Boston - The media and some market participants can get pretty worked up over the flattening Treasury curve. But the question is: Is it warranted?

It is true that historically a flat Treasury yield curve typically precedes a recession on average by roughly two years. But keep in mind, the yield curve is driven by a range of different factors that has drastically changed over time. The Treasury yield curve is not some soothsayer, with a magical crystal ball that knows the second the Treasury curve inverts, a recession is imminent in two years.

First of all, the 2-year period is an average. Sometimes it has been longer, and sometimes it has been shorter. If a recession is four years out, good luck staying solvent while you wait for that view to play out. Remember, being early is the same thing as being late in investing -- you are wrong in both cases.

Last I checked, the U.S. economy just grew 3.5% in the third quarter and 4.2% in the second quarter, and is on pace for its strongest year of growth since 2004. So why is it that a recession is imminent? I'll admit, I believe growth in the U.S. will start to trail off from these impressive levels, but there is a big difference between growth slowing to somewhere in the mid-2% area, and a recession.

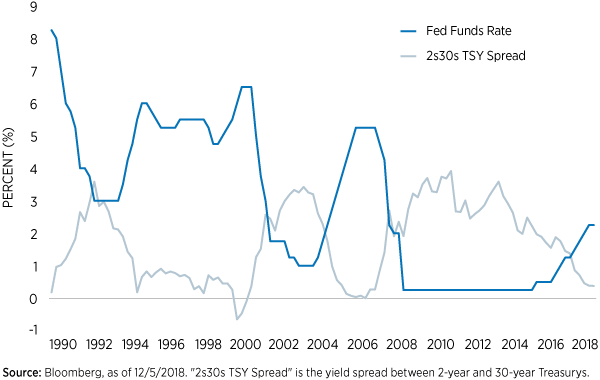

The short end of the Treasury curve has just inverted. This means you now get more yield investing in a 2-year Treasury than a 5-year Treasury. But this shouldn't be a surprise if you do your homework and look at history. As shown in the chart below, the curve always flattens during Federal Reserve hiking cycles.

So is this a concern? I would argue no, a flattening Treasury curve is not a problem. While it may be taboo to say this time is different in investing, there really are a number of forces that have distorted yield curves all over the world.

Many forget that a few years back, the Fed embarked on "Operation Twist," purposefully flattening the yield curve, because the long end of the curve has a greater transmission mechanism through the U.S. economy, as things like mortgages and corporate debt are generally tied to longer end rates.

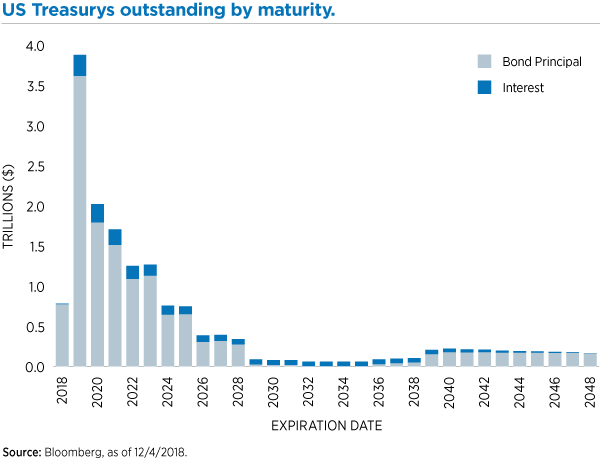

But it wasn't just Operation Twist that flattened the yield curve, it was also the Treasury and where on the curve the debt was issued. As shown in the chart below, the bulk of the outstanding Treasurys are actually inside of five years. It's pretty hard for the curve to steepen when all of the debt is so front-loaded. If the Fed was really concerned about a flat curve, it could work with the Treasury to issue more long-end debt, which would certainly steepen the curve.

With all this being said, I don't want you to think that I dismiss a flattening or inverted curve. I think an inverted curve very much can wreak havoc on the U.S. economy.

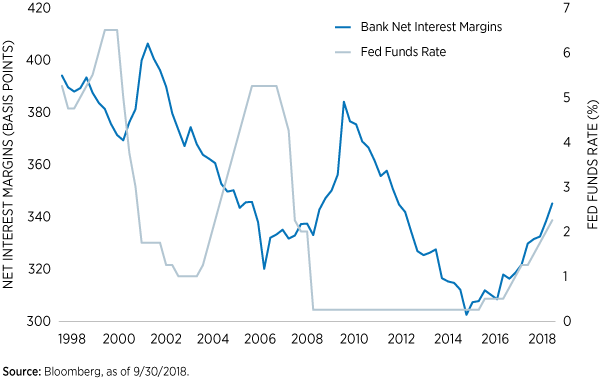

I just believe the market is looking at the wrong curve. It's not an inverted 2s-10s, or 2s-30s, or 2s-5s curve that matters. What really matters, in my mind, is what is happening to the curves at banks.

Historically as the Fed hikes rates, the spread between what a bank makes on its loans and what it pays on its deposits shrinks. But how many of you in your savings account have seen eight quarter-point rate increases as the Fed has hiked rates? I for one, am getting the same rate today as I was getting three years ago before the Fed began hiking rates.

At the same time, the rates banks are charging for a mortgage are up 150 basis points from their lows. This is the first hiking cycle where banks' margins are actually increasing as the Fed is hiking rates. The reason being, they aren't paying their depositors much more today than they were over the past few years.

I believe this is the curve that really matters. If a bank starts paying you 4% in your savings account and offering you a mortgage at 5%, then you should be concerned. It's a flat bank curve that causes banks to tighten credit, because it no longer makes sense for them to make loans when margins are so thin, which then causes a slowdown in the economy.

Bottom line: I believe a flat Treasury curve is not such a bad thing. For one, it means you no longer have to go out 10 or 20 years to get some sort of yield, since there is no term premium being priced in. If you can make the same yield in very short-duration bonds, why take on the added interest-rate risk if you aren't being paid to take it? Rising short-end yields also mean that cash alternative strategies are once again an investable asset class for yield. If you can get a 3% yield in a step out of cash strategy that avoids credit risk, and pays you more than inflation, there is now an opportunity cost to owning risk assets.

© Eaton Vance

© Eaton Vance

Read more commentaries by Eaton Vance