On My Radar: A Painful Week for Global Equities and Fixed Income; The 3.07% Line in the Sand is Cros

Learn more about this firmMembership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“I want to reiterate my headline: managing debt crises is all about spreading out the pain of the bad debts,

and this can almost always be done well if one’s debts are in one’s own currency.

The biggest risks are typically not from the debts themselves,

but from the failure of policy makers to do the right things due to a lack of knowledge and/or lack of authority.

If a nation’s debts are in a foreign currency, much more difficult choices have to be made to handle the situation well—

and, in any case, the consequences will be more painful.”

– Ray Dalio, A Template for Understanding Big Debt Crises

Asset price inflation (check). Financed by debt growth (check). We’ve spent the last three weeks reviewing Ray Dalio’s A Template for Understanding Big Debt Crises. I hope you found the insights as helpful as I did. Invaluable research for understanding how economies work, how they cycle, how short-term business cycles turn into long-term debt cycles, where we sit in the cycle today and what it means for our tomorrow. It is an extensive study of history, behavioral tendencies and a blueprint for policy makers and you and me to better navigate the challenges on the path ahead. We sit at the end of a long-term debt super-cycle.

The debt challenges will be resolved and, as deep into a state of depression we might choose to send ourselves, let’s not go there, stay positive and know we’ll all be fine. Though some of us will do better than others. It depends on how the path progresses, how policy makers and central bankers take action and how we position our portfolios. In the investment game, it’s about being on the right side of the trend.

I’m pulling for a beautiful deleveraging, but see an ugly as a probable outcome. Either way, as we witnessed this past week, it will be bumpy.

Ok, let’s step forward. The plan this week was for me to share my dashboard of indicators and talk about a few speculative bets to consider. Let’s put that on hold until next week and instead talk about the action in the markets this past week. And what a week it’s been. I’ll start with what I believe is the most significant event.

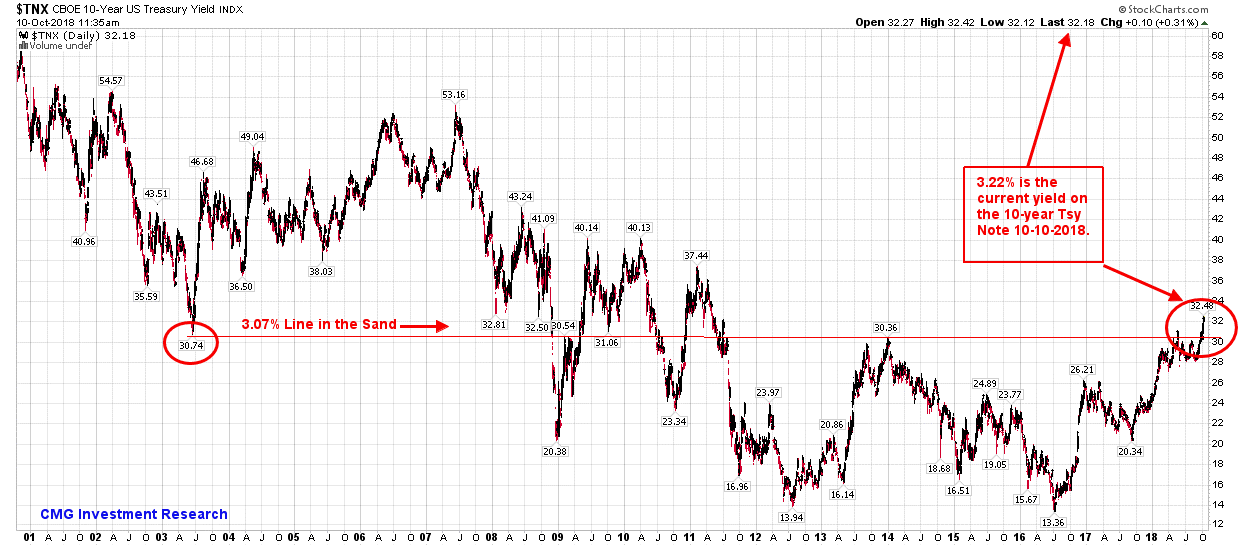

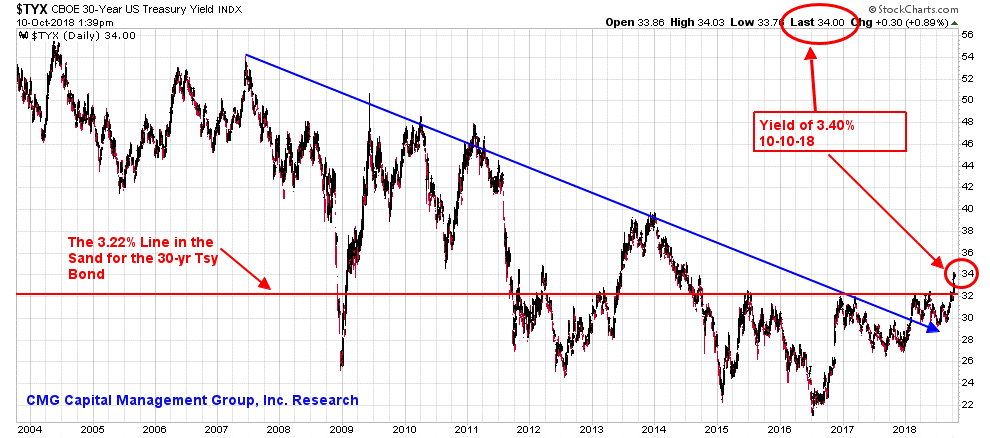

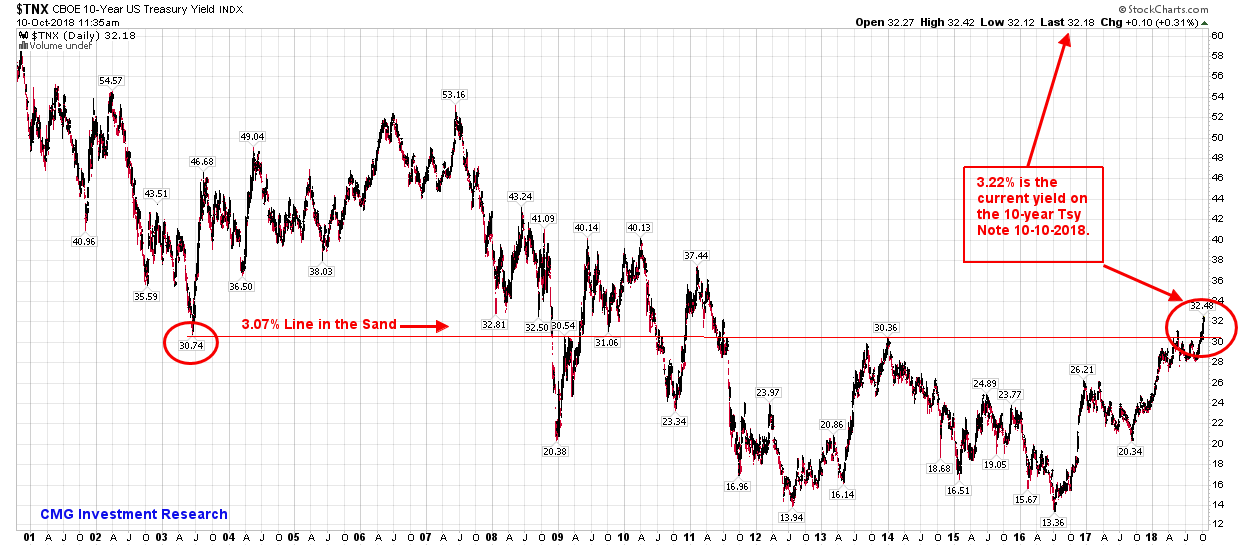

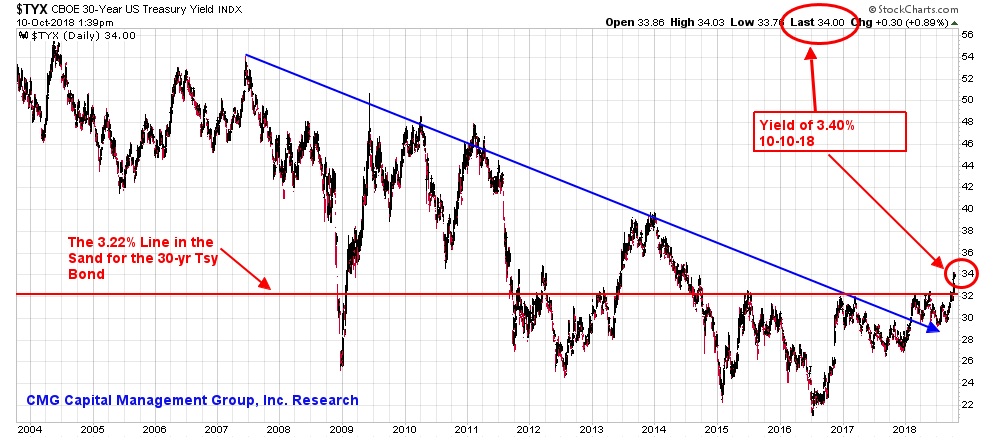

The Line in the Sand: 10-year Treasury Note 3.07%, 30-year Treasury Bond 3.22% (yields broke higher)

I’ve been writing for several months that the “Line in the Sand” for the yield on the 10-year Treasury Note was 3.07% and the tipping point for the 30-year Treasury Bond was 3.22%. Suggesting that a move above those markers would see a spike in rates and tumult in the markets. This past week, both lines were breached. The 10-year Treasury yield rose decisively above 3.07% and the 30-year above 3.22%.

Here is the 10-year Treasury – I posted this chart in Trade Signals on Wednesday.

- Note the red arrows. Note the straight red horizontal line. That marks the “Line in the Sand,” which is an important technical level at 3.07% on the 10-year. The Fed looks to be on path to raise rates “gradually” another four times. The next technical target for yields is 3.55% with more significant resistance between 3.80% and 4%. When rates go up, bond prices go down. As I said above, I believe we are on our way to 4%.

Here is a look at the 30-year Treasury bond yield:

Global equity markets fell hard. Both bonds and stocks declined together. The S&P 500 Index lost nearly 7% in a few short days. The DJIA opened up 400 points higher this morning and by 12:45 pm, the index turned negative. The markets are experiencing the worst rout since February. To give you some footing on year-to-date returns through yesterday, this from Pension Partners:

The “Greenspan Put” is Sidelined for Now

From Wikipedia: “The ‘Greenspan Put’ refers to the monetary policy approach that Alan Greenspan, the former Chairman of the United States Federal Reserve Board, and other Fed members exercised from late 1987 to 2000.” In English, the Fed led by Greenspan, Bernanke and Yellen would step in to protect the market with words (to support/provide confidence to investors), actions (like lowering interest rates/providing liquidity) and even, dare I say, selective buying in the equity futures market.

An important observation I’d like to share is there’s a new sheriff in town. Well, actually two new sheriffs. We are at a different stage in the cycle with different playmakers calling the shots. There will be no Powell Put forthcoming. Equity market stress will not deter the Fed from raising rates. There will be no Trump Put forthcoming. Equity market stress will not force Trump and his administration into a softer trade policy stance, especially towards China. Higher growth, lower unemployment gives the Fed room to stay on the gradual rate hike path.

“The economy is strong, [so] rates are going up,” [Jamie] Dimon said. “Most of us consider it a healthy normalization and going back to more of a free market when it comes to asset pricing and interest rates, etc. And we need that. So to me overall it’s a good thing, particularly if the economy is strong. We have a let free markets be free environment. Expect higher rates, expect more volatility.”

The Street expects a 1% (a quarter at a time) move from here. Jamie Dimon sees 4% in our near future. I agree.

Further on this point, this week the Fed’s John Williams said:

Moving Toward ‘Normal’ U.S. Monetary Policy

My view on the U.S. economy is well summarized by the most recent FOMC statement, in which variations on the word “strong” appeared five times in describing the U.S. economy… I expect the unemployment rate to edge down to slightly below 3.5 percent next year, the lowest level in nearly 50 years… I expect price inflation to move up a bit above 2 percent…

We are nearing the end of the process of normalizing monetary policy and are inching closer to conducting normal monetary policy… It makes sense to shift away from a focus on normalizing the stance of monetary policy relative to some benchmark “neutral” interest rate, often referred to as “r-star.”… r-star is just one factor affecting our decisions, alongside economic and labor market indicators, wage and price inflation, global developments, financial conditions, the risks to the outlook… the list goes on and on…

The most important issue in my mind is rising rates and what that means to the mountain of debt here, there and everywhere. To me, a sovereign debt crisis remains the predominant global systemic risk. In progression it looks like this: Emerging market countries with large debts financed in dollars likely fail first, followed by Europe, followed by Japan with the U.S., the cleanest shirt in the dirty debt laundry pile, the last debt reset domino to fall. It won’t play out in days. My best guess is that rising rates and a rising dollar are the likely trigger that sets the sovereign debt wave in motion. It will play out over several years, as policy makers first scramble then ultimately come together to figure it out. There will be winners and there will be losers.

As Dalio noted, “Typically the worst debt bubbles are not accompanied by high and rising inflation, but by asset price inflation financed by debt growth. That is because central banks make the mistake of accommodating debt growth because they are focused on inflation and/or growth—not on debt growth, the asset inflations they are producing, and whether or not debts will produce the incomes required to service them.”

Asset price inflation (check). Financed by debt growth (check).

I was asked if I think inflation is the issue that will keep the Fed on path. I believe that the asset bubble is the more concerning issue to the Fed. I was also asked if the top of the stock market is in. I don’t know and I don’t see that evidence in my Trade Signals indicators nor my recession indicators. So I don’t think so. I view today similar to where we were in early 2007 or early 1999. Then, excesses were just as clear as they are today yet there was more run in the run back then. That may be the same today.

My advice to my advisor friend was to keep reducing equity exposure on rallies and adding more and more to diversified trading strategies. An October 2018 crash? Maybe, but probabilities are low. I see this reset playing out over years, not days. I recommend a “participate and protect” stop-loss risk management process investment game plan put in place on everything you own. A rules-based way to get you out and back in.

When you click through, you’ll find a few more thoughts from Jamie Dimon’s shareholder meeting. And I share with you a quick review of this week’s Felix Zulauf’s Barron’s interview. For years Zulauf was on the Barron’s Roundtable. He’s exceptional. You’ll find my notes and a link to the full Barron’s article. Please know his views are his and not a recommendation by me to buy or sell any security. I have no idea of your goals, needs, risk suitability and time horizon. Side bar: coincidentally, John Mauldin called me to let me know Zulauf is going to be a keynote speaker at the next Mauldin Economics Strategic Investment Conference in May 2019. I love when that happens. “Way cool,” as my kids used to say! Or maybe that was me trying to act cool to them. Dad forgets.

Grab that coffee and find your favorite chair. You’ll find the balance of the post to be a quick read. When you get to the Trade Signals section, there is a link there that will take you to the market dashboard I post each week. I go through the drill each week because it helps me to keep my footing and stay disciplined. I hope you find it useful as well. You’ll see that the overall trend for U.S. equity markets remains bullish and the trend for high quality bonds remains bearish. Worth mentioning is the HY trade signal I’ve used since the early 1990s moved to a sell signal a week ago and bears watching. HY is a great leading indicator for equities and recessions.

Included in this week’s On My Radar:

- Jamie Dimon – Notes from October 12, 2018 Investor Call

- Barron’s – “The Markets are a Jungle. Good Thing Felix Zulauf Is Your Guide”

- Trade Signals – The 3.07% Line in the Sand is Crossed; Expect Bumps

Jamie Dimon – Notes from October 12, 2018 Investor Call

- “The economy is still very strong, and that’s across wages, job creation, capital expenditure, consumer credit; it’s pretty broad-based and it’s not going to be diminished immediately,” Dimon said.

- While rising rates amid a strong economy are good, they could eventually put a halt to the nearly decade-long economic growth cycle, he said.

- “If rates go up because you have inflation, that is not a plus. That is a bad thing,” Dimon said. “So far, we still have a strong economy in spite of these increasing overseas geopolitical issues bursting all over the place.”

- When asked to name these issues, Dimon rattled off a list that included the Trump administration’s trade dispute with China, Brexit, the unwinding of bond-purchasing programs by central banks around the world, as well as flare-ups across Europe, the Middle East and Latin America including in Italy and Turkey.

- “It’s an extensive list of stuff,” Dimon said, adding that most of the times, it’s rising rates and not geopolitical issues that ends up derailing economic cycles. “I’m just pointing that out. No one should be surprised if it happens down the road.”

Source: CNBC

Barron’s – “The Markets Are a Jungle. Good Thing Felix Zulauf Is Your Guide”

Article by Lauren R. Rublin, October 5, 2018

Felix Zulauf was a member of the Barron’s Roundtable for about 30 years, until relinquishing his seat at our annual investment gathering in 2017. While his predictions were more right than wrong, it was the breadth of his knowledge and the depth of his analysis of global markets that won him devoted fans among his Roundtable peers, the crew at Barron’s, and beyond. Simply put, Felix, president of Zulauf Asset Management in Baar, Switzerland, always knew—and still knows—better than most how to connect the dots among central bankers’ actions, fiscal policies, currency gyrations, geopolitics, and the price of assets, hard and soft.

With interest rates rising, governments in flux, and the world’s two biggest economies facing off over trade, it seemed the right time to ask him how today’s turmoil will impact investors in the year ahead. Ever gracious, he shared his thoughts and best investment bets in an interview this past week.

SB here: Following is a selection of what I feel are the most important takeaways from the interview. The bold is mine.

-

- Zulauf believes we have left the world of free markets and entered the world of managed economies and said this is a major change in in his lifetime.

- Central banks took over the running of economic policy after the financial crisis and run the show to this day.

- He also said the move to globalization is now moving backwards and moving to regional economic and trade partnerships, which could create problems for multinational companies.

- The past 30 years saw the biggest globalization process ever, with the integration of China into the world economy. With today’s trade conflict, that is changing.

- He believes, the Northeast Asia economic model isn’t compatible with the Western model.

- In the West, corporations are run for profit. In Northeast Asia, exports have been used to increase employment, income, and market share. In China, average export prices have been unchanged in U.S. dollar terms for the past 15 years, whereas the average wage has gone up six times. A company with such statistics goes bankrupt, but China has escaped that outcome through the use of debt.

- He believes the World Trade Organization should have sanctioned China for applying unfair trade practices, but didn’t. And added, Presidents Clinton, Bush, and Obama, and the Europeans, were asleep. President Trump has taken up the issue, as he was elected to do. Middle-class incomes in the U.S. and many European countries have been unchanged or down for the past 30 years in purchasing-power terms, while middle-class incomes in China and its satellite economies have risen tremendously.

- He expects the China trade conflict to continue. 25% tariffs on everything within 12 months. Concluding, the Chinese will lose a few trade battles, but eventually win the war.

-

-

More on China:

- China will build up its strategic partnerships around Asia, keep expanding in Africa, and try to convince Europe to join its trading bloc. If the U.S. continues to take an aggressive stance, it runs the risk of becoming isolated.

- He’s looking out next six or seven years. A trade war might protect U.S. industries for a while, but protectionism weakens industries and economies.

- He said, at present, the world economy is desynchronized.

- The U.S. economy is on steroids due to tax cuts and government spending and growing above trend.

- China is in a pronounced slowdown that could continue until the middle of next year, at least. The Chinese agenda is to have a strong economy in 2021, the 100th anniversary of the founding of the Communist Party of China, and 2022, the year of the next National Congress.

- That is why China started to address major problems, such as pollution and financial excesses, in 2017. Cleaning things up led to a slowdown that could intensify in coming months as U.S. tariffs increase.

-

This totally got my attention:

- China will launch another fiscal stimulus program, supported by monetary stimulus.

- When it does, the currency will fall 15% or 20%. The Chinese will let the currency go because they know they can’t please President Trump on trade. They aren’t prepared to do what he’s asking for.

- We’ll also see fiscal stimulus applied in emerging markets, which are largely dependent on China, and in Europe and maybe the U.S., where President Trump will launch a spending program to boost the economy ahead of the 2020 election.

-

Bad for bonds – a decisive bear market in bonds

- Global fiscal stimulus initiatives are poison for bond markets. Bond yields are rising around the world. After major new fiscal stimulus programs are announced, perhaps from mid-2019 onward, yields will rise quickly, resulting in a decisive bear market in bonds.

-

More on China:

-

-

On the Euro – Right on point! Watch the banks!

- Introducing the euro led to forced centralization of the political organization, as imbalances created by the monetary union must be rebalanced through a centralized system. As nations have different needs, the people are revolting; established parties are in decisive decline, and anti-establishment organizations are rising.

- The risk of a hard Brexit is high. Italy doesn’t listen to Brussels any longer. The March election brought anti-establishment parties to power that proposed a budget with a 2.4% deficit target. Eventually it will be closer to 4%. The Italian banking system holds €350 billion of government bonds. If 10-year government-bond yields hit 4%, banks’ equity capital will just about equal their nonperforming loans.

- By the middle of next year, you’ll see more fiscal stimulation in Germany, Italy, France, and possibly Spain. Governments will not care about the EU’s directives. The EU will have to change, giving more sovereignty to individual nations. If Brussels remains dogmatic, the EU eventually will break apart.

-

The European Central Bank

- ECB quantitative easing ends by the end of this year. The economy has been doing well, the inflation rate has risen, and yet the ECB has continued with aggressive monetary easing, primarily financing the weak governments. This is nonsense.

- They are the worst-run central bank in the world. I expect the euro to weaken further, possibly to $1.06 from a current $1.15.

-

The U.S. Fed

- The Federal Reserve is draining liquidity from the financial system [by not buying new bonds to replace maturing paper]. It will remove another $600 billion from the market in the next year.

- The Treasury will issue $1.3 trillion of Treasury paper to finance the budget deficit.

- All of this means a lot of liquidity is being withdrawn from the market, which is bearish for financial assets.

- He expects U.S. stocks to slide into the middle of next year, falling maybe 25% to 30% from the top, taking nearly all other markets down with them.

-

On the Euro – Right on point! Watch the banks!

Trade Signals – The 3.07% Line in the Sand is Crossed; Expect Bumps

S&P 500 Index — 2,840 (10-10-2018)

Interest rates are moving higher and the stock market is under pressure. For months, I’ve been suggesting the “Line in the Sand” for the 10-year Treasury is 3.07%. That important technical threshold was breached last week. Rates are heading higher. I believe we are on our way to 4%. That’s bad news for high quality, long duration bonds, bond funds and ETFs.

Following is the updated chart:

- Note the red arrows. Note the straight red horizontal line. That marks the “Line in the Sand,” which is an important technical level at 3.07% on the 10-year. The Fed looks to be on path to raise rates “gradually” another four times. The next technical target for yields is 3.55% with more significant resistance between 3.80% and 4%. When rates go up, bond prices go down. As I said above, I believe we are on our way to 4%. I’ll be talking about what that means to the debt load in Friday’s OMR. Hint: When 25% of your budget is spent to cover your interest costs and the interest rate on your debt moves up, you pay more. Stay tuned. Expect bumps.

Here is a look at the 30-year Treasury bond yield:

The equity market trend evidence remains modestly bullish. The Ned Davis Research CMG Large Cap Long/Flat Index remains in a buy. The Zweig Bond Model remains in a sell.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is a general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purpose.

In a rising interest rate environment, the value of fixed income securities generally declines and conversely, in a falling interest rate environment, the value of fixed income securities generally increases. High-yield securities may be subject to heightened market, interest rate or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Captial Management Group

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits