IN THIS ISSUE:

1. Powell Repeats: The Fed Can Be “Patient” On Rate Policy

2. No Talk of Slowing the Reduction of Fed’s Balance Sheet

3. Should President Trump & Congress Reform Federal Reserve?

4. Proposals For Reforming the Federal Reserve

Overview

Fed Chair Jerome Powell used the “patient” word again last week. He also added new words that the Fed can “wait and watch” before raising rates again. And he added another new word, that whenever interest rate increases resume, they will be “gradual.” The stock markets loved it!

There are growing calls for President Trump and Congress to reform the Fed, and there are some good reasons for it. There could be broad bipartisan support if the president decides to pursue it. I’ll discuss this issue as we go along today.

Powell Repeats: The Fed Can Be “Patient” On Rate Policy

For the second time this month, Fed Chairman Jerome Powell reiterated that the central bank now feels it can be “patient” with regard to additional interest rate hikes this year. He first used that word on January 4 while speaking at the American Economic Association conference in Atlanta.

At that time, he said that while the US economy is strong, the global economy is slowing, and this concerns the Fed. He added that US inflation remains quite low. Together, a slowing global economy and very low inflation allow the Fed to reduce the number of rate hikes this year. Markets rejoiced at this apparent reversal of policy and stocks rallied strongly last week.

Then he used the patient reference again last Thursday, speaking at The Economic Club in Washington, DC and added some other language that boosted the stock markets. Powell said the central bank can pause its rate hike policy as the Fed “waits and watches” to see if the US economy will slow down this year or continue the strong recovery that began last year.

Meanwhile, several other senior Fed officials began to use the patient language in their speeches around the country, thus confirming that the Fed has shifted policy at least for now.

The question is: What has happened to make the Fed soften its monetary policy on interest rates? You may recall as recently as late November that Powell and other Fed officials were considerably more hawkish, suggesting another 3-4 rate hikes this year.

Our best clue in figuring this out is the minutes of the last Fed Open Market Committee (FOMC) meeting on December 18-19, which were released to the public last Wednesday. Early-on in that meeting, the members discussed the possibility that the upward move in the Fed Funds rate could be “gradual,” another comforting word for the stock markets.

Elsewhere in the minutes, there was a discussion suggesting that most members of the Committee have shifted their thinking to a “more gradual path of federal funds rate increases.” OK, we get that. But why?

The minutes go on to reveal that most Committee members have grown more concerned about a variety of risks, both international and domestic, which include Brexit, financial instability in Italy, the slowing global economy and the growing risk of a trade war with China and others.

On the domestic side, the members feel that the US economy will slow down this year, although not dramatically. They worry about the ongoing slump in the housing market. They voiced concerns about the continued flattening yield curve. They also pointed to the recent declines in oil and energy prices, suggesting this could reflect softening global demand. They also discussed the recent sharp decline in the stock markets.

The members concluded that the Committee had “some latitude to wait and see how the data would develop amid the recent rise in financial market volatility and increased uncertainty about the global economic growth outlook.” There you go – they’re worried.

Near the end, they added: “… based on current information, the Committee judged that a relatively limited amount of additional tightening likely would be appropriate.” In Fed-speak, that means we’re not going to raise rates 3-4 times this year, and we’re going to wait and watch for a while before we do anything. This was music to the markets’ ears.

No Talk of Slowing the Reduction of the Fed’s Balance Sheet

What the Committee members didn’t talk about at the December meeting was slowing the reduction of its balance sheet. There has been a growing chorus in recent weeks that the Fed should slow down or halt the reduction of its huge balance sheet, which includes mostly US Treasuries and mortgage-backed securities, if it is going to continue raising the Fed Funds rate.

Apparently, the members feel that with the decision to pare down the number of rate hikes, there’s no reason to slow down or eliminate the balance sheet reduction. Mr. Powell was asked about this following his speech last week in Washington. He replied that the balance sheet will be “substantially lower” than it is today.

Since last October the Fed has been letting $50 billion a month in securities mature and roll off the balance sheet. While he didn’t say so specifically, his comment suggests that the $50 billion a month in reduction will continue indefinitely.

This news sent stocks temporarily lower just afterward. In the big picture, I think the reduction in the number of rate hikes is more important to the markets than the rate of reduction in the balance sheet. As always, time will tell.

Should President Trump & Congress Reform the Federal Reserve?

Since I’m on the topic of the Fed today, let’s turn to the growing calls for the president and Congress to reform it, which many believe is long overdue.

The Federal Reserve Bank, which is the US central bank, has long been one of the most controversial quasi-governmental entities since its founding in late 1913. There are many conspiracy theories surrounding the Fed – who owns it, who controls it, why does it exist, etc.

Rather than get into all that, let’s look at how the Fed is currently structured and some of the proposals for how to reform it. The Fed consists of the Federal Reserve Board of Governors, an independent government agency, located in Washington, DC.

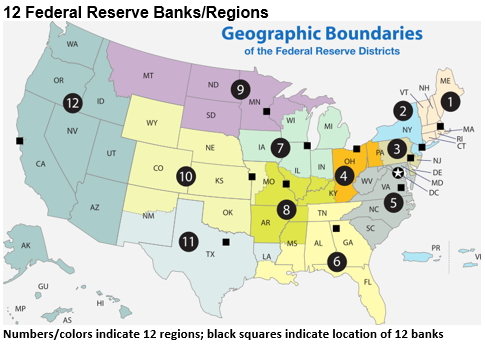

The Board of Governors (BOG) is made up of seven members who are nominated by the US President and confirmed by the Senate. It is charged with overseeing the 12 Federal Reserve Banks located around the country. Presidents of the Federal Reserve Banks are selected by their respective Boards of Directors with approval by the Board of Governors.

The Fed Open Market Committee, which sets monetary policy, consists of the seven members of the Board of Governors, the president of the New York Fed, and four of the other eleven regional Federal Reserve Bank presidents (on a rotating basis) – for a total of 12 voting members. The other seven Fed Bank presidents attend the FOMC meetings but do not vote.

Proposals For Reforming the Federal Reserve

The most important question is: Does the Fed need to be reformed? Most Fed-watchers agree the answer is YES. The Fed was widely blamed for missing the signs that led up to the 2008 financial crisis, and therefore the Great Recession.

Then there’s the issue of the devastating loss of community banks and local credit unions since the Great Recession. According to data from the House Financial Services Committee, we have lost one community bank or credit union every day since 2008.

While much of the blame for this is placed on the Dodd-Frank legislation which made it much more expensive for small banks to operate, the Fed is also blamed for policies that favor big banks over smaller ones.

More recently, the Fed has clearly been in the spotlight for raising short-term interest rates four times last year and until this month, was expected to do 3-4 more hikes this year. There are strong, emotional arguments on Fed monetary policy, how policies are developed and how much power the Fed should have.

Some are suggesting that President Trump use his upcoming State of the Union address to unveil a bold new plan to reform how the Fed is structured, how its top leaders are selected and to review the Fed’s mandate and policies. The Fed’s current mandate from Congress is to: "Promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates"

A bill to reform the Fed and look at alternative ways to conduct US monetary policy passed in the House of Representatives in 2015, only to be shot down in the Senate. That bill envisioned a 12-Member Committee, with six appointed by the Speaker of the House and six appointed by the President Pro-Tem of the Senate – along with two non-voting members, one appointed by the Treasury Secretary and another selected from among the Fed’s Governors.

There are many reasons to reform the Fed, many more than I have room to go into today. There are calls from both sides of the political aisle to reform the Fed. Some analysts believe that with the Democrats in control of the House, there could be wide bipartisan support for such a reform bill. Of course, it remains to be seen if President Trump gets on board.

Best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by Halbert Wealth Management, Inc. Gary D. Halbert is the president and CEO of Halbert Wealth Management, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific advice. Readers are urged to check with their financial counselors before making any decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, Halbert Wealth Management, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have their own money in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management

© Halbert Wealth Management

Read more commentaries by Halbert Wealth Management