As expected, the Federal Open Market Committee left short-term interest rates unchanged and provided some details on the unwinding of the balance sheet. The revised dot plot showed that a majority of senior Fed officials expect no change in rates in 2019 (but a majority also anticipate one or more hikes in 2020). In contrast, the federal funds futures market ended the week pricing in more than an even chance of at least one rate cut by the end of the year. It’s not unusual for the market’s expectations and the Fed’s expectations to differ. However, the fear that we saw at the start of the year may be back. The baseline scenario is for the economic expansion to continue, but the downside risks are what matter for investors.

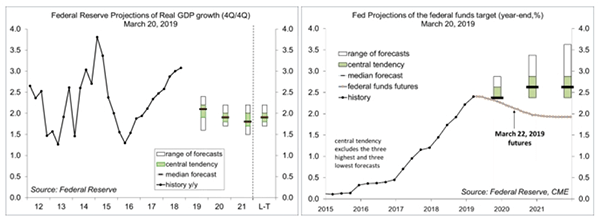

Estimate of 2019 GDP growth have declined. The median forecast of senior Fed officials has tracked the general expectations of economists over time. Last September, Fed officials were expecting 2.5% growth this year (4Q19/4Q18) – expectations fell to 2.3% in December and to 2.1% in March (and that may prove to be a little optimistic). In its policy statement, the FOMC acknowledged softness in consumer spending and business fixed investment. However, subpar first quarter growth is not unusual. The Bureau of Economic Analysis has worked to reduce residual seasonality in the GDP data, but first quarter figures in recent years still tend to be below the growth rates of the other three quarters. While consumer spending numbers were unusually weak in December and only partially rebounded in January, the fundamentals of the household sector (job gains, wage growth, purchasing power, and consumer sentiment) appear sound. At the same time, we know that conditions vary considerably across the income scale. Business fixed investment was supported by the corporate tax cut in 2018, but slower global growth and trade policy uncertainty are negatives in 2019.

Click here to enlarge

In his post-FOMC press conference, Fed Chairman Powell presented a positive outlook but also noted that growth was supported by the tailwinds of fiscal stimulus and strong global growth in 2018. Financial conditions “tightened considerably” in the fourth quarter, but “while conditions have eased since then, they remain less supportive of growth that during most of 2018.” While the federal funds target rate is at the bottom of the range of estimates of the neutral rate (the rate consistent with sustainable growth and stable inflation), most Fed officials believe the natural rate is a bit higher than it is now. However, signs of slower near-term growth, “muted” inflation, and the downside risks from Brexit and trade negotiations allow the Fed to be patient in deciding its next move. Still, by all indications, the Fed is on hold. Officials aren’t talking about cutting rates. In contrast, the federal funds futures market is pricing in a rate cut by the end of this year.

Fed officials expect the unemployment rate to edge a little lower this year, but then stabilize. That’s consistent with economic growth near a sustainable pace. However, the unemployment rate tends to either move higher or lower over time – it rarely trends flat. One often hears that the job market lags the economic cycle. To be clear, the unemployment rate is a lagging economic indicator, nonfarm payrolls are a coincident indicator, and weekly jobless claims are a leading indicator.

Click here to enlarge

The Fed expects inflation to be below the 2% target this year, reflecting lower energy prices. Core inflation is expected to be near the 2% goal. Fed officials don’t believe that we’re about to see a sharp rise in inflation anytime soon. In his press conference, Powell downplayed the relationship between wage inflation and price inflation. The Fed will undergo a major reconsideration of its monetary policy framework this year, and that includes a possible transition to price-level targeting system.

The FOMC has mapped out the end of the balance sheet unwinding. The maximum monthly run-off of Treasury securities (currently $30 billion per month) will be halved in May (to $15 billion per month) and ended in September. The maximum run-off in agency debt and agency mortgagebacked securities (currently $20 billion per month) will continue indefinitely, and beginning in October, the run-off will be offset by increased purchases of Treasuries (keeping the size of the balance sheet steady). According to the Fed, the decision on the balance sheet is not driven by fears of weaker economic growth, the stock market, or pressure from President Trump. The balance sheet is not viewed as active monetary policy. Rather, it’s all about ensuring an adequate level of reserves in the system. While the balance sheet may trend flat for a time, the Fed expects it to begin expanding again, at a pace in line with growth in the overall economy.

Meanwhile, a weaker growth outlook for Europe has put downward pressure on long-term interest rates. The yield curve has inverted (3-month to 5-year), but only slightly so far. That does not suggest a strong likelihood of a recession, but the odds have increased (the current spread between the 10-year Treasury note yield and the federal funds target rate implies about a 30% chance of a recession within the next 12 months). Fears of a recession could become self-fulfilling. The household sector fundamentals argue that consumer spending growth (68% of GDP) should continue to advance. However, if businesses fear the future, they would be more inclined to curtail capital spending plans and hiring intentions. Weekly jobless claims have remained low, but they bear watching more closely in the weeks ahead.

Predicting recessions with any accuracy is difficult. The evolution of the economy depends on the individual decisions of hundreds of thousands of firms and tens of millions of consumers. As we’ve seen over the last few months, fear can easily fade as easily as it builds. Lower long-term interest rate may provide support. Measures of consumer and business attitudes will be important. The most likely scenario is that the economic expansion will continue at a moderate rate this year, albeit somewhat slower than was expected at the start of the year.

Data Recap – As anticipated, the Fed left short-term interest rates unchanged and provided details about the balance sheet run-off. The revised dot plot showed that a majority of Fed officials expect to leave rates unchanged over the course of this year. The economic data reports of the last two weeks were mixed, consistent with slower growth (still positive) in the near term. U.S. investors did not appear to be rattled by ongoing Brexit difficulties, but succumbed to recession fears following weak European manufacturing sentiment data and an inverted yield curve.

President Trump indicated that tariffs may continue even if a trade agreement with China is reached.

As expected, the Federal Open Market Committee left the federal funds target range at 2.25-2.5%. In the policy statement, the FOMC acknowledged slower growth in consumer spending and business fixed investment, and repeated that it would be patient in deciding the next move. The FOMC also announced plans to finish the unwinding of the balance sheet, slowing the pace of run-offs of Treasuries in May and ending that in September. The maximum run-off of mortgage securities will continue, replaced by additional Treasury purchases in October.

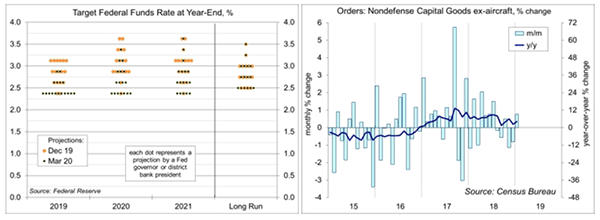

In the Fed’s Summary of Economic Projections (SEP), officials lowered their outlook for 2019 GDP growth (to 2.1%, from 2.3%). In the revised dot plot, 11 of the 17 senior Fed officials saw no rate increases this year (in December, all but two expected at least one increase). The dot plot also showed that 10 officials anticipate at least one rate increases in 2020.

In his post-FOMC press conference, Fed Chairman Powell described inflation as “muted” and noted potential downside risks to the growth outlook from “unresolved policy issues such as Brexit and the ongoing trade negotiations.”

Click here to enlarge

Factory Orders edged up 0.1% in the initial estimate for January (+4.2% y/y), down 0.2% excluding transportation (+1.8% y/y). Orders for nondefense capital goods excluding aircraft rose 0.8%, following a 0.8% decline in December and a 1.1% drop in November.

Jobless Claims have continued to trend at a low level. The four-week average was 225,000, the same as a year ago.

The Conference Board’s Index of Leading Economic Indicators rose 0.2% in the initial estimate for February, reflecting rebounds in the stock market and consumer expectations. A shorter factory workweek subtracted from the LEI, but that was likely due to the weather. The LEI has trended flat since September, consistent with slower growth in the near term.

Homebuilder Sentiment held steady at 62 in March, consistent with a stabilizing housing market and optimism for the spring selling season.

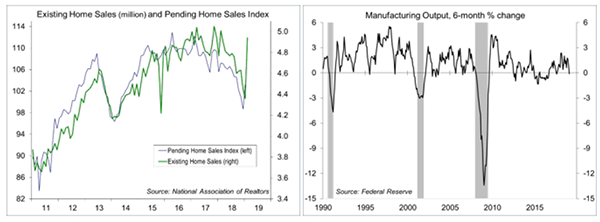

Existing Home Sales jumped 11.8% in February, to a 5.51 million seasonally adjusted annual rate (-1.8% y/y), reflecting lower mortgage rates and an increased supply of homes for sale.

Click here to enlarge

Industrial Production rose 0.1% in February (+3.5% y/y), boosted by a 3.7% increase in the output of utilities (colder weather). Manufacturing output fell 0.4% (+1.2% y/y).

Retail Sales rose 0.2% in the initial estimate for January (+2.3% y/y), following a 1.6% plunge in December (revised from -1.2%). Ex-autos, building materials, and gasoline, sales rose 1.0% (+3.1% y/y), following a 1.8% decline in December (revised from -1.6%).

The University of Michigan’s Consumer Sentiment Index rose to 97.8 in the mid-March reading (vs. 93.8 in February and 91.2 in January). Gains were concentrated in households in the bottom two-thirds of income. Sentiment for the top third, which accounts for more than half of consumer spending, fell, but remained high.

The Consumer Price Index rose 0.2% in February (+1.5% y/y), up 0.1% ex-food & energy (+2.1% y/y).

Real Hourly Earnings rose 0.3% (+1.9% y/y), up 0.2% for production workers (+2.2% y/y).

The Bank of England left short-term interest rates unchanged and continued to make no prediction on the direction of monetary policy post-Brexit.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

More Alternative Investments Topics >