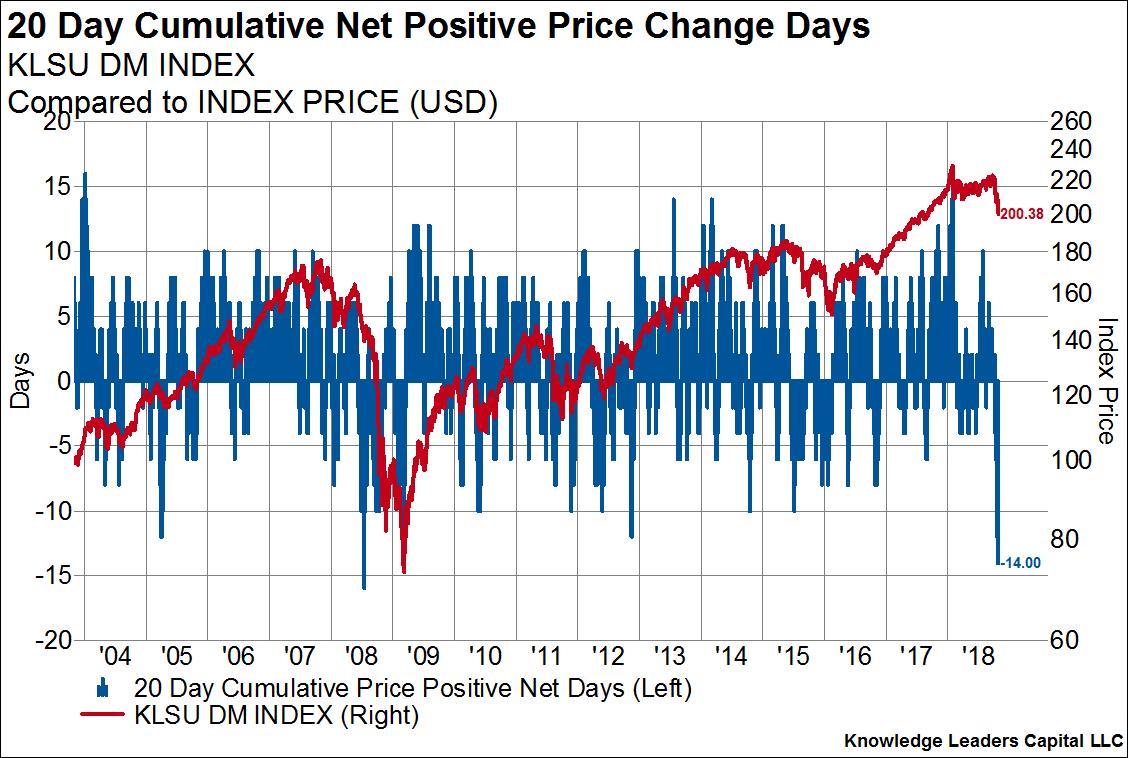

The selling over recent weeks has been fast and intense, providing investors almost no relief. This type of short-term selling pressure has reached fever pitch levels that is usually indicative of some sort of relief rally, even if the ultimate lows are still ahead of us.

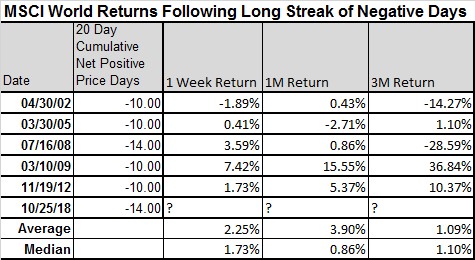

This first chart shows the net number of positive price change days in the market over the trailing month. The current reading of -14, means that the market has been up on only six days over the last 20. There have only been several times over the preceding 15 years in when this indicator fell to -10 or below. In the table below we show the forward 1 week, 1 month and 3 month returns in each of those instances. Returns over the next week and month were skewed strongly positive while longer-term returns were very mixed.

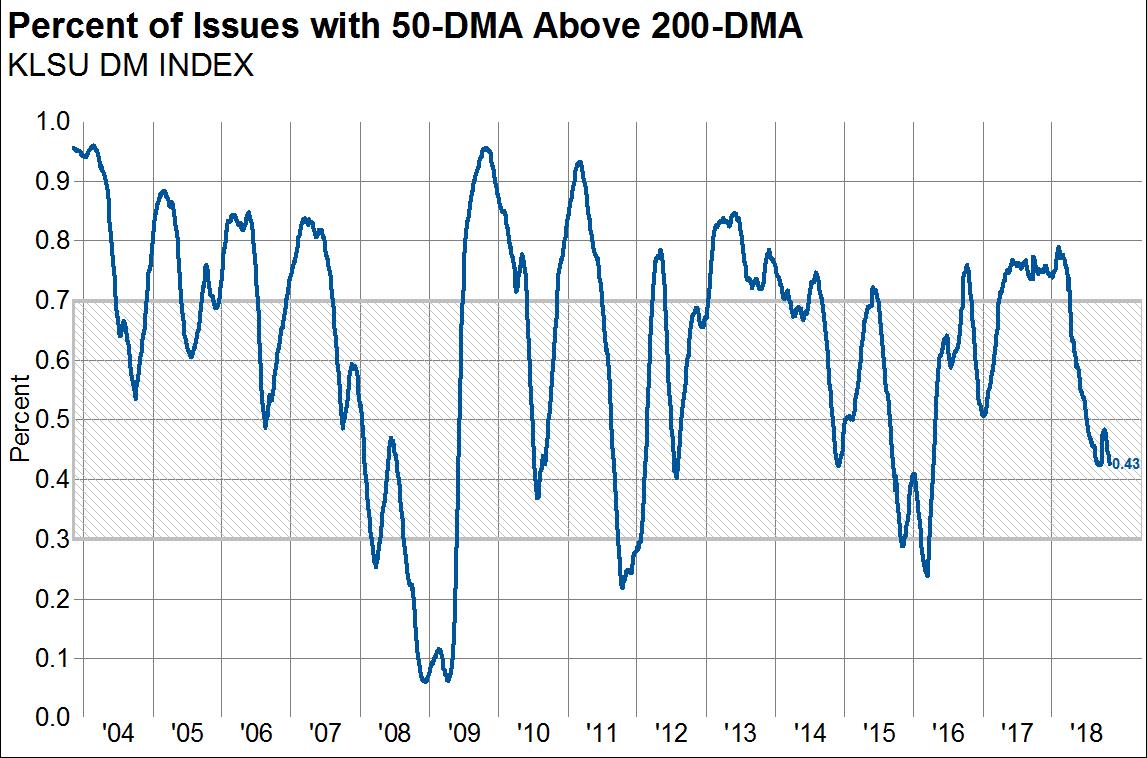

This mixed longer-term picture fits with other data we have showing a lack of extremes, even though the short-term momentum has been bad. For example, the percent of stocks in an uptrend, as measured by those with their 50 day moving average above their 200 day moving average, remains in a no-mans-land level and is far from levels seen at previous good lows. We need to see a complete washout in stocks before a durable rally can take hold, and that would require this ratio to move below the 30% range.