Release – 5/22/2019 5:56 PM ET

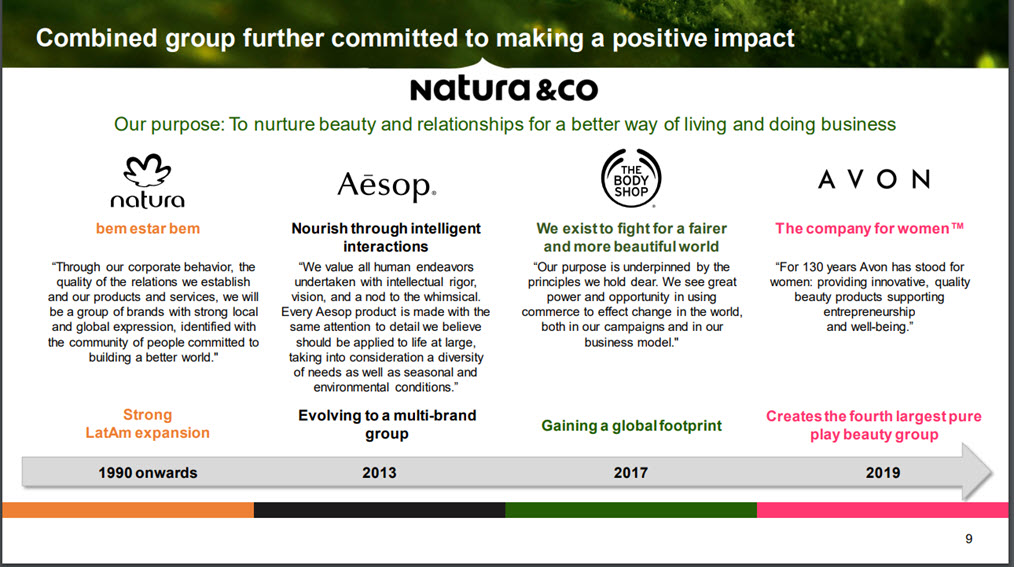

SÃO PAULO and LONDON, May 22, 2019 /PRNewswire/ — Natura &Co (B3: NATU3) announces that it is acquiring Avon Products, Inc. (NYSE: AVP) in an all-share transaction, creating the fourth-largest pure-play beauty group in the world and a major force for good in the industry.

The combination creates a best-in-class multi-brand and multi-channel beauty group, with direct connections to consumers on a daily basis. The group will hold leading positions in relationship selling through Avon´s and Natura’s over 6.3 million Consultants and Representatives, a global footprint through 3,200 stores, as well as an expanded digital presence across all companies. The combined Group is expected to have annual gross revenues of over US$10 billion, over 40,000 associates and be present in 100 countries.”

Although the deal seems very likely to happen in early 2020, it is not yet a done deal. The following press release from Avon illustrates that the deal has not yet been agreed upon, but again, would indicate that a transaction is likely to occur.

“Avon Comments in Response to Natura Announcement

Company Release – 5/22/2019 8:50 AM ET

LONDON, May 22, 2019 /PRNewswire/ — Avon Products, Inc. (NYSE:AVP) (“the Company”), a globally recognized leader in direct selling of beauty products, today confirmed the Company is in advanced discussions with Natura & Co. (BVMF: NATU3) regarding a potential all-stock transaction.

There can be no assurance any transaction will result from these discussions. Avon does not intend to make any additional comments regarding these discussions unless and until it is appropriate to do so, or a formal agreement has been reached.”

Here is a link to the presentation posted on May 23, 2019 that outlines the potential transaction:

The following slide summarizes the value of the transaction to both Avon and Natura &Co shareholders:

Furthermore, if the deal is consummated, the combined company intends to list their shares on the New York Stock Exchange as an ADR level II.

However, it should be noted that Natura Cosmeticos SA has not traded on a US stock exchange since March 25, 2015. Consequently, I believe this does provide vagary relative to what the potential deal might mean to Avon shareholders:

Avon Has Been Dynamically Restructuring

Prior to the announcement of the above acquisition by Natura, Avon products had been actively reorganizing its business. On April 25, 2019, Avon announced that they had entered into a transaction where Avon North America would be acquired by LG Household and Healthcare Limited as follows:

“Avon Products Comments on Avon North America Transaction

Company Release – 4/25/2019 2:29 AM ET

LONDON, April 25, 2019 /PRNewswire/ — Avon Products, Inc. (NYSE: AVP) (“Avon Worldwide”), a globally recognised leader in direct selling of beauty products, today commented on the announcement by New Avon LLC (“Avon North America”), that it has entered into an agreement to be acquired by LG Household & Health Care Ltd. (LG H&H).

In March 2016 Avon’s North American business was separated into a privately-held company — New Avon — as a result of a strategic partnership transaction between Avon Worldwide and an affiliate of Cerberus Capital Management, L.P. (“Cerberus”). Avon North America is majority-owned and managed by Cerberus. Avon Worldwide retained a minority interest in Avon North America which LG H&H will acquire as part of its transaction.”

FAST Graphs Analyze Out Loud Video:

The following analyze out loud video puts a clear perspective on Avon’s historical price action and operating results. It also will look at Avon’s potential growth going forward if it were to remain an independent company. However, as presented above, that seems unlikely due to the pending acquisition by Natura.

Summary and Conclusions

It should be clear from the above information that Avon has clearly been a company in transition and transformation. Prior to the announced acquisition by Natura, the consensus of leading analysts seemed to be positive that the reformed Avon Products Inc. had the potential to grow again. Therefore, that growth may also be transferable to the new company as it becomes a part of the Natura family of brands.

Nevertheless, I think the most important question that prospective investors need to ask, and answer, is whether (or not) the potential premium is worth speculating on. Additionally, prospective investors must also decide whether (or not) they would want to be an owner of the combined companies if the transaction does in fact go through. Personally, I have my doubts. However, I will let the reader decide for themselves.

Disclosure: No position.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.