The key phrase in Fed Chairman Powell’s speech to the Economic Club of New York was widely misinterpreted by the financial press and, in turn, the markets. That’s not unusual. The markets don’t do nuance. Stock market participants were likely looking for an excuse to rally. Still, while policy decisions will remain data-dependent, the central bank can be expected to maintain a more cautious approach to raising rates in 2019. Lost to the markets, Powell also spoke of possible technical adjustments in how monetary policy is conducted and the Fed unveiled its new semi-annual Financial Stability Report.

Here are some of the press headlines from Powell’s speech:

WSJ – “Fed Chairman Says Interest Rates Are Just Below Estimates of Normal”

CNBC – “Fed Chairman Powell now sees current interest rate level ‘just below’ neutral”

Reuters – “Dollar under pressure after Fed’s Powell says U.S. rates near neutral”

CBS – “Federal Reserve Chair Jerome Powell suggested for the first time in two years, the Fed may be close to ending rate hikes”

NYT – “Fed’s Powell in Apparent Dovish Shift, Says Rates Near Neutral”

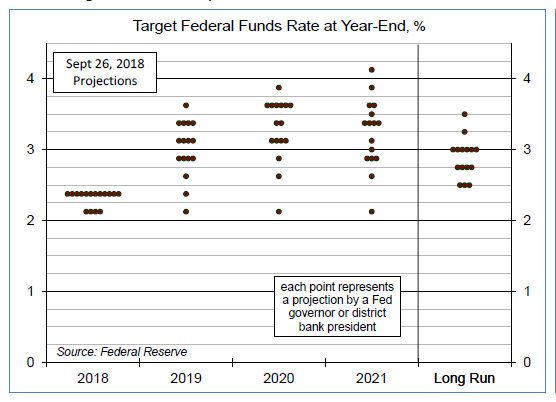

That’s wrong. Here is the actual quote: “Interest rates are still low by historical standards, and they remain just below the broad range of estimates of the level that would be neutral for the economy – that is, neither speeding up nor slowing down growth.” The key part of the phrase is “below the broad range.” Fed officials differ in their estimates of the neutral rate. In September, most saw the neutral rate as 50-75 basis points higher than it is now, implying two or three more rate hikes to get to a neutral level. Moreover, most Fed officials expected that the FOMC would need to move the federal funds rate above a neutral level in 2019 and2020. We’ll get a new dot plot on December 19, and while the dots may drift a little lower, they ought not to change much.

Click here to enlarge

Click here to enlarge

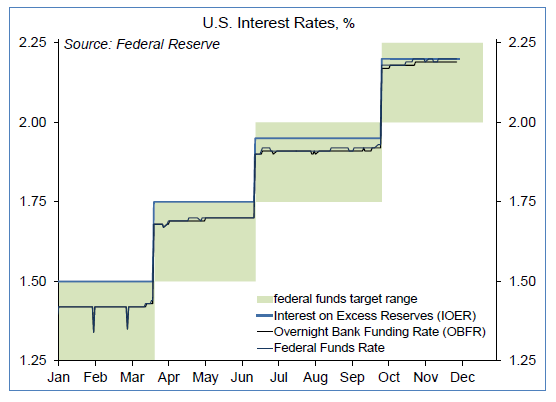

The minutes of the November 7-8 Federal Open Market Committee meeting noted that “almost all participants expressed the viewthat another increase in the target range for the federal funds rate was likely to be warranted fairly soon if incoming information onthe labor market and inflation was in line with or stronger than their current expectations.” The minutes also highlighted sometechnical issues. During the financial crisis, the Fed began announcing a range for the federal funds rate (the overnight lending ratefor bank reserves), rather than a target level, with the Interest on Excess Reserves rate (IOER) defining the top of the range. Theactual federal funds rate (a market rate) coalesced near the middle of the range, but has drifted higher, toward the IOER. In June,the Fed lowered the IOER by 5 basis points, in an attempt to push the federal funds rate down. Instead, it has continued to rise, andis now trending at the IOER. In November, the FOMC discussed the possibility of moving the IOER down relatively soon. This is atechnical adjustment, not a change in policy. But wait, there’s more. The Fed is also considering replacing its main policy tool (thefederal funds rate) with the Overnight Bank Funding Rate (ORFB), which is a weighted average of the federal funds rate and theovernight Eurodollar borrowing rate. “The larger volume of transactions and greater variety of lenders underlying the OBFR couldmake the rate a broader and more robust indicators of banks’ funding costs,” according to the FOMC minutes. The OBFR hastracked the federal funds rate closely – so this wouldn’t be a shift in monetary policy.

On financial stability, Powell noted some concerns in business lending (“firms with high leverage and interest burdens haveincreased their debt loads the most” over the last year). Equity market prices “are broadly consistent with historical benchmarks,”Powell noted, and market volatility is separate from events that threaten financial stability.”

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James