In the last couple of years, Nobel Laureate Robert Shiller has championed the idea of economic narratives. Economic data describe “the fundamentals,” but stories are often the key drivers of activity. Investors are currently faced with two competing narratives. There are no signs that the economy is in a recession or about to enter one. However, the risks to the economic outlook are weighted to the downside, and many market participants fear a downturn later this year or in 2020. Over time, these two narratives ought to evolve in a way that brings them closer together.

Stock market participants were upset in mid-December when the Fed signaled an expectation of further increases in short-term interest rates. The dot plot showed that most senior Fed officials thought it would be appropriate to raise rates one, two, or three times in 2019 (with a median of two). Market sentiment turned more positive recently when Fed Chairman Powell signaled the policy would be flexible and that the central bank could afford to be “patient” in deciding when to raise rates. This was nothing new. In his post-FOMC press conference of December 19, Powell noted that inflation has been “a touch below” the 2% goal, which “gives the Committee the ability to be patient in moving forward.”

Click here to enlarge

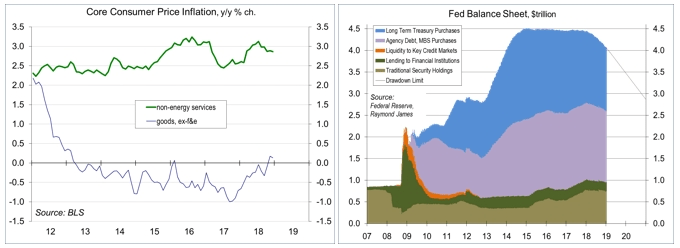

From the beginning, the Fed viewed the unwinding of its balance sheet as “background,” not active monetary policy. The Fed allows up to a certain amount of maturing securities to run off each month. The pace would not be adjusted to influence economic activity. The Fed’s asset purchase programs (QE1-3) are thought to have lowered the 10-year Treasury note yield by about 100 basis points. Accordingly, the decrease in the balance sheet should put upward pressure on bond yields. However, the unwinding is expected to occur over a few years and will not return the size of balance sheet to where it was before the financial crisis. Instead, the 10-year Treasury note yield has declined. That doesn’t mean that the balance sheet unwind hasn’t had an impact. Rather, there are a number of factors acting on long-term interest rates. The bigger concern about the balance sheet unwind is the effect on bank reserves. The FOMC minutes showed that the Fed is considering a number of technical adjustments to the federal funds market. Chairman Powell said that the balance sheet unwind did not appear to be a factor in recent financial market volatility, but the Fed could adjust the pace if that proved otherwise. Moreover, while nobody, including Fed officials, knows where the size of the balance sheet will end up, it is now likely to be higher than it was expected to be a month ago.

A year ago, many financial market participants expected that the Tax Cut and Jobs Act of 2017 (TCJA) would drive business fixed investment and new hiring. Many economists were less enthusiastic, noting that firms were generally flush with cash and borrowing costs were low. If businesses were willing to expend, they would have already done so. Moreover, roughly a third of the corporate tax cuts would go to foreigners (either through firms doing business in the U.S. or through foreign investors in U.S. companies). Deregulation was also seen as supportive, although it’s impossible to provide a precise estimate of the economic impact. Setting aside the question of the economic impact of the tax cuts and deregulation, the belief that these would provide an economic boost could be self-fulfilling (that is, this is mostly an issue of confidence). If that’s the case, then the economic gains would be more fragile.

Most economists expected that fiscal stimulus (tax cuts and increased government spending) would provide a boost to growth in 2019, but some expected labor market constraints to become more binding. The unemployment rate fell further last year, but labor force participation also increased. There was more slack in the job market that was thought at the start of last year. Still, the pickup in wage growth is consistent with a tighter labor market. In turn, increased wage growth should lead to a more efficient allocation of labor and faster productivity growth over time, which reduces the inflationary impact.

Trade policy disputes and the showdown over Trump’s border wall are unnecessary disruptions to the economy and present increased downside risks the longer these stalemates last. Any resolution to these issues would be taken well by the financial markets.

Click here to enlarge

Data Recap – Reports on factory orders and the trade balance were postponed due to the partial government shutdown. Inflation figures were as expected. Fedspeak was viewed as market friendly.

The FOMC Minutes from the December 18-19 policy meeting indicated that “participants noted the contrast between the strength of incoming data on economic activity and the concerns about downside risks evident in financial markets and in reports from business contacts.” Fed officials “generally revised down their individual assessments of the appropriate path for monetary policy and indicated either no material change or only a modest downward revision in their assessment of the economic outlook.” The increase in short-term interest rates at the meeting, brought the federal funds target “at or close to the lower end of the range of estimates of the longer-run neutral interest rate.” However, “participants expressed that recent developments, including the volatility in financial markets and the increased concerns about global growth, made the appropriate extent and timing of future policy firming less clear than earlier.” Hence, the FOMC “could afford to be patient about further policy firming.”

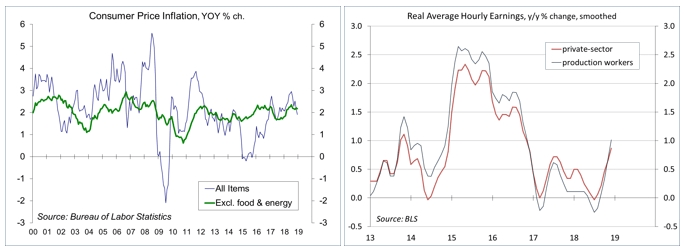

The Consumer Price Index fell 0.1% in December (+1.9% y/y), held down by a drop in gasoline prices. Food rose 0.4% (+1.6% y/y), while energy fell 3.5% (-0.3% y/y). Gasoline prices sank 7.5% (-9.9% before seasonal adjustment, -2.1% y/y). Ex-food & energy, the CPI rose 0.2% (+2.2% y/y). Owners’ Equivalent Rent (23.9% of the CPI) rose 0.2% (+3.2% y/y), while rent (7.9% of the CPI) rose 0.2% (+3.5% y/y), and lodging away from home (0.9% of the CPI) jumped 2.7% (+0.2% before seasonal adjustment, +0.9% y/y). New motor vehicle prices were flat (-0.3% y/y). Used motor vehicle prices fell 0.2% (+1.4% y/y). Airline fares fell 1.5% (-2.6% y/y). Ex-food & energy, prices of consumer goods rose 0.1% (+0.1% y/y) – a contrast to the moderate pressure seen in the core consumer goods component of the Producer Price Index (+2.7% y/y in November). Non-energy services rose 0.3% (+2.6% y/y).

Click here to enlarge

Real Average Hourly Earnings rose 0.5% in December (+1.1% y/y), up 0.6% for production workers (+1.5% y/y). The increase in purchasing power should help support consumer spending growth in the near term. Note that the January data should show a further increase in the year-over-year gain.

Jobless claims fell to 216,000 in the first week of the new year, following 233,000 in the previous week, leaving the four-week average at 221,750. The weekly figures are normally choppy through the first several weeks of the year due to difficulties in the seasonal adjustment. Idled federal government workers are not included in the total, but there is likely to be some secondary impact on non-federal employment (private-sector workers in food service and retail who supports government workers).

The ISM Non-Manufacturing Index dipped to 57.6 in December, vs. 60.7 in November. New orders remained strong. Business activity and employment slowed, but remained strong by historical standards. Input price pressures moderated. Comments from supply managers were generally upbeat, but continued to show ongoing concerns about tariffs and labor market constraints.

The Index of Small Business Optimism was little changed in December (104.4 vs. 104.8 in November). Respondents were less enthusiastic about general business conditions in the last two months, but hiring intentions and capital spending plans remained moderate.

The Bank of Canada left short-term interest rates unchanged. “Growth has been running close to potential,” according to the BOC, and “employment growth has been strong and unemployment is at a 40-year low.” The BOC’s Governing Council “continues to judge that the policy interest rate will need to rise over time into a neutral range to achieve the inflation target.” However, “The appropriate pace of rate increases will depend on how the outlook evolves, with a particular focus on developments in oil markets, the Canadian housing market, and global trade policy.”

This Week – The government shutdown means that the December retail sales report will be delayed. Reports from the Bureau of Labor Statistics (PPI, import prices) and the Federal Reserve (Beige Book, Industrial Production) should still be released on time. Earnings reporting season gets underway, and investors may be more interested in the guidance than the actual results for 4Q18. Financial market participants will continue to focus on trade policy and federal budget stalemates. Any signs of progress would be taken well by the stock market.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James