IN THIS ISSUE:

1. The Global Economy is the Weakest Since 2008-09

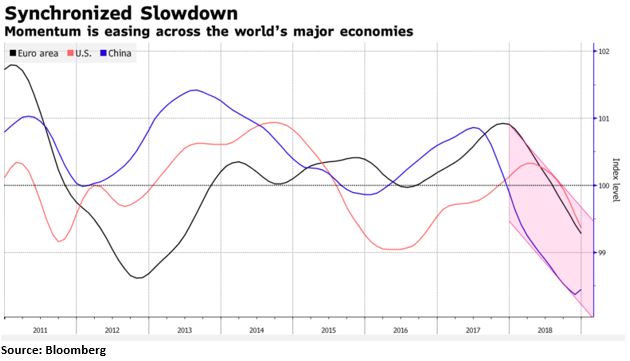

2. Momentum Easing Across World’s Major Economies

3. IMF Warns: “No Deal” Brexit Will Hurt Global Growth

4. Economists: Worst May be Over For Global Economy

Overview

Global economic growth contracted sharply in the second half of last year, from above a 4% pace in the first half to 2-2.5%. While still positive, momentum eased across all of the world’s major economies, including the US. The question is, will this global slowdown continue?

Fortunately, a growing number of forecasters believe the global economy is in the process of bottoming and predict it will strengthen considerably in the second half of this year. Let’s hope they are correct.

I also discuss “Brexit” involving the UK and the EU, which was nearing its March 29 deadline until the British Parliament extended it last Thursday. I will point out what you should be watching for in the negotiations just ahead, and I also suggest that Brexit may not be nearly as big a deal as the media would have us believe.

The Global Economy is the Weakest Since 2008-09

While the US economy grew at nearly 3% in 2018, its best showing in years, global economic growth lost considerable momentum in the second half of last year. While the International Monetary Fund (IMF) has yet to release its final estimate of global GDP for all of 2018, most forecasters believe the global economy slowed significantly in the second half of last year.

According to the IMF, the global economy was growing at a healthy rate of just over 4% in the first half of 2018. However, recent estimates from Bloomberg and some multinational banks suggest that global growth contracted significantly in the second half of last year to only 2-2.5%. If so, that would mean growth slowed to the lowest level since 2008-09 during the Great Recession.

On January 21, the IMF revised its global economic growth forecast for 2019 down to 3.5%, citing concerns about rising trade tariffs between the US and China and weakening in the European economy in the last half of 2018. It will not surprise me if the IMF cuts its global growth forecast more just ahead.

Here’s why: If global growth was in fact 4.1% in the first half of 2018 as the IMF believes, and if it did slow to only 2-2.5% in the second half of last year, that’s still average growth of over 3% for the year. But if growth did slow to near 2-2.5% in the second half of last year, that will mean there will have to be a substantial rebound to come anywhere near the IMF’s global growth forecast of 3.5% for 2019.

For the moment, that doesn’t look very likely. China’s car sales dropped significantly in January, and data last week showed US retail sales posted their worst drop in nine years in December. In Europe, where the slowdown has been particularly marked, sentiment indicators continue to weaken, and the latest OECD (Organization for Economic Cooperation & Development) leading economic indicator has also declined recently.

I could go on with specific economic reports that suggest the slowdown in the global economy is continuing this year, but the following chart illustrates what’s happening in the trend globally. It shows that economic growth is trending lower; it does not mean that growth is negative.

Take the US for example, which had nearly 3% growth last year, the best in a long time. Yet US GDP peaked in the 2Q at 4.2% and slipped to 3.4% in the 3Q and 2.6% in the 4Q. So while it was a great year overall, momentum was slipping in the second half of the year. The same was true in Europe and China.

According to the IMF, advanced economies have been on a declining path in terms of growth and this is taking place more rapidly than previously thought. These countries are forecast to grow only 2% this year and 1.7% in 2020. At the same time, there's also been a growth slowdown in emerging economies. The IMF projects a 4.5% growth rate in 2019 in emerging countries, down from 4.6% in 2018. But this could change as I’ll discuss below.

IMF Warns: “No Deal” Brexit Will Hurt Global Growth

In its latest report on January 21, the IMF warned that several factors, if they occur, could slow global growth even more this year: "A range of triggers beyond escalating trade tensions could spark a further deterioration in risk sentiment with adverse growth implications, especially given high levels of public and private debt."

Chief among the IMF’s concerns is the growing likelihood of a “no deal” Brexit for the United Kingdom. The problem is there is no deal in place to manage the UK’s relationship with the 27 countries in the European Union after Brexit, which was set to happen on March 29th.

Britain’s Prime Minister Theresa May has put forth several proposals to deal with trade between the UK and the EU countries beyond Brexit, but each proposed deal has been roundly shot down by Parliament. Britain’s Parliament is deeply divided over what Brexit should look like, or whether it should happen at all.

Perhaps the biggest sticking point of Brexit is the border between Northern Ireland, which is part of the UK, and the Republic of Ireland, which is part of the EU. There are two paths for moving forward:

Brexit with a deal: Parliament approves a deal that the EU can live with, and the departure takes place in a reasonably orderly way.

Brexit with no deal: If Parliament doesn’t make a deal with the EU, then the UK was still set to leave on March 29th, but in a chaotic fashion. There were projections of shortages of pharmaceuticals and other essential goods in the UK if no deal was reached. Now that the deadline has been extended, it is impossible to know what will happen just ahead.

Of course, there is a third option: There is a legal mechanism for the UK to call the whole thing off. Politically, this would almost certainly require another referendum or an upheaval in Parliament, but it’s not out of the question.

I don’t pretend to know what will happen. The EU is pressing hard for another Brexit vote and might be willing to give Britain more time, since it believes a new Brexit vote would fail (UK stays in the EU). Prime Minister May doesn’t want a second vote for the same reasons – she wants out.

We are told that if the UK departs the EU with no deal, the so-called “hard Brexit,” it will cause chaos in the global markets. No doubt it could cause some short-term volatility. But keep in mind that the UK’s economy is only the size of California. Thus, it should not be a really big deal no matter what the UK decides to do.

Economists: Worst May be Over For Global Economy

While the global economy slowed significantly in the second half of last year, as discussed above, more economists now say the global economy should bottom soon and that the worst may already be over. Bloomberg Economics, Deutsche Bank and Morgan Stanley are among those who believe the global slide will bottom out this quarter or next and will rebound in the second half of this year.

I’m not so sure, but I’ll give you their thinking. Bloomberg’s Chief Economist, Tom Orlik said last week: “Put the Federal Reserve pause, trade truce, and China stimulus together and we’re looking for a trough in the first quarter and very moderate pick up ahead.”

Obviously, those are some optimistic assumptions. Just because the Fed said it can be “patient,” that does not mean there won’t be an interest rate hike this year. It remains to be seen if we’ll get a trade deal done with China. Likewise, it remains to be seen if China’s economy will rebound this year. Ditto for the EU economy.

Orlik is correct that the Fed and many central banks have either held back on raising interest rates or introduced fresh stimulus in an effort to reverse the global slowdown. European Central Bank President Mario Draghi has ruled out rate hikes this year and unveiled a new batch of cheap loans for banks to stimulate the EU economy.

Elsewhere, authorities in Australia, Canada and the UK are among those to have adopted a wait-and-see approach on monetary policy. China, at its National People’s Congress this month, signaled a willingness to ease monetary and fiscal policies to support expansion.

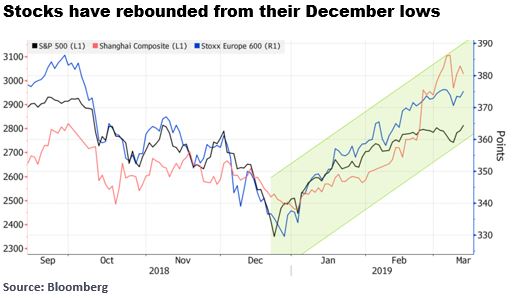

Investors have clearly become more optimistic in the wake of the December stock market correction, and this has pushed equity prices significantly higher this year. The S&P 500 has gained almost 20% from its December low, while the Shanghai Composite is up about 22%.

IHS Markit, a London-based global information provider, reported its global growth index rose in February for the first time in months. Citigroup’s Surprise Index for the Euro area has rebounded to the best reading in almost five months. In China, its Purchasing Managers Index, which measures new manufacturing orders, also reversed higher last month.

While I may not be as confident about the global economy rebounding as these and other forecasters are, signs of a turnaround before long are slowly increasing. I think part of this new optimism is the fact that most forecasters have given up on the view that the US is going into a recession this year. You remember that one, right? Now most forecasters suggest we’re safe from a recession until next year. Hum, where have we heard that before?

Best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by Halbert Wealth Management, Inc. Gary D. Halbert is the president and CEO of Halbert Wealth Management, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, Halbert Wealth Management, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management

© Halbert Wealth Management

Read more commentaries by Halbert Wealth Management