One of the main goals of this series of articles is to illustrate the significant differences between individual stocks, and the significant differences between different sectors. Therefore, from this perspective, I have been attempting to illustrate the “nature of the beast” for each of the sectors I have covered. The Process Industries Sector as reported by FactSet does consist of companies that are cyclical in nature. However, just as we’ve seen with other sectors, some are more cyclical than others.

Moreover, cyclicality is an attribute that can be problematic for many investors, but not necessarily a long-term negative. To clarify that statement, every research candidate except for one (International Paper) covered in this article has dramatically outperformed the S&P 500 on both dividend income and total return over the long run. However, that exceptional performance has not always been a smooth ride relative to the cyclical nature of these companies’ operating histories. Consequently, I feel comfortable stating that being a long-term investor in cyclical companies such as those covered here can be very challenging. Therefore, many investors might lack the fortitude to be able to stay the course during those times when earnings and cash flows are faltering.

On the other hand, the historical dividend records of most of these research candidates have been quite good and have grown consistently despite earnings cyclicality. Therefore, investors focused on earning a steadily increasing stream of dividend income can be more apt to ride through the cycles in order to achieve the strong long-term returns. More simply stated, although short to intermediate-term stock prices and operating results can be quite volatile, dividend growth is both more reliable and attractive. Consequently, most of these research candidates have generated more total cumulative dividend income than the market, and if held long enough, most have also produced higher growth and total returns as well.

Additionally, although cyclicality can be unnerving at times, it can also represent the precursor to significantly higher intermediate returns than those available from more “steady Eddie” type companies. One of the reasons for these “greater intermediate returns” phenomenon is the excitement created by extremely high year-to-year growth rates when companies are coming off a low point in their operating cycle. High growth off a low base generates extremely high quarterly and annual earnings reports that can get investors temporarily quite enthusiastic about the companies. I will be clearly illustrating this in the analyze out loud video later in this article.

A Sector By Sector Review

This is part 14 of a series where I have conducted a simple screening looking for value over the overall market based on industry classifications and subindustry classifications reported by FactSet Research Systems, Inc.

In this part 14 I will be covering the Process Industries Sector.

In each article in this series, I will be providing a listing of screened research candidates from each of the following industry sectors, the sector I’m covering in this article is marked in green:

Sector 14: Process Industries:

Chemicals: Major Diversified

Chemicals: Specialty

Chemicals: Agricultural

Textiles

Agricultural

Commodities/Milling

Pulp & Paper

Containers/Packaging

Industrial Specialties

A Simple Valuation and Quality Screening Process

With this series of articles, I will be presenting a screening of companies that have become attractively valued primarily as a result of the bearish market activities experienced in 2018 from each of the above sectors. I will be applying a rather simple valuation and quality-oriented screen across each of the sectors. First, I have screened for investment-grade S&P credit ratings of BBB- or above. Next, I have screened for low valuations based on P/E ratios between 2 and 17. Finally, I have screened for long-term debt to capital no greater than 70%.

By keeping my screen simple, and at the same time rather broad, I will be able to identify attractively valued research candidates that I might have overlooked through a more rigorous screening process. In other words, I’m looking for fresh ideas that I might have previously been overlooking. Furthermore, I want to be clear that I do not consider every candidate that I have discovered as suitable for every investor. However, I do consider them all to be attractively valued. Additionally, I also believe that every investor will be able to find companies to research that meet their own goals, objectives and risk tolerances as this series unfolds.

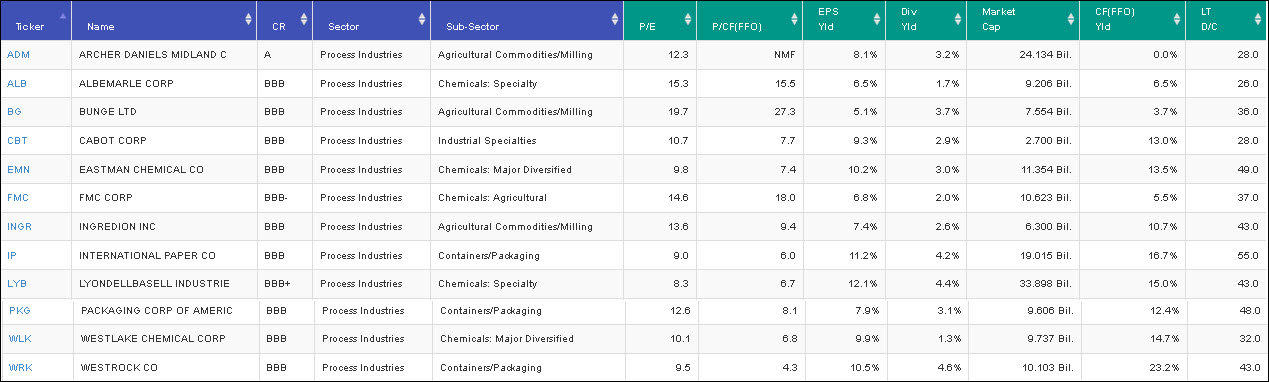

Portfolio Review: Process Industries Sector: 12 Research Candidates

FAST Graphs Screenshots of the 12 Research Candidates

The following screenshots provide a quick look at each of the 12 candidates screened out of over 19,000 possibilities. However, there are only 406 companies categorized as Process Industries Sector, and these 12 were the only ones I was comfortable presenting in this article. The company descriptions are provided courtesy of the Wall Street Journal. In the FAST Graphs analyze out loud video that follows the screenshots, I will provide additional details and thoughts on the possible attractiveness as well as the potential negatives of each of these research candidates.

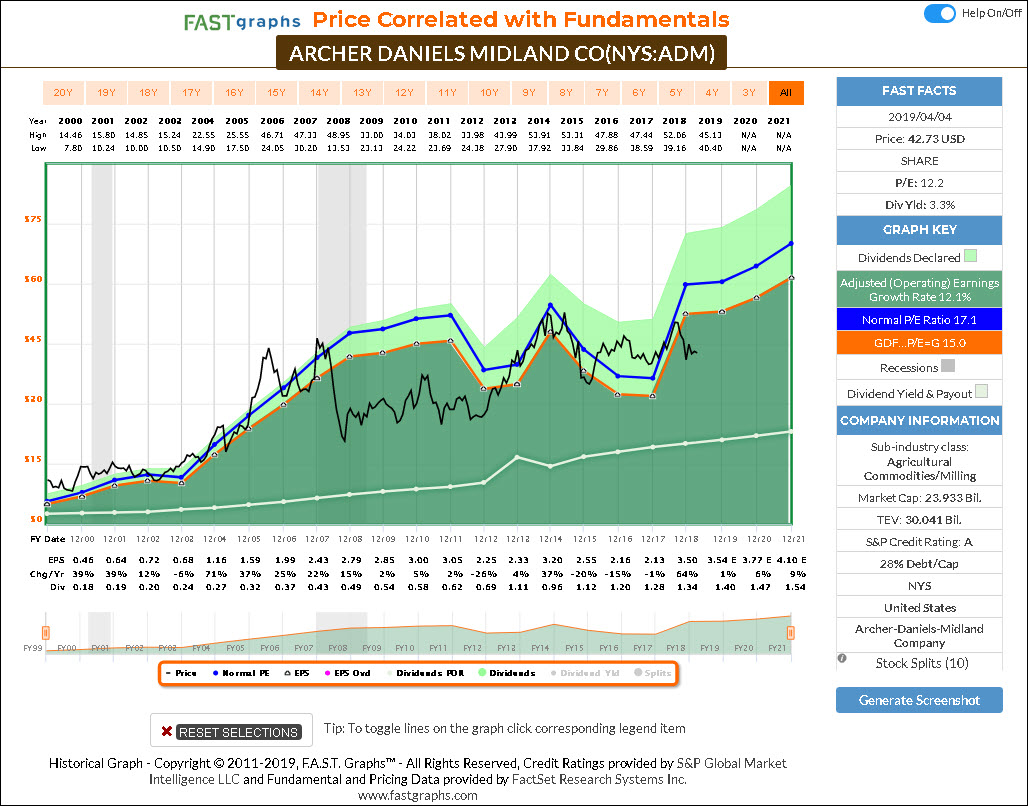

Archer Daniels Midland (ADM)

Archer-Daniels-Midland Co. processes oilseeds, corn, wheat, cocoa and other agricultural commodities. The company operates through the following segments: Oilseeds Processing, Corn Processing, Wild Flavors & Specialty Ingredients and Agricultural Services. The Oilseeds Processing segment includes activities related to the origination, merchandising, crushing, and further processing of oilseeds such as soybeans and soft seeds, such as cottonseed, sunflower seed, canola, rapeseed, and flaxseed into vegetable oils and protein meals.

The Corn Processing segment engages in corn wet milling and dry milling activities; and also converts corn into sweeteners, starches, and bioproducts. The Wild Flavors and Specialty Ingredients segment manufactures, sells, and distributes specialty products including natural flavor ingredients, flavor systems, natural colors, proteins, emulsifiers, soluble fiber, polyols, hydrocolloids, natural health and nutrition products, other specialty food, and feed ingredients.

The Agricultural Services segment utilizes its extensive United States grain elevator and global transportation network to buy, store, clean, and transport agricultural commodities, such as oilseeds, corn, wheat, milo, oats, rice and barley. It resells these commodities primarily as food and feed ingredients and as raw materials for the agricultural processing industry.

Archer-Daniels-Midland was founded in 1902 and is headquartered in Chicago, IL.

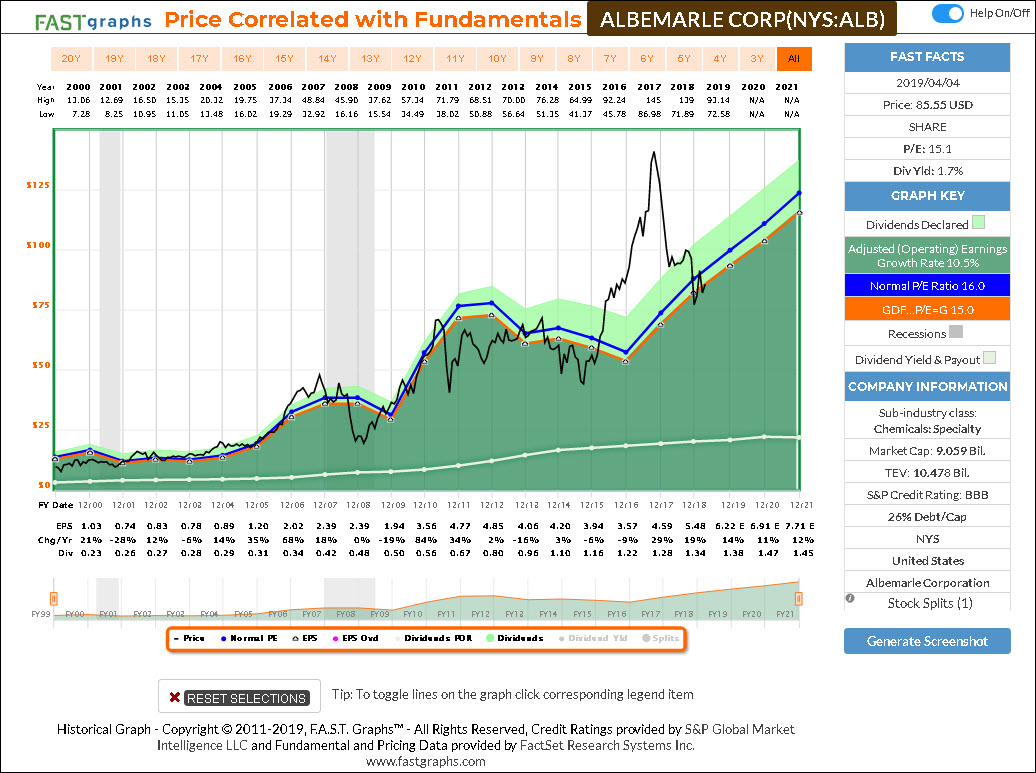

Albemarble Corp (ALB)

Albemarle Corp. is a specialty company, which engages in developing, manufacturing, and marketing of chemicals for consumer electronics, petroleum refining, utilities, packaging, construction, transportation, pharmaceuticals, crop production, food-safety, and custom chemistry services. It operates through the following segments: Lithium and Advanced Materials, Bromine Specialties, and Refining Solutions.

The Lithium and Advanced Materials segment include two product categories: Lithium and PCS. The Lithium business develops and manufactures a broad range of basic lithium compounds. The Performance Catalyst Solutions division operates in three product lines: organometallics, polymer catalysts and Curatives.

The Bromine Specialties segment consists of bromine and bromine-based business includes products used in fire safety solutions and other specialty chemicals applications. The Refining Solutions segment contain two product lines: clean fuels technologies, which is primarily composed of hydro processing catalysts, and heavy oil upgrading that comprises of fluidized catalytic cracking catalysts and additives.

The company was founded in 1993 and is headquartered in Charlotte, NC.

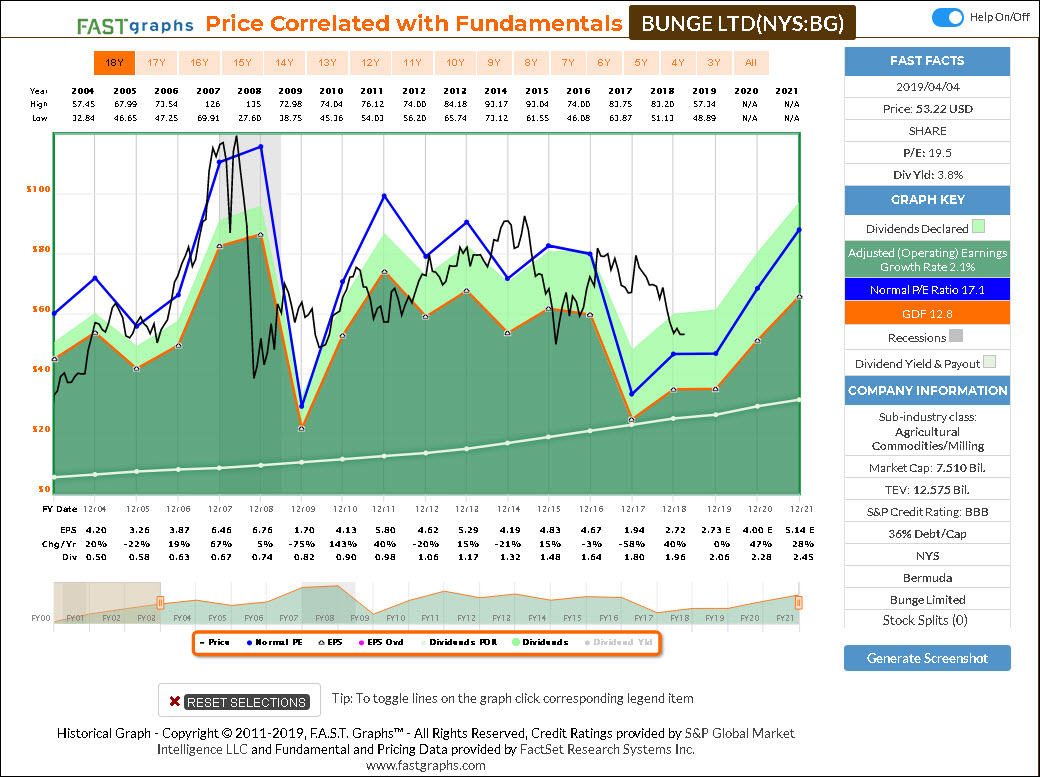

Bunge (BG)

Bunge Ltd. operates as a holding company, which engages in the supply and transportation of agricultural commodities. It operates through the following segments: Agribusiness, Edible Oil Products, Milling Products, Sugar and Bioenergy and Fertilizer. The Agribusiness segment involves in the purchase, storage, transportation, processing, and sale of agricultural commodities and commodity products. The Edible Oil Products segment includes production and sale of vegetable oils, shortenings, margarines, and mayonnaise.

The Milling Products segment consists of production and sale of wheat flours, bakery mixes, corn-based products, and rice. The Sugar and Bioenergy segment comprises manufacture and marketing of sugar and ethanol derived from sugarcane, as well as energy derived from the sugar and ethanol production process. The Fertilizer segment focuses on producing, blending, and distributing fertilizer products for the agricultural industry.

The company was founded by Johann Peter Gottlieb Bunge in 1818 and is headquartered in White Plains, NY.

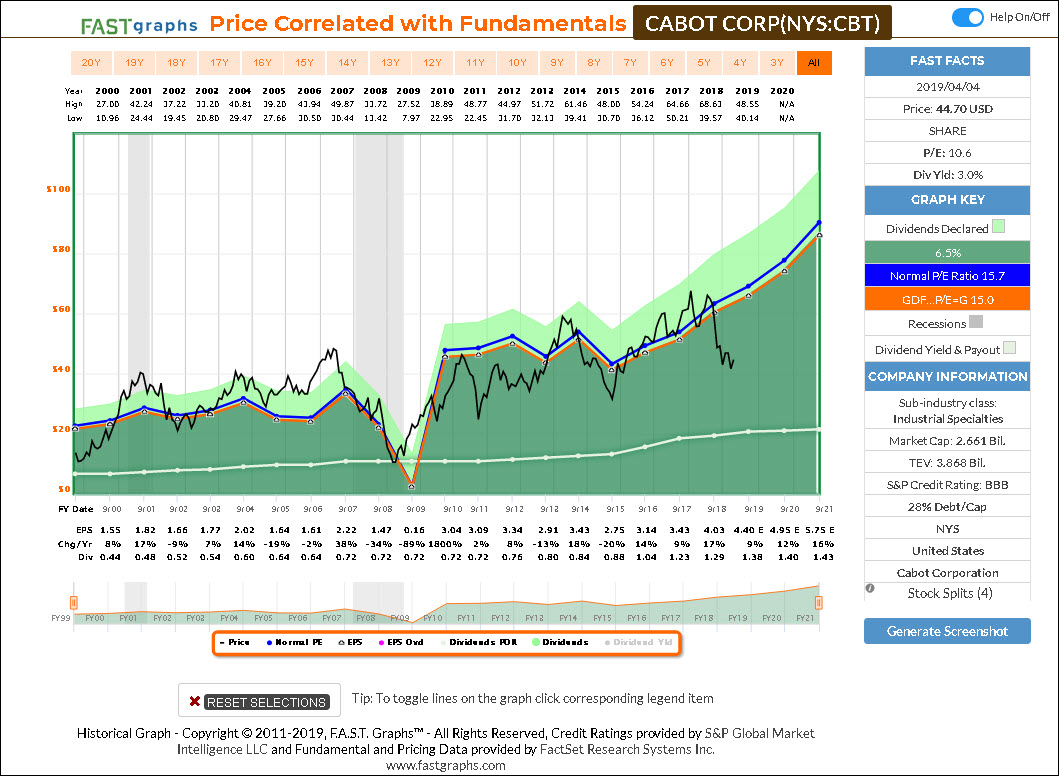

Cabot Corp (CBT)

Cabot Corp. is a global specialty chemicals and performance materials company. Its products are rubber and specialty grade carbon blacks, specialty compounds, fumed metal oxides, activated carbons, inkjet colorants, aerogel, cesium formate drilling fluids, and fine cesium chemicals. The company operates through the following segments: Reinforcement Materials, Performance Chemicals, Purification Solutions, and Specialty Fluids. The Reinforcement Materials segment involves the rubber blacks and elastomer composites product lines.

The Performance Chemicals segment combines the specialty carbons and compounds and inkjet colorants product lines into the specialty carbons and formulations business. The Purification Solutions segment refers to the activated carbon business and the specialty fluids segment. The Specialty Fluids segment represents the rental of cesium formate.

Cabot was founded by Godfrey Lowell Cabot in 1882 and is headquartered in Boston, MA.

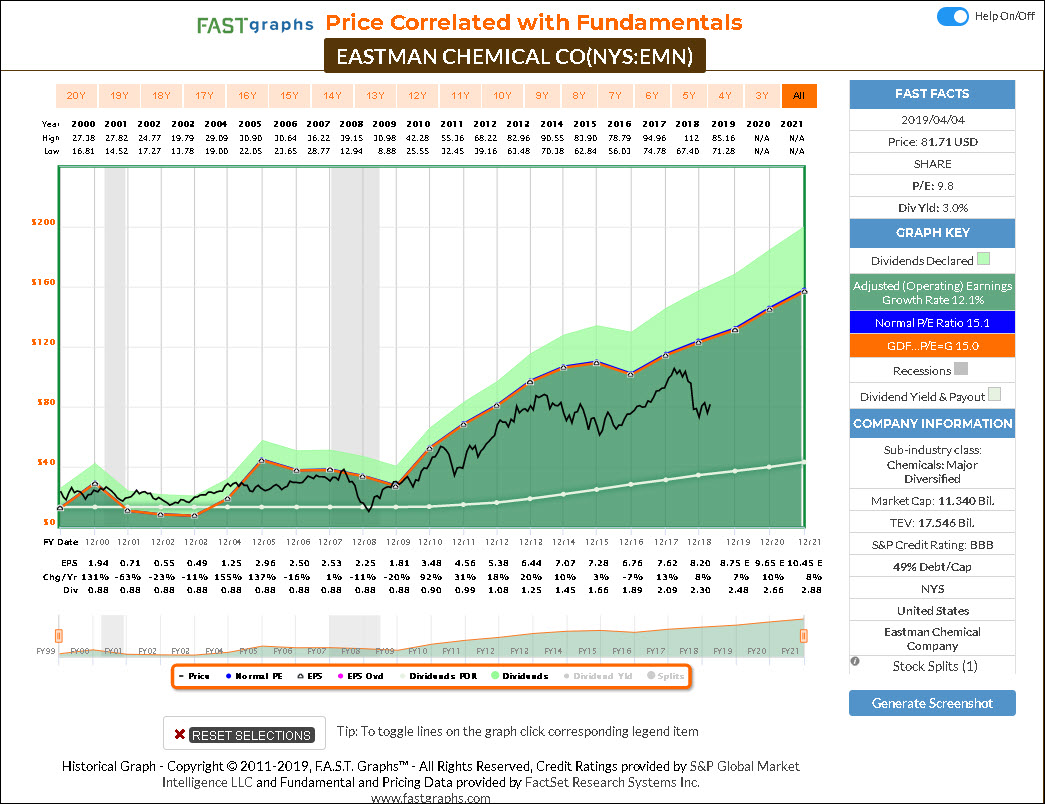

Eastman Chemical (EMN)

Eastman Chemical Co. engages in the provision of specialty chemicals. It operates through the following segments: Additives and Functional Products; Advanced Materials; Chemical Intermediates; and Fibers. The Additives and Functional Products segment includes chemicals for products in the transportation, consumables, building and construction, animal nutrition, crop protection, energy, personal and home care, and other markets.

The Advanced Materials segment produces and markets its polymers, films, and plastics with differentiated performance properties for value-added end uses in transportation, consumables, building and construction, durable goods, and health and wellness markets. The Chemical Intermediates segment consists of large scale and vertical integration from the cellulose and acetyl, olefins, and alkylamines streams to support operating segments with advantaged cost positions. The Fiber segment offers cellulose acetate tow for use in filtration media, primarily cigarette filters.

The company was founded by George Eastman in 1920 and is headquartered in Kingsport, TN.

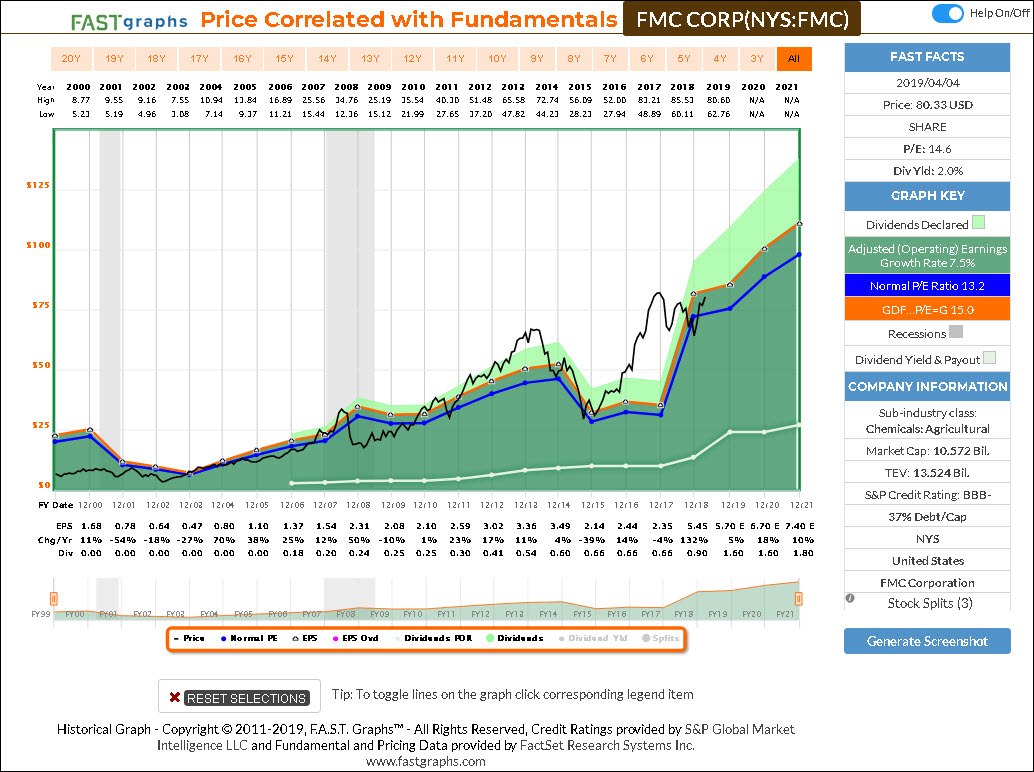

FMC Corp (FMC)

FMC Corp. engages in the provision of solutions, applications, and products for the agricultural, industrial, and consumer markets. It operates through two segments: FMC Agricultural Solutions and FMC Lithium.

The FMC Agricultural Solutions segment develops, markets, and sells all three major classes of crop protection chemicals: insecticides, herbicides and fungicides, which are used to enhance crop yield and quality. The FMC Lithium segment manufactures lithium for use in lithium products, which are used primarily in energy storage, specialty polymers, and chemical synthesis application.

The company was founded by John Bean in 1883 and is headquartered in Philadelphia, PA.

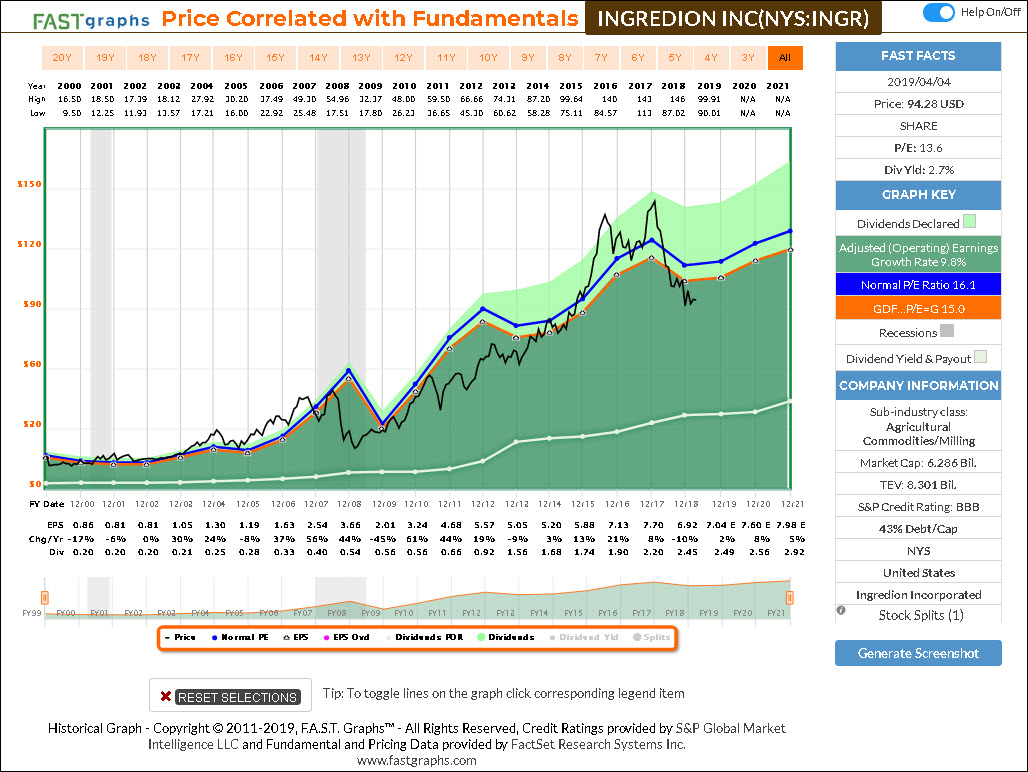

Ingredion Inc (INGR)

Ingredion, Inc. manufactures and sells sweetener, starches, nutrition ingredients, and biomaterial solutions derived from the wet milling and processing of corn and other starch based materials. Its activities include turning corn, tapioca, potatoes and other vegetables and fruits into value added ingredients and biomaterials for the food, beverage, paper and corrugating, brewing, and other industries.

The company was founded in 1906 and is headquartered in Westchester, IL.

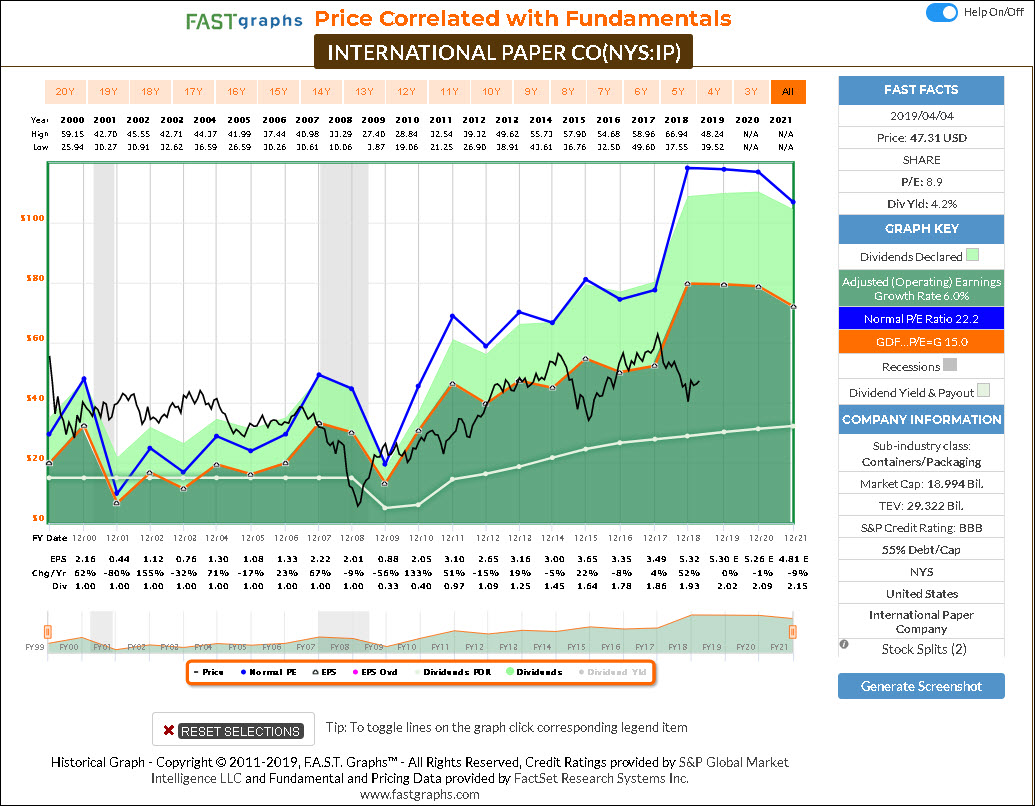

International Paper (IP)

International Paper Co. engages in the manufacture of paper and packaging products. It operates through the following segments: Industrial Packaging, Global Cellulose Fibers, and Printing Papers. The Industrial Packaging segment involves in the manufacturing of containerboards, which include linerboard, medium, whitetop, recycled linerboard, recycled medium, and saturating kraft. The Global Cellulose Fibers segment offers cellulose fibers product portfolio includes fluff, market, and specialty pulps. The Printing Papers segment includes manufacturing of the printing and writing papers.

The company was founded by Hugh J. Chisholm in 1898 and is headquartered in Memphis, TN.

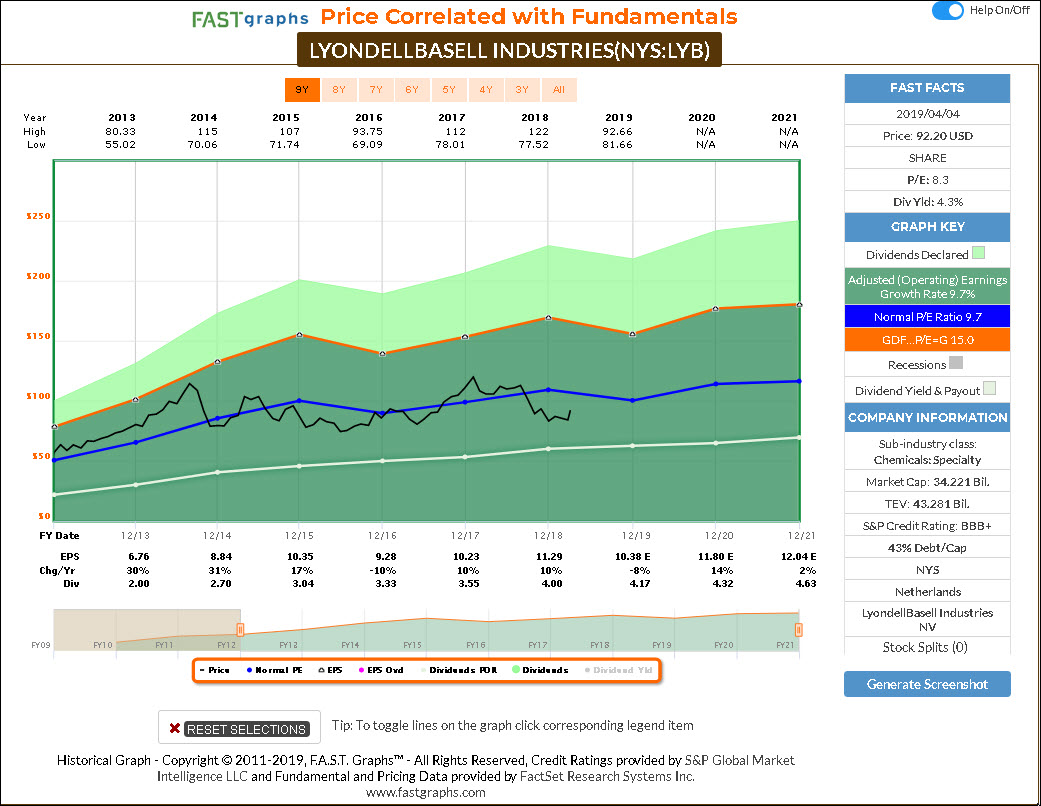

LyondellBasell Industries (LYB)

LyondellBasell Industries NV operates as an independent chemical company, which engages in the refinery and production of plastic resins and other chemicals. It operates through the following segments: Olefins and Polyolefins-Americas; Olefins and Polyolefins-Europe, Asia, International, Intermediates; and Derivatives; Refining; and Technology. The Olefins and Polyolefins-Americas segment produces and markets olefins which includes ethylene and ethylene co-products, and polyolefins.

The Olefins and Polyolefins-Europe, Asia, International segment offers olefins including ethylene and ethylene co-products, polyolefins and polypropylene compounds. The Intermediates and Derivatives segment makes propylene oxide and its co-products and derivatives, acetyls, and oxygenated fuels. The Refining segment supply gasoline and diesel fuel. The Technology segment develops chemical and polyolefin process technologies and manufactures and sells polyolefin catalysts.

The company was founded in December 2007 and is headquartered in London, the United Kingdom.

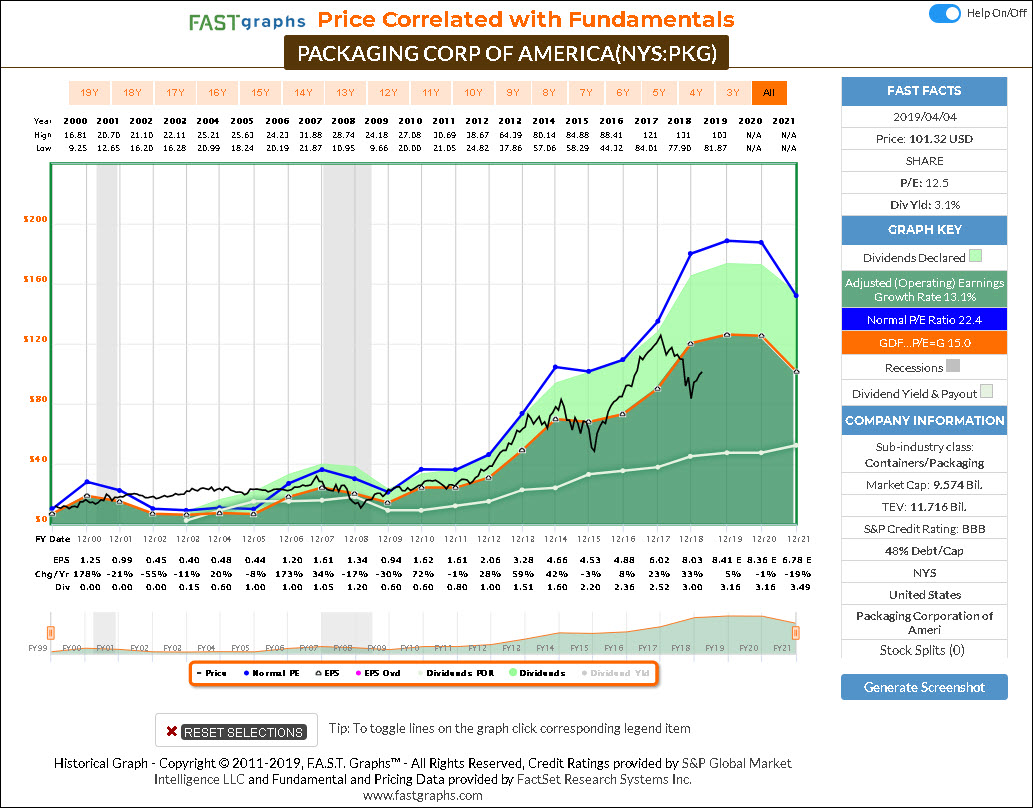

Packaging Corp of American (PKG)

Packaging Corp. of America engages in the production of container products. It operates through the following segments: Packaging, Paper, and Corporate and Other. The Packaging segment offers a variety of corrugated packaging products, such as conventional shipping containers. The Paper segment manufactures and sells a range of papers, including communication-based papers, and pressure sensitive papers. The Corporate and Other segment focuses on transportation assets, as well as rail cars, and trucks.

The company was founded in 1959 and is headquartered in Lake Forest, IL.

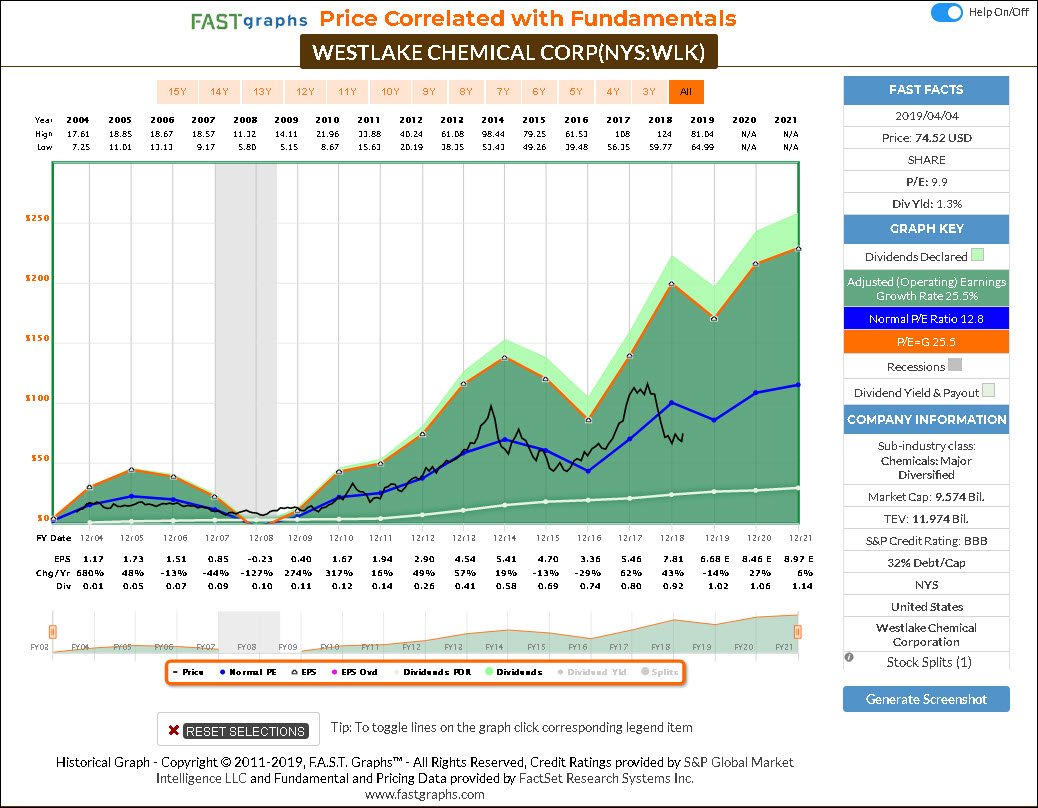

Westlake Chemical Corp (WLK)

Westlake Chemical Corp. manufactures and markets petrochemicals, polymers and fabricated building products. It operates through the Olefins and Vinyls segments. The Olefins segment manufactures ethylene, polyethylene, styrene, and associated co-products at the manufacturing facility in Lake Charles and polyethylene at the Longview facility.

The Vinyls segment manufactures and sells building products fabricated from polyvinyl chloride, including pipe, fittings, profiles, foundation, building products, fence and deck components, window, and door components, film, and sheet products.

The company was founded by Ting Tsung Chao in 1986 and is headquartered in Houston, TX.

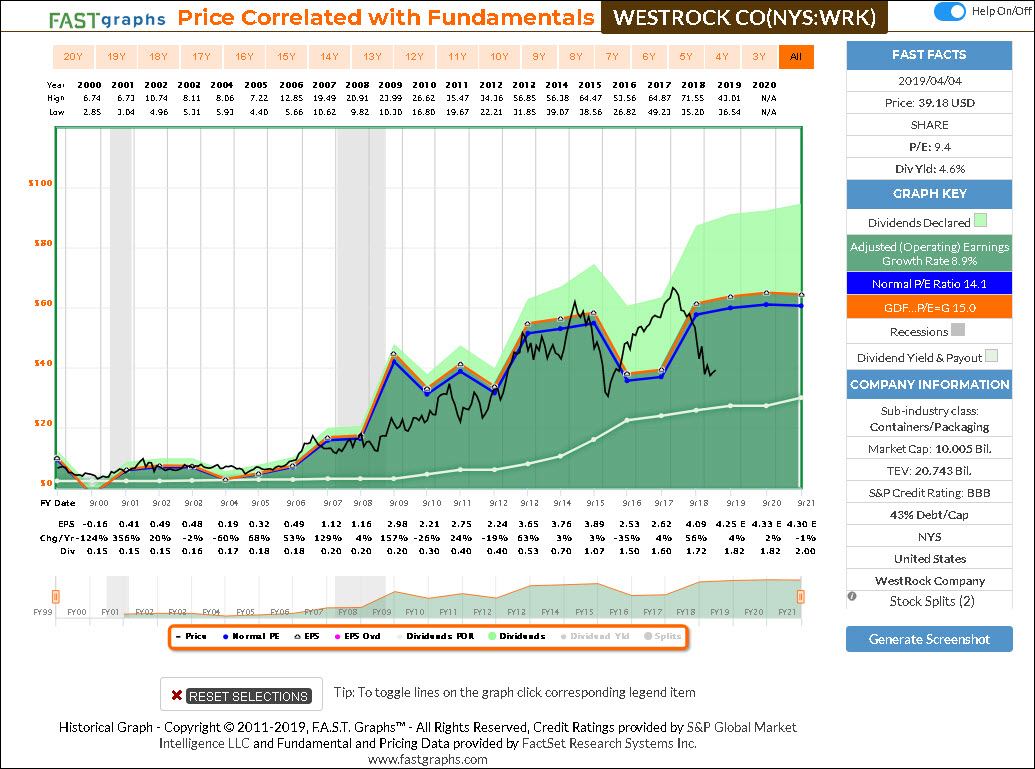

Westrock Co (WRK)

WestRock Co. engages in the provision of paper and packaging solutions. It operates through the following segments: Corrugated Packaging, Consumer Packaging, and Land and Development. The Corrugated Packaging segment consists of its containerboard mill and corrugated packaging operations, as well as recycling operations.

The Consumer Packaging segment includes consumer mills, folding carton, beverage, merchandising displays, and partition operations. The Land and Development segment sells real estate primarily in the Charleston, South Carolina region.

The company was founded on March 6, 2015 and is headquartered in Atlanta, GA.

F.A.S.T. Graphs Analyze Out Loud Video:

Summary and Conclusions

In part 13 of this series I covered the Non-Energy Minerals Sector and indicated that it was a sector that I was not too fond of investing in. In this part 14, I am covering a sector that – as I pointed out earlier -contains companies with very cyclical histories. As a rule, I prefer companies that produce consistent, predictable and reliable operating growth rates. I find companies with those attributes to be easier to evaluate, forecast and hold for the desired long-term period of time. Nevertheless, even though each of the research candidates presented in this article have cyclical histories, they have also dramatically outperformed the average company over time.

Consequently, as I stated in the title, I feel there are some exceptional long-term investments presented in this part 14 of this series. However, I do believe that prospective investors need to be cognizant of the cyclical nature of these companies and the short to intermediate-term results that that cyclicality might produce. Furthermore, I also pointed out earlier that investing in cyclicals at the bottom of a cycle can lead to exceptionally high short to intermediate-term results. The reason is simple. Cyclical companies can generate very high short to intermediate-term growth rates when they come off of the bottom of an earnings cycle. Moreover, typically when that does happen, great returns over the next few years quite often follow. Therefore, I suggest that prospective investors attempt to identify where these companies are in their operating cycles as part of their research and due diligence effort.

Disclosure: Long ADM,IP.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.