Decades ago I used to listen to Paul Harvey. At the time he was this country’s most famous talk radio personality. According to Wikipedia:

“Paul Harvey Aurandt, better known as Paul Harvey, was an American radio broadcaster for the ABC Radio Networks. He broadcast News and Comment on weekday mornings and mid-days and at noon on Saturdays, as well as his famous The Rest of the Story segments. From 1952 through 2008, his programs reached as many as 24 million people a week. Paul Harvey News was carried on 1,200 radio stations, 400 American Forces Network stations, and 300 newspapers. At the end of the first segment of his broadcasts, Paul would say ‘Page Two’ and at the end of his show, would say: ‘This is Paul Harvey . . . Good Day’.”

And, that is what I am saying this morning as I turn to “Page Two” of my career after a wonderful experience at the venerable firm of Raymond James. I hope I have left Raymond James on the high road because I cannot tell you how much I appreciate the opportunities Tom James, and the firm, have afforded me over the last 20+ years, but it was time to move on. I will be writing an investment letter on Monday’s, my semi-retired ex-Raymond James colleague Andrew Adams is going to bring back his much in demand “Charts of the Week” report on Wednesdays, and another ex-colleague, Harry Katica, will be writing about sectors and individual stock ideas on Friday. Of course, I also will be writing about stocks, and mutual fund ideas, like Amy Zhang’s Alger Small Cap Focus Fund (AOFAX/$20.44). I like the much-maligned small cap stocks and think the criticism of them has reached excessive levels. As market guru John Murphy writes:

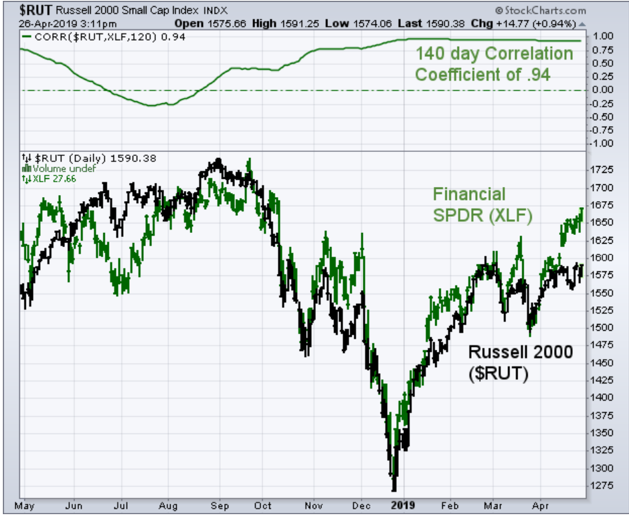

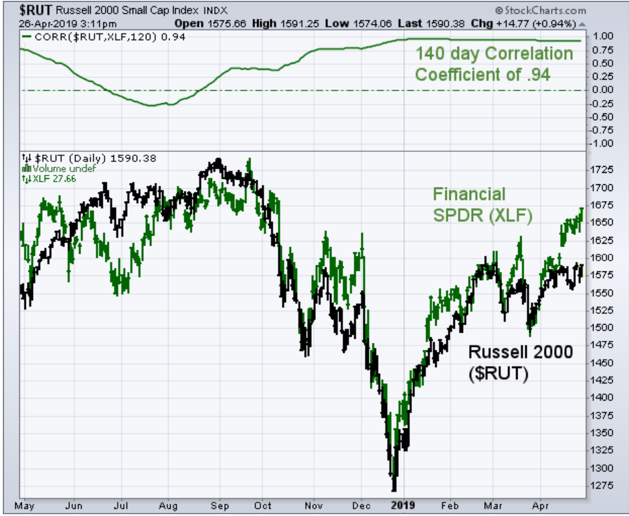

“APRIL REBOUND IN FINANCIALS IS GIVING A BIG BOOST TO SMALL CAPS. I've been writing about the recent upturn in financial stocks and, to a lesser extent, small cap stocks. I also suggested that a stronger dollar might be helping smaller stocks. That's because a rising dollar usually favors domestic-oriented smaller stocks more than large multinationals whose exports become more expensive to foreign buyers. Another boost to smaller stocks may be coming from a recent resurgence in financial stocks. That's because financials are the biggest sector in the Russell 2000. Chart 1 shows the Financial Sector SPDR (XLF/$27.70) clearing its 200-day average earlier this month before rising to the highest level in nearly seven months. Its relative strength ratio (solid line) started rebounding this month after underperforming for most of the past year. Chart 2 shows Russell 2000 Small Cap Index ($RUT/1591.82) moving above its 200-day line this month by a much smaller margin. But April has seen stronger performance. Its relative strength ratio (solid line) is also starting to recover (but by a smaller amount) from potential support near its December low. The fact that both groups have started to do better (both on an absolute and relative basis) during April may not be a coincidence.”

Market wizard Leon Tuey also chimes in on the small cap space by writing:

“Many pundits are whining about how the small caps have lagged in the rally and that it does not augur well for the economy. Whether it's ignorance or laziness, they are index-obsessed. If they take a look at the SML Advance-Decline Line, they would stop kvetching as last week, it closed at another record high. Clearly, the broad list of small cap stocks is doing far better than what the Index shows. As mentioned in my previous comments, given the strength of its internals, the Index, too, will post record highs.”

I like the small cap space, as well as the Financials, and both of those charts look like they have traced-out reverse head-and-shoulders chart patterns to me, which is a bullish pattern. As can be seen, since their March lows the RUT and XLF charts have been moving on rather nicely.

Speaking of “moving on,” the stock market moved on last week registering a new all-time high. We have suggested this was going to be the case after identifying the late-December 2018 “lows.” In fact, our models were, and are, waxing bullishly into June with little, or only marginal, pullbacks slated for the equity markets. That said, there is a slight “polarity flip” due in mid-May, but we doubt it will amount to much. Indeed, it is hard to argue with last week’s new all-time highs. It was on April 12th that we suggested the stock market was likely going into “stall mode” implying the rallies/declines were probably going to be muted, with little or no direction, because our short-term energy model was out of “gas.” Early last week we wrote that said “stall” was going to end by mid-week. Bingo . . . the S&P 500 (SPX/2939.88) popped out of its malaise last Tuesday and finished the week better by 1.30% and at new all-time highs.

Turning to earnings and the economy, for weeks we have opined that “The Street” had ratcheted down earnings expectations to levels that left room for companies to beat those lowered metrics and that is exactly what is happening. So far, more than 500 companies have reported earnings and revenues for the 1Q19. Of those reports ~67% have beaten the bottom-line consensus earnings estimates. However, only 53.6% have bettered revenue estimates. While this top-line beat rate is underwhelming, Bespoke Investment Group notes, “Last season we saw a similar trend as the top-line beat rate started very low before rebounding by the end of the reporting period and actually showing a sequential increase.” Moreover, in this week’s edition of Barron’s Bill Alpert quotes one savvy seer by writing, “Two hundred and thirty S&P 500 companies have reported first-quarter numbers, about 46% of the index. Of those, almost 80% beat Wall Street estimates.”

On the economic front, Friday’s GDP report was much better than expected at +3.2%. Speaking to this, our pal, Joe Brusuelas, RSM’s chief economist, writes:

“The primary growth drivers were a massive increase in inventory accumulation of $128.4 billion and a narrowing in the trade deficit to $899.3 billion from $955.7 billion, both of which provided a one-time boost to growth that will not be replicated in the current quarter. Stripping that out, the growth picture is decidedly different and points to a slowing toward the long-term trend growth rate of 1.8 percent.”

If that is correct, it implies there will probably be no interest rate increases soon, which is a decided plus for stocks.

The call for this week: Two weeks ago, I met with a portfolio manager that manages $40 billion who told me his two largest investment positions were Ford (F/$10.41) and General Electric (GE/$9.57). At the time I could not feature those stocks in these letters because we did not have any research coverage on them. While GE has not really worked, Ford certainly has with last Friday’s nearly 11% pop on better than expected earnings. I think better than expected earnings is the “watch word” going forward as the earnings-driven secular bull market extends for years. Golden Week begins for Japan today. Stocks are extremely overbought on multiple time frames and momentum divergences are present. However, stocks can stay overbought for a very long time. The FOMC meets on Tuesday & Wednesday. Because of the Fed’s U-turn and ensuing dovish bent, traders expect a dovish FOMC Communique on Wednesday. This morning the preopening futures are flat on no real overnight news.

Chart 1

Source: StockChart.com

Chart 2

Source: StockCharts.com

© Saut Strategy

Read more commentaries by Saut Strategy