Winter Quarterly Commentary

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsLife is divided into three terms – that which was, which is, and which will be. Let us learn from the past to profit by the present, and from the present, to live better in the future.”

William Wordsworth (1770-1850)

English poet laureate

Initiator of the Romantic Age

We would like to ring in the new year and provide our predictions for the U.S. economy in 2019:

- 3.7% unemployment – the best in 50 years

- Three percent real GDP growth – the best in a decade

- Double-digit corporate earnings growth – more than twice the long-term rate

- Consumers in good financial shape, with their strong spending driving two-thirds of GDP

- More fiscal stimulus

- Major stock market indices down six percent

Surely, given our sunny economic outlook, the stock market return prediction is a misprint? It’s not. In truth, these aren’t predictions for 2019 at all, they are the actual numbers for the upside-down year of 2018.

Last year’s good economy but bad stock market is not actually as surprising as one might initially think. We displayed the chart at right last quarter, but it is so striking we include it again. Markets rarely look at current conditions, but rather move based on what’s coming next. Today’s ultra-low unemployment rate, for example, points to a monthly market return near zero (left most bar with unemployment rate <4%) whereas stocks have annualized at a higher than 30% rate under double-digit unemployment rates, based upon data since 19551.

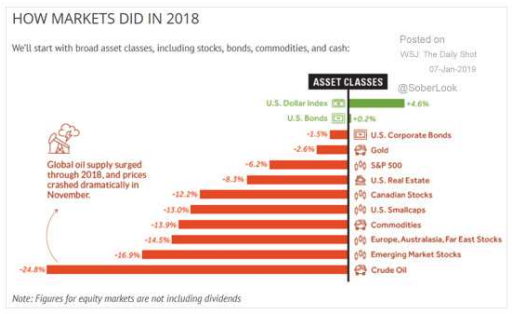

The breadth of declines in investment values around the world in 2018 was unprecedented. Both stocks and bonds declined, which is highly unusual. Additionally, commodities and gold were down along with nearly every single foreign equity market. 93% of all global asset classes showed negative returns last year according to Deutsche Bank, a first since 1901. Diversification did not save the day. In retrospect, the best option was to own cash… the best asset allocation didn’t involve making the most, but losing the least. Such a year is fortunately very rare.

The losses shown in the above graph are annual numbers and understate just how devastating the fourth quarter was in particular. The S&P 500 Index plunged 20% from peak to trough during the period. The quarter concluded with the worst December for the Dow and S&P 500 since the Great Depression year 1931. It was the worst December ever for NASDAQ. The good news is that historically, the market has performed well in the year following its worst quarters, and that’s exactly what’s been happening so far in 2019.

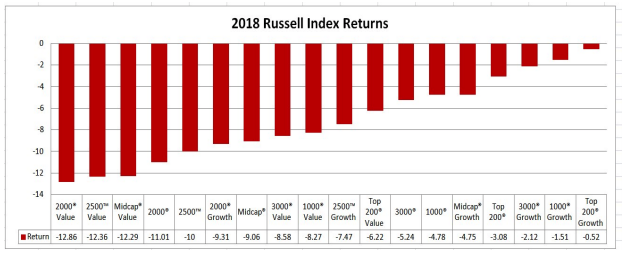

Looking at the S&P 500 Index, which was down “only” six percent in 2018, also understates the damage done in large swaths of the U.S. equity market. The following chart segments returns by company size and investment style. Large-company and growth stocks (the six red bars to the most right on the chart) were down less than smaller-company and value stocks (the six red bars to the most left). The latter groups fell deep into “bear market” territory, before bouncing back some after Christmas. Over the past 100 or so years of modern stock market history, smaller company and value stocks have outperformed their peers and for this reason we tilt towards them in the portfolio. Over the long-term we expect this to be beneficial, but in the present year of 2018 it was no small hinderance.

Also unfortunate was our ownership of PG&E (ticker PCG), which we purchased following the 2017 wildfires. The 2017 wildfires were tragic and horrific: the twelve major fires resulted in 44 fatalities, 245,000 acres burned, and 8,900 structures destroyed. While many of these fires were started by PG&E equipment2, it is not yet clear that PG&E was negligent or acted imprudently. We invested, believing that legislation would be passed to help the utility deal with fire-related costs, as it is in the interest of many important stakeholders to have a healthy utility. Legislation ultimately was passed, and our PG&E position was a winner. However, this legislation was designed to address the 2017 fires and those from 2019 forward. Strangely, any fires that might occur in 2018 were not to receive the same treatment. Unfortunately, another tragic fire did occur in 2018, and it again appears that PG&E’s equipment started the fire and they will have to pay (even if they rigorously followed all relevant safety procedures). Despite the current loss in value, we believe the probability of PG&E shares trading substantially higher in a few years from here outweighs the downside3. Past is not always prelude, but our ownership of this utility during and following its 2001 bankruptcy generated substantial gains. The day before PG&E filed for bankruptcy on April 7, 2001, the stock was trading for seven dollars; four years later it was trading for thirty-seven dollars. Thus, a substantial recovery from here would not be completely unprecedented.

Back to the broadly bad 2018… why did the stock market so swiftly drop 20% in the fourth quarter? It is tough to know for sure why the market does what it does, but it looks like it declined because the bond market was saying, “we’re going to have a recession”. Why did the bond market scream fire in a crowded theater? We will seek to answer that… but you may want to get your coffee ready as we prepare to head inside the bond market.

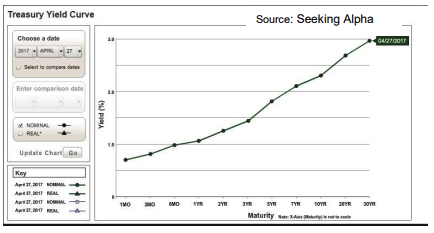

To understand the bond market’s verdict, we first introduce a “normal” looking yield curve, in this case, one from April 2017. The bottom of the chart shows U.S. Government bond maturities running from one month out to 30 years. The vertical axis shows the interest rate (yield %) associated with each of these maturities. We call this curve “normal” because the longer the maturity, the higher the yield. If you loan the government money for longer, you want more reward. This upward slope signifies a healthy economy and financial system.

Occasionally, the yield curve “inverts” to an opposite slope, with longer-term maturities yielding less than shorter-term maturities. This is a scary condition because all eleven U.S. recessions since WWII have been preceded by an inverted yield curve.4 The tricky thing is, inverted yield curves have “signaled twelve of the last six recessions”, and it can take some time for a presaged recession to actually show up. Note our example of an inverted yield curve from Nov 20, 2006. Everything was just fine then, right?

The important thing to remember is that an inverted yield curve is the bond market saying “you’re going to have a recession”. When people talk about an inverted yield curve, they are usually focusing on a specific “part” of the curve: the difference in yield, or “spread”, between 2- Year and 10-Year maturities. The link between inversion and recession can stem from the Fed raising short-term interest rates so high they break the financial system and we have a recession. Or it can be that investors think the Fed is about to break the economy, in which case longer-term yields drop amid a wave of demand for safety. We worry less about why the yield curve inverts and more about the economic implications this market signal portends.

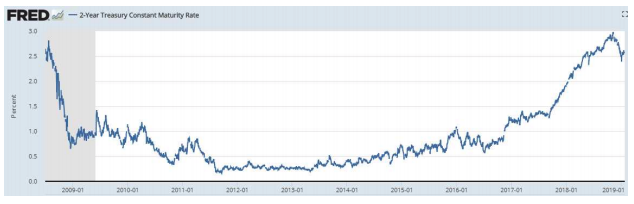

Our walk through the yield curve helps explain what the heck happened to the markets last year. The background is that the Fed had been raising short-term rates due to a healthy economy (thus raising the 2-Year rate). Then, after some ominous early-warning economic data emerged late in the year, stock investors, already jumpy given it has been nearly a decade since the last recession, went scurrying for cover. Economically-sensitive housing and auto stocks went into a tailspin. Investors sold stocks to move into long-term bonds. That influx of demand pushed down long-term yields (including the 10-Year), bringing the curve even closer to inversion.

The flattening yield curve (shown below in the graph of the 2-Year and 10-Year yields over time - if the lines cross it’s an inversion) started to become a self-fulfilling prophecy which reached a fever pitch when the Fed sounded like it was going to keep raising rates no matter what. This was when the market reached its steepest descent in December.

For those who know how to read the signs, the bond market seemed to be crying out to the Fed, “Stop it! You’re breaking the economy!” as the curve came closer and closer to an inversion. A yield curve spread of only ten basis points on December 10th suggested a 57.4% chance of recession in the next year. Stocks plunged. The bond market further declared, “Not only will you stop raising rates, you’re going to lower them.” Market-based odds of a Fed rate hike in 2019 promptly dropped from 90% to 0%5.

So there you have it, the story behind the quick 20% drop in the stock market in the fourth quarter: a situation in the bond market, sparked by slowing global growth fears and perpetuated by Fed language, that signaled to many that we were barreling into recession. Toward year-end the Fed changed its tune to suggest it would be “data dependent” with its tightening as opposed to being on auto-pilot. It recently went further, indicating it could end its quantitative tightening program sooner than expected.6 The Fed’s revised communication, along with actual hard economic data continuing to show an expanding U.S. economy, has sent stocks off to the races again in 2019. All is well then?

We are so far not finding other signs that a recession is about to unfold. However, it is possible the bond market knows something we don’t; the yield curve has backed off a bit but still says there is a ~35% chance of recession in the next year. We are in an unusually long (but shallow) economic expansion and there are areas of excess like at past recessionary points. We are thus on “recession watch”. Consider the following data points:

1) U.S. corporate debt to GDP is at a multi-decade high and consistent with past recessions (recessionary periods are represented by grey bars).

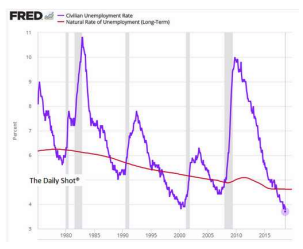

2) Unemployment is well below the “natural” rate considered sustainable without inflation. This condition is consistent with past recessions.

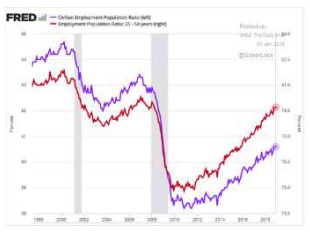

3) Workers as a percentage of the prime age population (the red line at right) has returned to the level prior to the last recession7. These workers coming off the sidelines were the reason we have not seen wage inflation. This trend may be over. Surveys are showing an increasing number of businesses reporting that the quality and cost of labor is becoming a big problem. In the past, such problems have led to wage growth, which leads to inflation, which leads to higher rates from the Fed, which leads to economic and stock market difficulties.

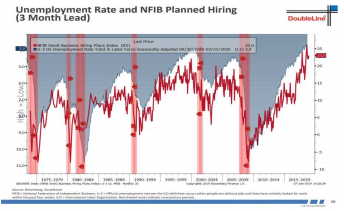

4) A low unemployment rate (shown inverted in grey to the right) and strong hiring demand (red line) both suggest labor tightness and are consistent with past recessions (red bars).

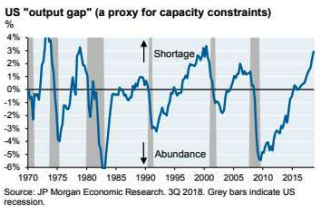

5) The “output gap”, the difference between actual economic output and the level most efficiently produced, is consistent with capacity constraints and past recessions.

For now, economic conditions remain solid and stocks are off to a nice start this year. However, as the above charts suggest, the economy is only likely to get worse going forward. As the market continues to heal, we will likely reduce exposure to positions which will suffer most in a recession. It is important to be thinking about such action now, in advance of a downturn. Stocks actually rise over the full course of recessions, as investors eventually look forward to recovery. It is the period leading up to a recession which becomes perilous and which we seek to defend against. That said, as (almost) always, the odds are good that the stock market is higher three to five years from now. Our focus is on adjusting the portfolio as appropriate for an evolving environment.

Above all else, we appreciate the trust you place in us and continue to invest our capital alongside yours. We wish you a good 2019. Already this year our colleague Ivan has been blessed with a beautiful baby and so the year is off to a fine start.

Sincerely,

John G. Prichard

Miles E. Yourman

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

1 Admittedly, this leaves out the Great Depression, when high double-digit unemployment rates and negative stock returns coexisted for some time.

2 In the past few days it has come to light that PG&E’s equipment did not, in fact, start the most deadly and destructive of the 2017 fires, the Tubb’s fire which burned portions of Santa Rosa.

3 While we expect a price higher than that which prevails today, we do not expect a full return to our purchase price.

4 Recessions have occurred, however, in other countries without an inverted yield curve. Japan, for example, has had multiple recessions since 1991 without an inverted yield curve. This is true also with three of the past four recessions in Germany.

5 The market was even pricing in a 2019 rate cut at one point. Which we would paraphrase the bond market as saying, “Mr. Fed Chairman, not only are you wrong in saying that you’ll be raising rates in 2019, but you’ve already broken the economy and soon you’ll see it my way and reverse course.”

6 Quantitative Tightening(“QT”) means the Fed is contracting its balance sheet as Treasury and mortgage securities mature and are sold, reducing banking system reserves and resulting in higher interest rates than would otherwise be. This reverses the Quantitative Easing (“QE”) of earlier years. In English: if QE was “printing money” then QT is “tracking down money and destroying it”.

7 We believe the employment to prime-age (25-54) population ratio is a much better measure than the official unemployment rate because the official ratio doesn’t capture people who have become discouraged and dropped out of the labor force. It is also a better measure than the plain “employment to population ratio” because the population is aging, and it is only natural that a lower proportion of people would be employed when a greater proportion of people are retired.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All