EM Versus DM Growth (2019-2023): How Global Is ‘Global’ Growth Really?

IMF recently lowered its growth rate forecast for the global economy. We expect growth to command a premium as it becomes scarcer, while growth laggards will be penalised. It is therefore important to unpack IMF’s global growth forecast to determine who is growing and who is slowing.

It turns out that slower ‘global’ growth is really a euphemism for slower developed market growth. Emerging Markets (EM) countries already contribute 74% of global growth and will contribute 84% by 2023. A lot of EM growth is concentrated in smaller economies, many of which barely feature on investors’ radar screens yet. Investors should therefore dramatically diversify their exposures across the EM universe, not just to protect against individual country risks, but also to generate better returns.

Why does growth matter?

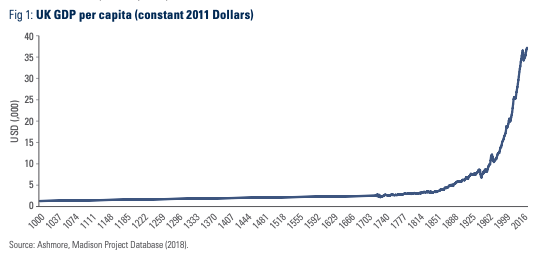

Prosperity is a relatively recent phenomenon. Consider the evolution of UK per capita GDP in constant 2011 Dollars as illustrated in Figure 1. Britain, erstwhile largest empire in the world, languished in abject poverty for most of the last thousand years; only in the last couple of hundred did per capita GDP begin to creep out of the primordial swamp. Even today, the majority of the world’s population suffers greatly from poverty. Growth is important because it affects the quality and quantity of life and exerts influence far beyond the narrow realm of human economic materialism, especially on politics and on the environment.

While there is no hard and fast link between growth and investment returns, investors understandably pay great attention to growth. The growth rate gives a reasonable indication of the investment environment in any given country. Faster growth tends to be associated with healthier credit fundamentals, better tax collection and higher company earnings, the latter associated with higher equity returns. Strong growth often pushes up term interest rates, which increases bank credit growth and supports currencies, thereby attracting foreign capital, which in turn can drive down default rates and reduce repayment risk. Rising growth rates also replenish political capital, which can lead to more stable politics, even economic reforms.1

Growth rates in large countries are particular important from a global growth perspective. In addition to benefitting the large country in question, fast growth in a large country can materially influence the entire global economy. This amounts to a positive externality, which means that large countries exert a disproportionate influence over global political and policy trends, the global military balance, trade and capital flows as well as risks, of course.

One of the most important differences between developed and EM countries is their growth dynamics during downturns in business cycles. EM countries typically have no choice but to engage in austerity and reforms during cyclical downturns, which can exaggerate the amplitude of the business cycle, i.e. sharp recessions, but then followed by strong, sustainable growth rates. By contrast, developed economies tend to increase fiscal spending and accumulate debt during downturns, which reduces the amplitude of downturns, but undermines productivity and trend growth rates over time due to neglect of deeper reforms.

Slower global growth ahead

It is against this backdrop that the IMF recently lowered its global growth forecast.2 The IMF now expects the world economy to slow from 3.7% in 2017 to 3.6% by 2020 and 3.5% by 2023. This means that the global economy will grow one third slower by 2023 than it did in the year before the Developed Markets’ Financial Crisis of 2008/2009 (5.6%).

Why is growth slowing? There are many reasons. The most important ones include:

• The end of the era of hyper-easy monetary policies in developed economies saddled with large debts and increasingly populist tax and spending policies.

• President Donald Trump’s trade war is hurting global supply-chains and denting business confidence.

• Europe’s irrepressible tribalism prevents reforms and sows division across the continent.

• China is slowing due to deep domestic economic reforms, but at least China’s reforms will sustain higher trend growth rates in the future.

Growth rates versus growth contribution

If IMF’s prediction of slower growth comes true, then markets will likely assign a premium to asset prices in countries with relatively stronger growth and penalise countries with relatively slower growth. This means that investors will increasingly have to distinguish more clearly between countries in terms of their capacity to grow. It turns out that IMF’s ‘global’ growth projections for the next five years contain dramatically different growth trajectories for EM countries versus developed economies.

IMF’s slowing global growth forecast conceals an extremely dramatic slowdown in developed economies from 2.4% in 2017 to just 1.4% by 2023, that is, a slowdown of about a third over the period. By contrast, IMF expects EM economies to grow marginally faster from 4.7% in 2017 to 4.8% by 2023.3 It is therefore not unfair to characterise IMF’s entire ‘global’ slowdown as a slowdown in developed economies in both absolute terms and relative to EM, at aggregate level. Figure 2 illustrates this important point. The growth differential between EM countries as a group and developed economies as a group rises every single year over the next five years. Incidentally, this is not just due to slower growth in Europe; EM growth also rises relative to US growth every single year in the next five years. Indeed, IMF expects the US to grow only 1.4% by 2023.

To what extent is the faster average growth in EM countries due to just a few atypical outliers? Figure 3 answers this question by way of a histogram of distribution of growth rates within EM and developed countries, based on the average growth rates from 2019 to 2023 for individual countries within the EM and developed market groups.4 The key take-away from Figure 3 is that EM growth rates tend to cluster towards the far right of the distribution, which means that high growth is a relatively widespread phenomenon within EM. In fact, the mode of the distribution – i.e., the single largest group of countries – is the +5% real GDP growth group. By contrast, growth rates in developed countries distribute relatively evenly around a rather unexciting mode of just 2%.

The fact that so many EM countries have high growth rates makes them more resilient as a group in the context of a slower global growth environment. The simple fact that they grow faster to begin with means that their growth rates have to slow down more and for longer before they drop into outright recession. This advantage actually increases over time relative to developed markets, because the distribution of growth rates for developed economies shifts visibly to the left between 2019 and 2013, while the distribution of EM growth does not shift visibly one way or the other (Figure 4)

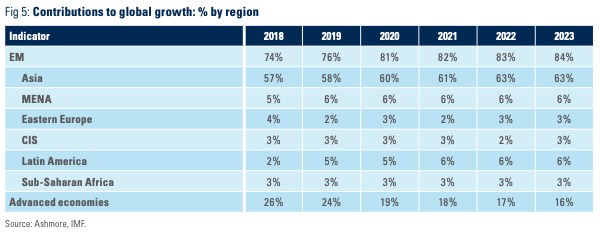

EM countries are not only growing faster, but they are also rapidly becoming very large economies, which means that their growth rates are becoming more important for global growth. Any country’s contribution to global growth depends on its growth rate as well as its size. If one thinks of growth as a source of buying power, then comparison of growth rates should be done using purchasing power parity adjusted exchange rates.5 Using this method, Figure 5 shows that EM countries contributed a massive 74% of global growth in 2018, but that this contribution rises to a startling 84% by 2023. The contribution of developed economies to global growth correspondingly shrinks from 26% in 2018 to just 16% by 2023.6 In short, EM countries are already overwhelmingly driving global growth rates and will do so even more in the next five years.7

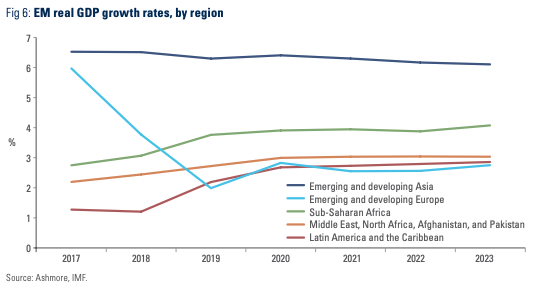

The pickup in EM versus developed economies’ growth rates is very broad based. IMF’s forecasts show that growth rates will rise across EM regions starting in 2019 and will continue to rise through 2023. The only exception Asia, where growth will moderate gently, although despite its slowdown, Asia will remain by far the fastest growing region in the world (Figure 6). The principal reason for the gentle moderation in Asian growth is that China continues to reform as part of its transition from rapid investment/export-led growth to more sedate consumption-led growth.

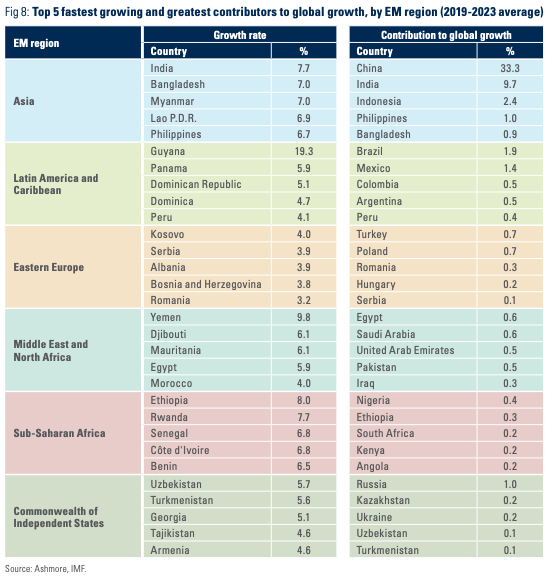

Who are the big global growth superstars? If one thinks of global growth superstars as countries, which both feature within the Top 20 fastest growth countries and the Top 20 contributors to global growth then there are very few indeed. As Figure 7 shows, only India, Bangladesh and Philippines fit this criterion.8 This is not necessarily a bad thing. The fact that the fastest growing countries are all in EM shows that convergence is happening between rich and poor countries. The fact that the largest contributors to global growth now also include many EM countries is also a sign that global growth has ‘broader shoulders’ than in the past, where EM countries did not contribute as much as they do now. As we shall see shortly, the broadening of the base of global growth also has important investment implications.

Perhaps the most important observation from Figure 7 is that every single country in the Top 20 fastest growing economies is an EM country. In fact, no developed economy features in the first ninety-eight fastest growing countries in the world. On other hand, many of the fast growing EM countries are small. Their solid growth rates makes them individually attractive as investment destinations, but their small size limits the capacity to invest there. This underlies the absolute importance of seeking diversification across EM, including being willing to go off benchmark. With 91% of EM bonds still not formally represented in the main EM fixed income benchmarks, many of these countries have strong growth, the best way to balance the desirability to invest in such countries with their small markets is to take small exposure to a very large number of them.

It is also clear from Figure 7 that EM countries make up exactly half of the Top 20 contributors to global growth. In other words, big EM countries are just as important for global growth as big developed countries. Large EM countries therefore ought to be represented better within global governance institutions, such as IMF, World Bank and the United Nations. Failure to give large EM countries the representation they deserve weakens global governance, for example, by causing parallel institutions to be established and increases rivalries between large nations to the further detriment of global growth.

Regional superstars are countries, which are in the Top 5 fastest growing economies in their region as well as in the Top 5 growth contributors. Figure 8 lists the fastest growing and greatest contributors to global growth within each of the main EM geographical regions. Reflecting the broad-based nature of EM growth these days, there are very few regional superstars:

• Asia has three regional superstars (India, the Philippines and Bangladesh)

• Eastern Europe and Commonwealth of Independent States each have two regional superstars (Uzbekistan, Turkmenistan, Romania and Serbia)

• Sub Saharan Africa, Middle East & North Africa and Latin America each have one regional superstar (Ethiopia, Egypt and Peru).

These special countries bear closer scrutiny in the coming years, since they are growth success stories in their own right, but they will also likely be growth drivers for their entire regions.

Conclusions Growth

is important. It reduces mortality and improves the quality of life, influences political life and the environment. Investors care about growth, because higher growth rates tend to be associated with better investment performance and strong growth in large countries materially influences the global economy. The recent downgrade in IMF’s global growth forecasts is therefore worrisome. However, closer inspection shows that practically all of the slowdown in IMF’s so-called ‘global’ growth is due to slower growth in developed countries, while EM growth is set to rise marginally. Strong growth is broad-based across EM with the single biggest group of EM countries being those with +5% growth rates over the next half a decade, while the distribution of growth rates in developed economies actually shifts meaningfully to the left over the same period as detailed in Figure 4 above. This means that EM countries, which already contribute 74% of all growth in the world today, will contribute 84% by 2023. All EM regions will grow faster between 2019 and 2023 with the exception of Asia, which nevertheless grows much faster than any other region in the world.

As growth becomes scarcer investors need to factor in these very material differences in growth rates between EM countries and developed economies, because markets will likely attach a premium to faster growing economies and a penalty to the laggards.

There are very few global growth superstars, these are countries that can claim to be both in the Top 20 for their growth rates as well as their contribution to global growth. All three, however, are in EM. The fact that global growth does not hinge on a small number of countries is a good thing. A broader base for global growth is a source of security for the world economy. There is strong growth across a large number of EM countries. This means that investors should seek to diversify their investments across as many EM countries as possible, not just to protect against risk, but also in order to increase returns. Investors should also pay attention to the small new and in some cases quite surprising group of regional superstars, which are likely to become important growth drivers within their own regions.

1 Growth may not translate into higher returns, if say; the stronger growth rates are already factored into the price. Strong growth can certainly be associated with poor technicals, bubble risks, environmental degradation, rising inequality, late cycle concerns, inflation, tighter monetary policies and other nasty things. However, on balance, when faced with the choice between fast and slow growth, investors prefer strong growth any day of the week.

2 See for example https://www.wsj.com/articles/imf-lowers-2019-global-growth-forecast-11548075601

3 See https://www.imf.org/en/Publications/WEO/Issues/2019/01/11/weo-update-january-2019

4 The averages cover 2018-2023 for each individual country. IMF produces growth forecasts for 193 countries of which 155 (80%) are classified as Emerging Market countries.

5 IMF notes that the Purchasing-power-parity (PPP) exchange rate (or conversion rate) between two countries is the rate at which the currency of one country needs to be converted into that of a second country to ensure that a given amount of the first country’s currency will purchase the same volume of goods and services in the second country as it does in the first.

6 Incidentally, using market exchange rates does not change the main conclusion. EM’s contribution to global growth rises from 56% in 2018 to 71% by 2023.

7 There is great variation in sizes of countries. Out of the 193 countries for which IMF makes forecasts, some eighty-six (45%) have GDP of USD 25bn or below, another forty-three countries (22%) have GDP between USD 25bn and USD 100bn, forty-eight have GDP between USD 100bn and USD 1trn and only sixteen countries have GDP in excess of USD 1trn.

8 Ranking is based on the individual average growth rates of the countries and the individual average contribution to global growth from 2019 to 2023.