Is last week’s 18 basis point selloff in 10 year government bonds the start of a bond bear market or a market adjusting to the realities of the time, albeit in a somewhat disorderly way? The answer to this question has obvious implications for not just bonds, but all asset classes from equities to commodities to real estate. After all, the cost of capital is like a magic number that informs the value of all financial assets. If long-term rates are set to explode higher a-la 1994, then bond and equity investors alike need to be careful.

When trying to understand the recent move in bonds, it’s helpful to measure the movement of each component of the bond: real growth expectations, break even inflation, and the term premium. The 18 basis point move was driven by the term premium rising by +18bps, a +1bps point rise in inflation expectations and a -1 basis point decrease in real growth expectations. That is, there was practically no alteration of either inflation expectations or growth expectations, and nearly the entire sell off was driven by the term premium.

What, then, does the term premium measure exactly? In our world of bloated central bank balance sheets, the term premium is both a reflection easy money policies as well as a measure of an unexpected growth or inflation shocks permeating the economy over the term of the bond. Therefore, last week’s selloff could be a caused by an expectation of a more normal Fed policy stance over the long-term and/or a reflection of something that materially changed causing investors to need more compensation for holding longer term treasuries. Included in major news items in the last week or so were a Fed meeting, some PMIs suggesting higher input prices, a decent employment report, and an escalation of the trade confrontation with China. Of these, only the first and fourth strike us as actual market moving news. So, explaining the move in term premiums may be the result of the bond market coming to terms with policy normalization with a bit of tariff fears mixed in. Since trade policy is so hard to discount, we’ll focus on Fed policy.

On the policy normalization front, it’s useful to think of the 10 year treasury bond yield as the sum of the expected future short-term rates. If expectations for short-term rates move up, the 10 year yield itself will reflect those changes by moving higher too. In the Fed’s most recent statement and dot plot, policy for rate hikes and balance sheet runoff were reiterated. It’s just that the market has been tracking below where the Fed itself is saying what policy rates will be. In other words, the market has been taking the under on Fed policy rates. We can clearly see this in the chart below, where the green line is the median Fed member’s rate expectation, the white line is the market’s current expectations for Fed funds rates, and the blue line was the market’s expectations for Fed funds rates before the most recent meeting. Before the most recent meeting, the market was pricing in only two rate hikes for 2019 versus the Fed telling us that they are expecting more like three hikes. Over the last week, the market has moved a lot closer to expected Fed policy, and this has caused the longer-dated bond yields to rise via the term premium.

But just how much more does the 10-year need to rise to reflect Fed policy expectations? Very short-term rates could rise a little further, but longer-term rates are about reflecting the terminal Fed funds rate for this cycle. That is, the market could fully discount the Fed’s dot plot via curve flattening. As previously stated, the 10 year treasury bond yield is just the sum of the expected future short-term rates. At the end of the rate hiking cycle, those expectations should configure themselves such that the 10 year bond equals the terminal Fed funds rate. The median Fed member’s terminal Fed funds rate is currently 3.375%, just 17bps higher than the current 10 year treasury yield. The weighted average Fed member’s terminal Fed funds rate is 3.28%, just a few basis points higher than the current rate. This tells is that the rise in yields may be closer to its end than its start, but there is still a little to go to completely discount Fed policy, especially on the short end of the curve.

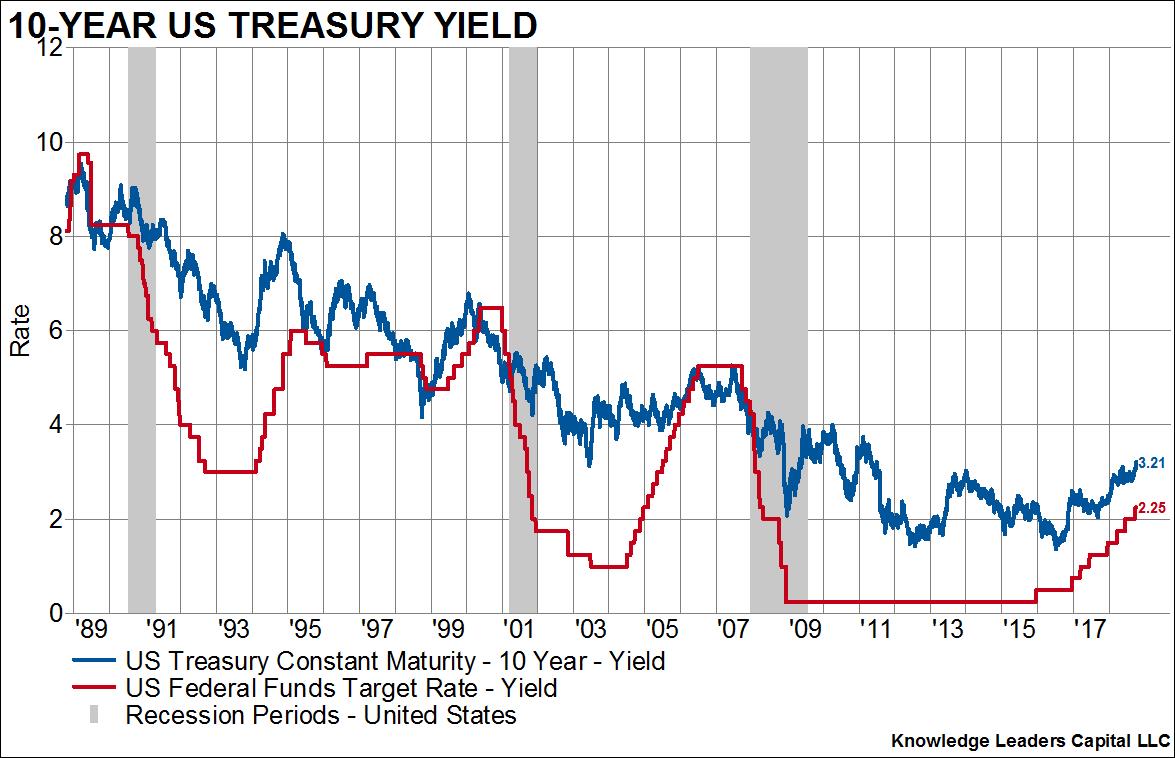

In the next chart below, it’s easy to see how the 10 year bond tracks the Fed funds rate and eventually meets it at the end of the rate cycle…usually. One major exception was in 1994 when long rates shot up due to the expectation of a much more hawkish Fed and as a result of too much leverage in the bond market. Even in 1994, it didn’t take that long for gravity to reassert itself on rates.

Technicals also don’t support a continued selloff in bonds. Traders are currently positioned net short of the 1o year bond by the largest amount since 2004. Extreme trader positioning is always unwound, it’s just a matter of when, and usually takes the underlying with it during the unwind. In this case an unwind would mean covering of short positions and lower rates.

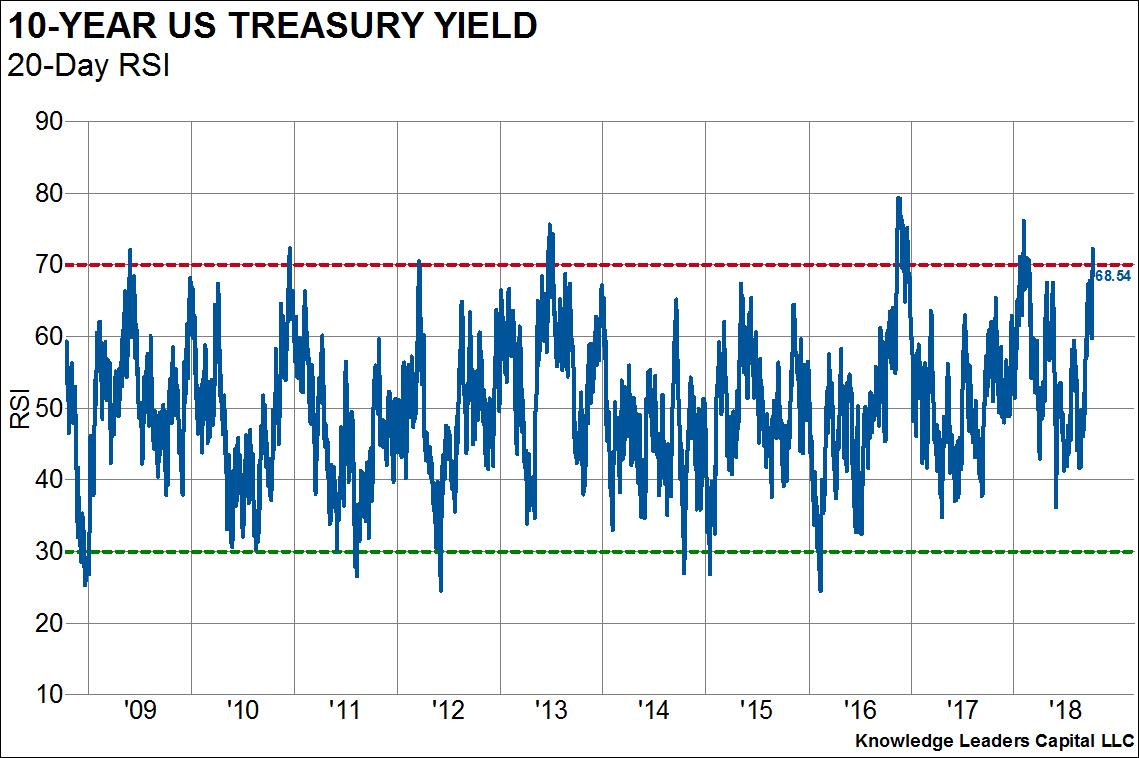

Finally, the 10 year bond is one standard deviation oversold on a relative strength index, a measure of the movement of an instrument relative to its previous levels. The RSI doesn’t tell us that the move higher in rates is over, just that the extremeness of the move we’ve seen over the last week probably will not be repeated over and over in the near future.

Bond yields have moved up, but we doubt this is the start of a major rerating of the bond market. For one, growth and inflation expectations have remained stable, leaving all of the rise in yields to be explained by the term premium. The term premium reflects to a great degree Fed policy expectations. As the market has moved closer to fully discounting Fed policy, the 10 year rate has moved higher. But now the 10 year rate is very near to the Fed funds terminal rate for this cycle. This implies that long rates may not need to move much more to fully discount Fed policy, but that shorter-term rates may need to move a bit higher still, flattening the curve a bit. Technicals also don’t support an extreme move higher from here. Trader positioning is already near record short of long bonds and shorter-term measures of price movements are at extremes too.

© Knowledge Leaders Capital

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital