10 Fairly Valued MLPs: Are the High Yields Worth the Risk and Effort? Part 12

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIntroduction

A major goal of this series on sectors is to illustrate the reality that it is a market of stocks rather than a stock market. With this article I am technically covering the Industrial Services Sector. However, all the research candidates I will be presenting come from the Oil & Gas Pipelines subsector. There is probably no better example illustrating how different companies are from each other than an examination of the unique attributes of oil and gas pipeline companies.

For starters, there are important tax considerations to be considered when investing in MLPs. These entities issue a K-1 that must be included in the investor’s tax filing. This factor alone deters many investors from investing in MLPs. On the other hand, there are tax advantages associated with investing in them that are worth the aggravation of the K-1’s for other investors. However, it is not the objective of this article to delve deeply into the intricacies of the tax advantages or complications of investing in MLPs. Instead, they are offered as research candidates that provide high tax advantaged yields that I also consider attractively valued currently. Although I do feel that it is appropriate that I mention these issues in this article, I leave it up to the individual investor to do their own due diligence.

There is an additional attribute that is common to MLPs that I believe is not discussed anywhere near enough. MLPs are very capital-intensive entities that require large capital investments to maintain and grow their revenues. Consequently, they are chronic issuers of new shares necessary to raise the capital they need to grow and expand their operations. This significant dilution associated with MLPs is a primary reason why I do not think it makes sense to value them based on earnings. A deep examination will show that most MLPs have earnings-based dividend payout ratios that are very high and often multiples of their earnings.

Other unique attributes of MLPs are significant capital investments leading to large depreciation schedules and significant increases in revenues. Therefore, I will be illustrating the valuation of the 10 MLP research candidates in this article based on EBITDA multiples rather than earnings multiples. The E in EBITDA stands for earnings. However, I see this as a soft form of cash flow because it is before interest, taxes depreciation and amortization. Therefore, I would argue that EBITDA better reflects the per-share benefits to their shareholders than highly diluted and depreciated traditional earnings metrics.

In the analyze out loud video associated with this article I will be covering these unique attributes more fully. Nevertheless, because of the complexity and nuisance of the K-1, the reality of the need to raise capital and the associated dilution, MLPs are not attractive to all investors. This is often in spite of the fact that there are very few investments that generate better cash flows and growth of those cash flows than MLPs.

A Sector By Sector Review

This is part 12 of a series where I have conducted a simple screening looking for value over the overall market based on industry classifications and subindustry classifications reported by FactSet Research Systems, Inc.

In part 1 found here I covered the Consumer Services Sector. In part 2 found here I covered the Communication Sector. In part 3 found here I covered the Consumer Durables Sector and its many diverse subsectors. In part 4 found here I covered Consumer Nondurables. In part 5 found here I covered companies in the Consumer Services Sector. In part 6 found here I covered the Distribution Services Sector. In part 7 found here I covered the Electronic Technology Sector. In part 8 found here I covered the Energy Minerals Sector. In part 9 found here I covered the Finance Sector. In part 10 found here I covered the Health Services Sector. In part 11 found here I covered the Health Technology Sector.

In this part 12 I will be covering the Industrial Services Sector.

In each article in this series, I will be providing a listing of screened research candidates from each of the following industry sectors, the sector I’m covering in this article is marked in green:

Sector 12: Industrial Services

Contract Drilling

Oilfield Services/Equipment

Engineering & Construction

Environmental Services

Oil & Gas Pipelines

A Simple Valuation and Quality Screening Process

With this series of articles, I will be presenting a screening of companies that have become attractively valued primarily as a result of the bearish market activities experienced in 2018 from each of the above sectors. I will be applying a rather simple valuation and quality-oriented screen across each of the sectors. First, I have screened for investment-grade S&P credit ratings of BBB- or above. Next, I have screened for low valuations based on P/E ratios between 2 and 17. Finally, I have screened for long-term debt to capital no greater than 70%.

By keeping my screen simple, and at the same time rather broad, I will be able to identify attractively valued research candidates that I might have overlooked through a more rigorous screening process. In other words, I’m looking for fresh ideas that I might have previously been overlooking. Furthermore, I want to be clear that I do not consider every candidate that I have discovered as suitable for every investor. However, I do consider them all to be attractively valued. Additionally, I also believe that every investor will be able to find companies to research that meet their own goals, objectives and risk tolerances as this series unfolds. However, this particular sector focuses on investors seeking high yield.

Portfolio Review: Industrial Services Sector: 10 Research Candidates

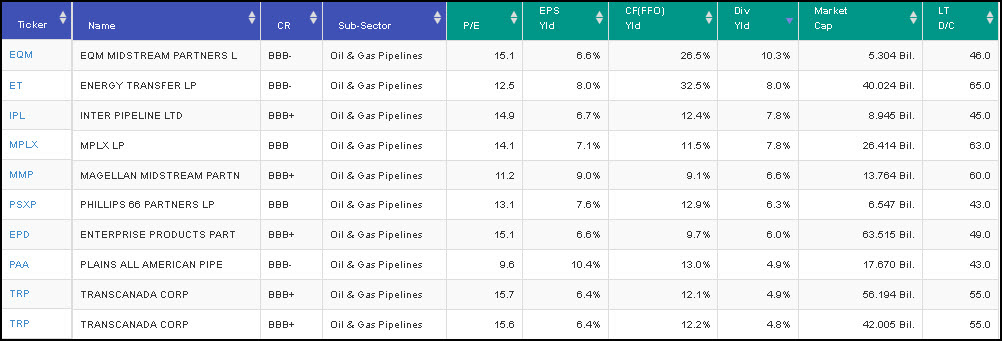

The following high yield oil and gas pipeline research candidates are listed in order of highest to lowest yield.

FAST Graphs Screenshots of the 10 Research Candidates

The following screenshots provide a quick look at each of the 10 candidates screened out of over 19,000 possibilities. However, there are only 1,264 companies categorized as Health Technology, and these 10 were the only ones I was comfortable presenting in this article. The company descriptions are provided courtesy of the Wall Street Journal. In the FAST Graphs analyze out loud video that follows the screenshots, I will provide additional details and thoughts on the possible attractiveness as well as the potential negatives of each of these research candidates.

Note: since these are high-yielding MLPs I am presenting these research candidates utilizing the EBITDA metric instead of the operating earnings metric I traditionally have utilized. The reason I’m doing this is because a common characteristic of MLPs is raising capital by issuing additional shares. Consequently, there is an enormous amount of dilution associated with these corporate structures.

In the FAST Graphs analyze out loud video that follows the screenshots, I will provide additional details and thoughts on the possible attractiveness as well as the potential negatives of each of these research candidates.

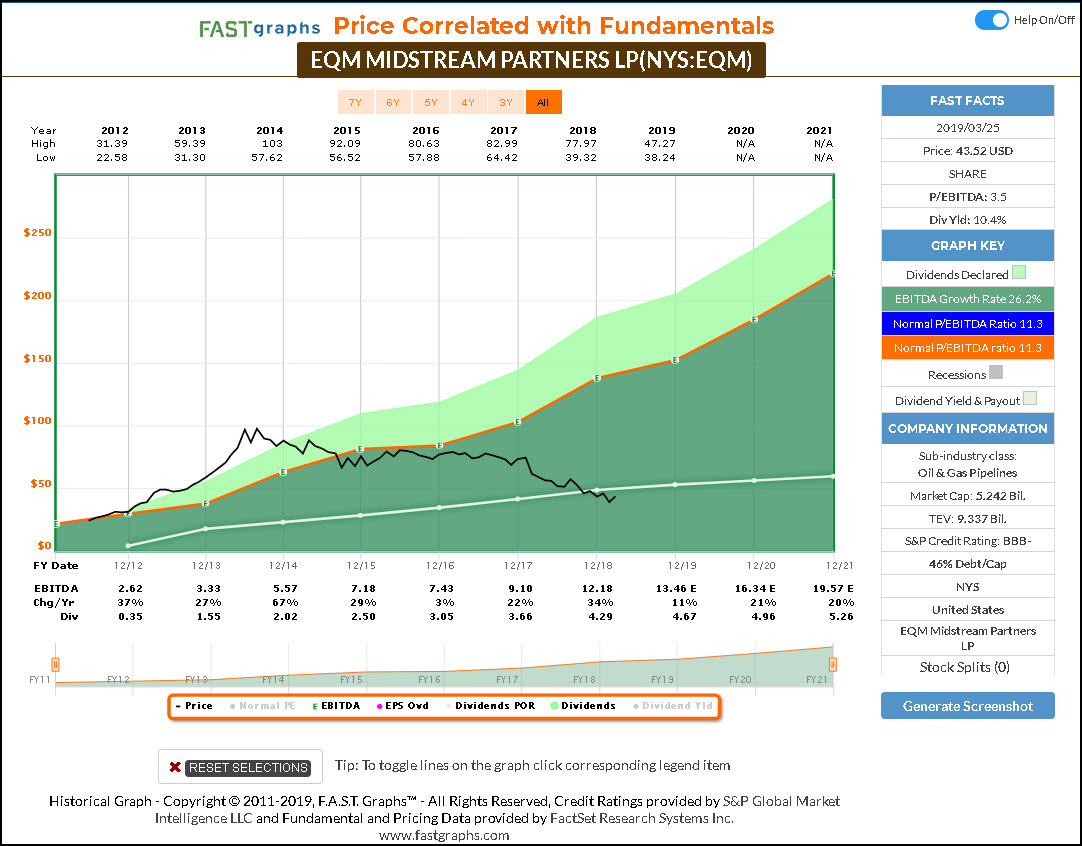

EQM Midstream Partners (EQM)

EQM Midstream Partners LP engages in the ownership, operation, acquisition, and development of midstream assets in the Appalachian Basin. It operates through the following segments: Gathering, Transmission and Water.

The company was founded on January 18, 2012 and is headquartered in Pittsburgh, PA.

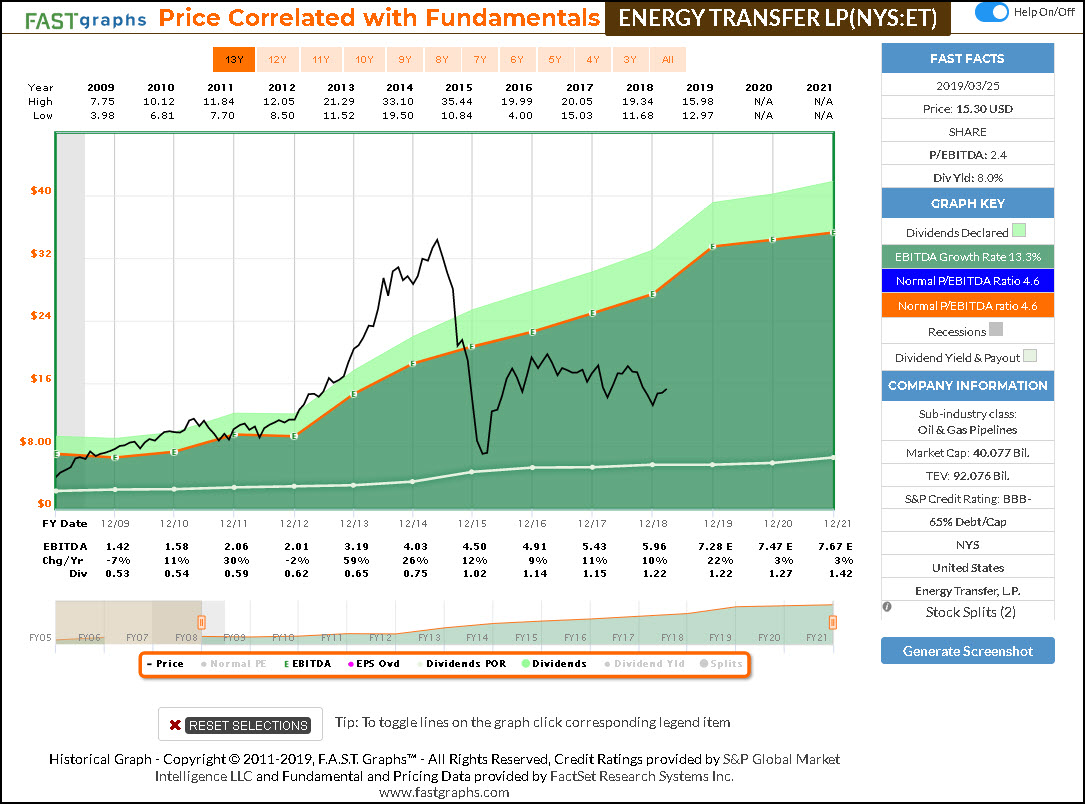

Energy Transfer (ET)

Energy Transfer LP provides natural gas pipeline transportation and transmission services. It operates through following segments: Investment in ETP, Investment in Sunoco LP, Investment in Lake Charles LNG, and Corporate and Other.

The Investment in ETP segment engages in the gathering and processing, compression, treating and transportation of natural gas, focusing on providing midstream services in some of the most prolific natural gas producing regions in the United States, including the Eagle Ford, Haynesville, Barnett, Fayetteville, Marcellus, Utica, Bone Spring and Avalon shales. The Investment in Sunoco LP segment is engaged in the wholesale distribution of motor fuels to convenience stores, independent dealers, commercial customers, and distributors, as well as the retail sale of motor fuels and merchandise through Sunoco LP operated convenience stores and retail fuel sites.

The Investment in Lake Charles LNG segment is engaged in interstate commerce and is subject to the rules, regulations and accounting requirements of the FERC. The Corporate and Other segment engages in the activities of the parent company.

Energy Transfer was founded in September 2002 and is headquartered in Dallas, TX.

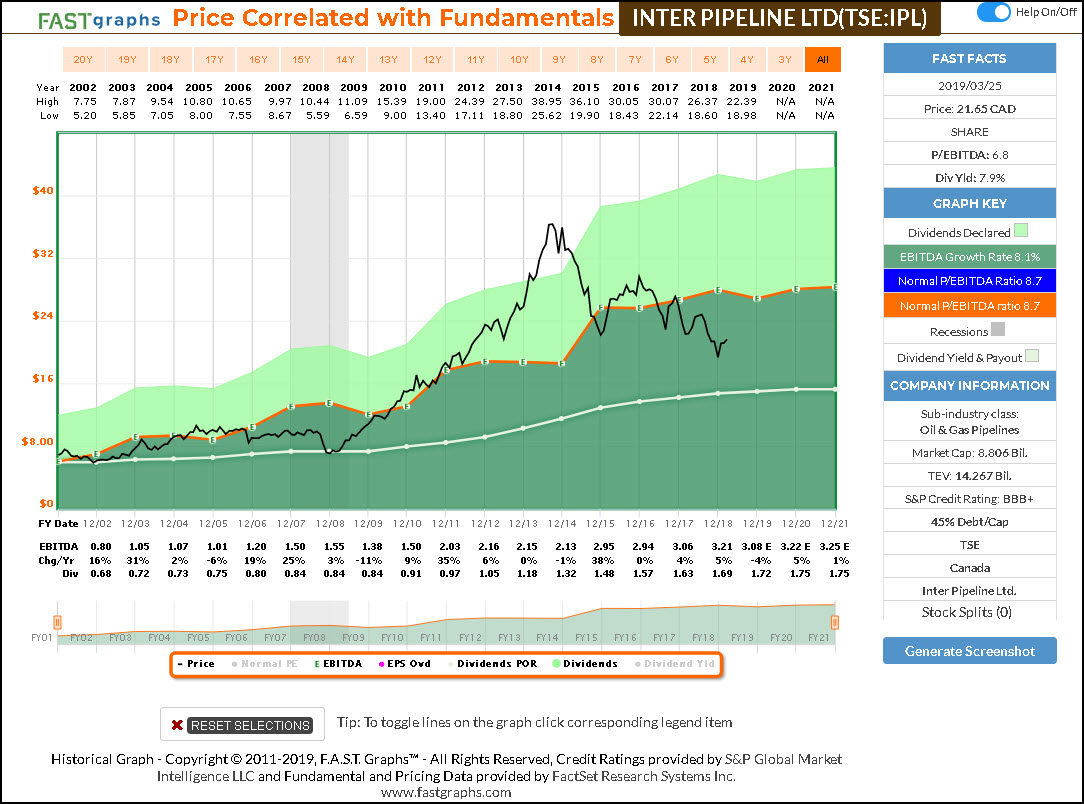

Inter Pipeline (TSE:IPL)

Inter Pipeline Ltd. is a midstream oil and natural gas company, which engages in the provision of oil transportation, natural gas liquid processing, and bulk liquid storage services. It operates through the following segments: Oil Sands Transportation, Conventional Oil Pipelines, Natural Gas Liquids (NGL) Processing, Bulk Liquid Storage, and Corporate. The Oil Sands Transportation segment consists of the Cold Lake, Corridor, and Polaris pipeline systems that transport petroleum products and provide related blending and handling services in Alberta.

The Conventional Oil Pipelines segment primarily implicates the transportation, storage, and processing of hydrocarbons, as well as midstream marketing blending and handling services. The NGL Processing segment comprises of processing natural gas to extract NGLs including ethane and a mixture of propane, butane and pentanes plus. The Bulk Liquid Storage segment involves the primary storage and handling of bulk liquid products through the operation of sixteen bulk liquid storage terminals. The Corporate segment consists of general and administrative costs.

The company was founded on October 9, 1997 and is headquartered in Calgary, Canada.

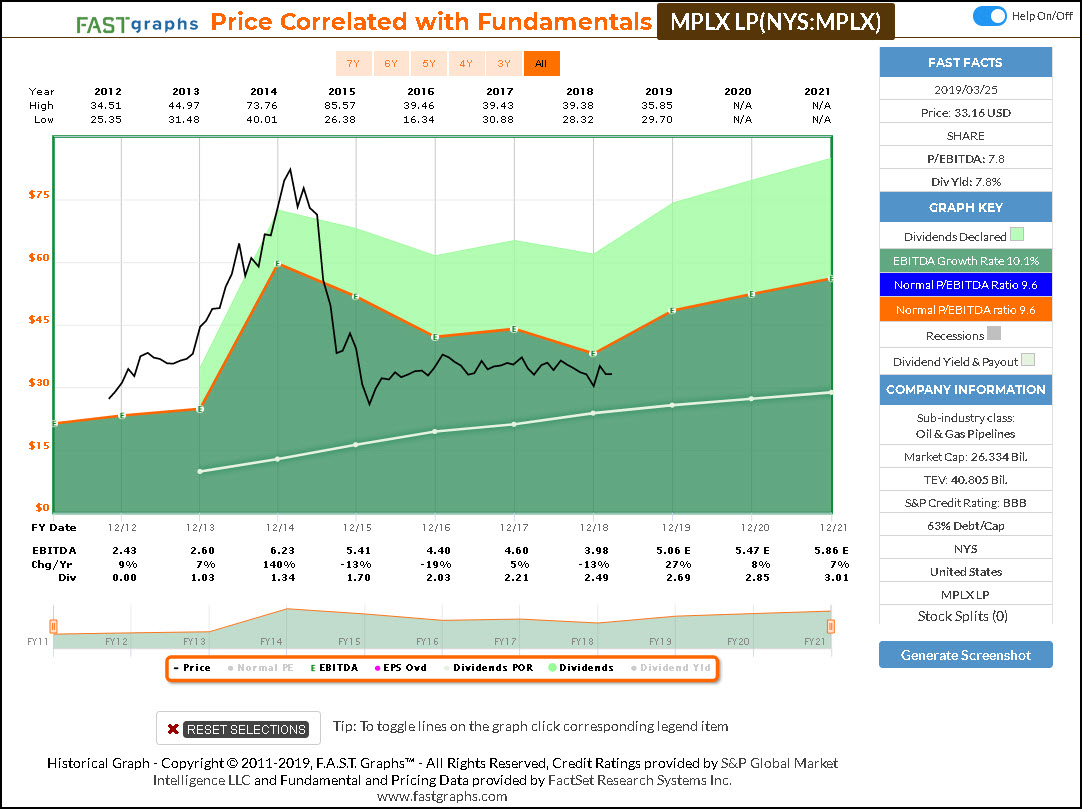

MPLX LP (MPLX)

MPLX LP is a fee-based, growth-oriented limited partnership company. It is engaged in the gathering, processing and transportation of natural gas; the gathering, transportation, fractionation, storage and marketing of natural gas liquids; and the gathering, transportation and storage of crude oil and refined petroleum products.

The company operates through two segments: Logistics & Storage and Gathering & Processing. The Logistics and Storage segment includes transportation and storage of crude oil, refined products and other hydrocarbon-based products. The Gathering and Processing segment engages in gathering and processing of natural gas.

MPLX was founded in March 27, 2012 and is headquartered in Findlay, OH.

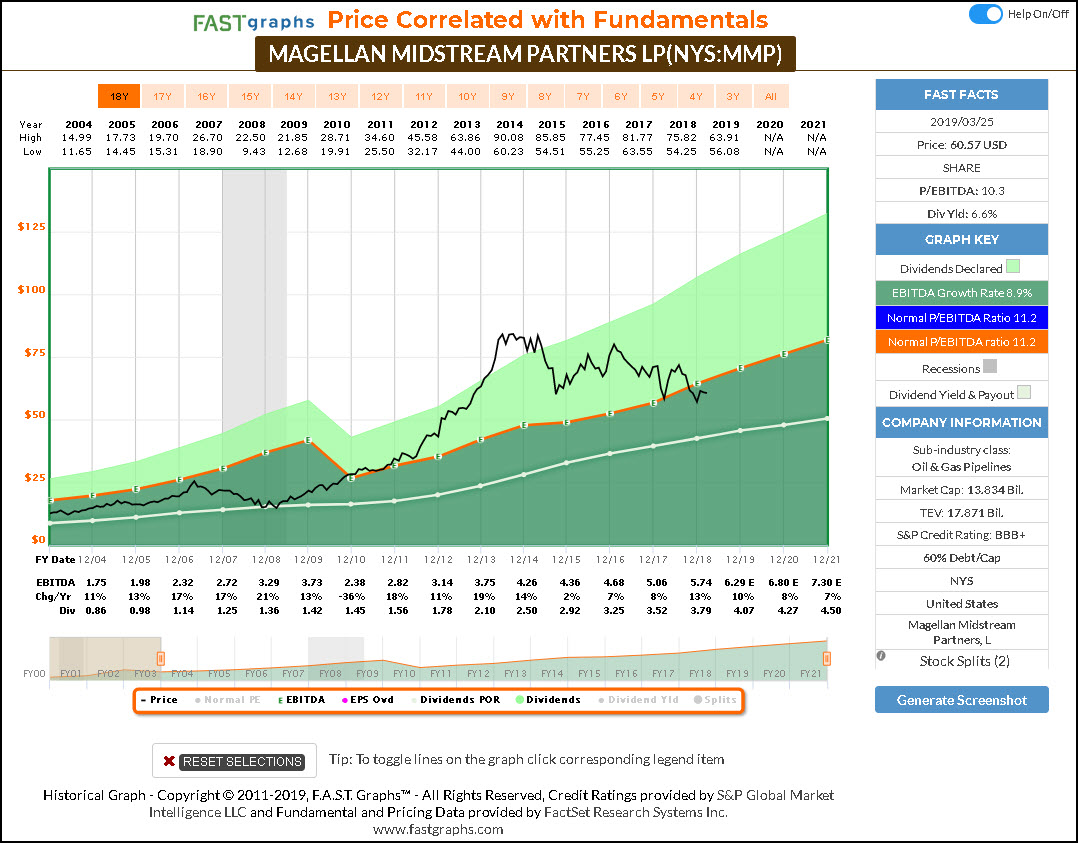

Magellan Midstream Partners (MMP)

Magellan Midstream Partners LP engages in the transportation, storage and distribution of petroleum products, such as crude oil. It operates through the following segments: Refined Products, Crude Oil and Marine Storage.

The Refined Products segment consists of common carrier refined products pipeline system, independent terminals, and its ammonia pipeline system. The Crude Oil segment comprises of crude oil pipelines, splitter and storage facilities which are used for contract storage. The Marine Storage segment includes marine terminals located along coastal waterways.

The company was founded in August 2000 and is headquartered in Tulsa, OK.

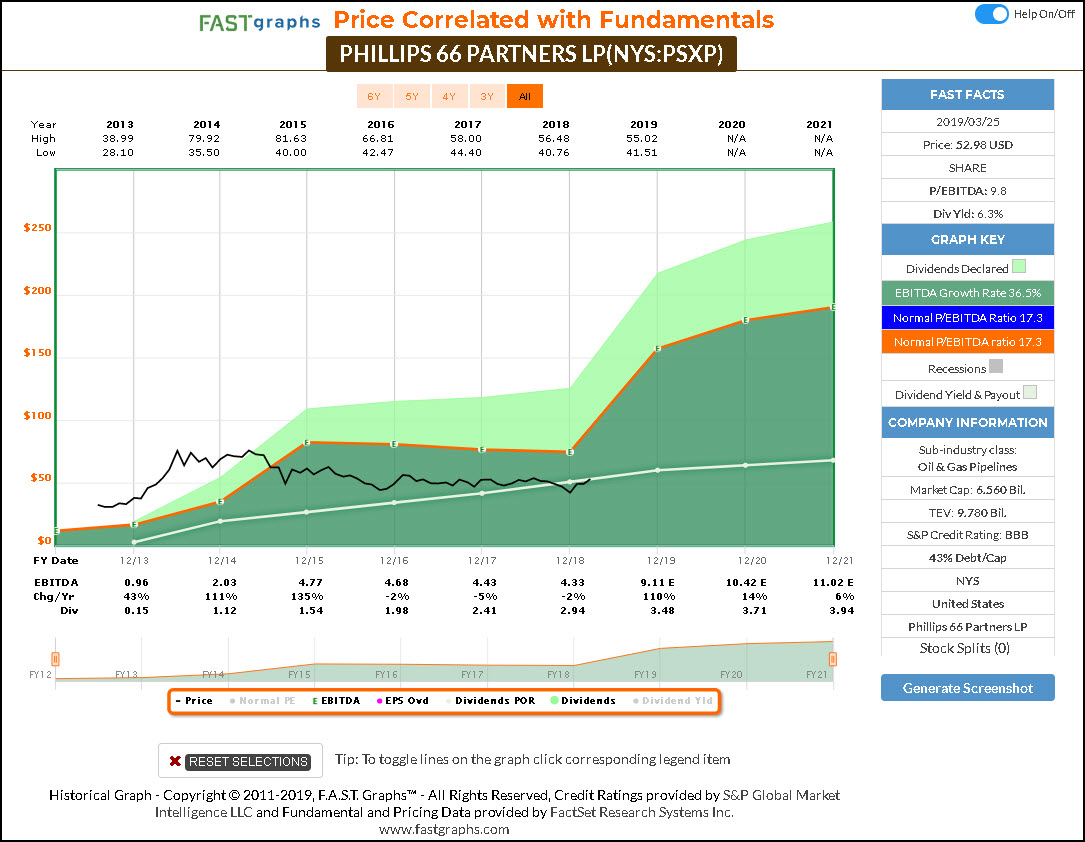

Phillips 66 Partners (PSXP)

Phillips 66 Partners LP engages in the ownership, operation, development, and acquisition of fee-based crude oil, refined petroleum product and natural gas liquids pipelines and terminals, and other transportation and midstream assets. It also provides terminals and storages for oil and petroleum products.

The company was founded on February 20, 2013 and is headquartered in Houston, TX.

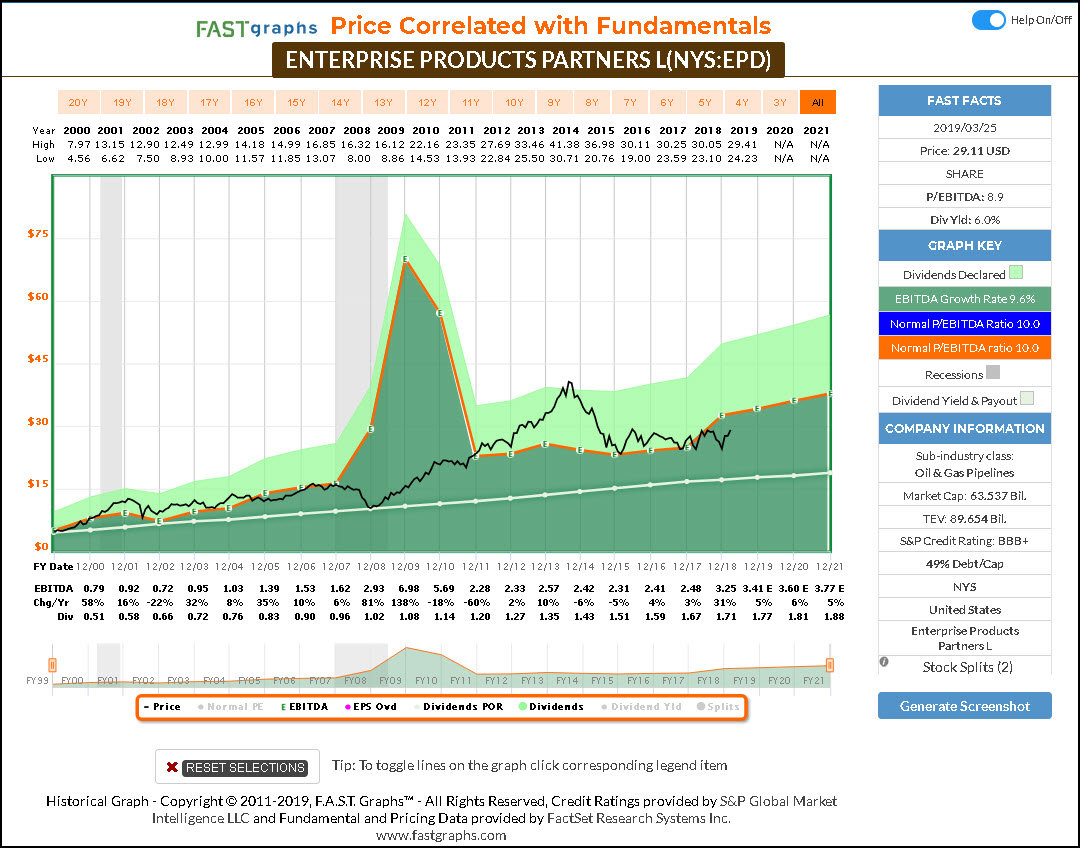

Enterprise Products Partners (EPD)

Enterprise Products Partners LP operates as holding company, which engages in the production and trade of natural gas and petrochemicals. It operates through the following segments: NGL Pipelines & Services; Crude Oil Pipelines & Services; Natural Gas Pipelines & Services; and Petrochemical & Refined Products Services.

The NGL Pipelines & Services segment manages natural gas processing plants. The Crude Oil Pipelines & Services segment stores and markets crude oil products. The Natural Gas Pipelines & Services segment stores and transports natural gas. The Petrochemical & Refined Products Services segment offers propylene fractionation, butane isomerization complex, octane enhancement, and refined products.

The company was founded by Dan L. Duncan in April 1998 and is headquartered in Houston, TX.

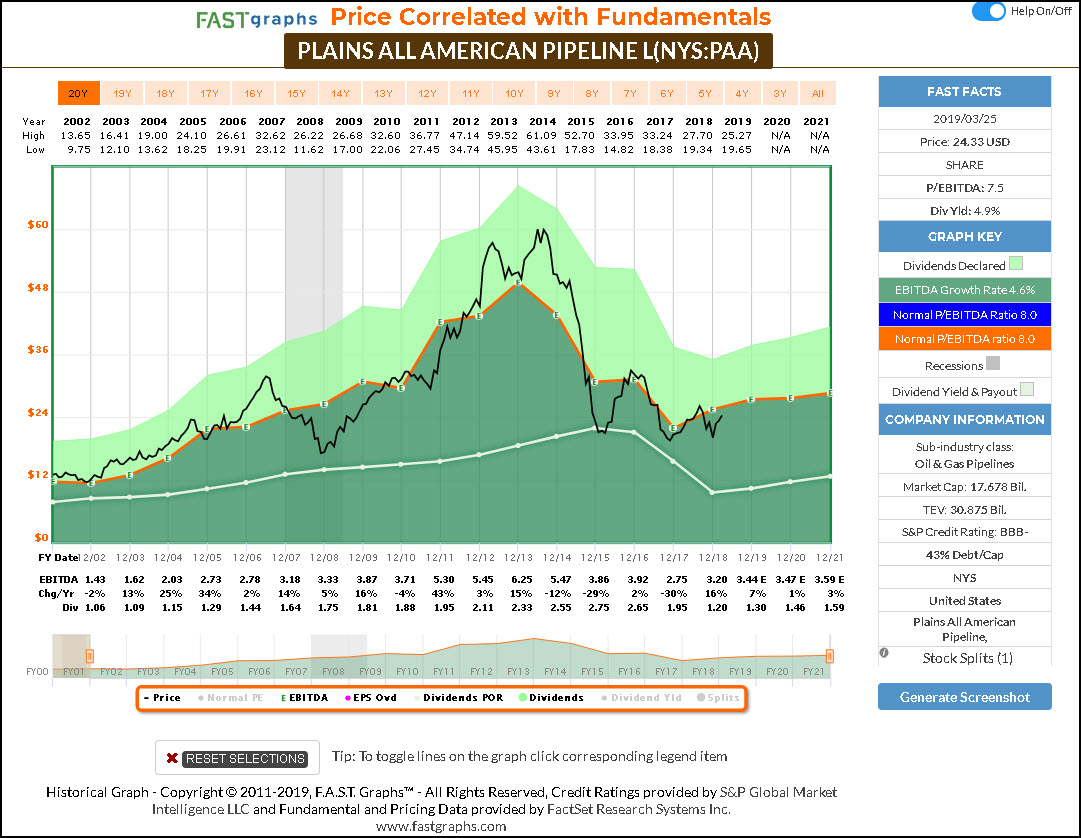

Plains All American Pipeline (PAA)

Plains All American Pipeline LP engages in the provision of transportation, storage, terminalling and marketing of crude oil, refined products and other natural gas-related petroleum products. It operates through the following business segments: Transportation, Facilities, and Supply and Logistics. The Transportation segments consist of fee-based activities associated with transporting crude oil and refined products on pipelines, gathering systems, trucks and barges.

The Facilities segment includes fee-based activities associated with providing storage, terminalling and throughput services for crude oil, refined products, and natural gas, as well LPG fractionation and isomerization services. The Supply and Logistics segment is engaged in the sale of gathered and bulk-purchased crude oil and natural gas liquids volumes.

The company was founded in 1998 and is headquartered in Houston, TX.

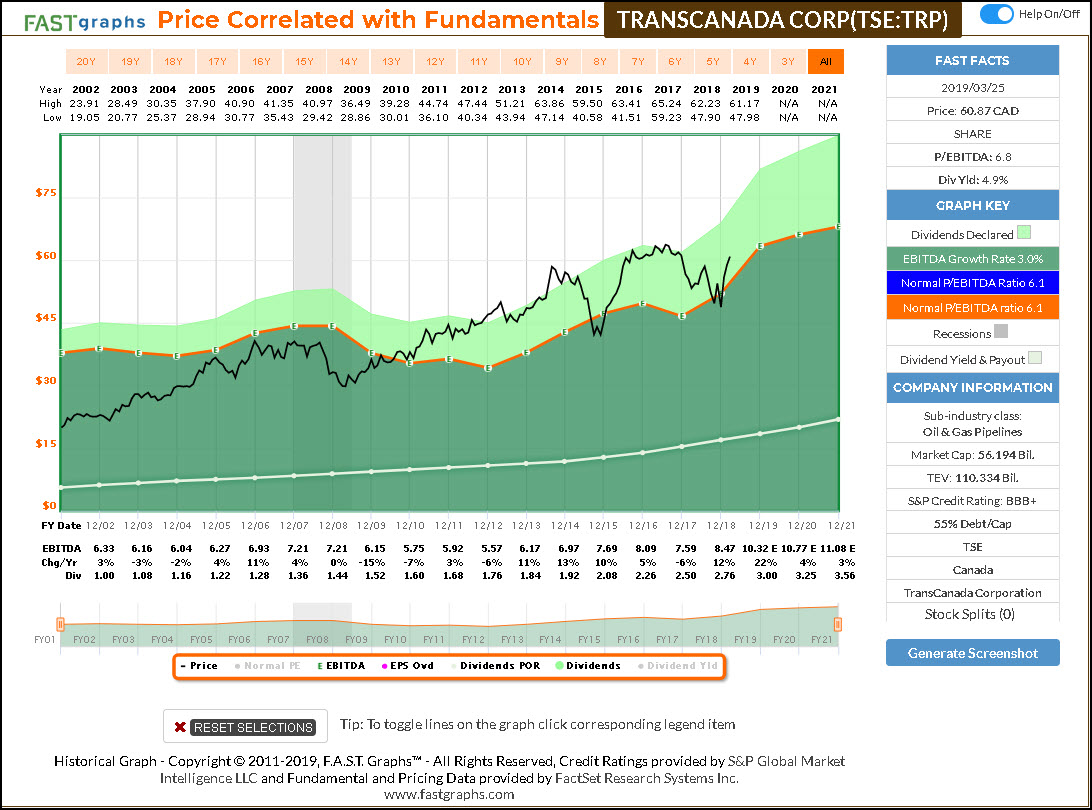

TransCanada Corp (TSE:TRP)

TransCanada Corp. is an energy infrastructure company. It operates through the following business segments: Canadian Natural Gas Pipelines, U.S. Natural Gas Pipelines, Mexico Natural Gas Pipelines, Liquids Pipelines, and Energy. The Canadian Natural Gas Pipelines segment consists of regulated natural gas pipelines.

The U.S. Natural Gas Pipelines segment manages the regulated natural gas pipelines, regulated natural gas storage facilities, midstream, and other assets. The Mexico Natural Gas Pipelines invests on regulated natural gas pipelines in Mexico. The Liquids Pipelines handles investments on crude oil pipeline systems. The Energy segment consists of power generation plants and non-regulated natural gas storage facilities.

The company was founded on May 15, 2003 and is headquartered in Calgary, Canada.

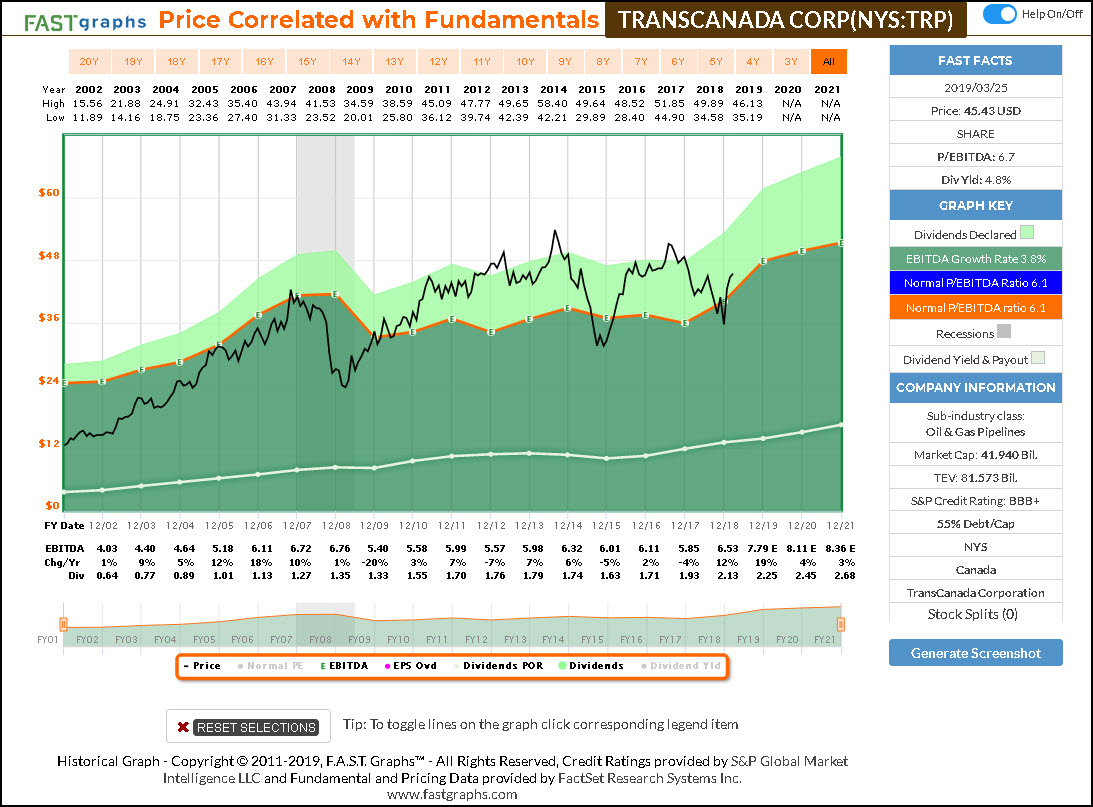

TransCanada Corp (TRP)

TransCanada Corp. is an energy infrastructure company. It operates through the following business segments: Canadian Natural Gas Pipelines, U.S. Natural Gas Pipelines, Mexico Natural Gas Pipelines, Liquids Pipelines, and Energy. The Canadian Natural Gas Pipelines segment consists of regulated natural gas pipelines.

The U.S. Natural Gas Pipelines segment manages the regulated natural gas pipelines, regulated natural gas storage facilities, midstream, and other assets. The Mexico Natural Gas Pipelines invests on regulated natural gas pipelines in Mexico. The Liquids Pipelines handles investments on crude oil pipeline systems. The Energy segment consists of power generation plants and non-regulated natural gas storage facilities.

The company was founded on May 15, 2003 and is headquartered in Calgary, Canada.

F.A.S.T. Graphs Analyze Out Loud Video:

Summary and Conclusions

I hope this article and the associated analyze out loud video provided some deeper insights into the advantages and disadvantages of investing in high-yielding MLPs. There is no question that MLP investments tend to be more complex than investing in a simple common stock. In addition to the tax complications, there are also other characteristics such as dilution that need to be considered. Nevertheless, for those that are willing to take on the complexity and extra tax filing effort, the yields and total returns of investing in an attractively valued MLP can be worth the risk and effort. Nevertheless, my main recommendation is to invest with full awareness and your eyes wide open.

Disclosure: Long ET, EPD at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits