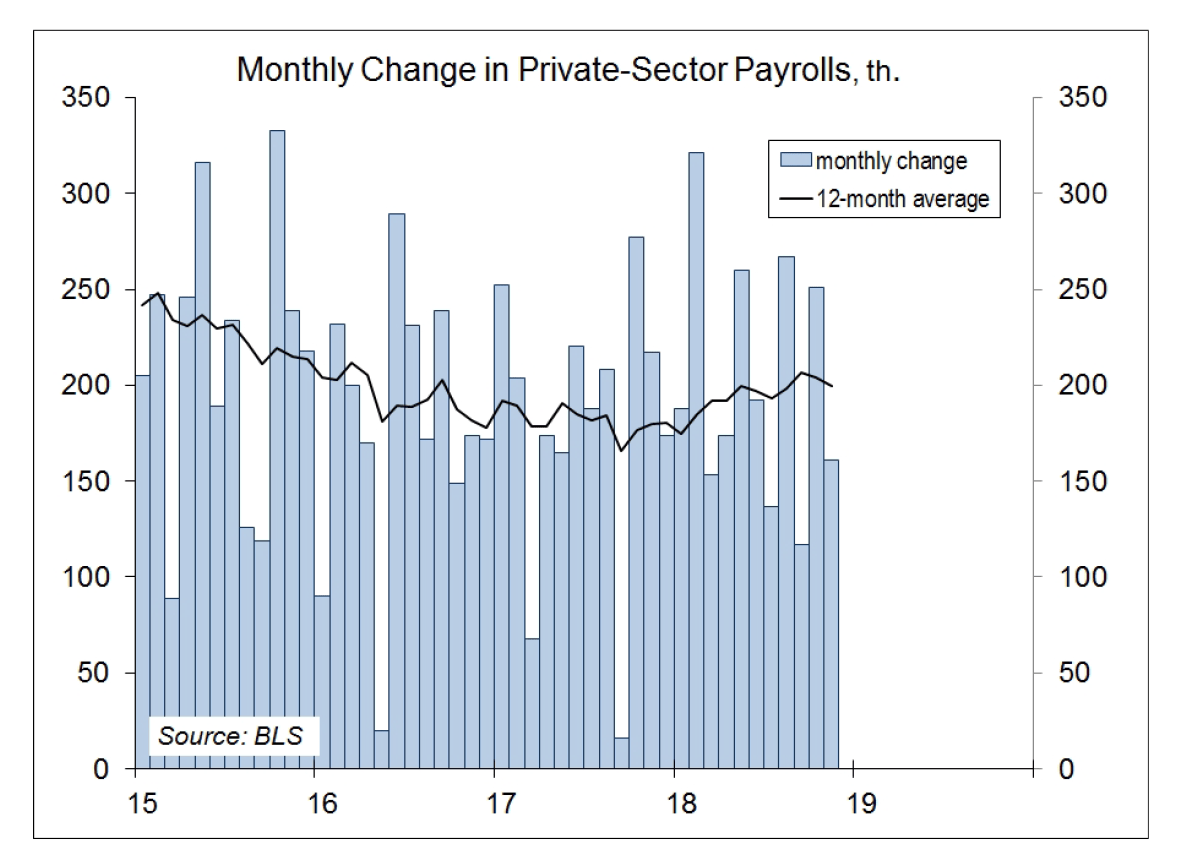

Nonfarm payrolls rose less than expected in November. The three-month average remained relatively strong, although below the pace of the first half of the year. That's not surprising. As the job market tightens, the number of available workers decreases. Anecdotal reports suggest that firms are having further difficulty finding skilled labor, and workers are more likely to quit to find better employment. Wage pressures remain moderate, but are rising. This is consistent with a December 19 Fed rate increase. The pace of tightening in 2019 is unclear, but the markets anticipate a more cautious Fed, and that has contributed to the flattening of the yield curve. Nonfarm payrolls rose by 155,000 in the initial estimate for November. The monthly change is reported accurate to ± 115,000, meaning that there is a 90% chance that the true change is between +40,000 and +270,000. Statistically, we can't say that job growth slowed last month. The noise in the payroll data can be reduced by looking at an average over a period of months. For the private sector, job gains averaged 176,000 per month over the last three months, vs. +215,000 for the first half of the year.

Click here to enlarge

Click here to enlarge

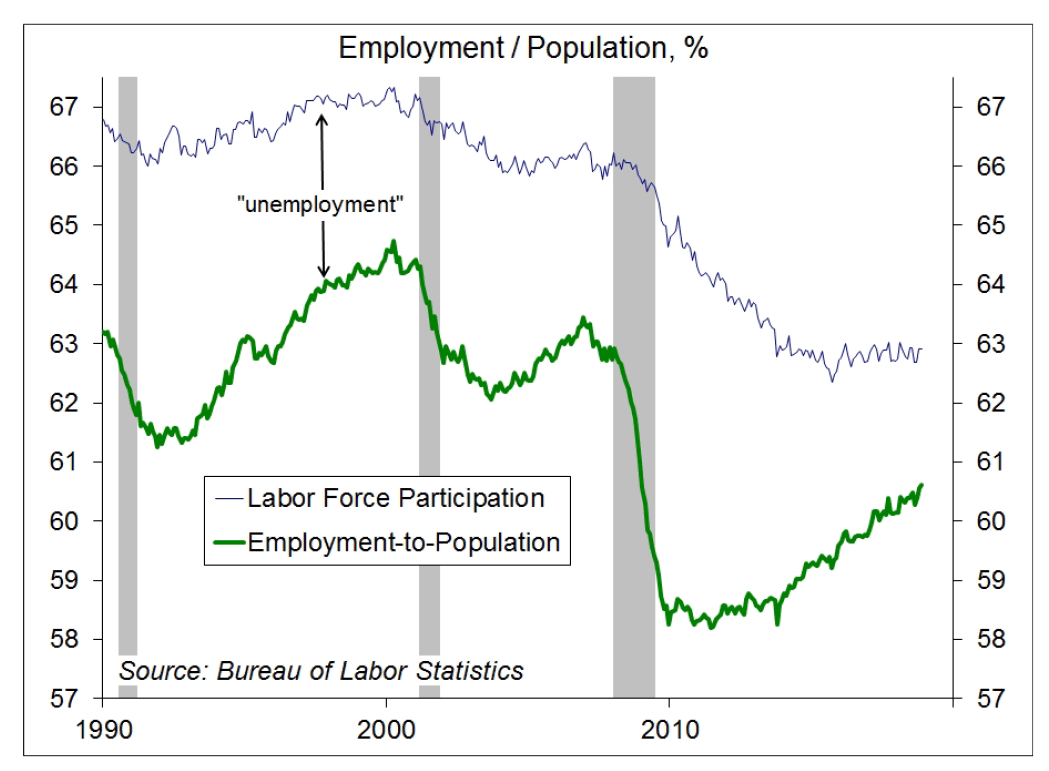

The unemployment rate held steady at 3.7% last month (note that annual benchmark revisions to the household survey data will arrive next month). Labor force participation held steady, and has been trending flat over the last several months. That's actually a sign of strength, as demographic changes (the aging population) imply that the participation rate should be trending lower. The employment/population ratio has been trending gradually higher, but remains below the pre-recession level. However, for the key age cohort, those aged 25-54, the ratio is nearing where it was before the recession While there is often a focus on prices of raw materials, the labor market is the widest channel for inflation pressures. Fed officials fear that a further tightening in the job market would continue to lift wage inflation. If not offset by faster productivity growth, higher labor costs would lead to higher consumer price inflation (if firms can pass the increase along) or reduced profit margins (if not). Rising wage pressures ought to lead to a more efficient allocation of labor over time (in other words, faster productivity growth). Anecdotal reports suggest that there is a shortage of skilled labor, but unskilled labor remains plentiful. This mismatch could be addressed through in-house training, but firms may be reluctant to take this route (that is, to incur training costs) if the economy is expected to slow. The Fed could help by signaling a slower pace of tightening. In the late 1990s, the Fed, led by Alan Greenspan, held off on raising short-term interest rates as the unemployment rate fell. However, the late 1990s was an extraordinary period for the U.S. economy, when new technologies (cell phones, the internet) were coming on. It was a transformative time. Job destruction was extremely high, but job creation was even higher. Could the Fed usher in a similar period now? Hard to say. The late 1990s ended with a mis-allocation of capital (the dot-com boom), which ended badly, and the new technologies, which allowed firms to do more with fewer workers, restrained a recovery in the job market in the 2000s.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James