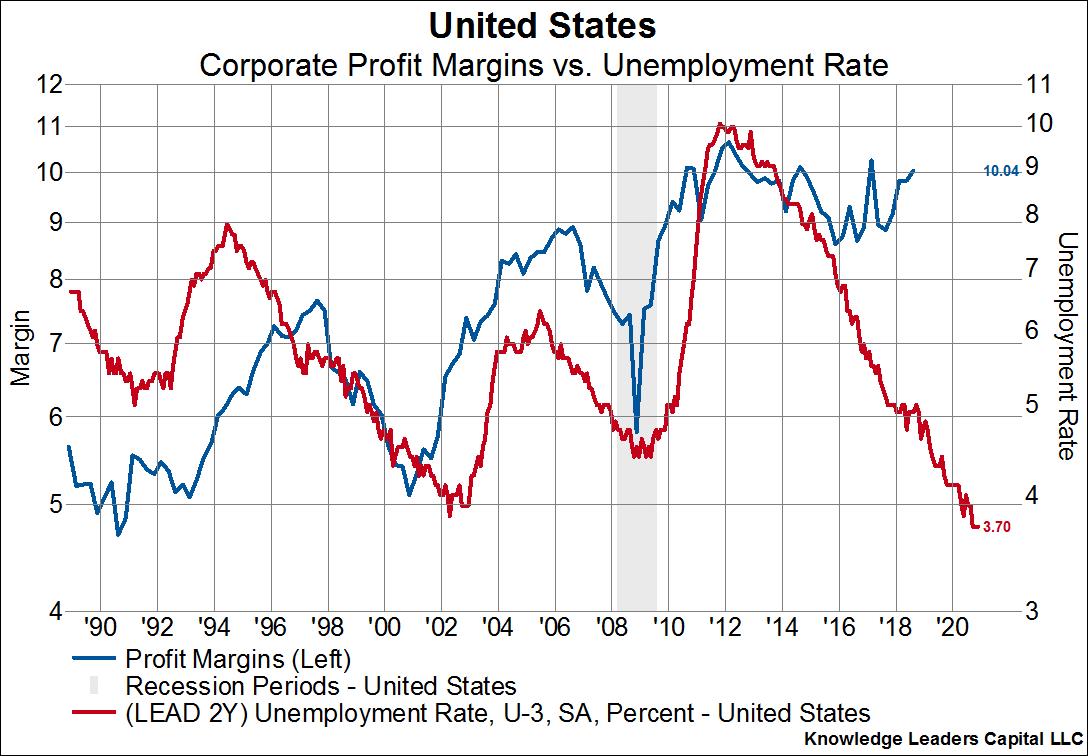

Is 2019 Going to be the Year of the Profit Margin Problem?

2018 has been kind to corporate profit margins. In fact, the margin expansion we’ve seen so far in 2018 is unprecedented in a late cycle economic environment when wages are rising briskly, at least looking back over the last thirty years. What has been different this time around is that the corporate tax rate was lowered from 40% to 25%, allowing profits to expand even in the face of rising wage and variable cost pressures. So the question moving forward is, can companies maintain this level of profitability for another few years, or have we seen the best of it? Based on at least the few factors we highlight below, we think 2019 and beyond will look much different from 2018.

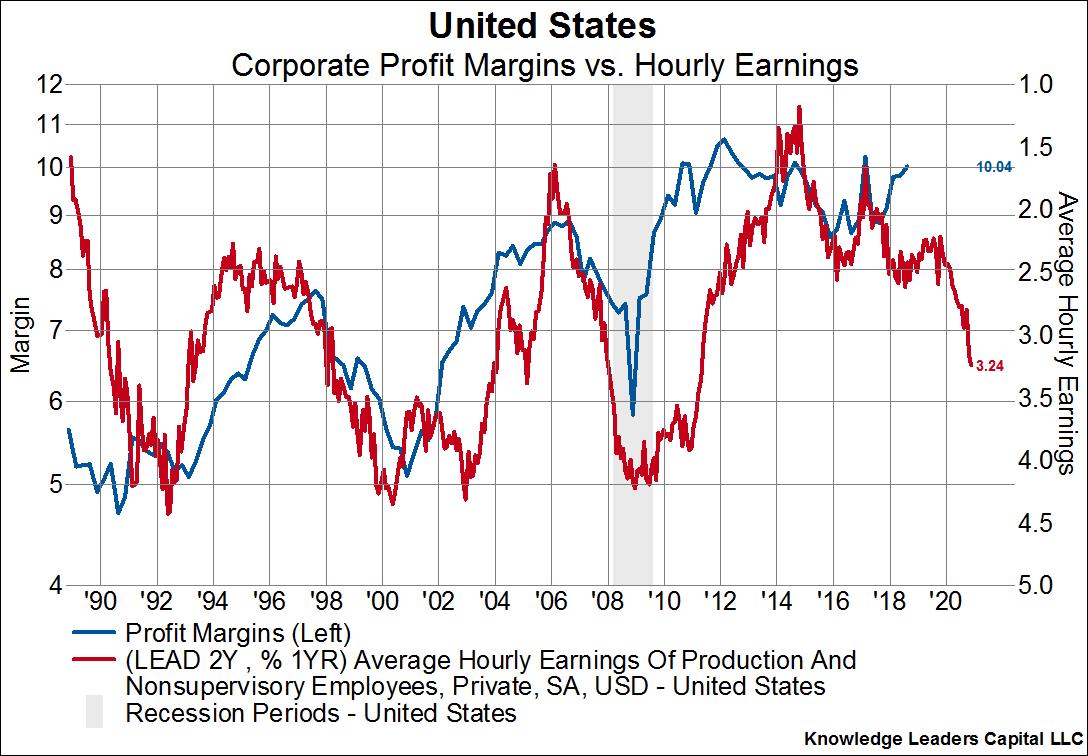

As we can see in the first chart below, there is a strong negative relationship between profit margins (blue line, left axis) and average hourly earnings (red line, right axis, inverted). When average hourly earnings rise, margins invariably fall with a two year lag time. Average hourly earnings have been rising in a strong trend (red line going down) since early 2017, but profitability was able to buck the consequent drop off due to tax reform. However, now that hourly earnings have so clearly broken out to the upside and are rising at the fastest pace since 2007, we have serious doubts about the ability of profit margins to not follow the path of least resistance, which is down.

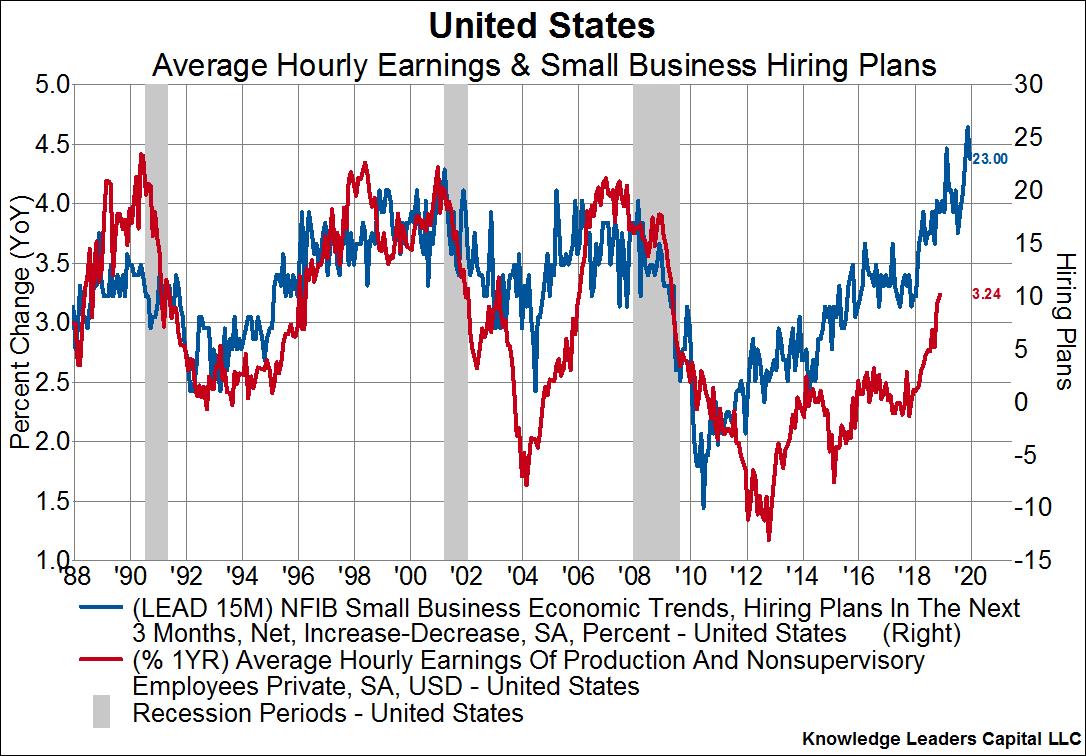

And we further have reason to expect hourly earnings will continue to rise even more briskly in the year ahead, which of course will add duration and magnitude to the pressure on margins. As the next chart below demonstrates, small business hiring plans lead hourly earnings growth by 15 months. Hiring plans (blue line) remain near an all-time high and in a strongly rising trend. As such, hourly earnings growth (red line) has every reason to follow hiring plans higher for the next year or so.