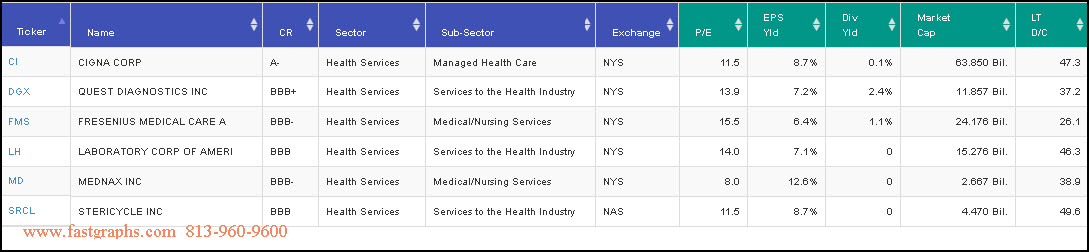

The Health Services Sector is one of the smallest sectors as presented by FactSet as it only contains 137 companies out of more than 19,000 in the US and Canadian universe. Furthermore, since I was also screening for quality based on investment grade S&P Credit Ratings of BBB- or better, I was additionally surprised that only 11 companies met that benchmark. Additionally, since I was also screening for valuation, I only found 6 companies with P/E ratios below 17. There were a few well-known names (Anthem Inc., Humana Inc. and United Health Group Inc.) that missed the cut because their P/E ratios were moderately above 17, that otherwise could have also been featured.

Nevertheless, despite what was stated above, one characteristic that is shared by each of the research candidates on this list, is an above-average rate of earnings growth. On the other hand, only 2 out of the 6 pay a dividend which suggests that this sector is most appropriate for investors interested in capital appreciation or growth. This growth orientation is also consistent with the fact that these best-of-breed companies in this sector have outperformed the S&P 500 over the long run despite the lack of dividend income.

Another characteristic that I found common, but not universal, with companies in the Health Services Sector was a penchant for the market providing premium valuations to their shares. However, ironically, these premium valuations were awarded to the non-dividend paying research candidates more so than the dividend paying ones. This seemed somewhat counter-intuitive to me since I would’ve expected dividend paying stocks in this sector to be more popular. On the other hand, the non-dividend paying research candidates have tended to experience significantly more severe price drops over recent market history. To me this suggests that their high valuations were more vulnerable when sentiment turned negative.

Regarding the two research candidates that do pay a dividend, I found it interesting that they both outperformed the S&P 500 on growth and on total dividend income. These results are clearly a function of above-average earnings growth that also translated into above-average dividend growth.

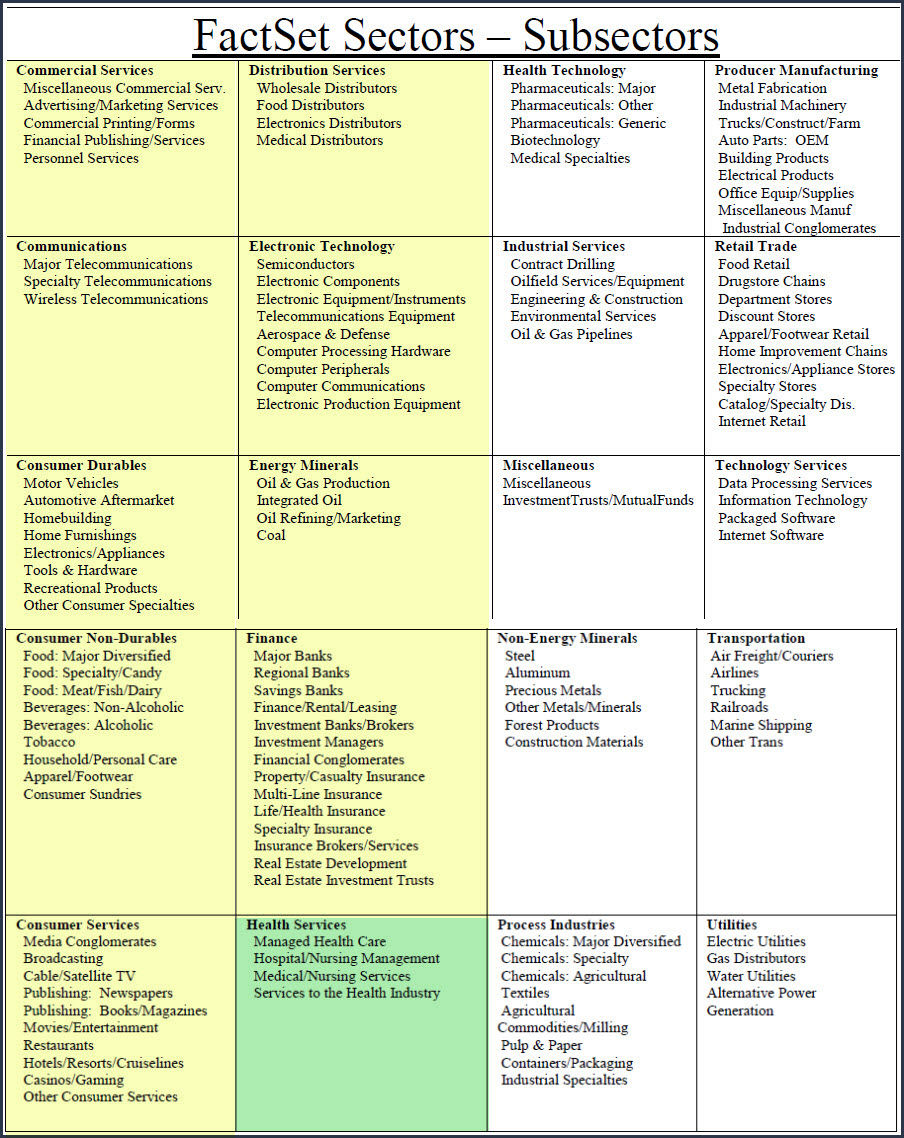

A Sector By Sector Review

This is part 10 of a series where I have conducted a simple screening looking for value over the overall market based on industry classifications and subindustry classifications reported by FactSet Research Systems, Inc.In part 1 found here I covered the Consumer Services Sector. In part 2 found here I covered the Communication Sector. In part 3 found here I covered the Consumer Durables Sector and its many diverse subsectors. In part 4 found here I covered Consumer Nondurables. In part 5 found here I covered companies in the Consumer Services Sector. In part 6 found here I covered the Distribution Services Sector. In part 7 found here I covered the Electronic Technology Sector. In part 8 found here I covered the Energy Minerals Sector. In part 9 found here I covered the Finance Sector.

In this part 10 I will be covering the Health Services Sector.

In each article in this series, I will be providing a listing of screened research candidates from each of the following industry sectors, the sector I’m covering in this article is marked in green:

A Simple Valuation and Quality Screening Process

With this series of articles, I will be presenting a screening of companies that have become attractively valued primarily as a result of the bearish market activities experienced in 2018 from each of the above sectors. I will be applying a rather simple valuation and quality-oriented screen across each of the sectors. First, I have screened for investment-grade S&P credit ratings of BBB- or above. Next, I have screened for low valuations based on P/E ratios between 2 and 17. Finally, I have screened for long-term debt to capital no greater than 70%.

By keeping my screen simple, and at the same time rather broad, I will be able to identify attractively valued research candidates that I might have overlooked through a more rigorous screening process. In other words, I’m looking for fresh ideas that I might have previously been overlooking. Furthermore, I want to be clear that I do not consider every candidate that I have discovered as suitable for every investor. However, I do consider them all to be attractively valued. Additionally, I also believe that every investor will be able to find companies to research that meet their own goals, objectives and risk tolerances as this series unfolds.

Sector 10: Health Services

Managed Health Care

Hospital/Nursing Management

Medical/Nursing Services

Services to the Health Industry

Portfolio Review: Health Services Sector: 6 Research Candidates

FAST Graphs Screenshots of the 6 Research Candidates

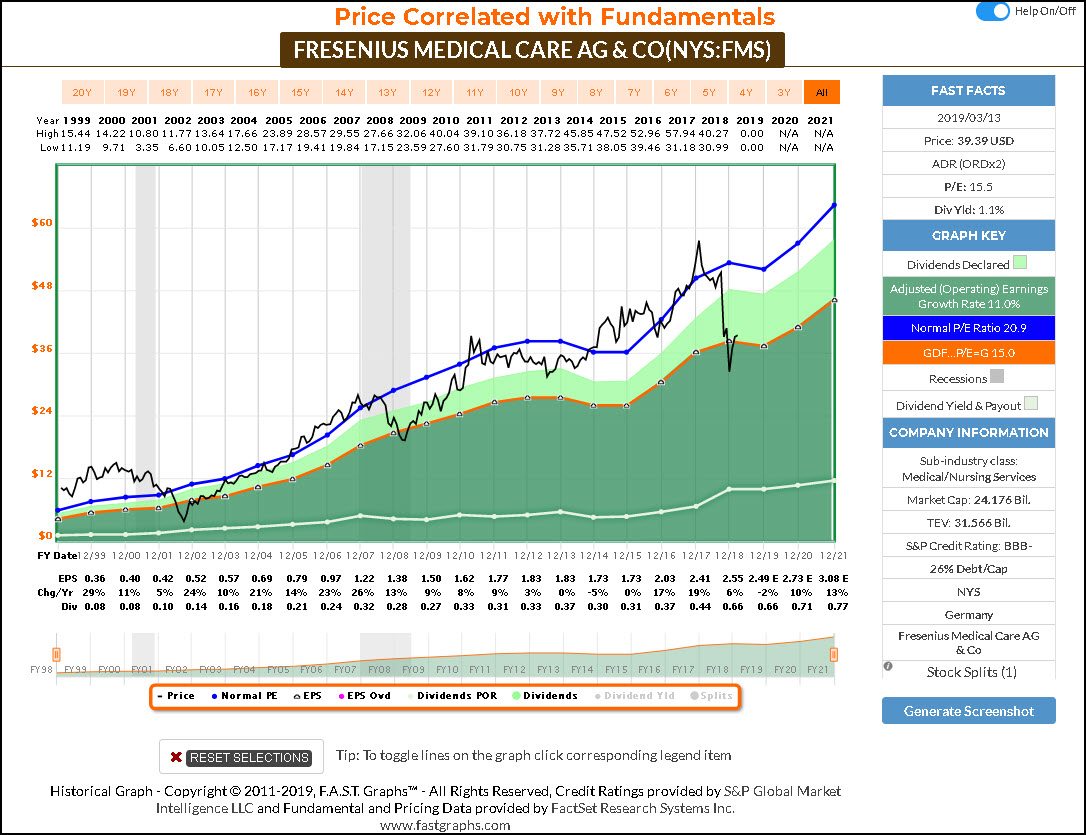

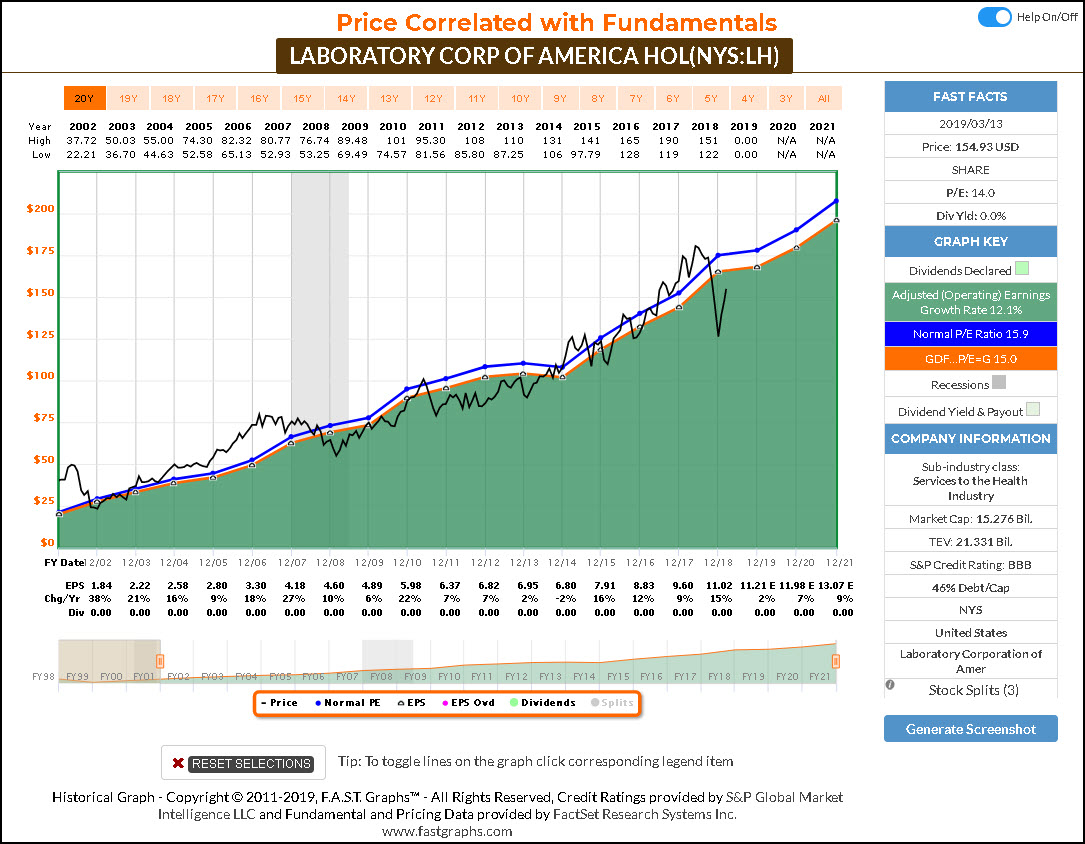

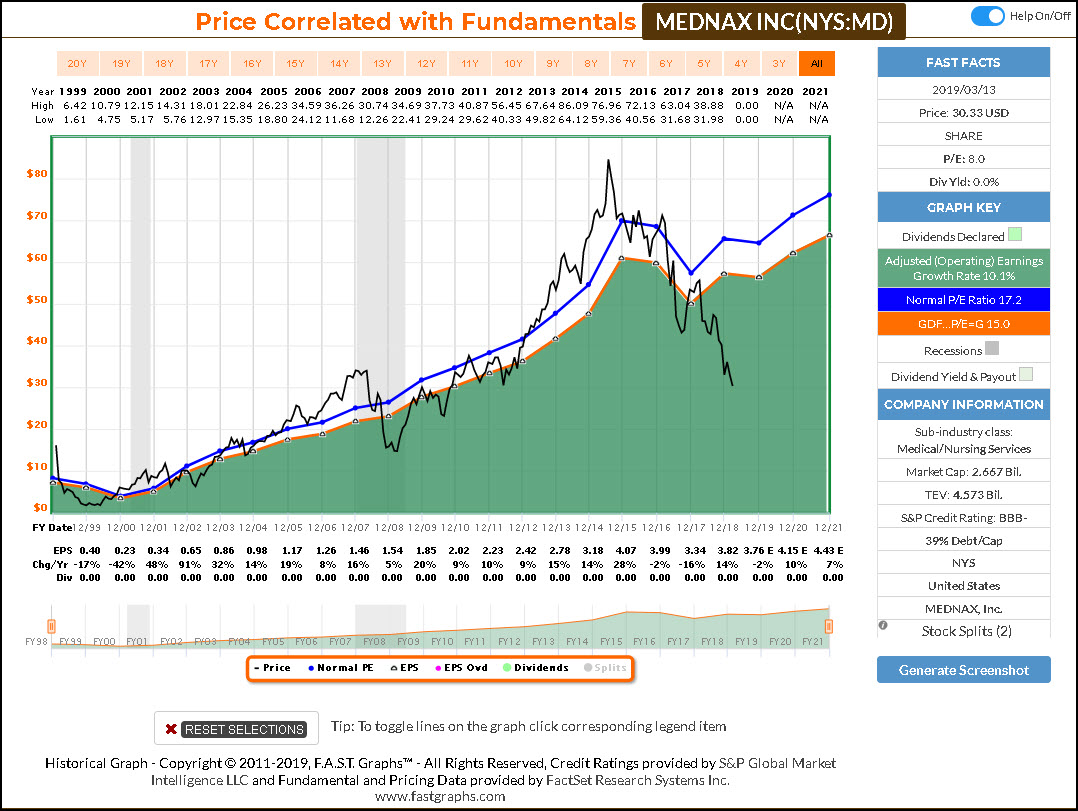

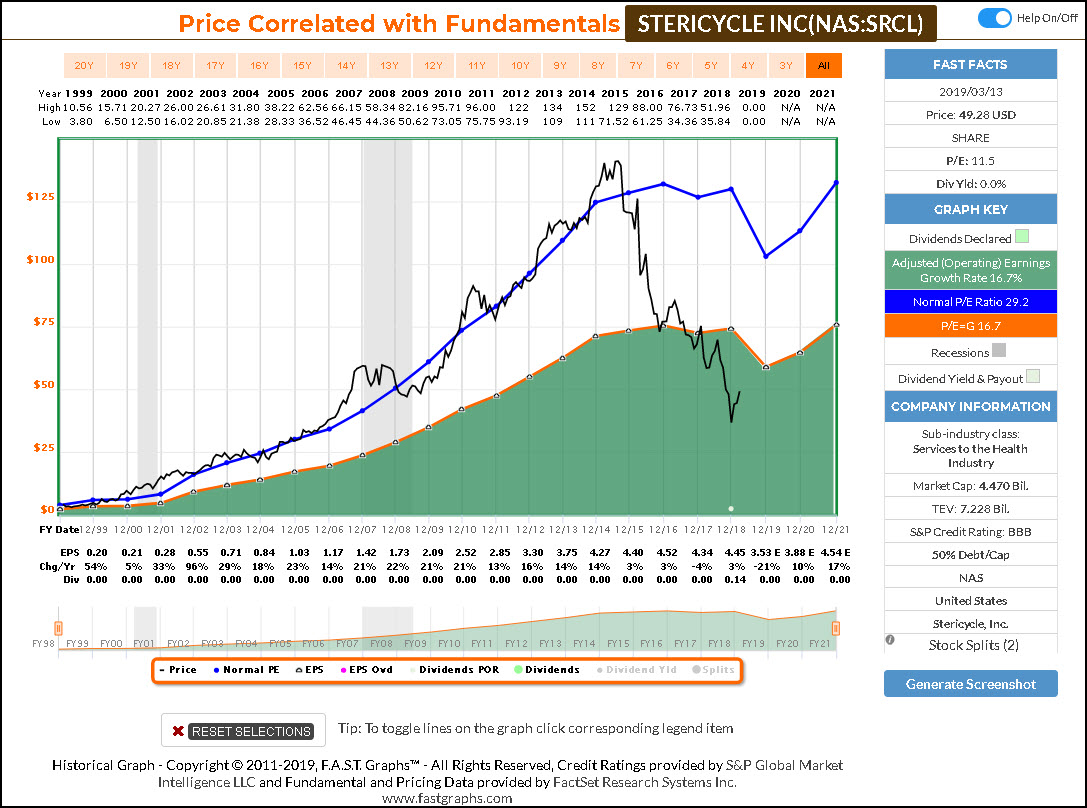

The following screenshots provide a quick look at each of the 6 candidates screened out of over 19,000 possibilities. However, there are only 137 companies categorized as Health Services, and these 6 were the only ones I was comfortable presenting in this article. The company descriptions are provided courtesy of the Wall Street Journal. In the FAST Graphs analyze out loud video that follows the screenshots, I will provide additional details and thoughts on the possible attractiveness as well as the potential negatives of each of these research candidates.

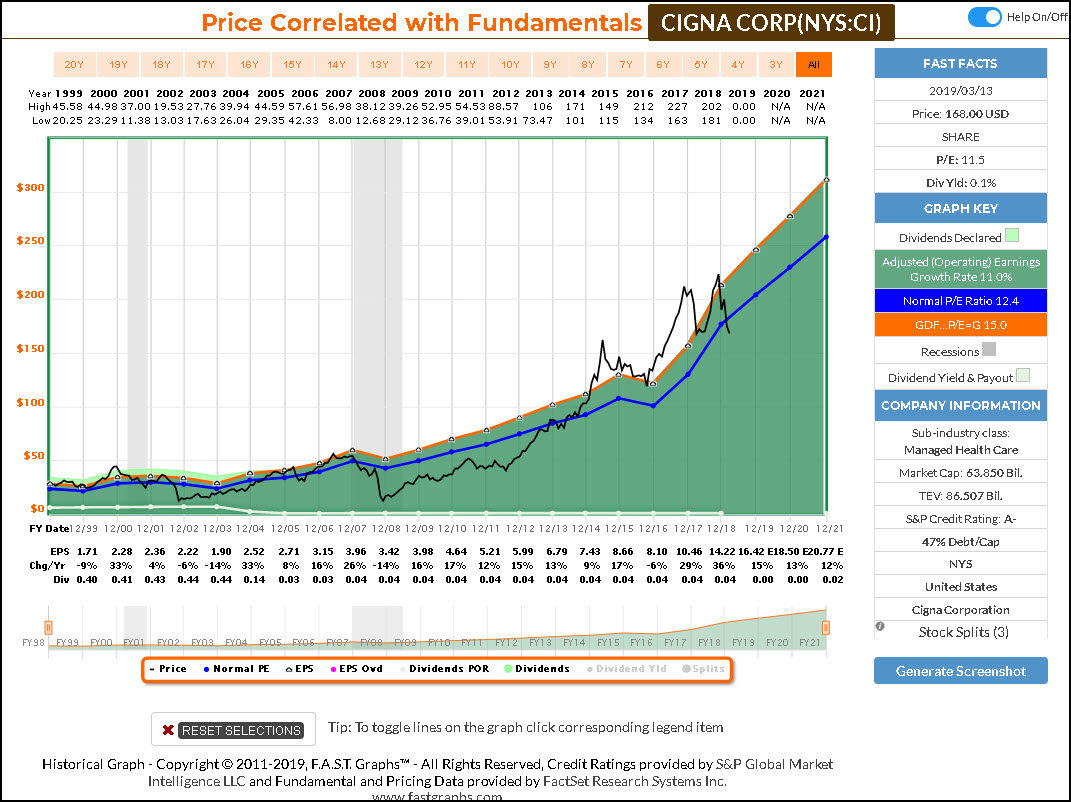

Cigna Corp (CI)

Cigna Corp. is a global health service company, which is dedicated to improving the health, well-being and peace of mind. The company delivers choice, predictability, affordability and quality care through integrated capabilities and connected, personalized solutions that advance whole person health. Its products and services include an integrated suite of health services, such as medical, dental, behavioral health, pharmacy, vision, supplemental benefits, and other related products including group life, accident and disability insurance.

The company was founded in 1792 and is headquartered in Bloomfield, CT.

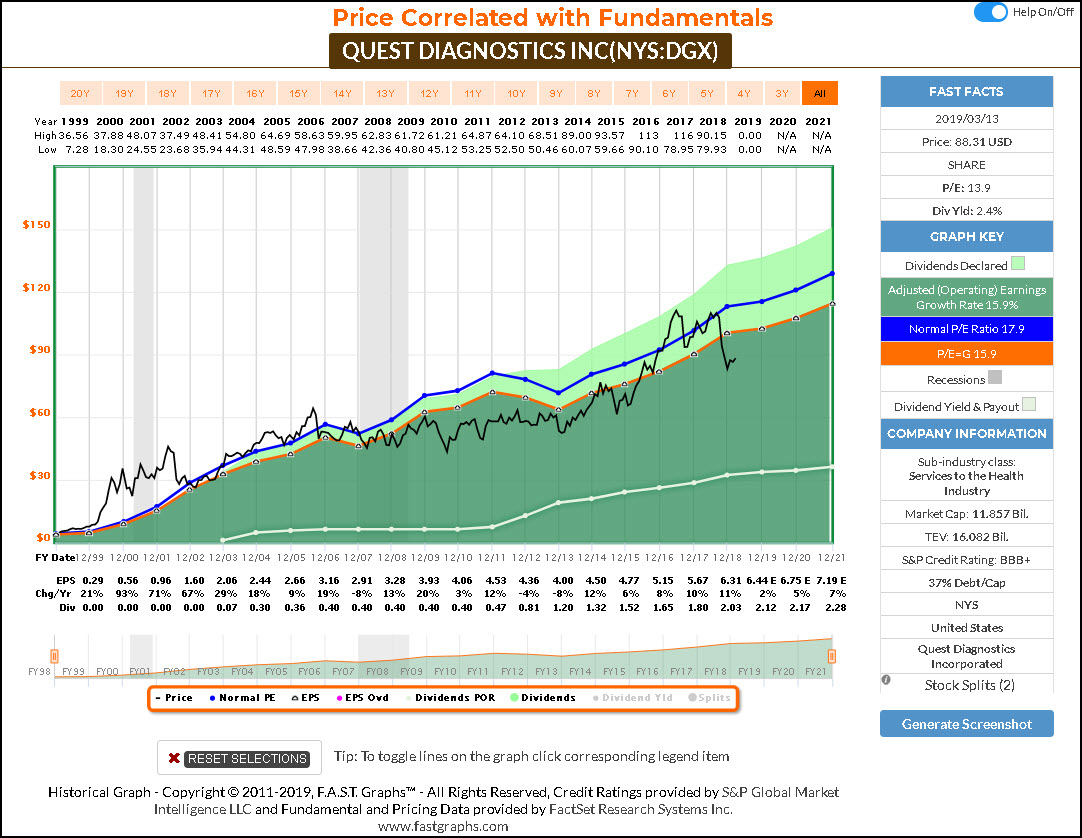

Quest Diagnostics Inc (DGX)

Quest Diagnostics, Inc. engages in the provision of diagnostic testing, information and services. It operates through the Diagnostic Information Services (DIS) and All Other segments. The DIS segment offers diagnostic information services to patients, clinicians, hospitals, health plans, and employers. The All Other segment consists of risk assessment services, healthcare information technology, diagnostic products, and clinical trials testing businesses.

The company was founded in 1967 and is headquartered in Secaucus, NJ.

Fresenius Medical Care (FMS)

Fresenius Medical Care AG & Co. KGaA engages in the provision of products and services for patients with chronic kidney failure. It also develops and manufacture a variety of health care products, which includes dialysis and non-dialysis products.

The company was founded on August 5, 1996 and is headquartered in Bad Homburg, Germany.

Laboratory Corp of America (LH)

Laboratory Corp. of America Holdings is a clinical laboratory company, which engages in the provision of clinical laboratory and end-to-end drug development services. It operates through the LabCorp Diagnostics and Covance Drug Development segments. The LabCorp Diagnostics segment includes core testing as well as genomic and esoteric testing. The Covance Drug Development segment involves in providing drug development solutions, to companies in the pharmaceutical and biotechnology industries.

The company was founded in 1971 and is headquartered in Burlington, NC.

Mednax Inc (MD)

MEDNAX, Inc. provides physician services including newborn, anesthesia, maternal-fetal, tele radiology, pediatric cardiology and other pediatric subspecialty care. The company’s solution include anesthesiology & pain management, prenatal, neonatal, pediatric, radiology, tele radiology, revenue cycle management and perioperative improvement consulting.

MEDNAX was founded by Roger J. Medel in 1979 and is headquartered in Sunrise, FL.

Stericycle Inc (SRCL)

Stericycle, Inc. engages in the provision of waste management services. It operates through the following segments: Domestic and Canada Regulated Waste and Compliance Services (“RCS”); International RCS; and Domestic CRS. The Domestic and Canada RCS segment manages medical and pharmaceutical waste disposal, hazardous wastes, and unused and expired inventory.

The International RCS segment includes patient transport services. The Domestic Communication and Related Services segment consists of inbound/outbound communication, automated patient reminders, online scheduling, notifications, product retrievals, product returns, and quality audits.

The company was founded in March 1989 and is headquartered in Lake Forest, IL.

F.A.S.T. Graphs Analyze Out Loud Video:

Summary and Conclusions

Although the Health Services Sector is one of the smaller sectors in the FactSet universe, it does offer some very interesting research candidates. The 6 research candidates presented in this article all appear to be attractively valued relative to their future growth expectations. Consequently, they all theoretically offer above-average future rates of return.

Furthermore, this sector might appeal more to the total return investor than it would the dividend growth investor. Nevertheless, the few candidates that do pay a dividend also appear attractive for their future dividend growth potential. Although their current yields are not large, their growth yields (potential yield on cost) might be attractive to those dividend growth investors interested in total return.

Disclosure: Long CI at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.