Value investing, which is often traced back to Ben Graham in the 1940s, is among the most influential trends in finance in recent decades. Value investing is based on the idea that lots of stocks are out of investors’ favor because of myriad of reasons, such as recent losses, management upheaval (think GE), product failures, etc. Investors beat down the share prices of these companies, resulting in low market-to-book ratios (market value of company divided by its book, or equity (net assets) value reported on the balance sheet). These are the “value stocks.”

At the other extreme, are the glamour (growth) companies―think Apple, Amazon and Netflix―whose recent success leads investors to believe in an unending growth, or permanent prosperity. Investors bid up the shares of these companies, resulting in high market-to-book ratios.

And here is the essence of the value theory: Many investors make systematic mistakes; they over-emphasize recent evidence (a phenomenon termed by behaviorists―the “recency effect”) namely, they are convinced that 2-3 quarters of losses are harbingers of long-term corporate decline, or that a short streak of sales increases portend long-term expansion. That’s the reason they bid down the former and up the latter. In reality, though, many of the out-of-favor “losers” recover soon (that’s the reason they are called “value”), and at the other extreme, many of the seemingly permanent growth companies falter. Growth is notoriously ephemeral.

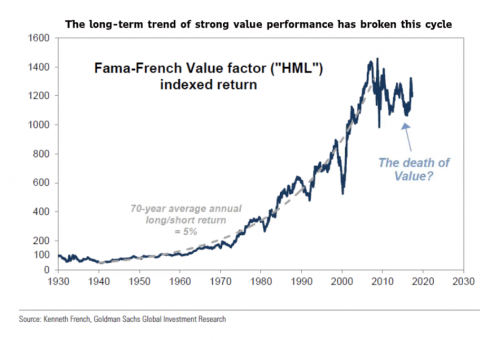

Under this scenario of investors’ systemic misvaluations, investing in value (beaten up) stocks pays off, because their share prices subsequently rise, and selling short growth (inflated) stocks is a winner, because these shares are soon to decline. And, indeed, historically, such value investing was a very successful strategy, as the following figure demonstrates.

In fact, value investing was so successful that hundreds of funds and ETFs were based on the value strategy, drawing untold billions of investor’s dollars. Value investing ruled for decades. Academics, though, were puzzled by the success of value investing, because many don’t really believe in sustained investor irrationality and protracted misvaluations. Markets are widely believed to be efficient, that is, rational. But reality was stronger and investors flocked into value funds undisturbed by academic bewilderment.

Alas, nothing lasts forever, particularly fun, and as the right-hand-side of the above figure shows the good days of value investing came to a screeching halt 10-12 years ago. A shocking development which led to massive investors’ losses and the demise of many value funds. Practically everybody declared that “value investing is dead,” see next figure.

The widely-believed death of value investing naturally intrigued me. I don’t believe in sudden economic shifts, particularly without a good explanation. So, with my colleague Anup Srivastava (University of Calgary), I embarked on research into the value apparent demise. Our research is in progress, but I want to share with you an early, very interesting finding, suggesting that the value strategy isn’t dead yet.

I have written extensively on this blog, and in my recent book, The End of Accounting, on the devastating effect on reported earnings and book values of the misguided expensing of intangibles by accountants. In essence, if an investment in R&D (patents, products), brands, or IT, is immediately expensed in the income statement, as accounting rules require, the asset, reflecting the investment in these intangibles is missing from the balance sheet and from book value. Accordingly, the price-to-book ratio, which is used by investors to divide stocks into “growth” (glamour) and “value” classes is misspecified. The denominator of the ratio―book value―is missing the most important assets, or value-creators of modern companies. Like Apple without its patents, or Coke without its brands. Since the investment of companies in intangibles is constantly growing, the misspecification of the market-to-book ratio gets worse and worse, and adversely affects the outcome of value investing.

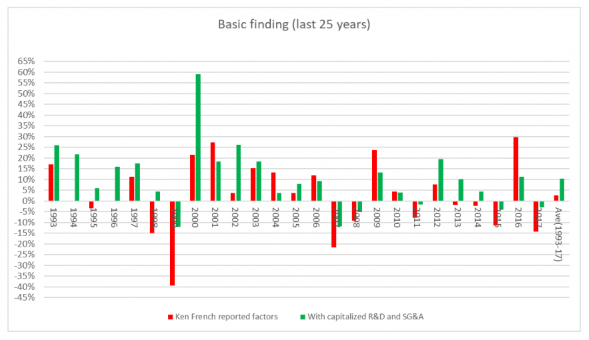

And that’s exactly what our research shows. In the first phase of the research we undo what accountants do: Rather than expensing R&D and SG&A (sales, general, and administrative expenses, which include many intangible investments, such as IT, brands, systems consulting), we capitalize these investments. Full capitalization and amortization of R&D, and half of SG&A. (1) We then adjust the book value of all firms by adding the capitalized values of R&D and SG&A to the reported values, and recalculate the market-to-book ratios. We form new portfolios of “value” and “growth” companies, and compute the one-year returns on the value strategy, namely investing in value companies and selling short the growth companies. The results of this analysis, displayed in the figure below, really surprised me.

For every year (1993-2017), the red bar on the left indicates the return on the traditional (using reported book values) value investing, whereas the green bar on the right indicates the return on value investing based on our adjusted book values by intangibles’ capitalization. It is evident that in practically every year, the adjusted return is either higher or less negative than the return based on accounting book values. The average annual return over the past 25 years (right-hand columns) is about 2% for the conventional value investing and 10%! for the adjusted strategy. A substantial difference. Note that these are riskless returns, derived from a hedge (long on value, short on growth) strategy.

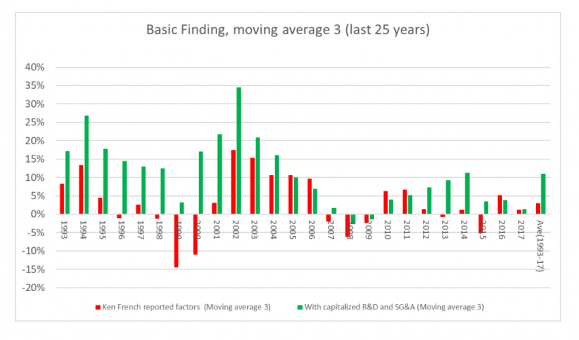

Results are clearer using a 3-year moving average of returns, presented below. The adjusted value strategy clearly dominates in practically every year.

This is only the first stage of our research into the “demise of value.” It is clear that even our adjusted value returns fell in the past 10-12 years, relative to previous years. There is more to the “value story” than accounting deficiencies. Stay tuned.

(1) DETAILS OF OUR CAPITALIZATION PROCEDURES WILL BE PROVIDED IN A FORTHCOMING PAPER.

Baruch Lev is the Philip Bardes Professor of Accounting and Finance at the Stern School of Business, NYU. This article first appeared at the Lev End Of Accounting Blog and is shared here with his permission. Professor Lev is not affiliated with Knowledge Leaders Capital and his opinions are his own.

© Knowledge Leaders Capital

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital