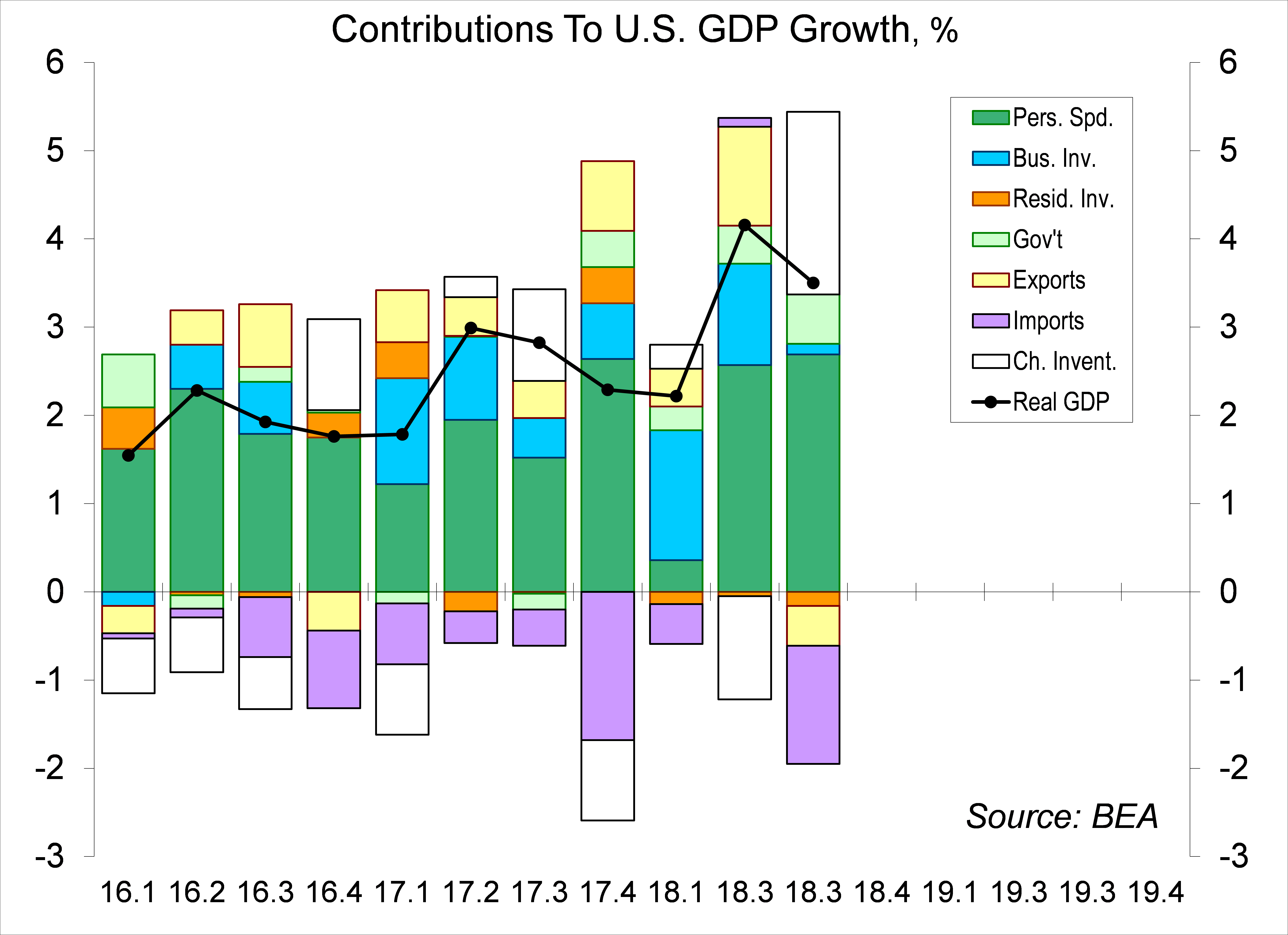

Real GDP rose at a 3.5% annual rate in the advance estimate for 3Q18, about as expected. However, there were a few surprises in the details. Consumer spending growth was even stronger than anticipated. However, business fixed investment was unexpectedly weak. The quarterly swings in inventory growth and net exports were larger than anticipated, likely reflecting the impact of trade policy. For the financial markets, the strong growth figure provided little comfort. Investors are more concerned about the prospects for slower growth in the quarters ahead.

Click here to enlarge

Click here to enlarge

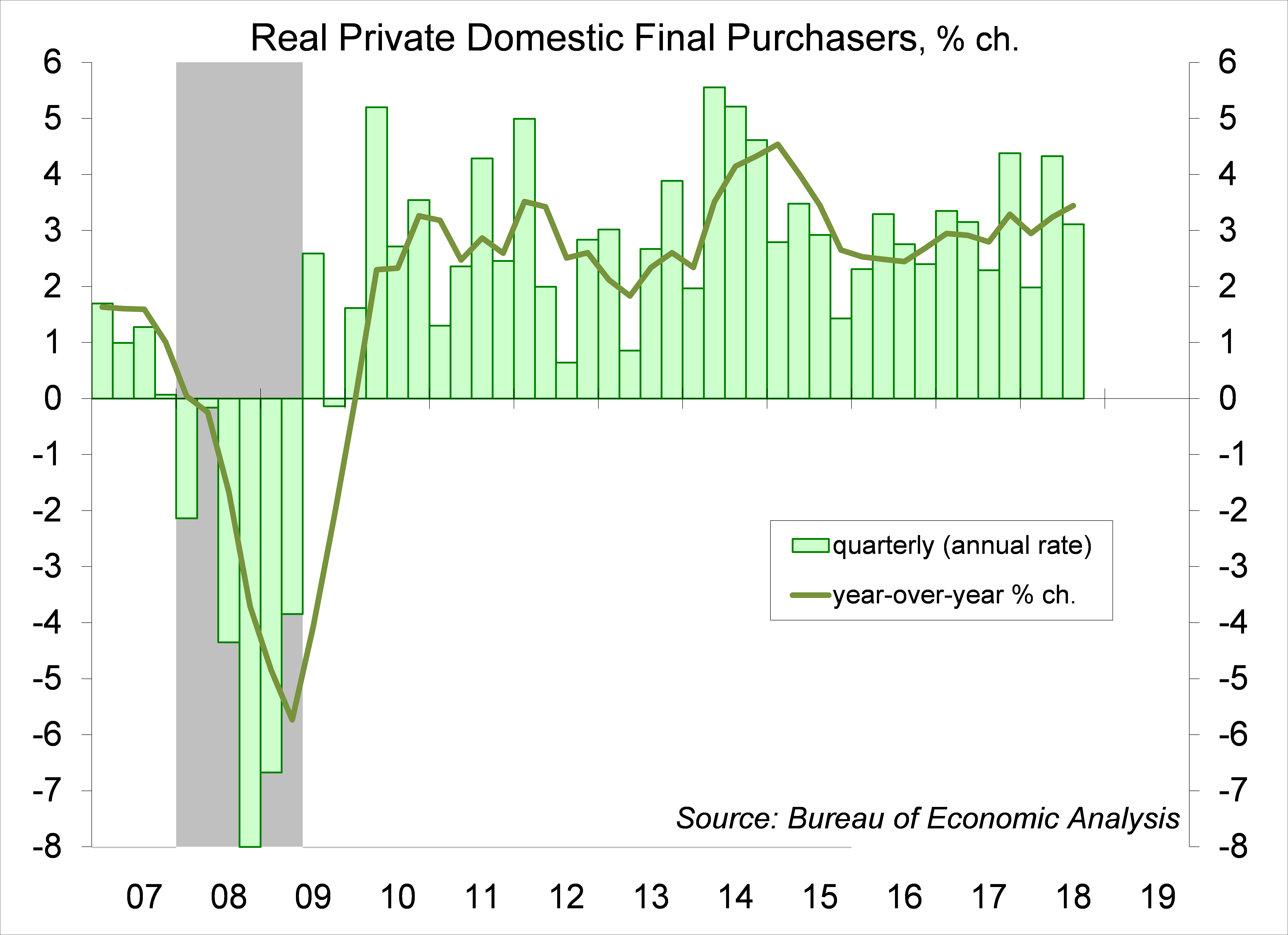

Consumer spending, which accounts for 68% of GDP, rose at a 4.0% annual rate (+3.0% y/y, matching the average pace of the last five years). Business fixed investment rose at a meager 0.8% pace, with weakness in structures (-7.9%), softness in equipment (+0.4%), and strength in intellectual property products (+7.9%). Residential fixed investment fell at a 4.0% pace (+0.4% y/y), following declines in the first two quarters of the year. Together, these three components make up Private Domestic Final Purchases (+3.1%). Government consumption and investment rose 3.3% (+2.4% y/y), adding 0.6 percentage point to overall GDP growth.

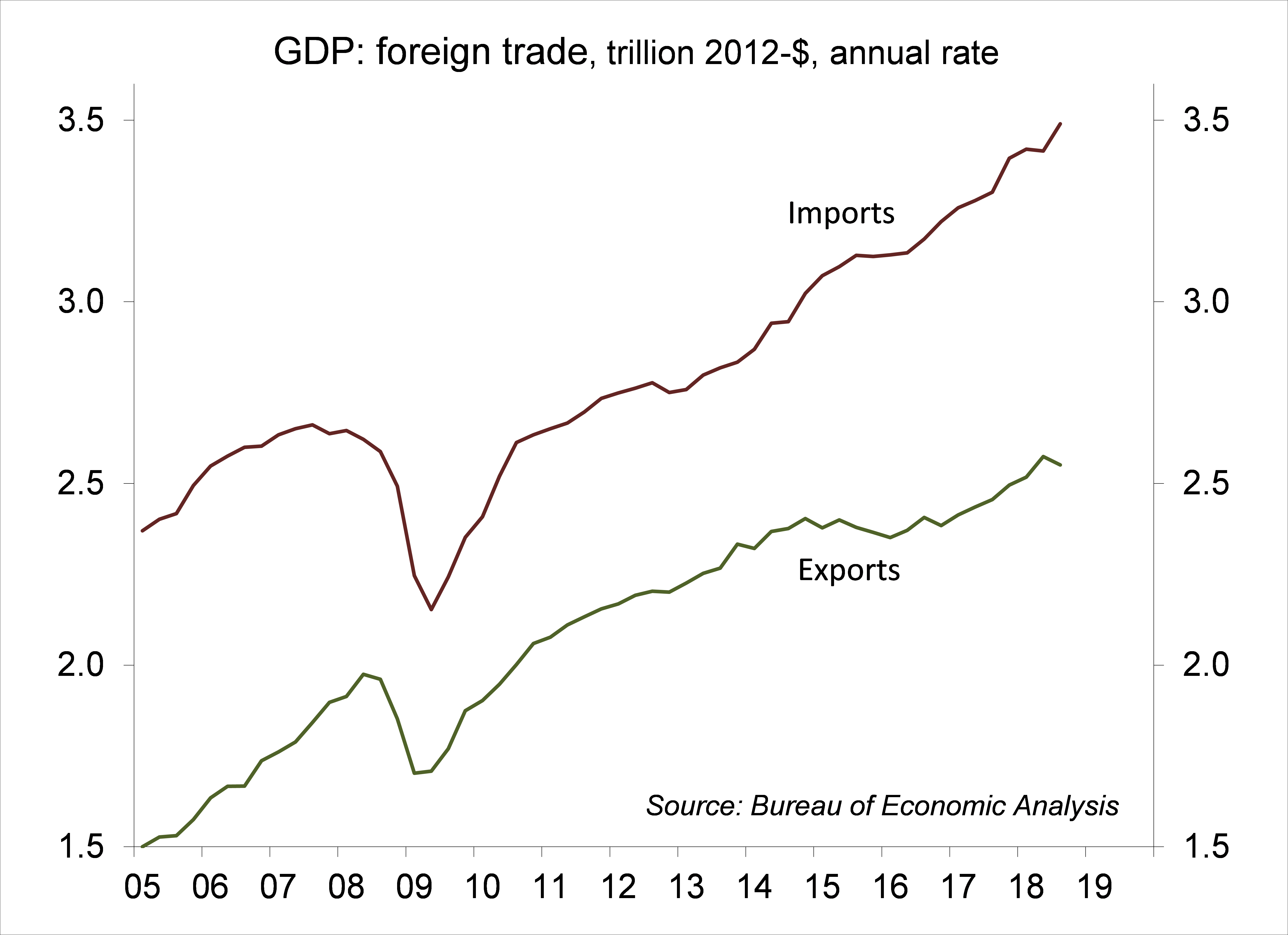

The trade deficit widened in 3Q18, but more than expected, subtracting 1.8 percentage points from GDP growth. A rising trade deficit is a sign of strength in the domestic economy (we consume more domestic goods and more imported goods).

Click here to enlarge

Click here to enlarge

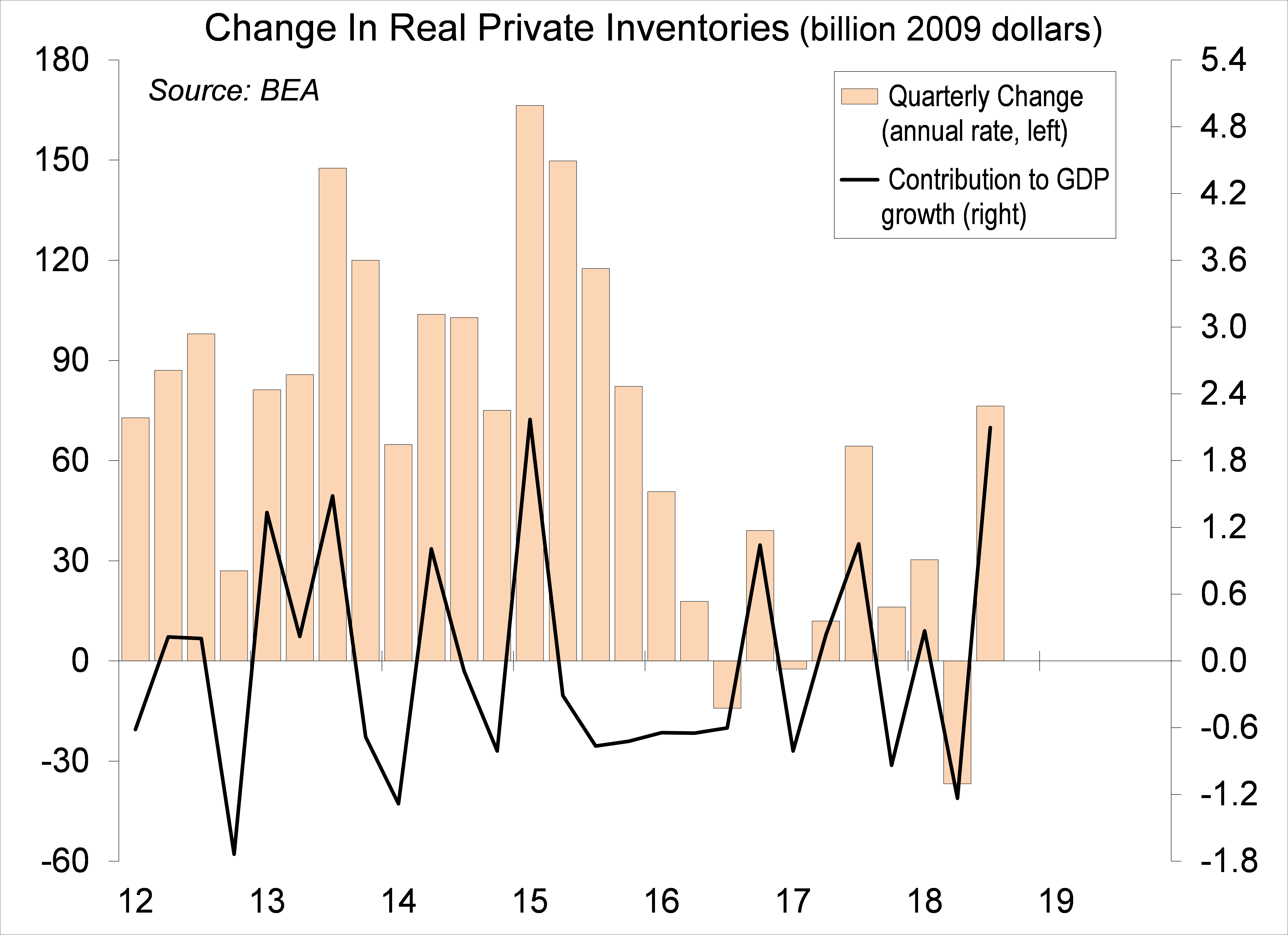

Inventory growth picked up (after slowing in 2Q18), but more than expected, adding 2.1 percentage points to growth. It’s always difficult to say whether faster inventory growth is due to disappointing sales results or optimism regarding future sales. However, in this case, there was likely a stockpiling of inventories in anticipation of tariffs. That is also likely reflected in the wider trade deficit.

Whether trade policy disruptions unwind or grow worse will depend on whatever progress we see in trade talks with China (and that’s not looking good so far). Consumer spending has been driven by job growth and (to a lesser extent) wage gains, but the pace should slow as job market constraints become more binding, leading to slower GDP growth in 2019.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James