A GDP Report That Screams Trade Wars and Government Spending

Third quarter real GDP came in at a 3.5% QoQ annualized rate for the third quarter, above expectations for a 3.3% growth rate. The growth rate itself wasn’t much of a surprise, and frankly, neither were the drivers of growth. But, the report is reminder of a GDP report that was, to some extent, manufactured by trade war concerns and late cycle fiscal stimulus.

In the first chart below we show the components of QoQ annualized GDP growth for the last two years. We see that in the most recent quarter personal consumption (grey column), inventories (dark blue column) and government consumption (black column) all added to GDP growth while trade (light blue column) and fixed investment (red column) both subtracted from growth.

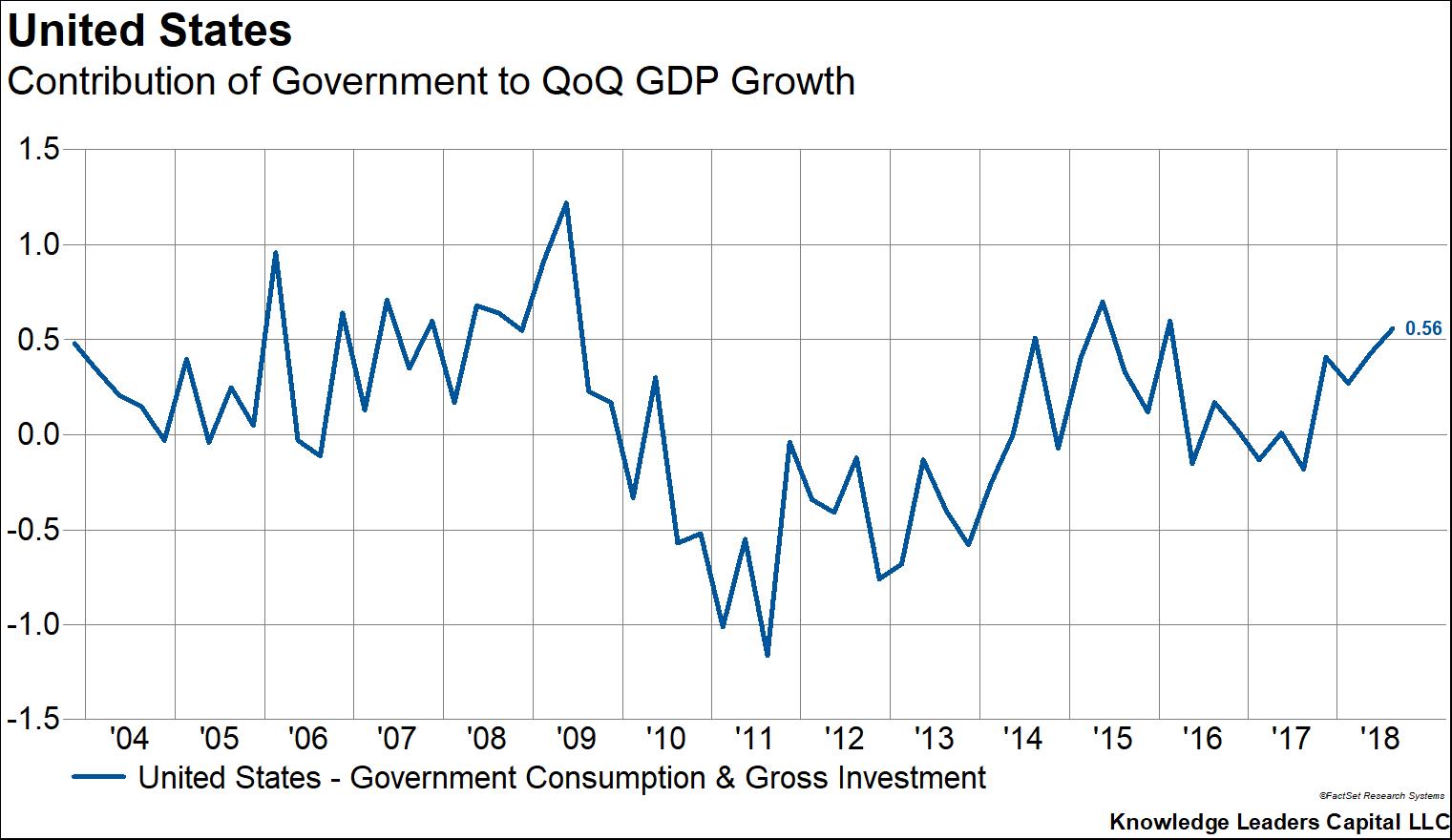

In deconstructing GDP growth, we observe that trade was unusually weak (imports outpaced exports by a wide margin) and inventory growth was unusually strong. Inventories often flip from being a drag on growth to adding to growth whereas trade is typically a small to moderate drag on growth. Both inventories and trade were affected by domestic companies bringing forward imports to avoid higher duties once tariffs on half of Chinese imports rise to 25% at the end of the year. We also observe government spending adding .56% to GDP growth, consistent with the rate of change in fiscal stimulus peaking right about now.

The next chart shows the contribution of inventories to GDP growth going back 15 years. As we can see, inventories added the most to GDP since 1Q15, 4Q11 and 4Q09. In contrast to today, growth was recovering from weak quarters in each of those instances. In none of those instances did inventory builds continue.