Investment Opportunities in the Producer Manufacturing Sector: Part 15

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIntroduction

Although I consider the overall stock market as represented by the S&P 500 to be overvalued, not all stocks are overvalued. This has been one of the primary reasons that I have attempted to cover the 20 sectors reported on by FactSet. It’s very common for investors to get caught up in either their views or others views of stock market values based on generalities. However, it is my position that it is a market of stocks and not a stock market. Consequently, I consider it more prudent and in the long run profitable to pay more attention to your individual holdings than the overall market.

Now that I have covered 15 of the 20 possible sectors, it should be clear to those who have followed this complete series that there are more differences between individual stocks than similarities. Moreover, not only are companies in different sectors quite different from companies in other sectors, there are also a lot of differences between companies in the same sector. As the following 23 screenshots on the companies I am covering in this Producer Manufacturing Sector clearly illustrate, even companies in the same sector can possess their own unique and often radically different characteristics from other constituents in the same sector.

Some of you may be asking what’s the point of all this, aren’t I merely stating the obvious? When your focus is clear, that may be true. However, I am reminded of a recent conversation I had with a long-standing client who was asking me why I was not currently including bonds in his portfolio. I pointed out that I am only temporarily avoiding bonds because I believe their interest rates are too low. Nevertheless, he responded with “yes, but stocks are risky.” I responded back with the level of risk in stocks varies from company to company. Additionally, I pointed out that the risk of price volatility in bonds are also potentially high due to today’s low interest rates.

My point is simple and straightforward. All stocks should not be judged the same. The concept of risk is a very multifaceted concept. As this relates to stocks, there are some that are quite risky, and others not so much. It is my contention and opinion that these risk assessments should be made on a case-by-case basis and not in a general way. Therefore, I offer this series of articles in order to put a spotlight on this very important point. Although all the companies I’m covering with this article are in the same sector, I hope the reader appreciates that there are significantly different levels of risk between one and the other.

A Sector By Sector Review

This is part 15 of a series where I have conducted a simple screening looking for value over the overall market based on industry classifications and subindustry classifications reported by FactSet Research Systems, Inc.

In part 1 found here I covered the Consumer Services Sector. In part 2 found here I covered the Communication Sector. In part 3 found here I covered the Consumer Durables Sector and its many diverse subsectors. In part 4 found here I covered Consumer Nondurables. In part 5 found here I covered companies in the Consumer Services Sector. In part 6 found here I covered the Distribution Services Sector. In part 7 found here I covered the Electronic Technology Sector. In part 8 found here I covered the Energy Minerals Sector. In part 9 found here I covered the Finance Sector. In part 10 found here I covered the Health Services Sector. In part 11 found here I covered the Health Technology Sector. In part 12 found here I covered the Industrial Services Sector. In part 13 found here I covered the Non-Energy Minerals Sector. In part 14 found here I covered the Process Industries Sector.

In this part 15 I will be covering the Producer Manufacturing Sector.

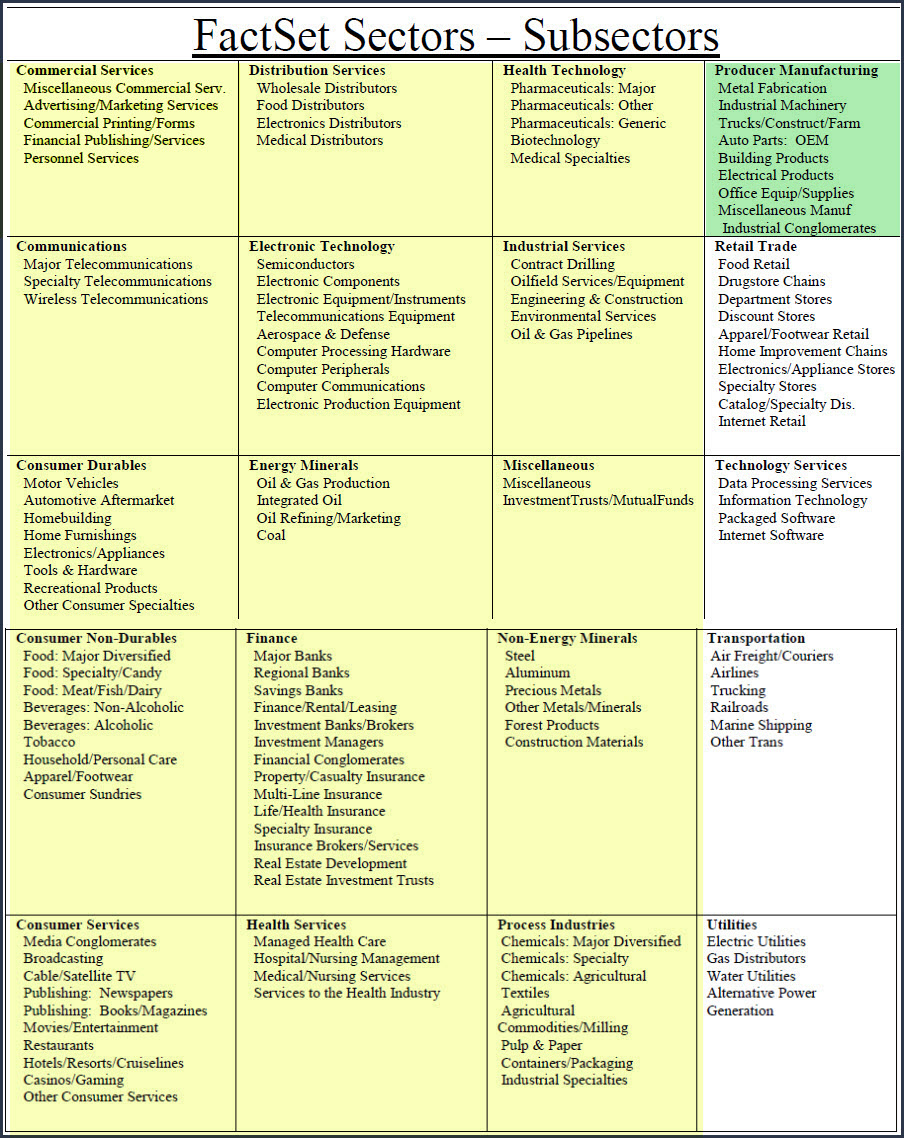

In each article in this series, I will be providing a listing of screened research candidates from each of the following industry sectors, the sector I’m covering in this article is marked in green:

Sector 15: Producer Manufacturing

Metal Fabrication

Industrial Machinery

Truck/Construct/Farm

Auto Parts: OEM

Building Products

Electrical Products

Office Equip/Supplies

Miscellaneous Manufacturing

Industrial Conglomerates

A Simple Valuation and Quality Screening Process

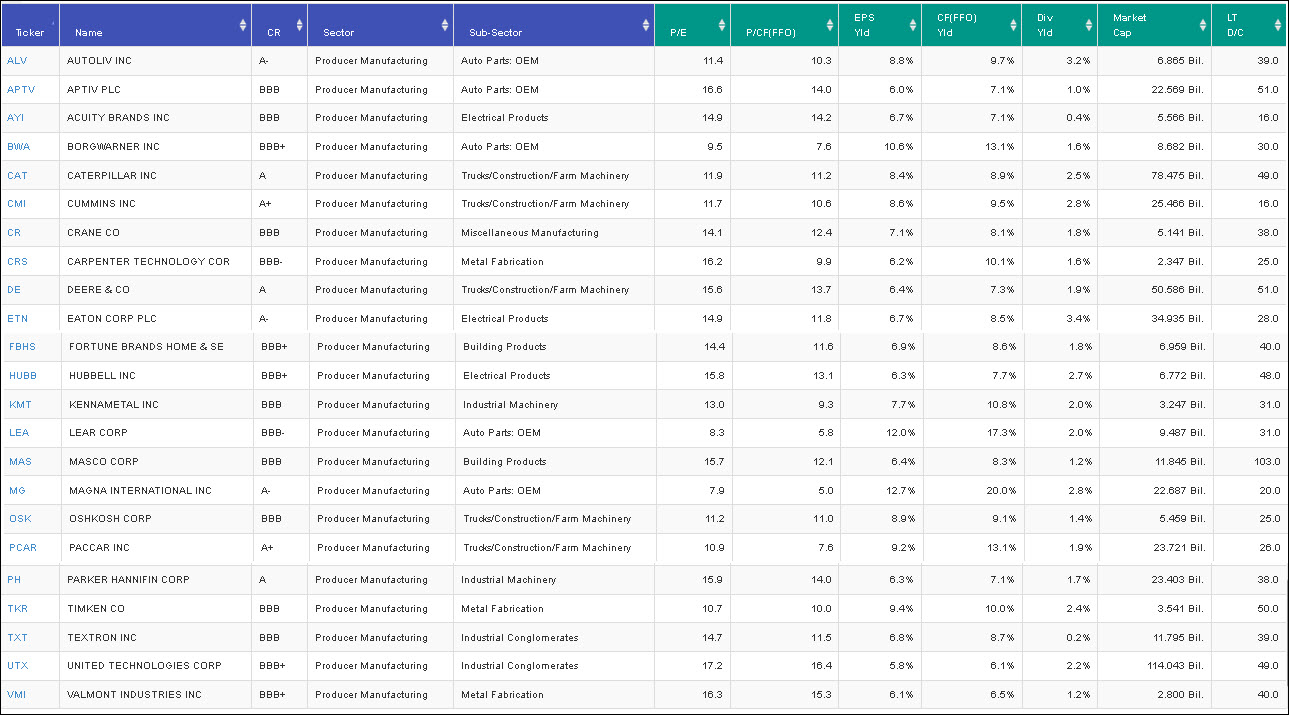

With this series of articles, I will be presenting a screening of companies that have become attractively valued primarily as a result of the bearish market activities experienced in 2018 from each of the above sectors. I will be applying a rather simple valuation and quality-oriented screen across each of the sectors. First, I have screened for investment-grade S&P credit ratings of BBB- or above. Next, I have screened for low valuations based on P/E ratios between 2 and 17. Finally, I have screened for long-term debt to capital no greater than 70%.

By keeping my screen simple, and at the same time rather broad, I will be able to identify attractively valued research candidates that I might have overlooked through a more rigorous screening process. In other words, I’m looking for fresh ideas that I might have previously been overlooking. Furthermore, I want to be clear that I do not consider every candidate that I have discovered as suitable for every investor. However, I do consider them all to be attractively valued. Additionally, I also believe that every investor will be able to find companies to research that meet their own goals, objectives and risk tolerances as this series unfolds.

Portfolio Review: Producer Manufacturing Sector: 23 Research Candidates

FAST Graphs Screenshots of the 23 Research Candidates

The following screenshots provide a quick look at each of the 23 candidates screened out of over 19,000 possibilities. However, there are only 639 companies categorized as Producer Manufacturing, and these 23 were the only ones I was comfortable presenting in this article. The company descriptions are provided courtesy of the Wall Street Journal. In the FAST Graphs analyze out loud video that follows the screenshots, I will provide additional details and thoughts on the possible attractiveness as well as the potential negatives of each of these research candidates.

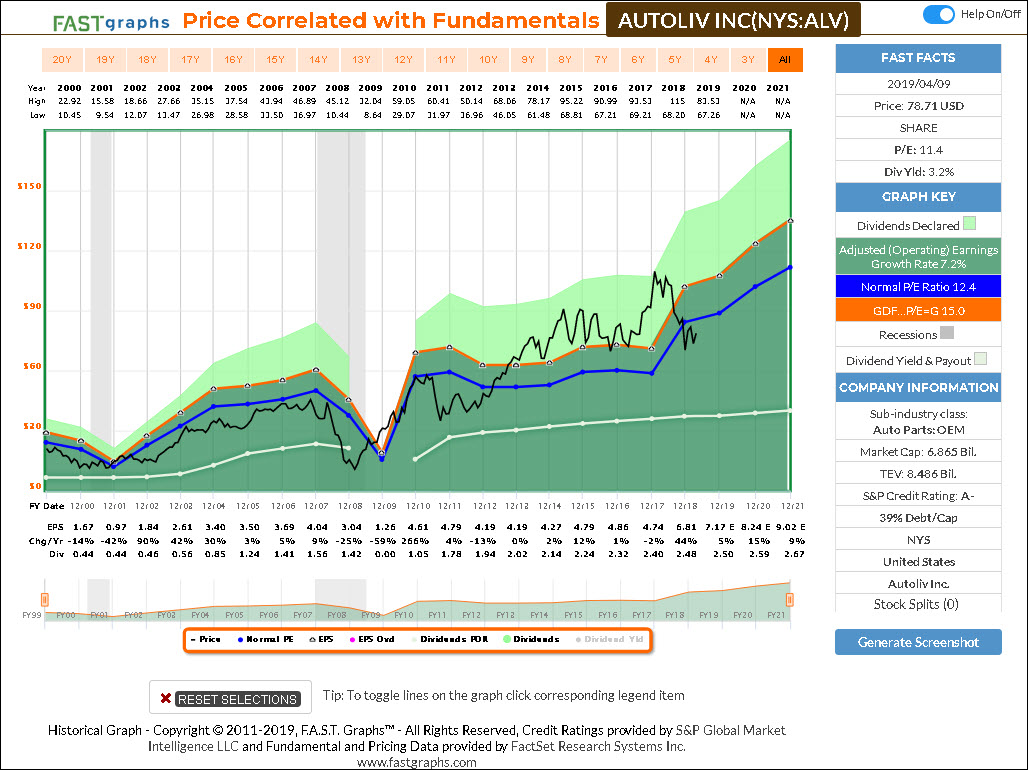

Autoliv Inc (ALV)

Autoliv, Inc. engages in the development, manufacture, and supply of automotive safety systems. It operates through the Passive Safety and Electronics segment. The Passive Safety segment includes airbags, seatbelts, steering wheels, and restrain electronics. The Electronics segment comprises of restraint control systems, brake control systems and active safety.

The company was founded by Lennart Lindblad in 1953 and is headquartered in Stockholm, Sweden.

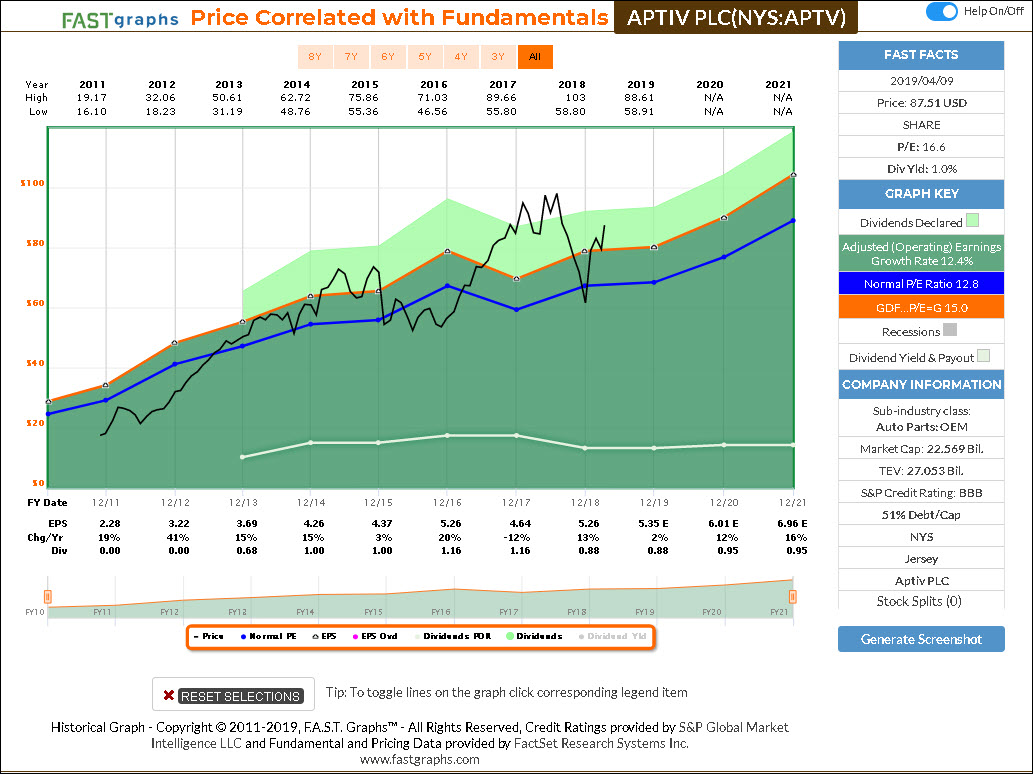

Aptiv Plc (APTV)

Aptiv Plc engages in the design, development, and manufacture of vehicle components. The firm also provides electrical, electronic, and safety technology solutions to the global automotive and commercial vehicle markets. It operates through the following business segments: Signal and Power Solutions; Advanced Safety and User Experience segments; and Eliminations and Other.

The Signal and Power Solutions segment covers component and systems integration expertise in infotainment and connectivity; body controls and security systems; displays; passive and active safety electronics; autonomous driving software and technologies; and software development. The Eliminations and Other segment comprises of elimination of inter-segment transactions, other expenses, and income of a non-operating or strategic nature.

The company was founded on May 19, 2011 and is headquartered in Dublin, Ireland.

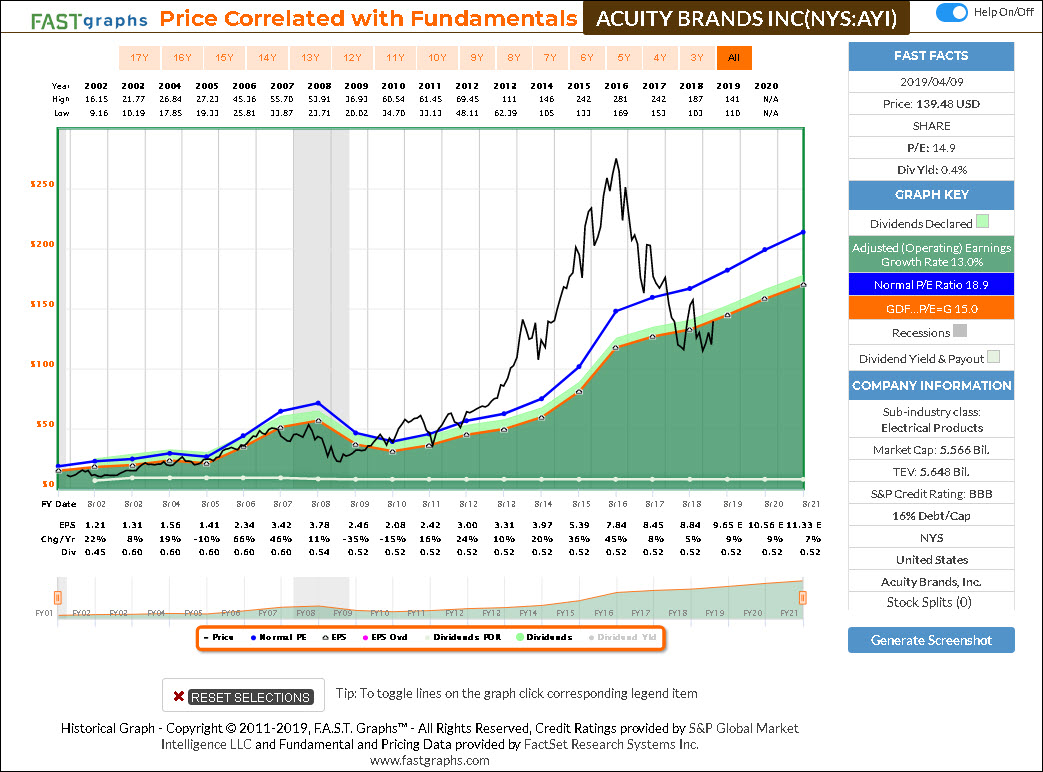

Acuity Brands Inc (AYI)

Acuity Brands, Inc. engages in the provision of lighting and building management solutions and services. It caters commercial, institutional, industrial, infrastructure, and residential applications for various markets. It offers luminaires, lighting controls, controllers for various building systems, power supplies, prismatic skylights, and drivers, as well as integrated systems for various indoor and outdoor applications.

The company was founded in 2001 and is headquartered in Atlanta, GA.

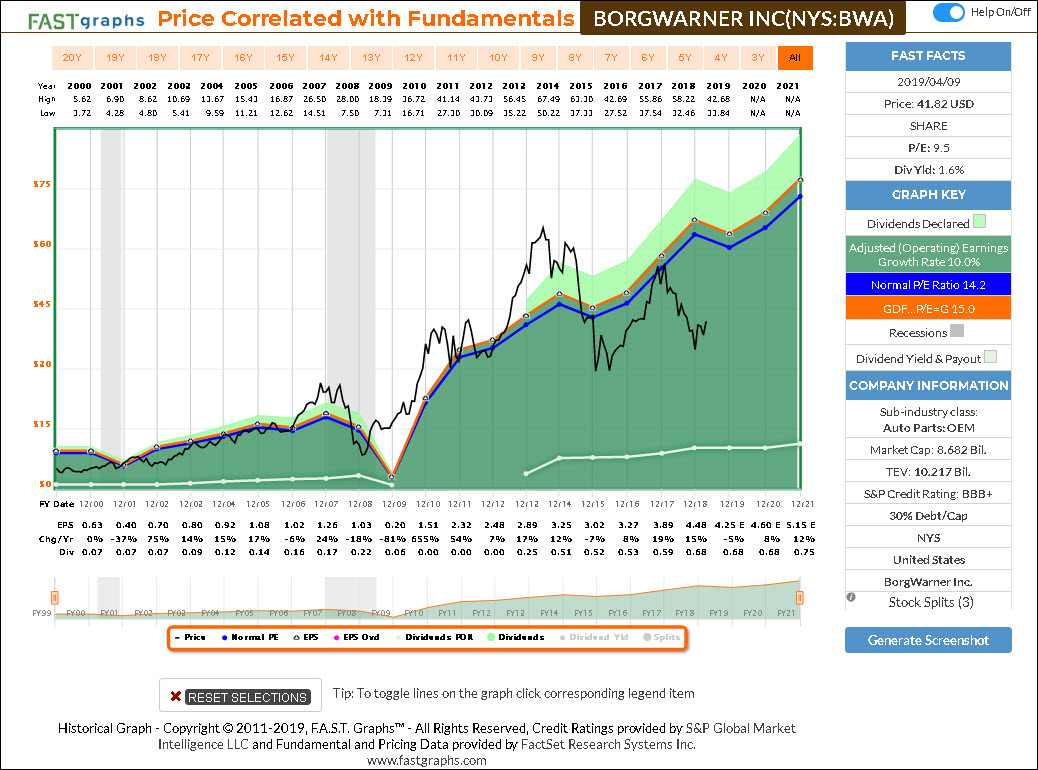

BorgWarner Inc (BWA)

BorgWarner, Inc. engages in the provision of technology solutions for combustion, hybrid and electric vehicles. It operates through Engine and Drivetrain segments. The Engine segment develops and manufactures products to improve fuel economy, reduce emissions and enhance performance. The Drivetrain segment focuses in the products that improve fuel economy, reduce emissions, and enhance performance in combustion, hybrid and electric vehicles.

The company was founded in 1928 and is headquartered in Auburn Hills, MI.

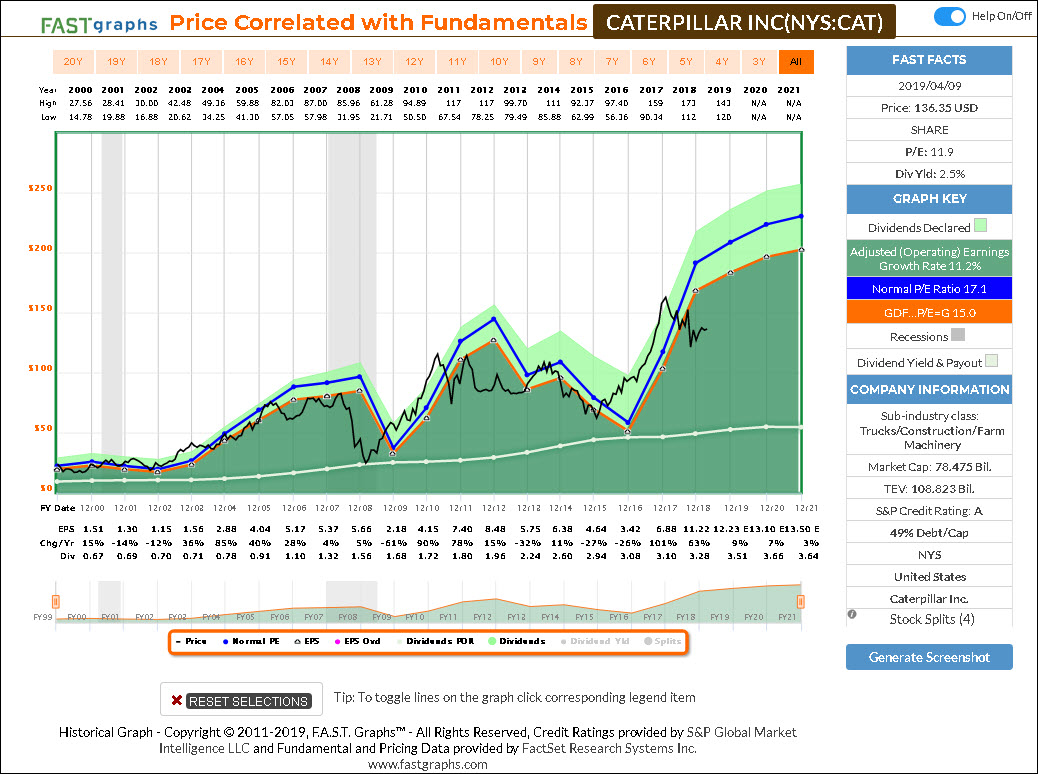

Caterpillar Inc (CAT)

Caterpillar, Inc. engages in the manufacture of construction and mining equipment, diesel and natural gas engines, industrial gas turbines, and diesel-electric locomotives. It operates through the following segments: Construction Industries, Resource Industries, Energy and Transportation, Financial Products, and All Other.

The Construction Industries segment supports customers using machinery in infrastructure and building construction applications. The Resource Industries segment is responsible for supporting customers using machinery in mining and quarrying applications and it includes business strategy, product design, product management and development, manufacturing, marketing and sales and product support.

The Energy and Transportation segment supports customers in oil and gas, power generation, marine, rail, and industrial applications. The Financial Products segment offers a range of financing alternatives to customers and dealers for Caterpillar machinery and engines, solar gas turbines, as well as other equipment and marine vessels. The All Other segments include activities such as; the business strategy, product management and development, and manufacturing of filters and fluids, undercarriage, tires and rims, engaging tools, and fluid transfers.

The company was founded on April 15, 1925 and is headquartered in Deerfield, IL.

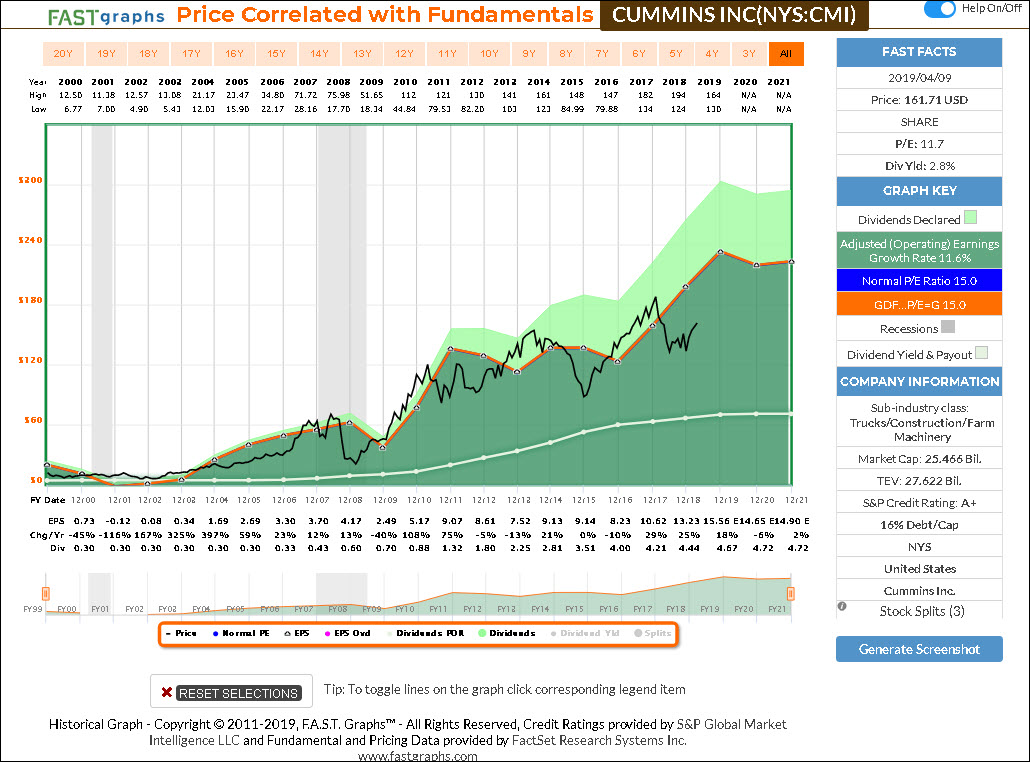

Cummins Inc (CMI)

Cummins, Inc. engages in the design, manufacture, sale and service of diesel and natural gas engines and powertrain-related technologies, including fuel systems, controls, air handing, filtration, emission, solutions and electrical power generation systems. It operates through the following segments: Engine, Distribution, Components and Power Generation.

The Engine segment manufactures and markets a range of diesel and natural gas powered engines under the Cummins brand name, for the heavy- and medium-duty truck, bus, recreational vehicle, light-duty automotive, agricultural, construction, mining, marine, oil and gas, rail and governmental equipment markets. The Distribution segment consists of parts, engines, power generation and service, which service and distributes range of its products and services.

The Components segment supplies products which complement its Engine and Power Systems segment, including after treatment systems, turbochargers, filtration products and fuel systems for commercial diesel applications. The Power Generation segment designs and manufactures most of the components that make up power generation systems, including controls, alternators, transfer switches and switchgear.

The company was founded by Clessie Lyle Cummins and William Glanton Irwin on February 3, 1919 and is headquartered in Columbus, IN.

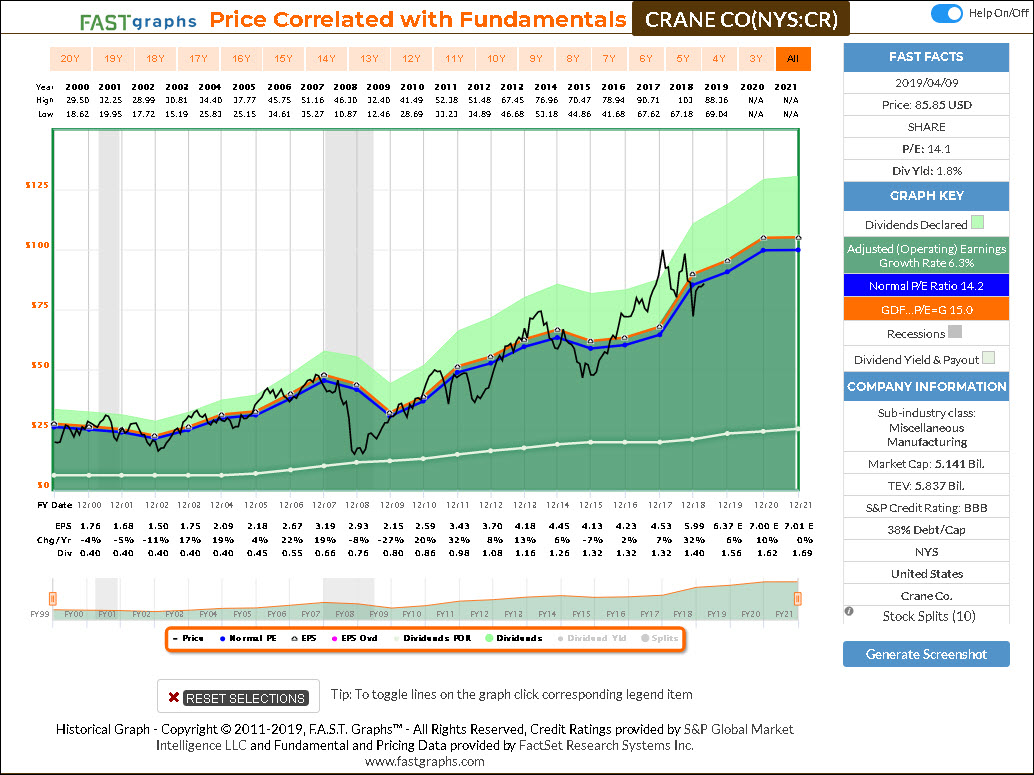

Crane Co (CR)

Crane Co. manufactures engineered industrial products. It operates through the following business segments: Fluid Handling; Payment and Merchandising Technologies; Aerospace and Electronics; and Engineered Materials. The Fluid Handling segment provides industrial fluid control products and systems. The Payment & Merchandising Technologies segment comprises of Crane Payment Innovations and Merchandising Systems.

The Aerospace & Electronics segment supplies critical components and systems, including original equipment and aftermarket parts, primarily for the commercial aerospace and military aerospace and defense markets. The Engineered Materials segment manufactures fiberglass-reinforced plastic panels and coils, primarily for use in the manufacturing of recreational vehicles, truck bodies, truck trailers, with additional applications in commercial and industrial buildings.

The company was founded by Richard Teller Crane on July 4, 1855 and is headquartered in Stamford, CT.

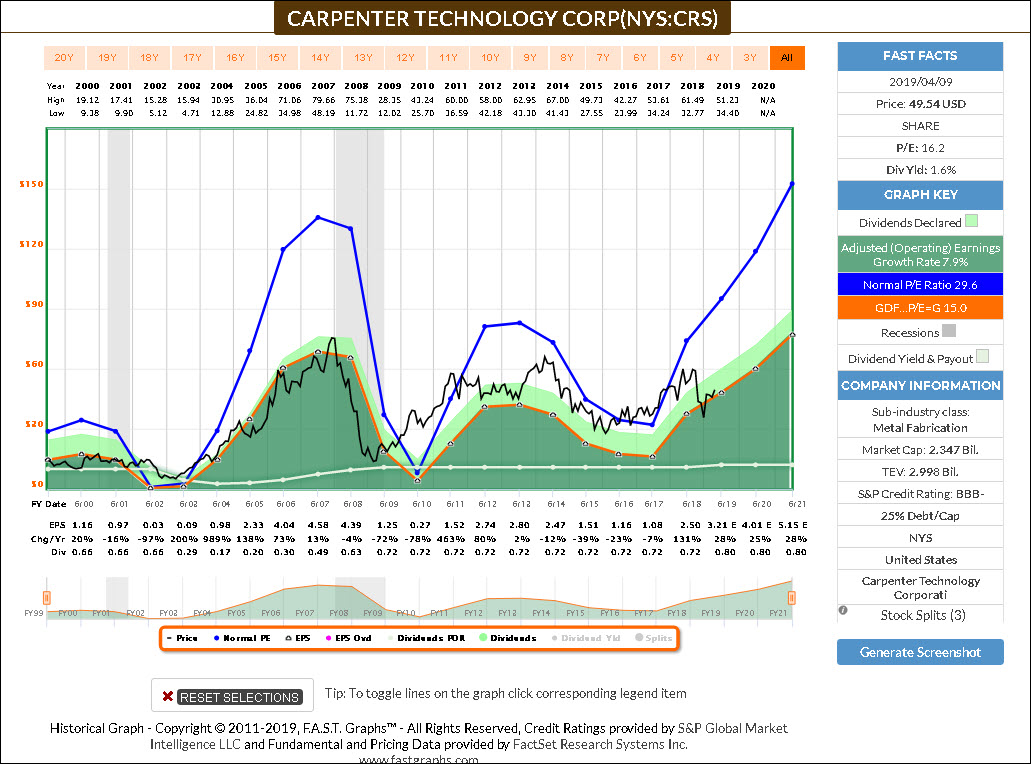

Carpenter Technology Corp (CRS)

Carpenter Technology Corp. engages in the manufacture, fabrication, and distribution of specialty metals. It operates through the Specialty Alloys Operations, and Performance Engineered Products segments. The Specialty Alloys Operations segment comprises of major premium alloy, and stainless steel manufacturing operations. The Performance Engineered Products segment includes the dynamet titanium, carpenter powder products, amega west, CalRAM, and the Latrobe and Mexico distribution businesses.

The company was founded by James Carpenter in 1889 and is headquartered in Wyomissing, PA.

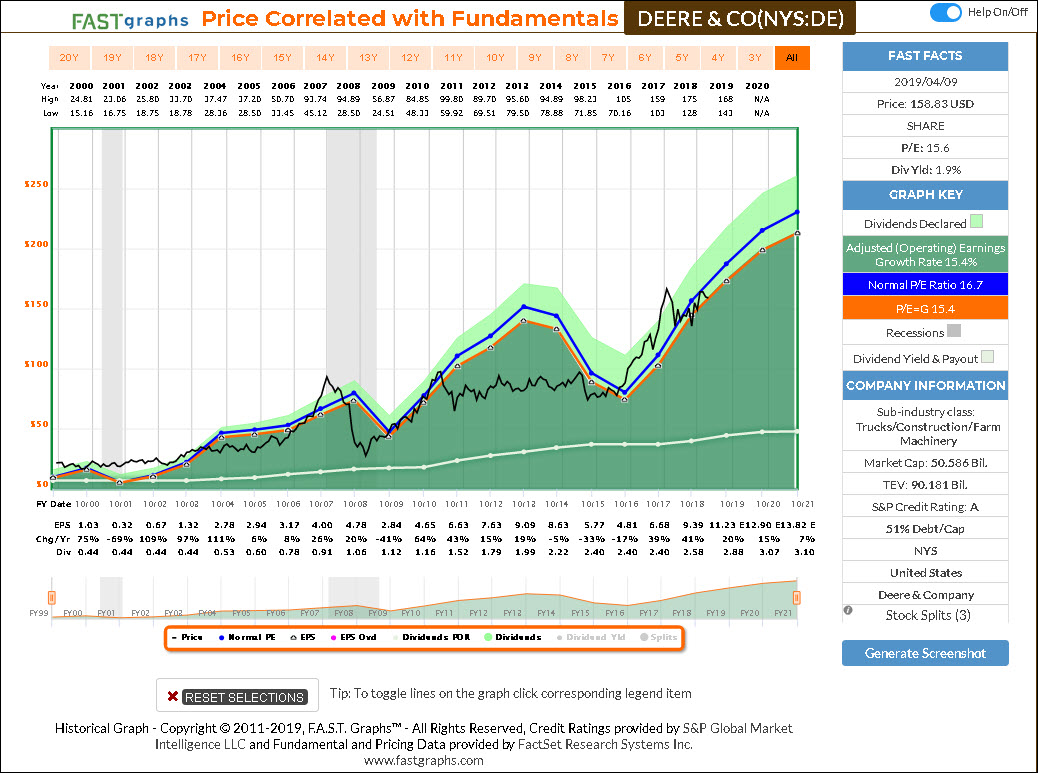

Deere & Co (DE)

Deere & Co. engages in the manufacture and distribution of equipment used in agriculture, construction, forestry, and turf care. It operates through the following segments: Agriculture and Turf, Construction and Forestry, and Financial Services. The Agriculture and Turf segment focuses on the distribution and manufacturing of full line of agriculture and turf equipment and related service parts.

The Construction and Forestry segment offers machines and service parts used in construction, earthmoving, road building, material handling, and timber harvesting. The Financial Services segment finances sales and leases by John Deere dealers of new and used agriculture and turf equipment and construction and forestry equipment.

The company was founded by John Deere in 1837 and is headquartered in Moline, IL.

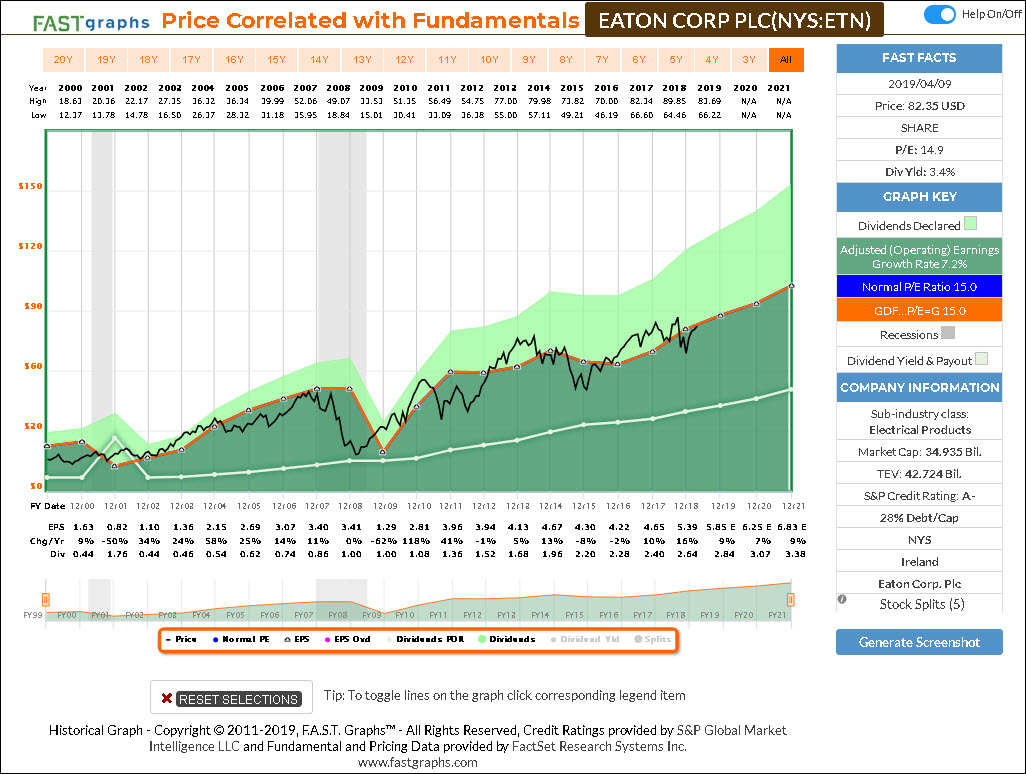

Eaton Corp (ETN)

Eaton Corp. Plc is a diversified power management company, which provides energy-efficient solutions for electrical, hydraulic and mechanical power. It operates through the following segments: Electrical Products, Electrical Systems and Services; Hydraulics; Aerospace, Vehicle and eMobility. The Electrical Products segment consists of electrical components, industrial components, residential products, single phase power quality, emergency lighting, fire detection, wiring devices, structural support systems, circuit protection, and lighting products.

The Electrical Systems and Services segment consists of power distribution and assemblies, three phase power quality, hazardous duty electrical equipment, intrinsically safe explosion-proof instrumentation, utility power distribution, power reliability equipment, and services. The Hydraulics segment includes hydraulics components, systems and services for industrial and mobile equipment.

The Aerospace segment is produces aerospace fuel, hydraulics, and pneumatic systems for commercial and military use. The Vehicle segment engages in designing, manufacturing, marketing, and supply of drivetrain and powertrain systems and critical components that reduce emissions and improve fuel economy, stability, performance and safety of cars, light trucks and commercial vehicles. The eMobility segment designs, manufactures, markets, and supplies electrical and electronic components and systems that improve the power management and performance of both on-road and off-road vehicles.

The company was founded on May 10, 2012 and is headquartered in Dublin, Ireland.

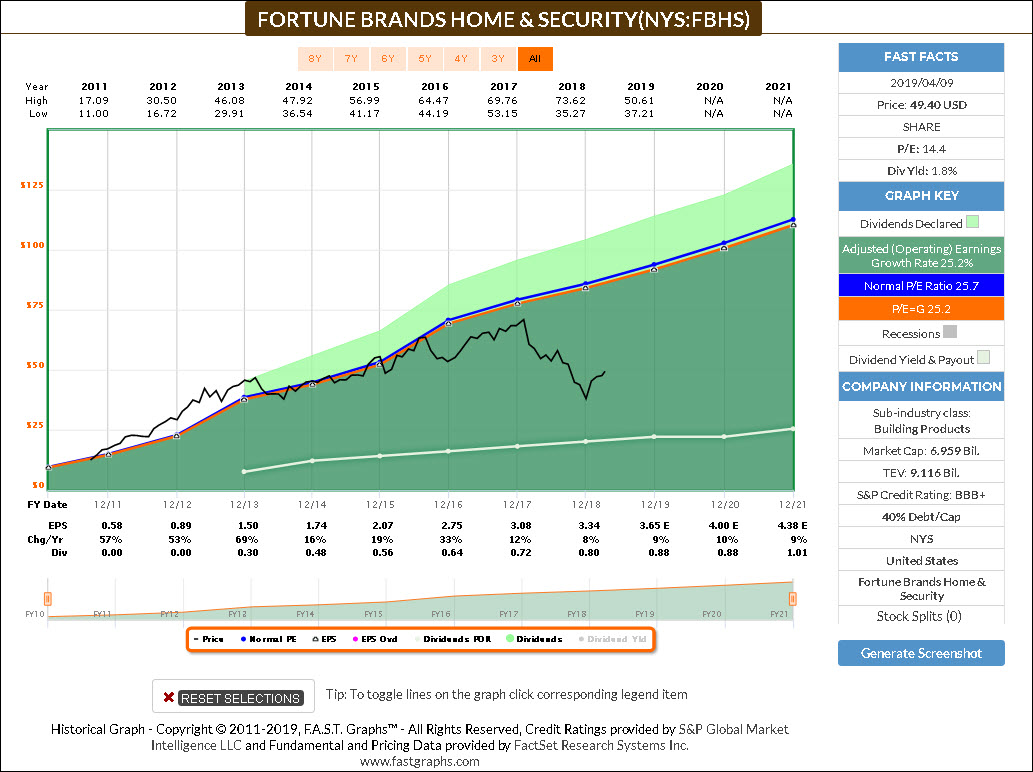

Fortune Brands (FBHS)

Fortune Brands Home & Security, Inc. manufactures and supplies home and security products and services. The company operates through the following segments: Cabinets, Plumbing, Doors, and Security. The Cabinets segment manufactures custom, semi-custom, and stock cabinetry, as well as vanities, for the kitchen, bath and other parts.

The Plumbing segment involves faucets, accessories, and kitchen sinks. The Doors segment comprises of fiberglass and steel entry door systems. The Security segment offers locks, safety and security devices, and electronic security products manufactured, sourced, and distributed under the Master Lock brand. Its brands include master lock security products, masterbrand cabinets, Moen faucets, Simonton windows, and Therma-Tru entry door systems.

The company was founded on June 9, 1988 and is headquartered in Deerfield, IL.

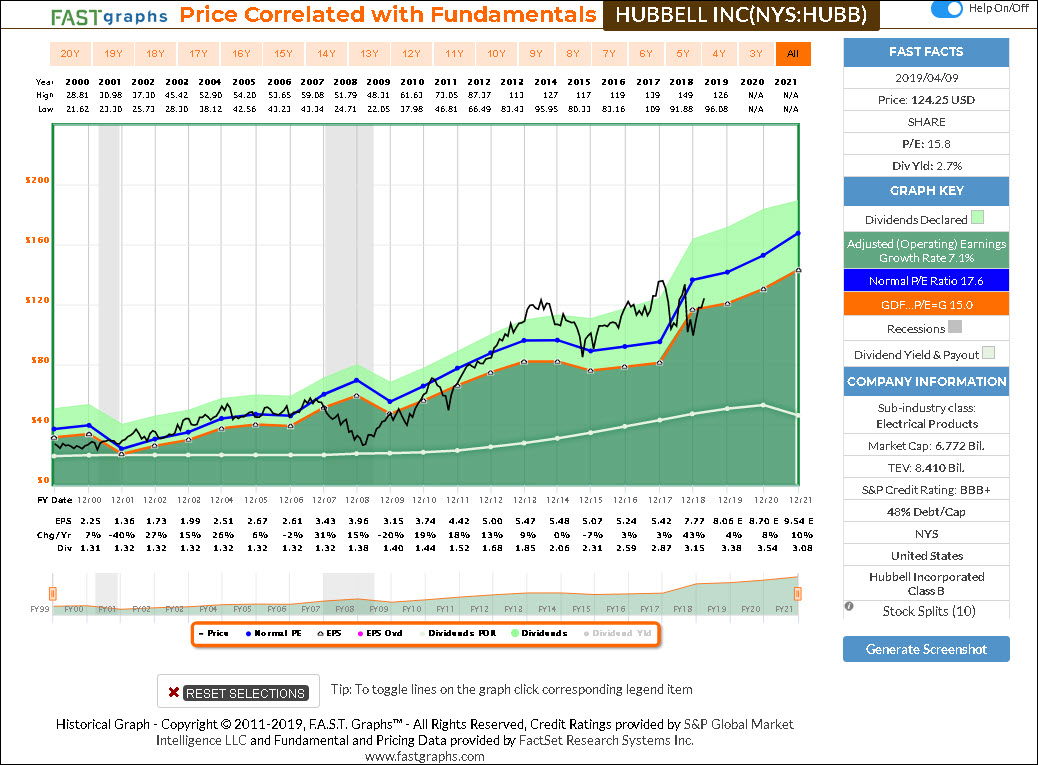

Hubbell Inc (HUBB)

Hubbell, Inc. engages in designing, manufacturing and sale of electrical and electronic products for non-residential and residential construction, industrial, and utility applications. It operates though the following two segments: Electrical and Power.

The Electrical segment manufactures and sells wiring and electrical, lighting fixtures and controls for indoor and outdoor applications as well as specialty lighting and communications products. The Power segment consists of operations that design, manufacture and sale of transmission and distribution components primarily for the electrical utilities industry.

The company was founded by Harvey Hubbell II in 1888 and is headquartered in Shelton, CT.

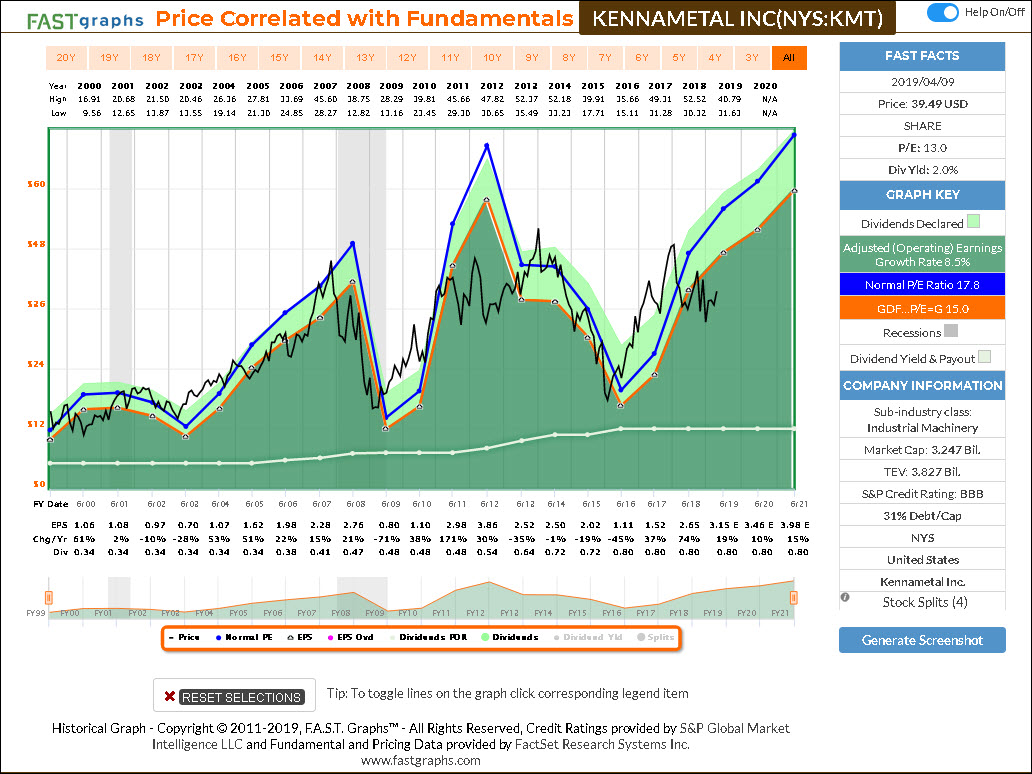

Kennametal Inc (KMT)

Kennametal, Inc. engages in the manufacture of tungsten carbide metal cutting tooling. It operates through the following segments: Industrial, Widia, and Infrastructure. The Industrial segment focuses on customers in the transportation, general engineering, aerospace and defense market sectors, delivering high performance metalworking tools for specified purposes.

The Widia segment offers a focused assortment of standard and custom metal cutting solutions to general engineering, aerospace, energy and transportation customers. The Infrastructure segment involves customers in the energy and earthworks market sectors that support primary industries such as oil and gas, power generation and chemicals; underground, surface and hard-rock mining; highway construction and road maintenance; and process industries such as food and feed.

The company was founded by Philip M. McKenna in 1938 and is headquartered in Pittsburgh, PA.

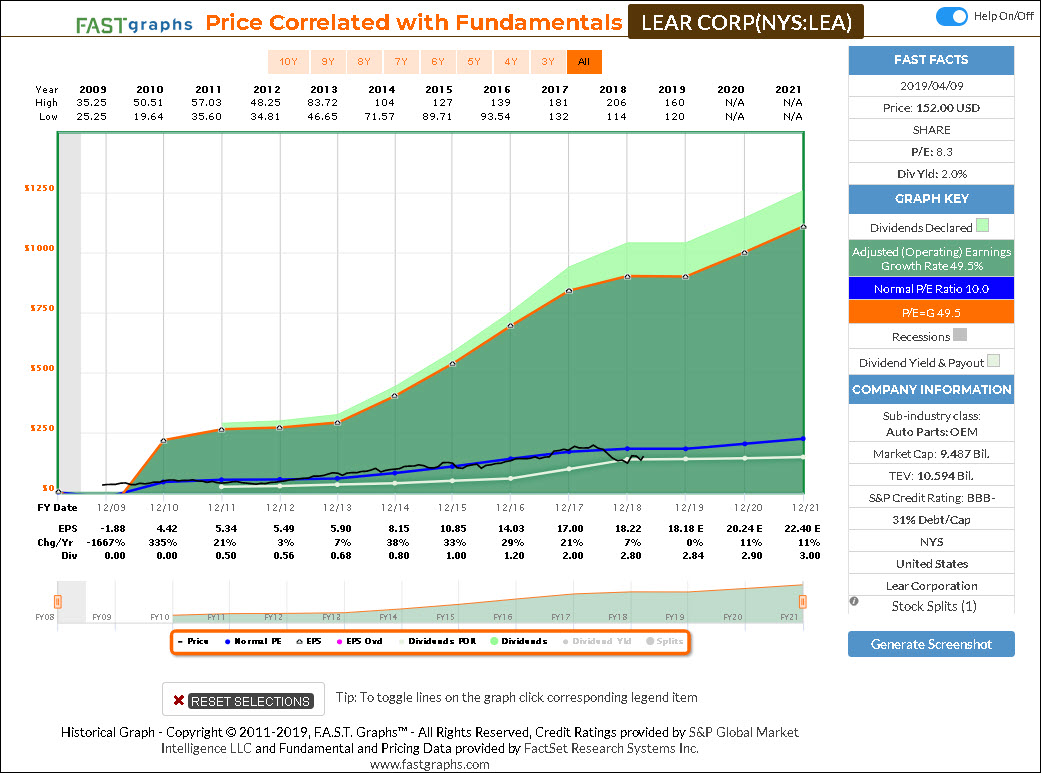

Lear Corp (LEA)

Lear Corp. engages in the design, manufacture, and supply of automotive seat, electrical distribution systems, and electronic modules, as well as related sub-systems, components, and software. It operates through the Seating and E-Systems segments. The Seating segment consists of the design, engineering, just-in-time assembly and delivery of complete seat systems, as well as the manufacture of all major seat components, including seat covers and surface materials such as leather and fabric, seat structures and mechanisms, seat foam and headrests.

The E-System segment consists of the design, development, engineering and manufacture of complete electrical distribution systems that route electrical signals and manage electrical power within a vehicle and electronic control modules that facilitate signal, data, and power management within the vehicle.

The company was founded in 1917 and is headquartered in Southfield, MI.

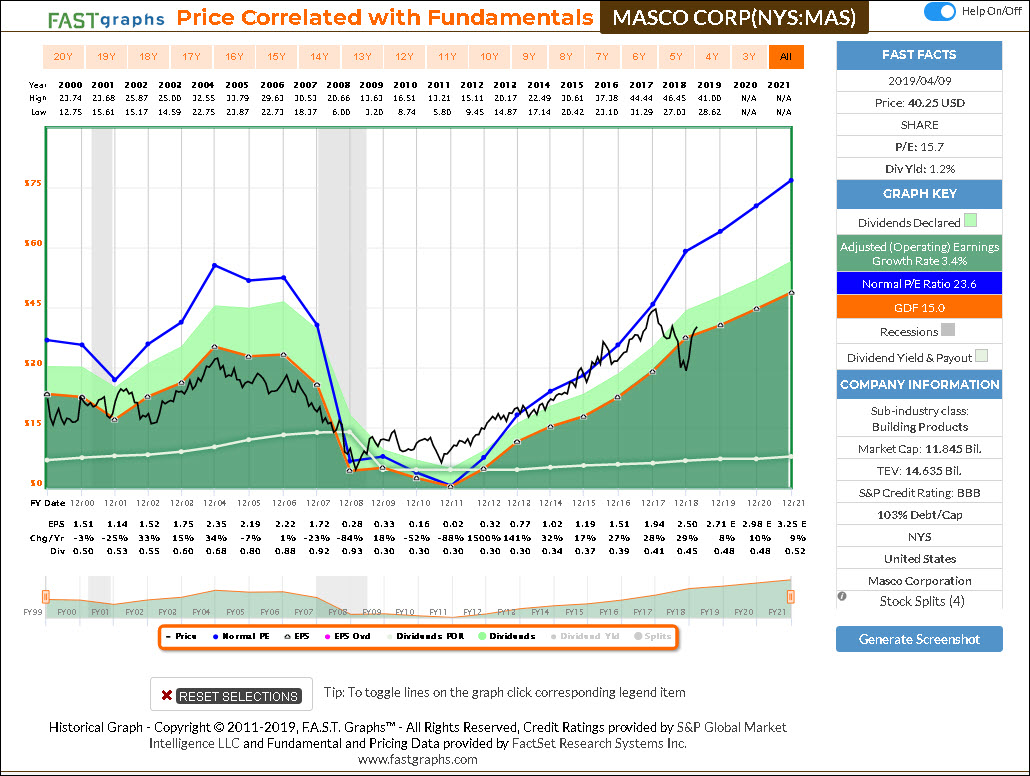

Masco Corp (MAS)

Masco Corp. engages in the design, manufacture, marketing and distribution of branded home improvement and building products. It operates through the following business segments: Plumbing Products, Decorative Architectural Products, Cabinetry Products, and Windows & Other Specialty Products. The Plumbing Products segment includes faucets; plumbing fittings and valves; showerheads and hand showers; bathtubs and shower enclosures; toilets; spas, and exercise pools.

The Decorative Architectural Products segment offers paints and coating products; and cabinet, door, window, and other hardware. The Cabinetry Products segment comprises of assembled kitchen and bath cabinets; home office workstations; entertainment centers, and storage products. The Windows & Other Specialty Products segment consists of windows; window frame components; patio doors; staple gun tackers; staples, and fastening tools.

The company was founded by Alex Manoogian in 1929 and is headquartered in Taylor, MI.

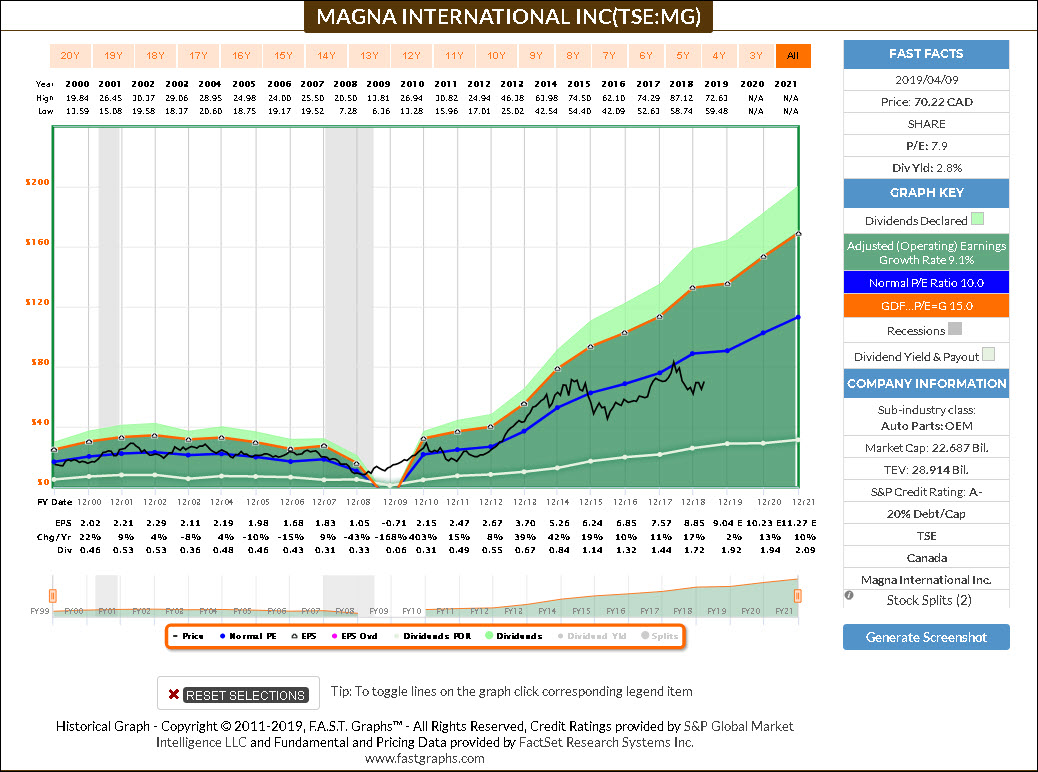

Magna International (TSE:MG)

Magna International, Inc. is a mobility technology company, which supplies to the automotive industry. It operates through the following segments: Body Exteriors and Structures; Power and Vision; Seating Systems; and Complete Vehicles. The Body Exteriors and Structures segment includes body and chassis systems, exterior systems and roof systems operations.

The Power and Vision segment comprises of global powertrain systems, electronics systems, mirrors and lighting and mechatronics operations. The Seating Systems segment deals with global seating systems operations. The Complete Vehicles segment focuses on vehicle engineering and manufacturing operations.

The company was founded by Frank Stronach in 1957 and is headquartered in Aurora, Canada.

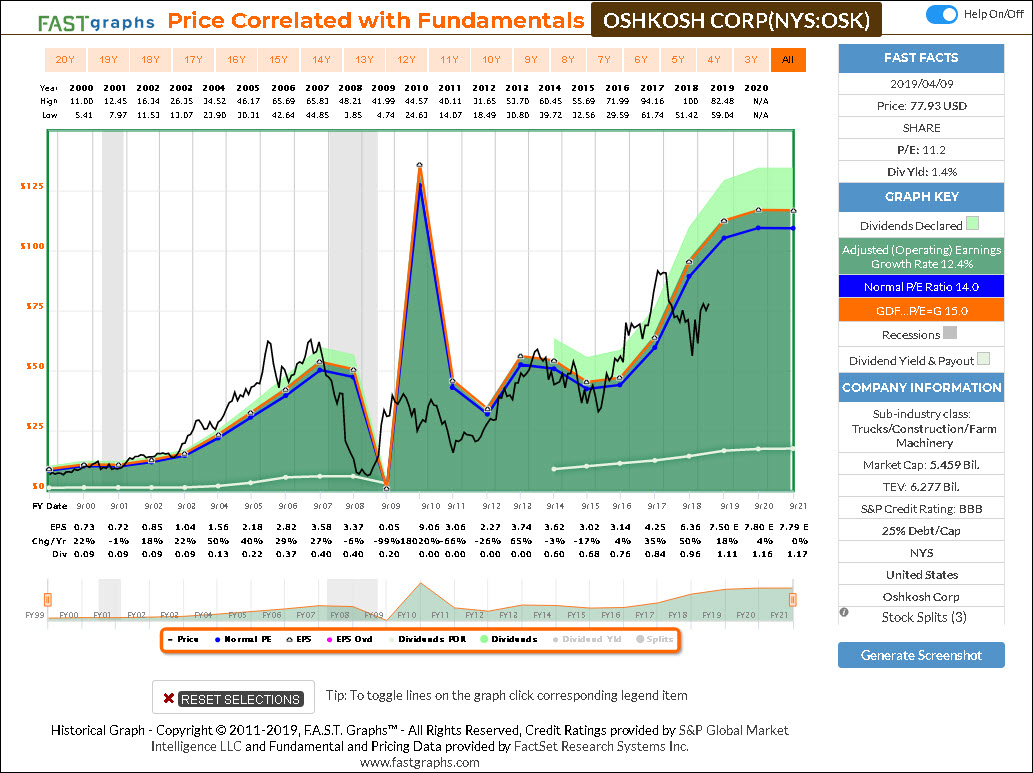

Oshkosh Corp (OSK)

Oshkosh Corp. engages in the design, manufacture, and market of specialty vehicles and vehicle bodies. It operates through the following segments: Access Equipment; Defense; Fire and Emergency; and Commercial. The Access Equipment segment consists of JerrDan and JLG, which manufactures aerial work platforms; and telehandlers that are used in construction, industrial, institutional, and general maintenance applications to position workers and materials at elevated heights.

The Defense segment produces tactical wheeled vehicles; and supply parts and services for the United States military and other militaries around the world. The Fire and Emergency segment sells commercial and custom fire vehicles; simulators and emergency vehicles primarily for fire departments, airports and other governmental units; and broadcast vehicles for broadcasters and television stations.

The Commercial segment includes McNeilus, CON-E-CO, London, Iowa Mold Tooling Co., Inc (IMT), and Oshkosh Commercial. The company was founded in 1917 and is headquartered in Oshkosh, WI.

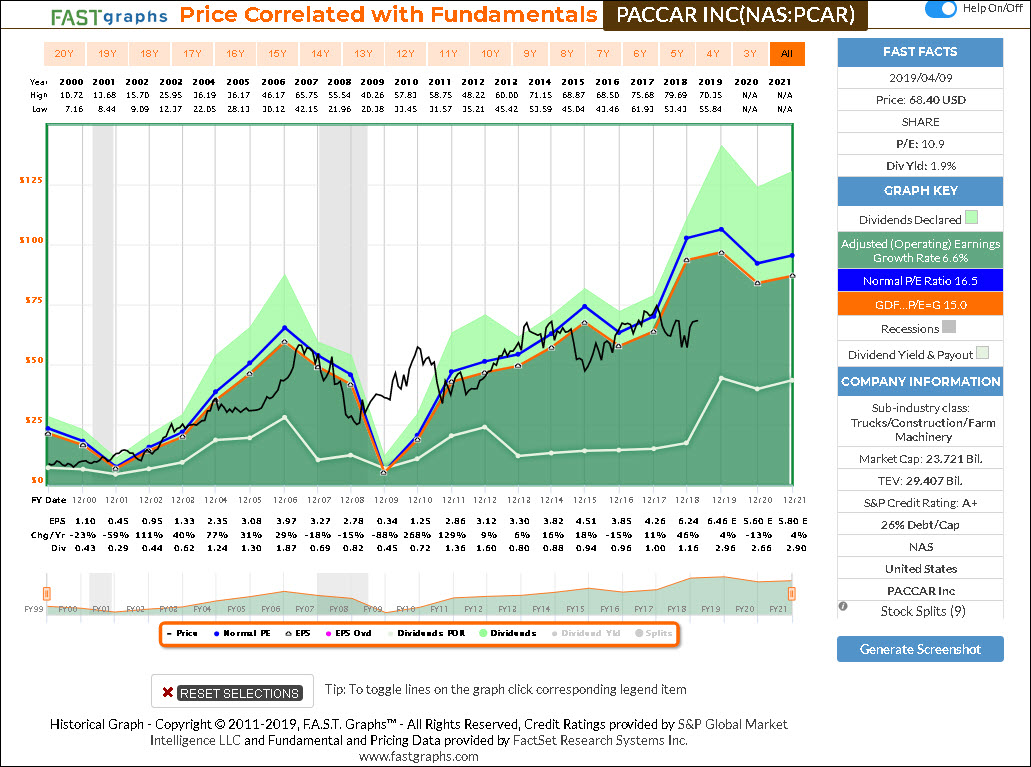

PACCAR Inc (PCAR)

PACCAR, Inc. is a global technology company, which engages in the design and manufacture of light, medium, and heavy-duty trucks. It operates through the following segments: Truck, Parts, Financial Services, and Other. The Truck segment designs and manufactures heavy, medium, and light duty diesel trucks which are marketed under the Kenworth, Peterbilt, and DAF brands.

The Parts segment distributes aftermarket parts for trucks and related commercial vehicles. The Financial Services segment provides finance and leasing products; and services provided to truck customers and dealers. The Other segment covers the manufacturing and marketing of industrial winches.

The company was founded by William Pigott Sr. in 1905 and is headquartered in Bellevue, WA.

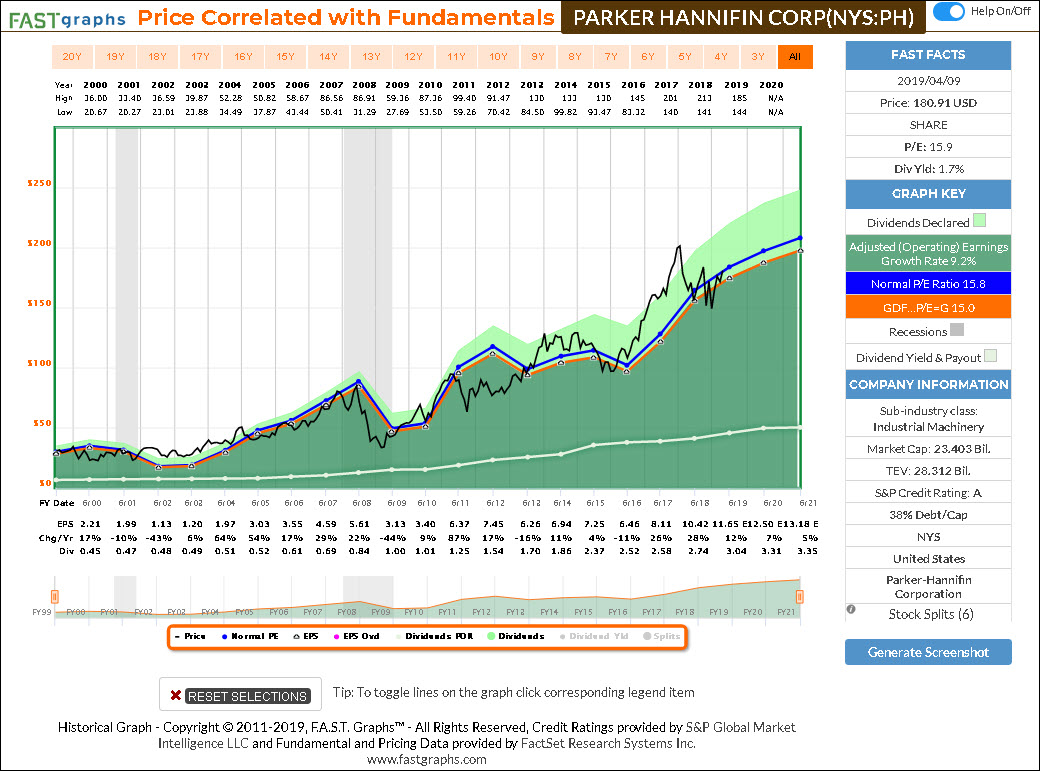

Parker Hannifin (PH)

Parker-Hannifin Corp. engages in the manufacture of motion and control technologies and systems. The firm also provides engineered solutions for mobile, industrial, and aerospace markets. It operates through the Diversified Industrial and Aerospace Systems business segments.

The Diversified Industrial segment offers products to original equipment manufacturers. The Aerospace Systems segment supplies aftermarket services, commercial transports, engines, helicopters, military aircraft, missiles, and unmanned aerial vehicles.

The company was founded by Arthur L. Parker in 1918 and is headquartered in Cleveland, OH.

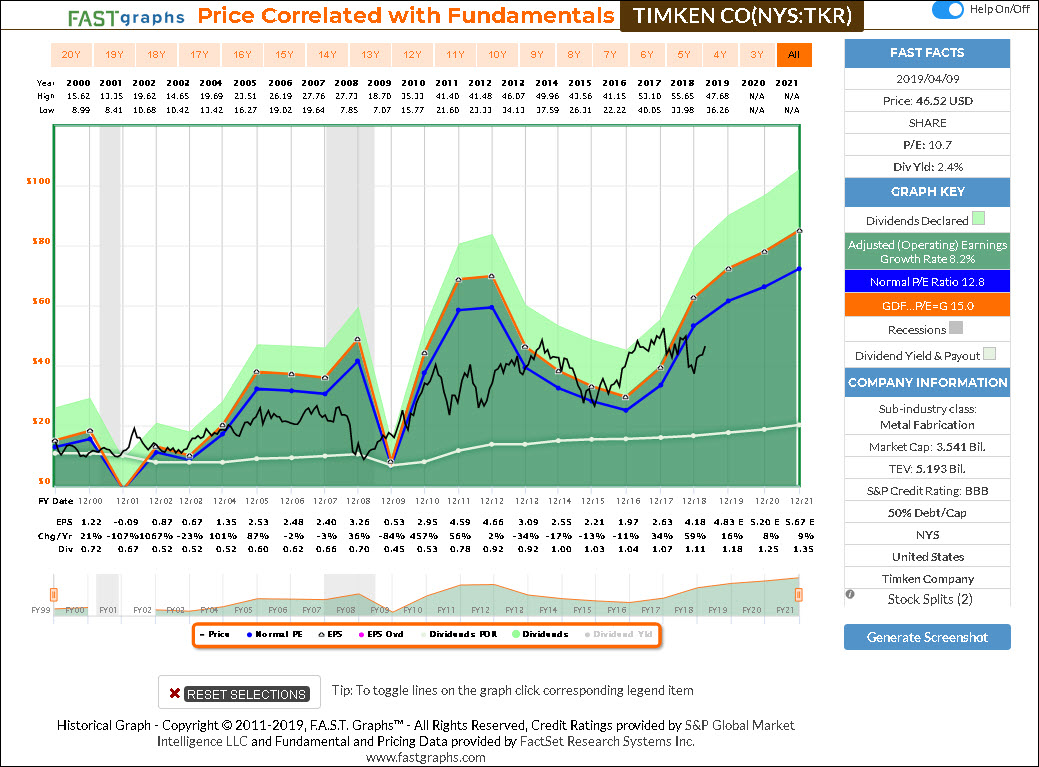

Timken Co (TKR)

The Timken Co. engages in the engineering, manufacture and marketing of bearings, transmissions, gearboxes, belts, chain, lubrication systems, couplings, industrial clutches and brakes, and related products. It operates through the Mobile Industries and Process Industries segments.

The Mobile Industries segment serves OEM customers that manufacture off-highway equipment for the agricultural, mining and construction markets; on-highway vehicles including passenger cars, light trucks, and medium- and heavy-duty trucks; rail cars and locomotives; outdoor power equipment; and rotorcraft and fixed-wing aircraft. The Process Industries segment handles OEM and end-user customers in industries that place heavy demands on the fixed operating equipment they make or use in heavy and other general industrial sectors.

The company was founded by Henry Timken in 1899 and is headquartered in North Canton, OH.

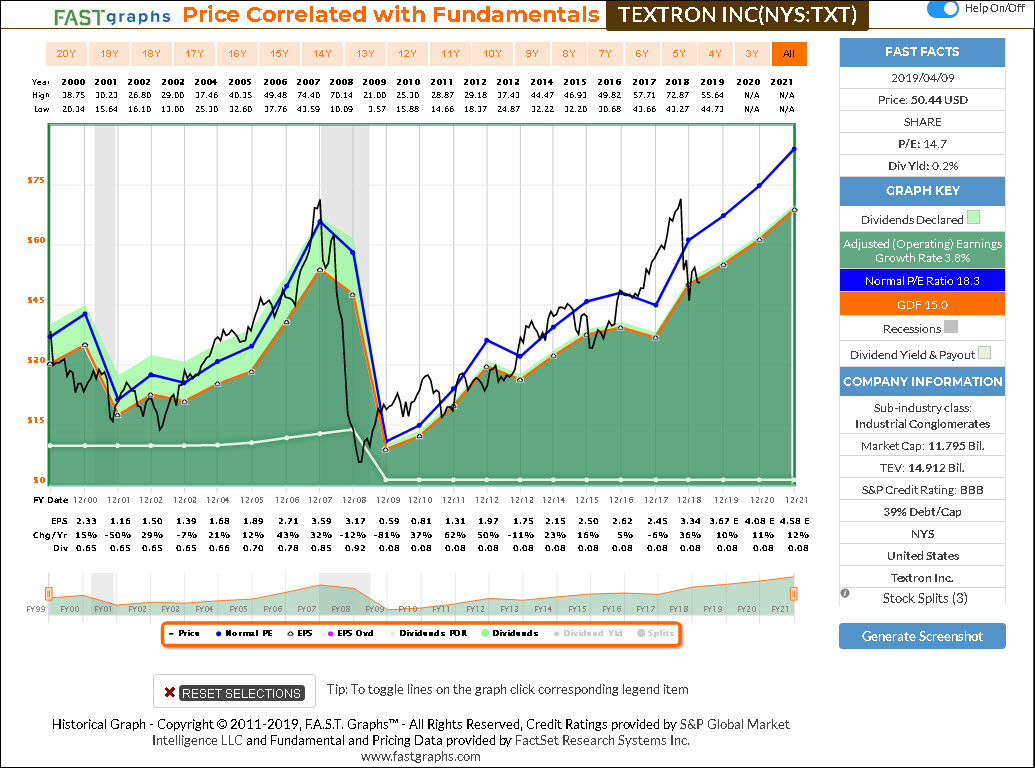

Textron Inc (TXT)

Textron, Inc. is a multi-industry company, which leverages global network of aircraft, defense, industrial, and finance businesses to provide customers innovative solutions and services. The company operates its business through the following segments: Textron Aviation, Bell, Textron Systems, Industrial, and Finance. The Textron Aviation segment manufactures, sells, and services Beechcraft and Cessna aircraft. The Bell segment supplies military and commercial helicopters, tiltrotor aircraft, and related spare parts.

The Textron Systems segment product lines consist of unmanned aircraft systems; land and marine systems; weapons and sensors; and a variety of defense and aviation mission support products and services. The Industrial segment designs and manufactures a variety of products under the Golf; Turf Care and Light Transportation Vehicles; Fuel Systems and Functional Components and Powered Tools; and Testing and Measurement Equipment product lines. The Finance segment consists of Textron Financial Corp. and its consolidated subsidiaries, which provides finances primarily to purchasers of new Cessna aircraft and Bell helicopters.

The company founded by Royal Little in 1923 and is headquartered in Providence, RI.

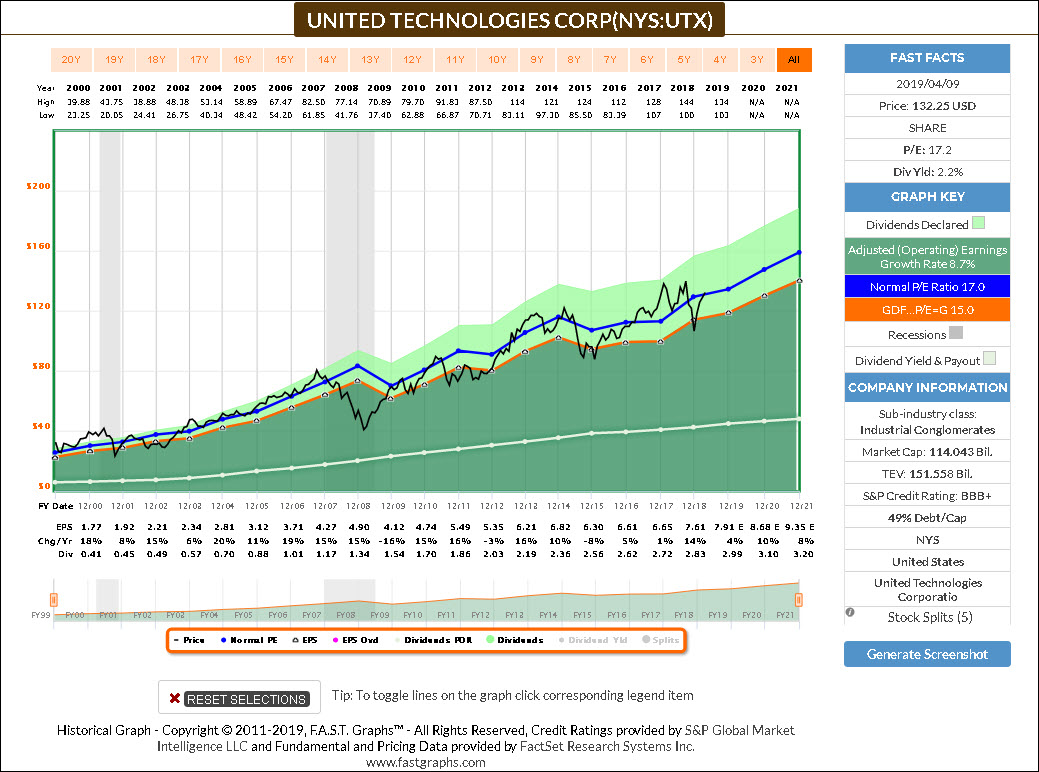

United Technologies (UTX)

United Technologies Corp. engages in the provision of products and services to the building systems and aerospace industries worldwide. It operates through the following business segments: Otis; Carrier; Pratt and Whitney; and Collins Aerospace Systems. The Otis segment designs, manufactures, and markets elevators, escalators, moving walkways, and service. The Carrier segment provides heating, ventilating, air conditioning, and refrigeration solutions.

The Pratt and Whitney segment includes aircraft engines for the commercial, military, business jet, and general aviation markets. The Collins Aerospace Systems segment offers technologically advanced aerospace products and aftermarket service solutions for aircraft manufacturers, airlines, regional, business and general aviation markets, military, space and undersea operations.

The company was founded in 1934 and is headquartered in Farmington, CT.

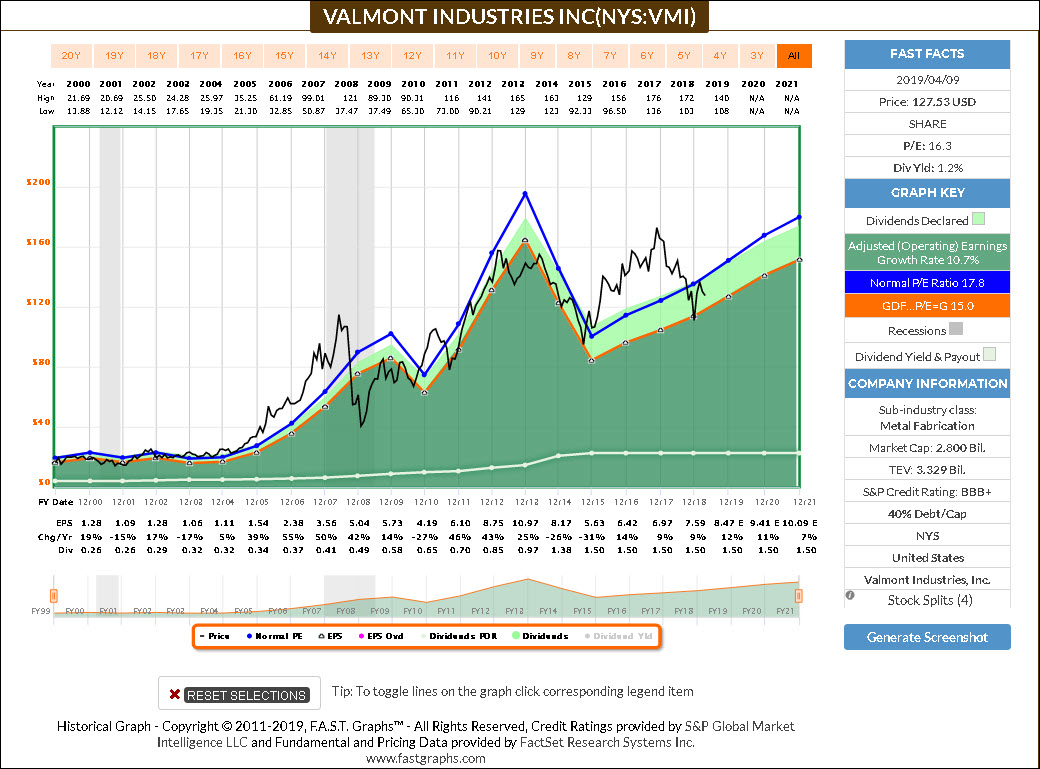

Valmont Industries (VMI)

Valmont Industries, Inc. engages in the manufacturing of engineered fabricated metal products. It operates through the following four segments: Engineered Support Structures, Utility Support Structures, Irrigation and Coatings. The Engineered Support Structures segment produces engineered access systems, highway safety products, and integrated structure solutions for smart cities.

The Utility Support Structures segment manufactures steel and concrete pole structures for global utility transmission, distribution and generation platforms primarily in the U.S., and also produces steel energy generation structures and engineered solar tracking solutions sold outside the U.S. The Irrigation segment mechanized irrigation systems and provides water management solutions for large-scale production agriculture, and technology for precision agriculture. The Coatings segment provides global galvanizing, painting and anodizing services to preserve and protect metal products.

The company was founded by Robert B. Daugherty in 1946 and is headquartered in Omaha, NE.

F.A.S.T. Graphs Analyze Out Loud Video:

Rather than attempt to cover 23 companies in a single video, I have selected 6 of the companies I screened in the Producer Manufacturing sector. The reason I chose these 6 companies is because I believe they each offer important lessons about prudent investing. Here are the 6 companies I will be reviewing in the analyze out loud video listed in order of highest to lowest dividend yield:

<

Summary and Conclusions

With this 15th installment in this series, we continued to see undeniable evidence that operating results (earnings/cash flows) drive market values in the long run. Consequently, it logically follows that it is more important to focus on the business and how it’s likely to perform in the near and longer-term future than it is what the stock price might do over the shorter run. Even more importantly, it should also be logical and clear that forecasting business results can be done a lot more accurately and predictably than attempting to forecast price movements.

However, we should also consider and recognize that forecasting future operating results can be more precise with companies that are consistent operators. In contrast, more cyclical companies are more challenging when attempting to forecast future business results. Nevertheless, it is still easier to predict the business results of even a cyclical company than it is their stock price. As I have said previously, I believe investors should quit worrying about stock price movements and “mind their own businesses.”

Disclosure: Long BWA,CMI,CR,ETN,UTX

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits