1. August Jobs Report Was a Pleasant Surprise… Except

2. The Fed’s Ideal Plan For Normalizing Interest Rates

3. Fed Might Accelerate Rate Hikes in 2019, Stall Economy

4. Fed to Continue Hiking Rates Until Something Breaks

Overview

In light of last Friday’s better than expected jobs report for August, the odds are near 100% that the Fed will hike short-term interest rates by another 25 basis points at its next policy meeting near the end of this month. Odds are also high that there will be another 0.25% hike at the December Fed policy meeting. Until recently, it has been widely expected that the Fed will hike 2-3 more times in 2019, but that view may be changing.

Many Fed-watchers believe a majority of members on the Fed Open Market Committee would like to see the Fed Funds rate end-up about 2% higher than it is today (currently 1.75%-2.00%). As a result, many Fed-watchers are starting to worry that the Fed will accelerate its rate hikes next year and risk a slowdown in the economy. Some believe the Fed could hike rates 4-5 times in 2019, and that would be bad for the economy.

I think this assumption of 4-5 rate hikes or more next year is premature. Part of the reason is that no one, not even the Fed, knows when the next recession will arrive. Plus, President Trump has been critical of the Fed for raising rates, so I doubt the Fed would accelerate its pace of rate hikes for next year. I could be wrong, of course, so that’s what we’ll talk about today.

August Jobs Report Was a Pleasant Surprise… Except

Last Friday’s unemployment report for August was a pleasant surprise in that the economy created 201,000 new jobs last month, well above the pre-report consensus. The initial August jobs estimate has a history of coming in well below expectations, and then gets revised higher in subsequent months. This time, it was considerably better than expected.

On the wage front, the report was also better than expected. Wages rose by a faster-than-expected 2.9% (annual rate) for blue-collar and low-wage workers, the fastest pace in nine years. Meanwhile, on Thursday of last week, the government reported that jobless claims for unemployment benefits fell to 203,000 in August, the lowest level in 49 years.

Yet Friday’s jobs report was not a pleasant surprise if you are one of those who increasingly worry that the Fed will go too far in raising interest rates next year and choke off this booming economy. It’s happened plenty of times before as I’ll discuss below.

As a reminder, the Fed feels compelled to “normalize” (i.e. – raise) short-term interest rates to higher levels so as to be able to cut them once again whenever the next recession arrives. Keep that in mind as we go along today.

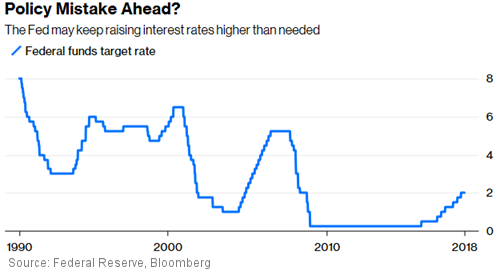

The Fed’s Ideal Plan For Normalizing Interest Rates

The next Fed Open Market Committee (FOMC) meeting is on September 25-26 when the odds are near 100% that the members will vote to hike the Fed Funds rate from 1.75%-2.00% to 2.00%-2.25%. There continues to be high confidence the FOMC will hike by another 25 basis points at the last meeting of this year on December 18-19. And the Fed has suggested more rate hikes in 2019 and possibly 2020.

While the FOMC hasn’t said so specifically, most Fed-watchers believe a majority of members on the Committee wants to see the Fed Funds rate end-up about 2% higher than it is today (currently 1.75%-2.00%). If true, and I believe it probably is, that would put the Fed Funds rate range at 3.75%-4.00% in 2020.

The problem is, the Fed may not have until late 2020 to end its rate hiking cycle to get ready for the next recession. They hope they have that long but also know that the next recession could arrive well before their preferred normalization schedule plays out. Whenever the next recession arrives, the Fed will stop hiking interest rates.

Fed Might Increase Rate Hikes in 2019, Stall Economy

There is growing concern in the financial markets that the Fed might feel compelled to increase the number of rate hikes next year out of fear that a recession may begin to unfold in late 2019 or early 2020 – before they reach their Fund Funds rate target.

I have to say at this point that such fears are largely driven by the media which hates Trump and virtually promises that this economic boom will not last, and that the benefits from Trump’s tax cuts and deregulation will be short-lived. How much this media propaganda is affecting the Fed’s thinking is unknown.

While no one knows when the next recession arrives, this economy does not look like it’s anywhere near the peak. In fact, more and more forecasters are now predicting that GDP growth will be 5% or better in the second half of this year.

In any event, I think it’s too early to assume the Fed is going to raise rates more than three times next year. Add to that the fact that President Trump has already been critical of the Fed for raising rates. I think new Fed Chairman Jerome Powell would be hesitant to raise rates even more than expected in 2019, given that Trump can replace him at any time.

Fed to Keep Hiking Rates Until Something Breaks

While I don’t expect more than three rate hikes next year, the Fed does have a history of pushing rates too high and depressing the economy. Fed Chairman Jerome Powell made it clear at the Fed’s summer gathering in Jackson Hole, Wyoming last month that he is committed to the FOMC plan to raise rates at least several more times.

He also reiterated that the FOMC will continue to look to its traditional indicators for signals as to when to stop hiking interest rates. The problem is, the Fed’s economic indicators – just like the ones we all look at – are quite dated by the time they come out from the various reporting agencies.

By the time it becomes clear in the economic reports that a recession is looming, it’s usually too late for the Fed to take action that would reverse it. This is nothing new. The same is true for past times when it was appropriate for the Fed to raise interest rates to slow down the economy and head off looming inflation.

If we go back to 1913 when the Fed was created, we can find repeated examples when the Fed was late in lowering interest rates to head-off recessions, and late in raising rates to slow down the economy and avoid inflation.

Maybe this is inevitable. Truth is, the Fed doesn’t have any better information than most of us do, especially in this “digital age” where more information than ever is available. And let’s not forget that the Fed’s myriad of internal economists are no better than the ones we subscribe to.

The point I wish to make is that the Fed doesn’t make major monetary decisions until it is clear that something is wrong, or as noted in the above subtitle, something breaks. That’s usually too late but I don’t expect it to change.

9/11 – Seventeenth Anniversary

It’s hard to believe 9/11 happened 17 years ago today. Our hearts and prayers go out to the families and loved ones of Americans that lost their lives in the September 11, 2001 terror attacks. Our heartfelt thanks go out to all the men and women in the military, law enforcement and first responders who put their lives in danger to keep us safe. God bless them!

All the best,

Gary D. Halbert

Forecasts & Trends E-Letter is published by Halbert Wealth Management, Inc. Gary D. Halbert is the president and CEO of Halbert Wealth Management, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, Halbert Wealth Management, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management

© Halbert Wealth Management

Read more commentaries by Halbert Wealth Management