In his post-FOMC press conference on December 19, Fed Chairman Powell said that low inflation would allow the Fed to be more patient in adjusting rates. The stock market fell. He said essential the same thing in his January 30 press conference. The market rallied. Okay, that’s an over-simplification. The Fed’s tone has shifted, but not because of the stock market or pressure from the White House. The baseline economic outlook hasn’t changed much since mid-December. However, cross-currents and downside risks have increased. The employment report would suggest that the Fed might have more work to do in achieving its soft landing, but come on – it’s January. The bigger test for the job market will come in the spring. Over time, it will become apparent whether this current phase is merely a pause or the end of the Fed’s tightening cycle.

As expected, the Federal Open Market Committee removed the phrase suggesting “some further gradual increases” in the federal funds rate would likely be required. Expectations of rate increases had already been dampened in December, with senior Fed officials divided on whether there would be zero, one, or two rate hikes in 2018. We won’t get a new dot plot until March 20, but it’s likely that the dots will drift a little lower.

In his January 30 press conference, Powell noted that “the economy is in a good place.” The job picture “continues to be strong,” and “inflation remains near our 2% goal.” However, “despite the positive outlook, we have seen some cross-currents and conflicting signals about the outlook.” He cited slower growth abroad, “particularly China and Europe.” Financial conditions “tightened considerably in late 2018, and remain less supportive of growth than they were earlier in 2018.” In additions, some surveys of business and consumer sentiment moved lower, “giving reason for caution.” The cumulative effect of these developments “warrant a patient, wait-and-see approach regarding future policy changes.” The change in attitude “was not driven by a major shift in the baseline outlook for the economy,”Powell noted, “but the cross-currents suggest the risk of a less favorable outlook.” In addition, “the case for raising rates has weakened somewhat.”

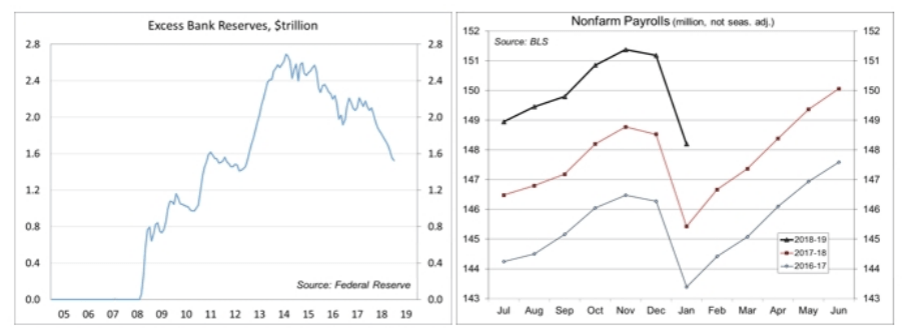

The Fed also released guidance on the balance sheet. The Fed began to unwind its balance sheet in October 2017, allowing a certain portion of maturing Treasuries and mortgage-backed securities in its portfolio to roll off. The Fed increased the pace of the roll off over time. From the beginning, the Fed was a bit unsure of how the financial markets would react and where the process would end. Now it appears that the unwinding will end sooner, leaving the size of the balance sheet at a higher level than was expected several months ago, but Powell declined to say exactly when (that decision is coming). The FOMC also stressed the monetary policy will focus on maintaining ample reserves in the banking system. Reserves have been falling, but these are excess reserves – nothing to panic about. Moreover, it’s unclear why the balance sheet unwind would have such an asymmetrical impact on the financial markets compared to the buildup. That doesn’t make much sense, other than if the unwind is viewed with fear.

Click here to enlarge

Meanwhile, growth in nonfarm payrolls remained strong in January. January figures are always a bit suspect. We lost nearly three million jobs before seasonal adjustment, somewhat less than a year ago, but that could reflect more favorable weather. Unadjusted payrolls trend sharply higher from February to June. The job market will remain a major factor in the Fed’s decision-making process, and investors should watch the figures closely over the next few months.

The partial government shutdown had no discernable impact on payrolls, hours, and wages in January, according to the Bureau of Labor Statistics, but it did lift the unemployment rate slightly (to 4.0%, from 3.9% in December).

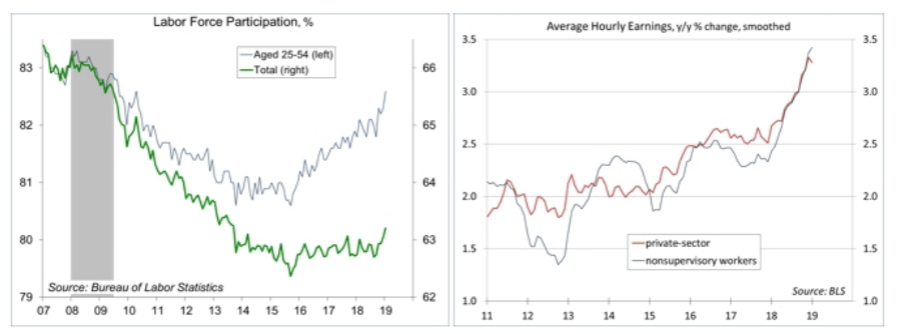

The recent increase in the unemployment rate (it was 3.6% in November) is a puzzle. In fact, the strong pace of growth in nonfarm payrolls would suggest that the unemployment rate should be falling more significantly. Labor force participation has improved (a flat participation rate would be taken as a sign of strength given the aging of the population). So that’s part of the story, and higher wages ought to bring a lot of those on the sidelines (recent retirees, stay-at-home spouses) back into the workforce. Higher wages should lead to a reallocation of labor, with underemployed workers moving up, creating space for younger workers to acquire skills.

Click here to enlarge

The Fed has always viewed the labor market as the widest channel for inflation pressure. Average hourly earnings rose modestly in January (+0.1%), a surprise given the expectation of more robust cost-of-living increases and increases in the minimum wage in some states. However, the wage figures are often revised the next month and the trend is still higher (+3.2% y/y).

In his press conference, Powell noted that “we think that these cross-currents, these risks, are going to be with us for a while.” That doesn’t mean that the Fed won’t tighten further, or even cut rates, if needed. When asked directly if he would characterize the current stance as “a pause” or “an end to the tightening cycle,” Powell once again emphasized patience, adding “I think we’re going to know in hindsight.” The length of the patient period is going to depend entirely on incoming data and its implications for the outlook.”

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James