N THIS ISSUE:

1. Household Debt Hit New Record High in the 1Q

2. While Total Debt Rose, Balance Sheets Strengthened

3. Fed Minutes Dashed Hopes For Rate Cut This Year

Overview

Today we’ll look at new Fed data which showed that US household debt hit a new record high in the first quarter, marking the 19th consecutive quarterly increase in debt held by American families. However, that same report noted that household balance sheets improved over the same period. How can that be, you might ask? I’ll explain as we go along.

Following that discussion, we’ll look at the minutes from the latest Fed Open Market Committee meeting earlier this month. Those minutes clearly indicate the Fed has no plans to cut interest rates this year. This disappointed many who had been hoping for a rate cut before year-end, but not my readers. Twice in April I predicted there would be no rate cut this year.

Finally, I have a challenge for clients and readers who pick their own stocks at the end of today’s E-Letter. It will be interesting to see how many take me up on it!

Household Debt Hit New Record High in the 1Q

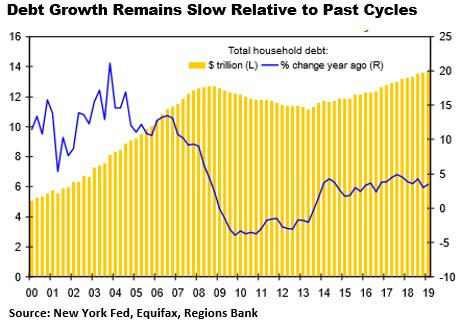

The Federal Reserve Bank of New York, in conjunction with Equifax, released their latest quarterly report on trends in household debt last week. Total household debt rose to a new record high of $13.668 trillion in the 1Q, a $124 billion increase from Q4 2018. At $13.668 trillion, the level of outstanding household debt stands 7.83% above the prior cyclical peak of $12.675 trillion seen in Q3 2008.

Total household debt was up 3.46% year-on-year in the 1Q, which is considerably slower than that seen in some prior cycles. Still, it was the 19th consecutive quarterly increase in outstanding household debt.

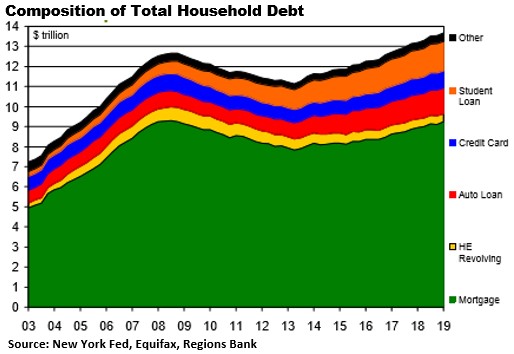

Outstanding mortgage balances rose by $120 billion in the 1Q, with student loan balances up by $29 billion and auto loan balances up $6 billion, while outstanding balances on credit cards, home equity lines, and other forms of household debt fell.

In the 1Q, mortgage debt accounted for 67.6% of total household debt, with student loan debt accounting for 10.9%, auto loan debt accounting for 9.4%, credit card debt accounting for 6.2%, revolving home equity lines accounting for 3.0%, and the “Other” category accounting for 2.9%.

While Total Debt Rose, Balance Sheets Strengthened

While the 1Q saw (yet) another record-high level of total household debt, the good news is that household balance sheets improved to the strongest level in years. While household debt continued to increase, balance sheets (assets minus liabilities) continued to strengthen. This means the value of households’ assets rose more than their liabilities.

Meanwhile, loan performance improved modestly in the 1Q, with 4.56% of all outstanding debt in some stage of delinquency, compared to 4.65% as of 4Q 2018. In terms of dollar volume, there was $623 billion of delinquent household debt as of Q1, which is lower than the totals in the prior two quarters.

One way to gauge households’ ability to meet debt service obligations is to look at disposable after-tax personal income, excluding transfer payments (Social Security, pensions, welfare, alimony, student grants, etc.). As of 1Q 2019, the level of disposable personal income was 41.8% above its prior cyclical peak in 2008, according to the Fed’s data. This large increase was due to the fact that the current expansion is the second longest in history (soon to be the longest), and that many households deleveraged in the wake of the Great Recession.

What has long been the more relevant story is that the aggregate household debt-to-income ratio has continued to fall, household debt service burdens remain near historical lows and delinquencies on household debt remain notably low. The bottom line is that, while by no means perfect, household balance sheets on average are in better condition today than has been the case for quite some time. You don’t hear that in the mainstream media!

Fed Minutes Dashed Hopes For Rate Cut This Year

Back in January when Fed Chairman Jerome Powell said the Fed would be “patient” and hold off on further interest rate hikes, investors took that to mean no rate hikes this year. Many forecasters took it a step further and began to call for a rate cut this year.

The Fed Funds futures market, an indication of what the Fed will do next, began a significant rise suggesting a rate cut this year. Earlier this month, the Fed Funds futures were signaling a 75% chance the Fed would cut rates this year, despite the fact that the Fed has not even hinted it might consider a rate cut. 75% odds of a rate cut – you’ve got to be kidding!

Regular readers will recall that I have never bought into the rate cut this year circus. In fact, I went on the record in these pages – on April 2 and again on April 30 – saying I did NOT believe the Fed would cut rates this year.

I mention this because last Wednesday the Fed Open Market Committee (FOMC) released the minutes from its May 1-2 policy meeting, the contents of which should dash the hopes of the rate cut crowd. Federal Reserve officials remained firmly committed to a “patient” policy stance at their meeting earlier this month, saying rates likely will remain unchanged well into the future.

The minutes also revealed that the FOMC raised its forecast for full-year economic growth and said that earlier concerns they had about a slowdown had abated. Despite their general optimism, the committee held the line on interest rates, primarily citing a lack of inflation pressures that allow the central bank to continue to watch how events unfold before making any further moves, indefinitely.

“Members observed that a patient approach to determining future adjustments to the target range for the federal funds rate would likely remain appropriate for some time, especially in an environment of moderate economic growth and muted inflation pressures…”

That alone should be enough to give the rate cut crowd pause. But the language in the minutes got even more disappointing for them. There was even some push for higher rates this year. The minutes noted “a few” members saying that if the economy continued to progress, the Fed would need “to firm” its policy (ie – raise rates) to keep inflation in check.

In the end, the FOMC members voted unanimously to keeping the Fed Funds rate unchanged. The Fed is holding its benchmark overnight funds rate in a target range of 2.25% to 2.5%.

It’s too early to know how well the economy is performing in the current April-June quarter – we won’t get our first official estimate until late July. But if we get a 2Q GDP estimate that is above 3% (it was 3.2% for the 1Q), I believe there could be more than a few FOMC members suggesting a rate hike at the July 30-31 FOMC meeting.

The bottom line is that the FOMC would like to raise the Fed Funds rate several more times so that it has more room to lower the rate whenever we hit the next economic slowdown or recession. They are not inclined to cut the rate with the economy as strong as it is today.

I’m not predicting a rate hike this year. As long as the Fed’s preferred inflation gauge, the core (less food and energy) Personal Consumption Expenditures Index, does not rise well above 2%, I think Fed Chair Powell will insist on holding the Fed Funds rate steady at least through the end of this year.

Best regards,

Gary D. Halbert

© Halbert Wealth Management

© Halbert Wealth Management

Read more commentaries by Halbert Wealth Management