This is part 19 and the final part of my series covering all the various sectors reported by FactSet. However, the popular idea of saving the best for last does not apply in this instance. As I indicated throughout each installment, there were some sectors that I felt offered better investment opportunities than others. Furthermore, I attempted to indicate that growth coupled with purchasing that growth at a reasonable valuation was a major key to long-term investment success. Stated very simplistically, a faster growing company will generate significantly more future cash flows (and dividends if they apply) than a slower growing company will. It’s not only common sense, it’s mathematical reality.

With that said, the Utilities Sector is largely recognized as being comprised of some of the slowest growing companies in all the market. However, the Utilities Sector is also recognized as providing higher levels of dividend income than the average dividend paying company. Consequently, there are many investors that have historically and are currently utilizing utility stocks as bond alternatives. However, please don’t be confused by that statement. This is not the same as saying that utility stocks are as safe as bonds. Instead, this simply implies that utility stocks offer higher yields than the average stock and thereby provide some of the benefit that bonds traditionally have offered.

Furthermore, people are looking to utility stocks because even though they tend to be low growth entities, the good ones do have a legacy of increasing dividends each year. Therefore, although bonds provide the theoretical safety of having your original investment returned at the end, they do not necessarily provide the security of protecting your purchasing power. Inflation eats at both the income you receive from a fixed investment and the future purchasing power as well. Consequently, an alternative option such as utility stocks can provide an inflation fighting rising dividend income stream, as well as modest capital appreciation.

Low Growth Utility Stocks and The Importance of Valuation

Regular readers of my work know that I am literally obsessive-compulsive about only investing when valuation makes sense. However, valuation is even more critical when investing in slow growing investments such as utility stocks. One of the primary advantages of only being willing to invest at fair valuation is that it positions you to earn returns that are consistent with the operating results that the company produces.

Investing when overvaluation is manifest reduces your returns while investing when undervaluation is manifest can increase them. Therefore, when growth potential is low there is little to no margin of error or safety. If you even slightly overpay for a slow growth stock such as a utility, you are very likely to earn unsatisfactory long-term returns. Moreover, you will earn these lower returns at elevated levels of risk. Higher risk and lower returns are the exact opposite of what prudent investors seek.

The key to understanding this is to understand the realities of compounding. Any investment is ultimately worth the amount of cash flows or earnings that it can generate for its stakeholders. In simple terms, a slow-growing entity such as a utility stock does not produce a large enough stream of future cash flows to provide a margin of safety. Therefore, even the slightest miscalculation can devastate future returns. In contrast, a faster growing entity produces a much larger future stream of income thereby providing a greater margin of safety. Of course, that assumes that the faster growth does manifest. I will be expanding on this in the analyze out loud video later in the article.

A Sector By Sector Review

This is part 19 – the final installment in my series where I have conducted a simple screening looking for value over the overall market based on industry classifications and subindustry classifications reported by FactSet Research Systems, Inc.

In this part 19 I will be covering the Utilities Sector.

In each article in this series I provided a listing of screened research candidates from each of the following industry sectors, the sector I’m covering in this article is marked in green:

Sector 19: Utilities

Electric Utilities

Gas Distributors

Water Utilities

Alternative Power Generation

A Simple Valuation and Quality Screening Process

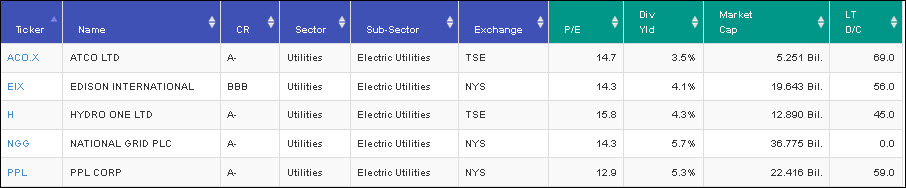

With this series of articles, I have presented a screening of companies that have become attractively valued primarily as a result of the bearish market activities experienced in 2018 from each of the above sectors. I’ve applied a rather simple valuation and quality-oriented screen across each of the sectors. First, I screened for investment-grade S&P credit ratings of BBB- or above. Next, I screened for low valuations based on P/E ratios between 2 and 17. Finally, I screened for long-term debt to capital no greater than 70%.

By keeping my screen simple, and at the same time rather broad, I was able to identify attractively valued research candidates that I might have overlooked through a more rigorous screening process. In other words, I’m looking for fresh ideas that I might have previously been overlooking. Furthermore, I want to be clear that I do not consider every candidate that I have discovered as suitable for every investor. However, I do consider them all to be attractively valued. Additionally, I also believe that every investor will be able to find companies to research that meet their own goals, objectives and risk tolerances within this series.

Portfolio Review: Utilities Sector: 5 Research Candidates

FAST Graphs Screenshots of the 5 Research Candidates

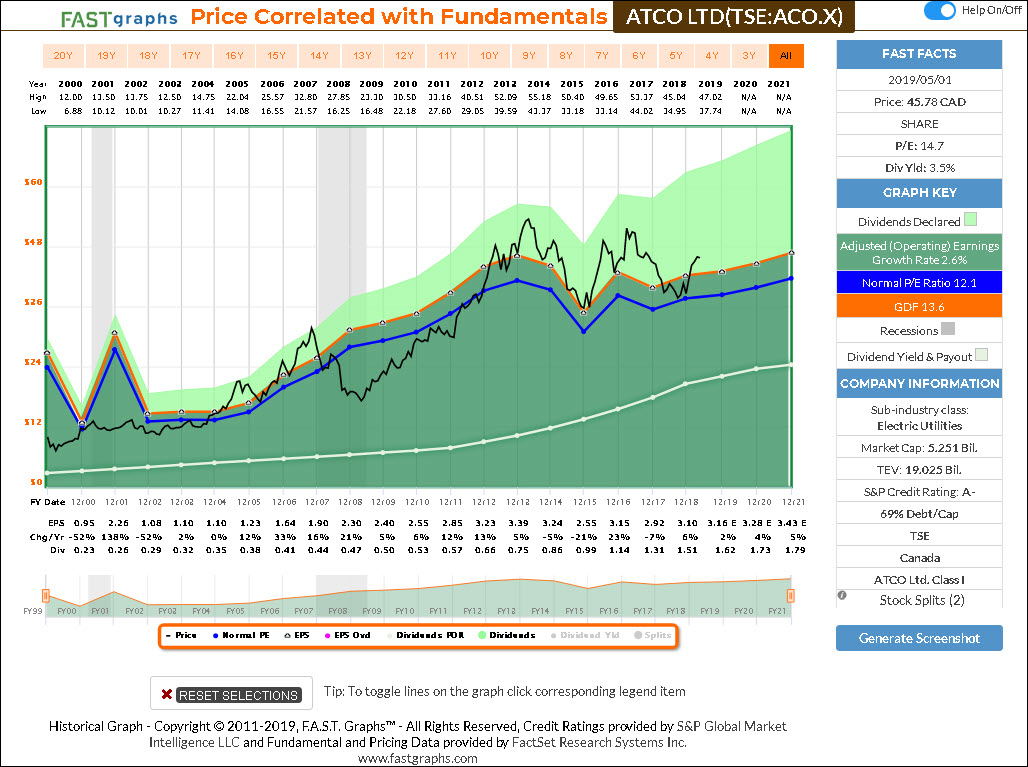

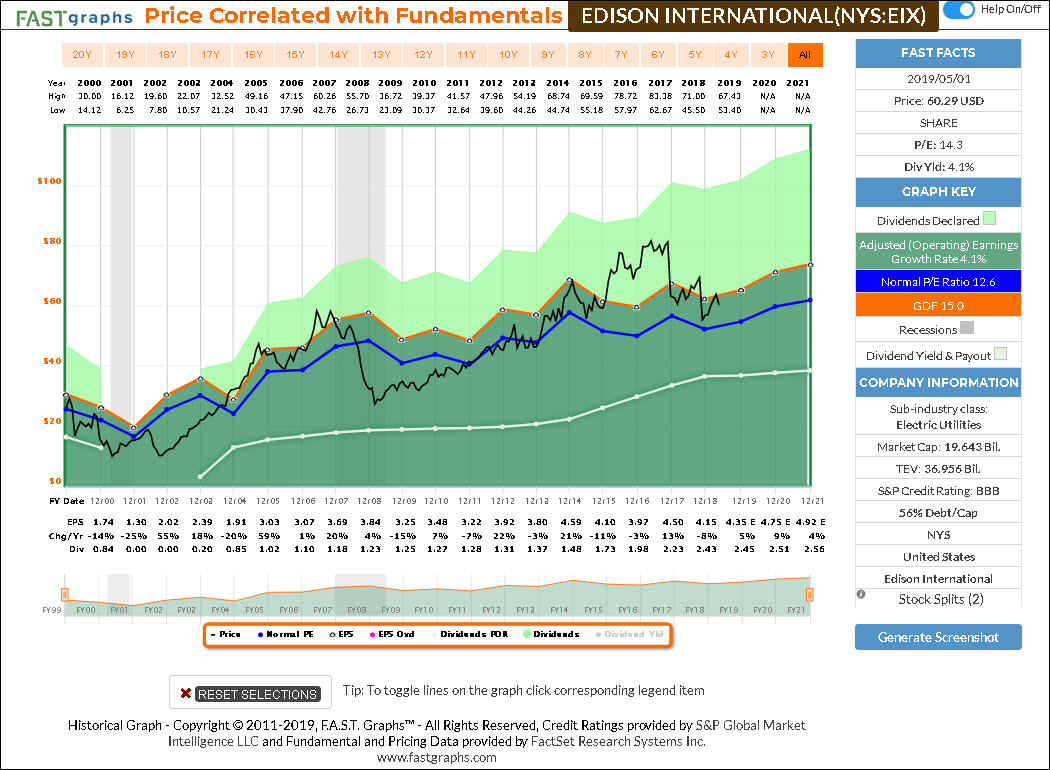

The following screenshots provide a quick look at each of the 5 candidates screened out of over 19,000 possibilities. However, there are only 257 companies categorized as Utilities, and these 5 were the only ones I was comfortable presenting in this article. The company descriptions are provided courtesy of the Wall Street Journal. In the FAST Graphs analyze out loud video that follows the screenshots, I will provide additional details and thoughts on the possible attractiveness as well as the potential negatives of each of these research candidates.

ATCO Ltd (TSE:ACOX)

ATCO Ltd. is engages in structures and logistics, utilities and ports & transportation logistics business. It operates through the following segments: Structures & Logistics, Electricity, Pipelines & Liquids, Neltume Ports and Corporate & Other. The Structures & Logistics segment provides workforce housing, innovative modular facilities, construction, site support services, and logistics and operations management.

The Electricity segment includes ATCO Structures & Logistics. This company offers workforce housing, modular facilities, site support services and logistics and operations management. The Pipelines & Liquids segment includes ATCO Gas, ATCO Pipelines, ATCO Gas Australia, and ATCO Energy Solutions. These businesses provide integrated natural gas transmission, distribution and storage, industrial water solutions and related infrastructure development throughout Alberta, the Lloydminster area of Saskatchewan, Western Australia and Mexico.

The Corporate & Other segment includes commercial real estate owned by the company in Alberta and ATCO Energy, a retail electricity and natural gas business in Alberta. The Neltume Ports segment includes the equity interest in Neltume Ports S.A., a port operator and developer in South America.

The company was founded by S. D. Southern and Ronald D. Southern on February 14, 1947 and is headquartered in Calgary, Canada.

Edison International (EIX)

Edison International is a renewable energy company, which through its subsidiaries, generates and distributes electric power, and invests in energy services and technologies.

The company was founded on July 4, 1886 and is headquartered in Rosemead, CA.

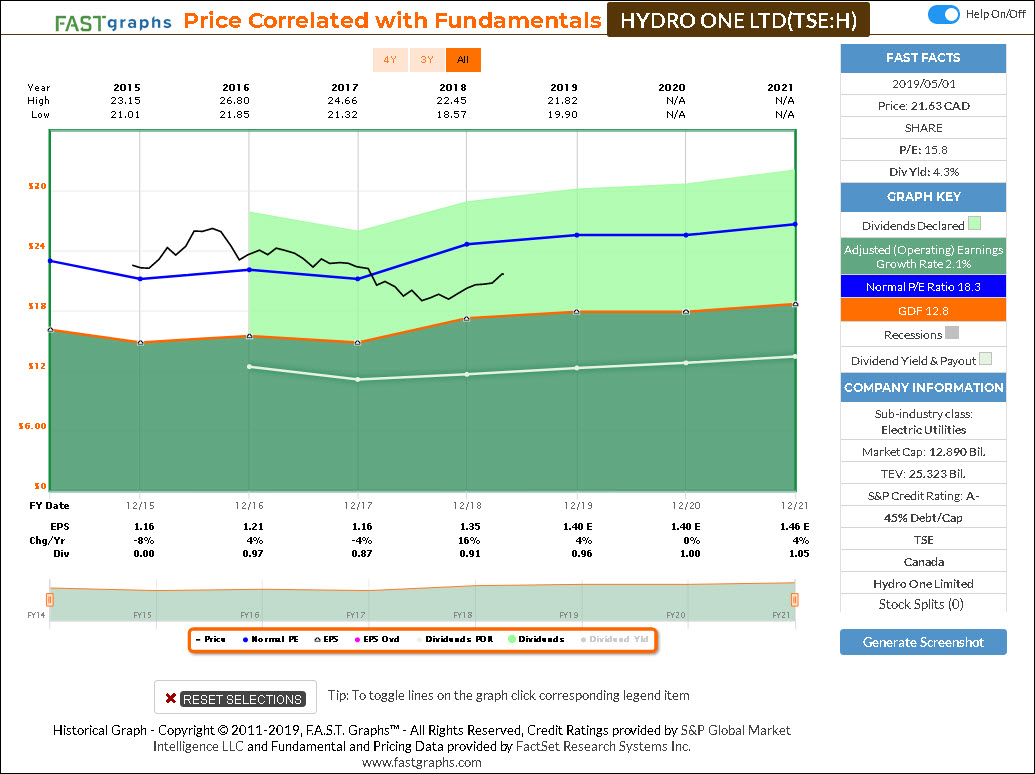

Hydro One Ltd (TSE:H)

Hydro One Ltd. engages in the transmission and distribution of electricity. The company was founded on August 31, 2015 and is headquartered in Toronto, Canada.

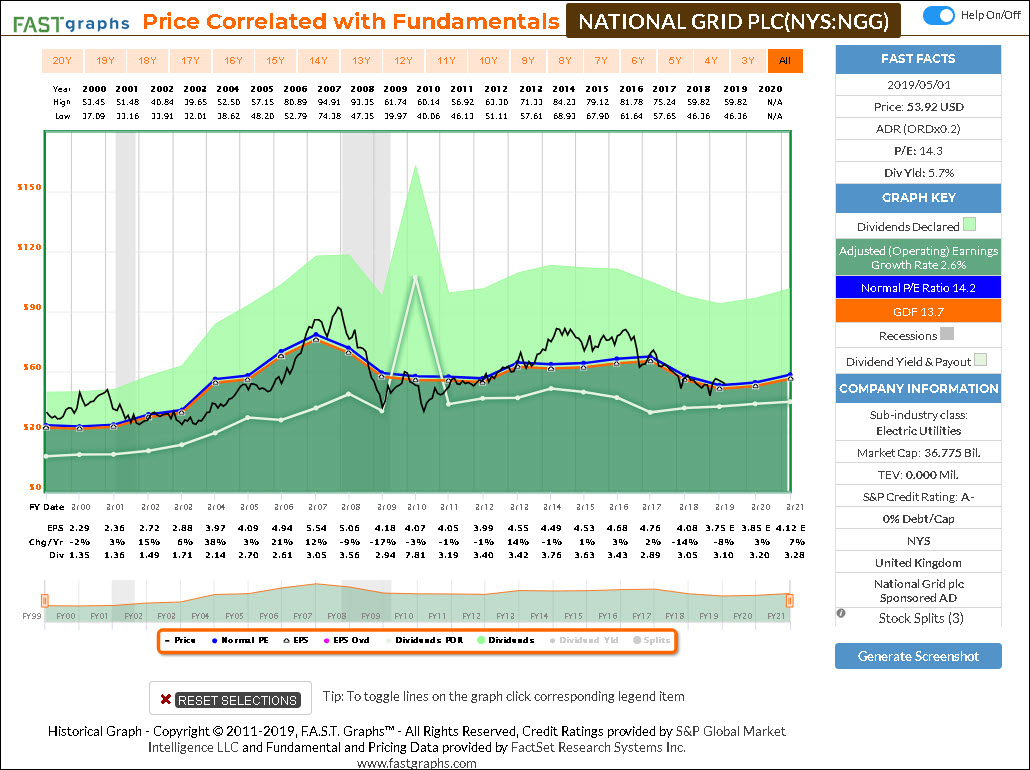

National Grid Plc (NGG)

National Grid Plc engages in the transmission and distribution of electricity and gas. It operates through the following segments: UK Electricity Transmission, UK Gas Transmission, and U.S. Regulated. The UK Electricity Transmission segment engages in electricity transmission in England and Wales.

The UK Gas Transmission segment owns and operates the gas national transmission system in Great Britain, with day-to-day responsibility for balancing demand. The U.S. Regulated segment owns and operates electricity distribution networks in upstate New York, Massachusetts, and Rhode Island.

The company was founded in 1989 and is headquartered in London, the United Kingdom.

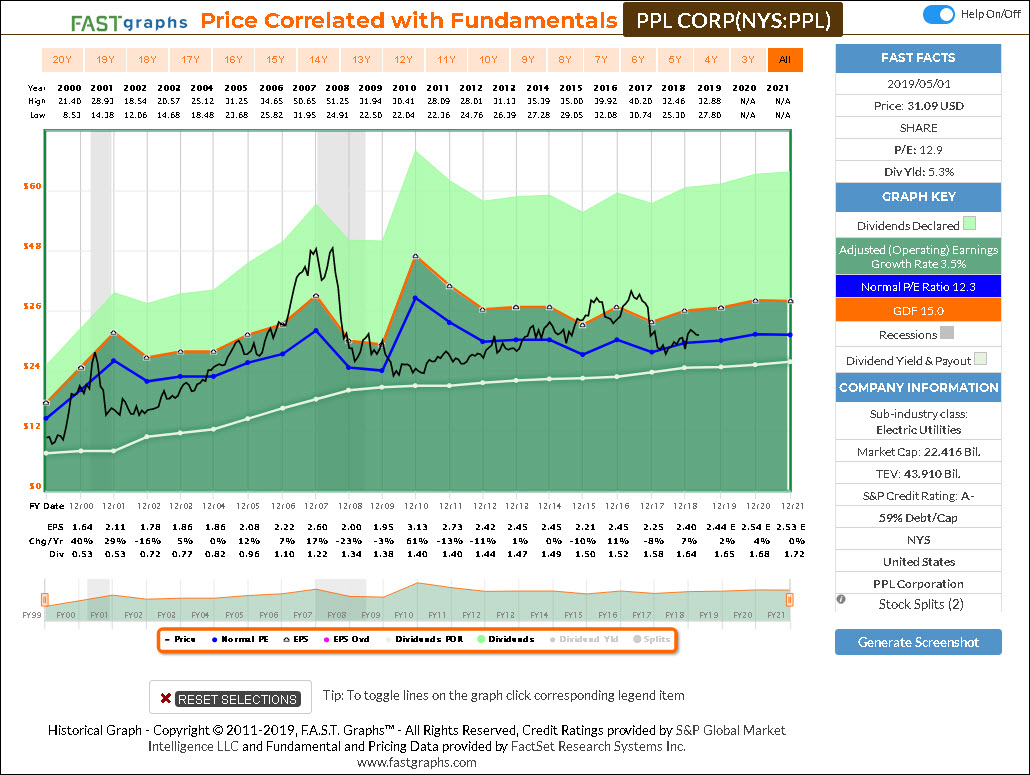

PPL Corp (PPL)

PPL Corp. is a utility holding company, which engages in the generation, transmission, and distribution of electricity. It operates through the following segments: U.K. Regulated, Kentucky Regulated, and Pennsylvania Regulated. The U.K. Regulated segment includes regulated electricity distribution operations of Western Power Distribution.

The Kentucky Regulated segment comprises of LKE’s regulated electricity generation, transmission, and distribution operations of Louisville Gas and Electric Company and Kentucky Utilities Company; as well as regulated distribution and sale of natural gas of Louisville Gas and Electric Company. The Pennsylvania Regulated segment consists of regulated electricity transmission and distribution operations of PPL Electric Utilities Corporation.

The company was founded in 1994 and is headquartered in Allentown, PA.

F.A.S.T. Graphs Analyze Out Loud Video

Summary and Conclusions

This is the 19th and final installment in my series looking for valuation over all the sectors covered by FactSet. From my point of view, the Utility Sector is one of the, if not the most unique of all sectors. Although there are a lot of differences between one utility stock to the next, there are also a lot of similarities. Regarding valuation, the five companies I covered in this article were all electric utilities. This was only because I could not find much value in any of the other utility subsectors. However, that is not too different than what I experienced with the other 18 sectors. The general market is highly valued, therefore, finding fair value in any sector has been a challenge.

With that said, there are some excellent utility stocks that I like and have invested in. Next Era Energy (NEE) and Wisconsin energy (WEC) are two of my favorites. However, their valuations have become extremely high in my analysis and conclusions. Consequently, they were not mentioned in this article although they should have been had their valuations made any sense at all. I bring this up to be clear that I am not recommending any of the stocks covered in this article. Instead, I am simply suggesting that these might be some of the best valued utility stocks, even though they might not be great long-term investment choices.

Series Summary and Conclusions

I hope the reader enjoyed this series of articles covering various sectors, and even more I hope that this series provided some additional insights in the degree of diversity among various common stocks. As I’ve stated throughout, I do believe it is a market of stocks and not a stock market. Nevertheless, I think it’s also important to recognize that attractive valuations are difficult to find after such a long-running bull market. More importantly, finding value in best-of-breed companies is even more difficult. Consequently, prudent investors might need to make some compromises in the quality characteristics of the companies they need to invest in.

Generally speaking, I believe in investing in the highest quality companies your mind can conceive and/or identify. However, and at the same time, I also believe that even the best of companies can become dramatically overvalued. Unfortunately, I believe that is the general state of the equity markets today. On the other hand, that doesn’t mean that good value and excellent long-term investments can’t be found. Because, as I’ve attempted to illustrate over this series, there are many good investments out there. Simply stated, it is simply harder to find good value in a bull market than it is in a bear market. Nevertheless, it doesn’t make any sense to overpay for even the best of companies. Additionally, it doesn’t make any sense to invest in bad companies either regardless of valuation. Nevertheless, if you find a good company, maybe not a great company, at an attractive valuation it can be more prudent to invest in it than to invest in a higher quality company at a much higher valuation. The simple point is that valuation matters, and it matters a lot.

Finally, allow me to conclude this series with a lament that is rooted in why I have written this series. After almost 50 years as an investment advisor, the number 1 question I have been asked is: what do I think the market’s going to do? Since I believe it is a market of stocks, the reader might see why I abhor this question. Succinctly stated, I believe the only reason to worry about what the market might do is if you are invested in a market index fund. If you are, then the overall value of the market is important.

On the other hand, if you are invested in a select portfolio of individual stocks, then to me, the better question is: what do I think the stocks I am currently invested in are going to do? Personally, I have a clear, thoroughly researched (but sometimes erroneous) opinion of what my individual holdings are worth and how much they might grow going forward. More precisely, I understand their valuations and the specific and precise opportunities they present me.

Consequently, instead of worrying about what the overall market might do, I believe in minding my own businesses. In the long run, my results are going to be directly and functionally related to how well the businesses I’m invested in performed as operating companies. Of course, this is only true as long as I am prudent with valuation especially at time of purchase. You make your money on the buy side.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.