I find it serendipitous that after just completing a 19-part series on how highly valued the general market is, I get the pause that refreshes. Now please don’t read more into my words than are being offered. I still believe that the market at large is fully valued. Consequently, finding great companies at great values is still rare and hard to do. However, after Monday’s swoon, we are finally (at least I am) starting to see some value coming into focus on some of my favorite companies. Therefore, I can finally feature some of my favorite companies that have become good value choices.

3M Company (MMM) is a case in point. There are a lot of valid reasons to like 3M, therefore, it’s no surprise that many dividend growth investors do. Although I am a long-term fan of the business, as a value investor, I have not been a fan of the stock for more than 2 ½ years. However, that changed as of yesterday. Today, I consider 3M fairly-valued but not necessarily cheap – at least yet. Stated more directly, I consider 3M a sound investment today based on quality and valuation.

This leads me to a brief discussion on what my personal experience suggests is a common misconception about quality stocks at attractive valuations. Just because a company becomes fairly- valued does not simultaneously suggest that it is also a great investment. It may now be sound and prudent, but still not be capable of generating exceptionally high rates of return. This is how I currently see 3M Company. Because it has moved into fair valuation territory, I have added it to my buy watch list. However, I am still not quite ready to lay my money down, but I am close. Therefore, I will be watching it carefully looking for an entry point that I believe would make it both a good company and a good investment.

Investment Thesis: Short and Long-Term Perspective

I never invest in any stock without first calculating a specific and precise forecast of what future returns I might expect. In other words, I never buy a stock simply hoping that it will go up, or in hopes that it might raise its dividend over time. Instead, I attempt to assemble as much relevant information as I can that will support a thesis for growth and/or sustainability. Furthermore, I utilize this information to run my expected future return numbers out to their most logical conclusion.

Additionally, I go through this exercise from a best, worst and most likely expectation. Future returns can never be precisely calculated. However, rational forecasts supported by data can provide a reasonable level of expectations that are highly likely to unfold within an acceptable range or level. So, this might beg the question, how do I do that, or what’s the process? The central idea is to simply run your growth expectations out to their logical conclusions and apply rational valuation methodologies to the numbers. In the FAST Graphs analyze out loud video later in this article, I will cover this process extensively.

Moreover, I will not rely on one single metric in order to attempt to make my determination of what my future returns might be. Instead, I will look at 3M utilizing numerous earnings and cash flow metrics to include EV/EBITDA. Finally, the critical point I’m attempting to illustrate is that I am not offering an opinion on 3M. Instead, I am analyzing factual data that enables me to offer real world calculations based on fundamentals and sound principles of valuation. Consequently, this allows me to keep my emotions out of the equation and think analytically instead.

About 3M Company

The following overview and description of 3M is provided courtesy of the Wall Street Journal:

“Description 3M Co.

3M Co. is a technology company, which manufactures industrial, safety and consumer products. It operates through the following five segments: Industrial, Safety & Graphics, Health Care, Electronics & Energy, and Consumer.

The Industrial segment provides products, including tapes, abrasives, adhesives, ceramics, sealants, closure systems for personal hygiene products, acoustic systems products, specialty materials and filtration systems.

The Safety & Graphics segment offers personal protection products, ransportation safety products, commercial graphics systems, commercial cleaning and protection products, floor matting, roofing granules, all protection products, self-contained breathing apparatus systems, and gas and flame detection instruments.

The Health Care segment supplies medical and surgical equipment, skin health & infection prevention products, drug delivery systems, dental & orthodontic products, health information systems and food safety products.

The Electronics & Energy segment involves in the optical films solutions for electronic displays, packaging and interconnection devices; insulating and splicing solutions; touch screens and touch monitors; renewable energy component solutions; and infrastructure protection products.

The Consumer segment products includes sponges, scouring pads, high-performance cloths, consumer and office tapes, repositionable notes, indexing systems, home improvement products, home care products, protective material products, and consumer & office tapes, as well as adhesives.

The company was founded by Henry S. Bryan, Hermon W. Cable, John Dwan, William A. McGonagle and J. Danley Budd in 1902 and is headquartered in St. Paul, MN.”

3M’s business playbook is reasonably well diversified across all their business segments. The following slide taken from 3M’s website illustrates the relative contributions that each of their operating segments contribute to the company’s growth and success:

According to MorningStar, 3M is a wide moat company that they refer to as a GDP- plus business. The following quote illustrates 3M’s commitment to future growth:

“In 3M’s case, the “plus” is a testament to the value-additive nature of the company’s products, churned out by its virtually inimitable research and development platform. Unlike many diversified industrials companies, 3M has committed to leveraging innovation across its disparate businesses, making it worth more than the sum of its parts. This commitment manifests itself in the apportionment of just under 6% of net sales to R&D, which we expect to increase toward 6% by 2023. We forecast the firm will earn just under $9 in gross profit for every dollar spent on R&D. Our forecast is relatively in line with recent experience, which historically has been significantly greater than other highly innovative firms.”

To summarize, MorningStar considers 3M to be one of the most innovative diversified industrial firms in the world. In addition to committing a significant portion of sales to R&D, the company holds over 112,000 global patents (9,000 awarded since 2001) and offer over 55,000 products that touch virtually every industry. Additionally, MorningStar believes that 3M’s strong brands in its manufacturing scale allow it to be a low cost producer thereby enhancing their profitability.

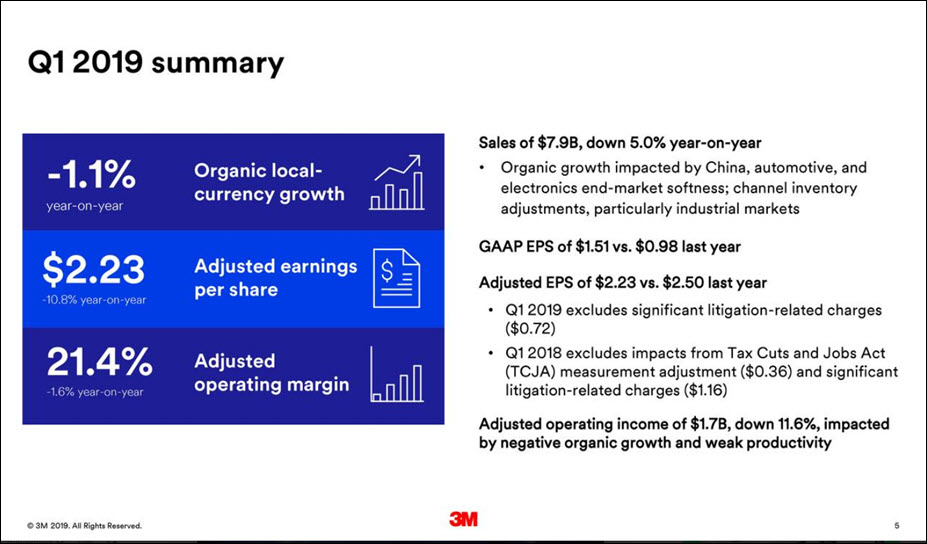

Nevertheless, as indicated in their 1st quarter 2019 earnings call, 3M has admitted to a disappointing start to the year. However, they are also suggesting they will be taking aggressive action to get back on track. The following Q1 2019 summary slide indicates the current weakness in 3M’s businesses. Of course, the real question will be if this is a temporary phenomenon or something more permanent in nature:

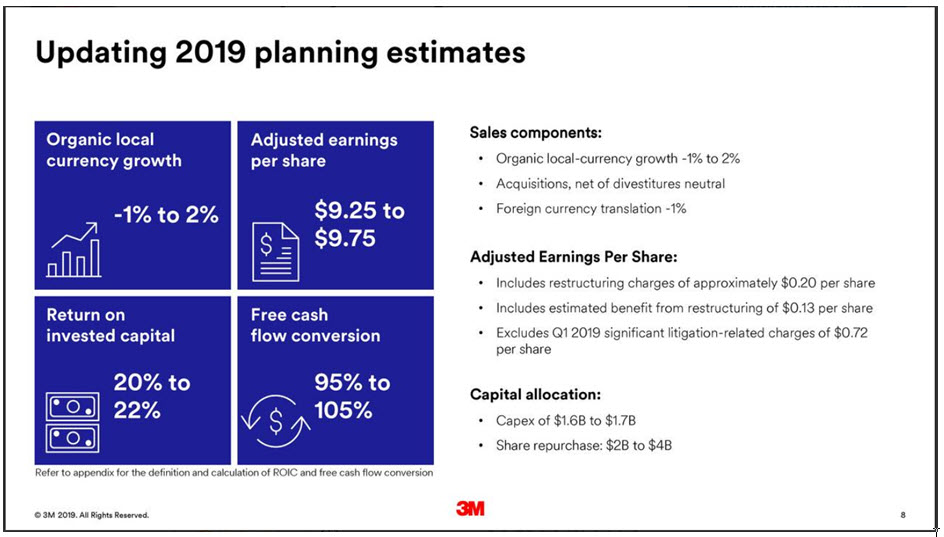

3M also provided disappointing guidance for 2019. As I previously discussed, 3M was a great company that was significantly overvalued throughout 2017 and fully valued for most of 2018. On May 31, 2018 I penned an article titled “3M Company: It Didn’t Take A Crystal Ball to See That It Was Overvalued.” Therefore, the company’s high valuation made it vulnerable to the bad news which includes negative earnings growth for 2019. Furthermore, as I will discuss later in the video, because I do not consider 3M’s valuation attractive enough, I am not supportive of the company’s share repurchase plans suggested under the capital allocation portion of the following slide:

Later in the FAST Graph analyze out loud video I will illustrate both near-term valuation models and their impact on returns as well as running calculations on 3M’s long-term return potential based on its current valuation levels.

3M FAST Graph Analyze Out Loud Video: Fundamental Analysis By The Numbers

Before I conduct a comprehensive research and due diligence process on a company, I first run it through various fundamental metrics in order to determine if it’s research worthy. For a company to be research worthy, it needs to be available at a reasonable valuation based on multiples of important fundamentals such as cash flows and earnings. If it’s not, I am not going to waste my time and energy researching it further no matter how much I like the business. Valuation matters and it matters a lot.

However, I do not rely on any single metric to make that determination. Instead, I attempt to evaluate all the valuation methodologies at my disposal. In the following video, I will be running 3M through the valuation model paces utilizing various earnings and cash flow metrics. Since 3M is a Dividend Aristocrat I will also be looking for dividend sustainability and safety in addition to valuation. Finally, I am analyzing the data past, present and future in order to make the determinations described above. Simply stated, I am attempting to identify and evaluate real world historical multiples and then make rational forecasts based on the conclusions drawn from my analysis. Frankly, I believe the meat of this article is in the following video. Therefore, I suggest and ask that you please take advantage of the insights it provides.

Summary and Conclusions

The bottom line is that 3M has recently become a prudent and sound investment based on the principles of valuation and considering the extreme quality of this Dividend Aristocrat. Regarding whether (or not) it has simultaneously become an excellent investment requires judgment on the investor’s part. If you assume that Mr. Market will soon apply a quality premium valuation based on operating earnings, as it historically has, then 3M would meet the definition of an attractive blue-chip dividend growth stock. On the other hand, if you believe that a true reversion to the mean will be more permanent, then 3M would only produce below average total returns going forward.

Additionally, there is the question of your investment objectives. If you’re investing for current dividend income, then 3M would make sense at current levels and yields. Furthermore, if you’re investing for future dividend growth, 3M would also make sense on that basis. But as stated above, above-average total return would be more of a challenge.

Moreover, if you are an active trader, you should be concerned about 3M’s current operating weakness. On the other hand, if you are a long-term oriented investor, you might take solace in the company’s long legacy of quality and performance, and even be willing to accept some additional short-term pain if it were to occur.

In the final analysis, 3M is an extraordinarily high-quality blue-chip dividend growth stock. In addition to paying an uninterrupted dividend for more than 100 years, 3M has increased its dividend for more than 60 consecutive years. Furthermore, based on operating cash flow and free cash flow coverage of the dividend, it seems rational to assume that the dividend is both sustainable and safe. In closing, and as always, caveat emptor.

Disclosure: No position.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.