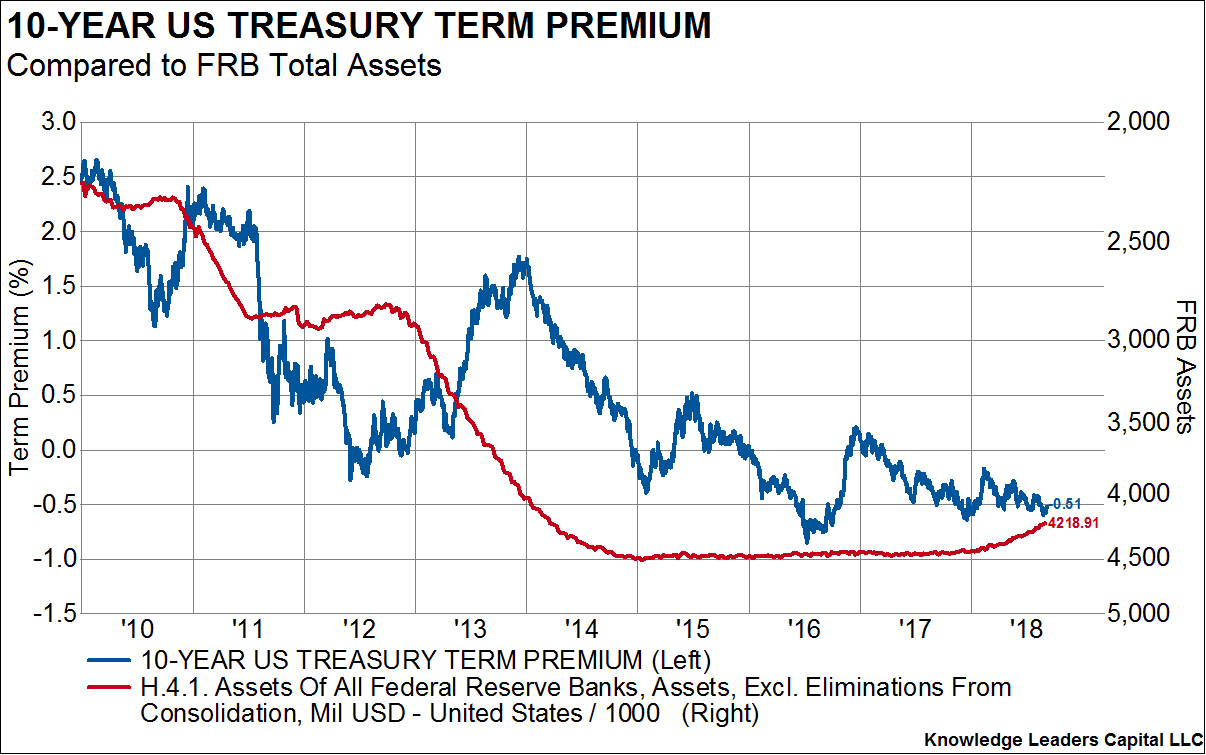

As many have documented, the main channel of transmission for the Fed’s quantitative easing policy was via the term premium component of US treasuries. As the Fed’s balance sheet doubled from 2010 to 2015, the term premium embedded in US treasuries fell from 2.5% to -75bps. The Fed is now shrinking its balance sheet, which on the surface would seem to suggest a rising term premium.

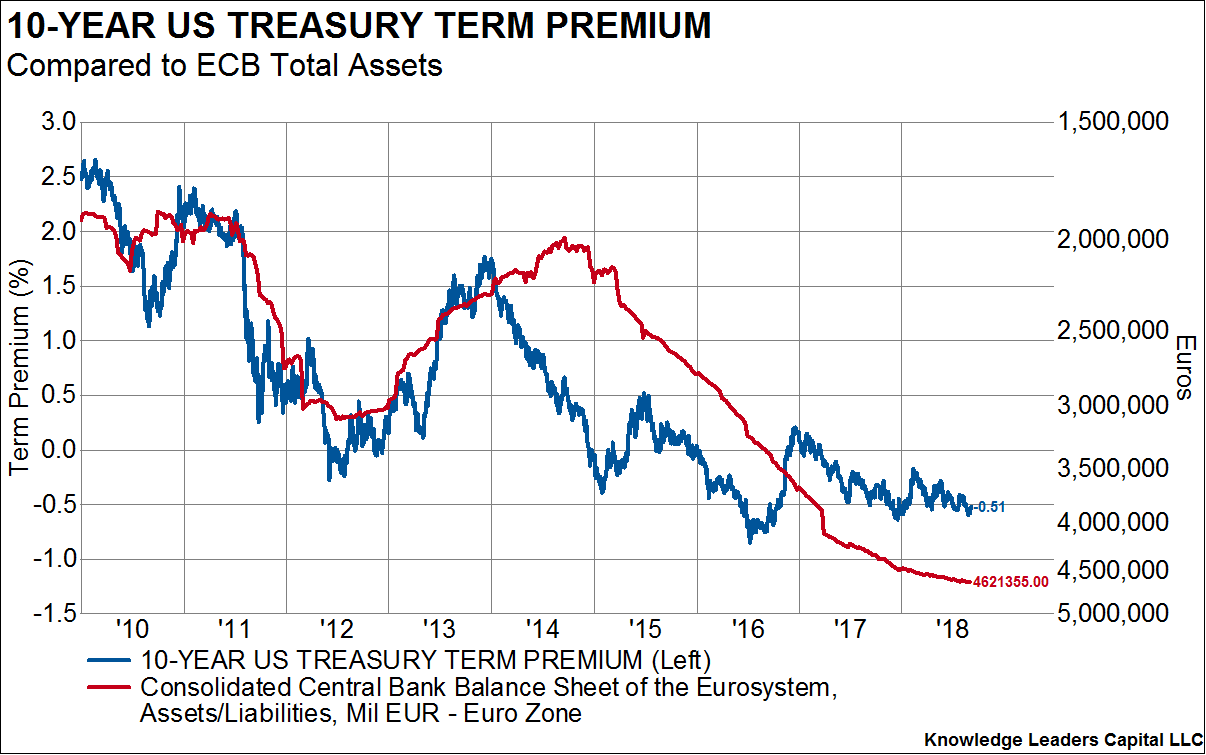

It wasn’t just Fed led quantitative easing, but the ECB’s asset purchase policies have also imparted a negative impact on US term premiums. The acceleration in the ECB’s QE program in 2016 helps explain why the term premium didn’t bottom until mid-2016. As the ECB’s asset purchases are scheduled to end in December 2018, it would suggest the ECB will be adding to upward pressure on the term premium.

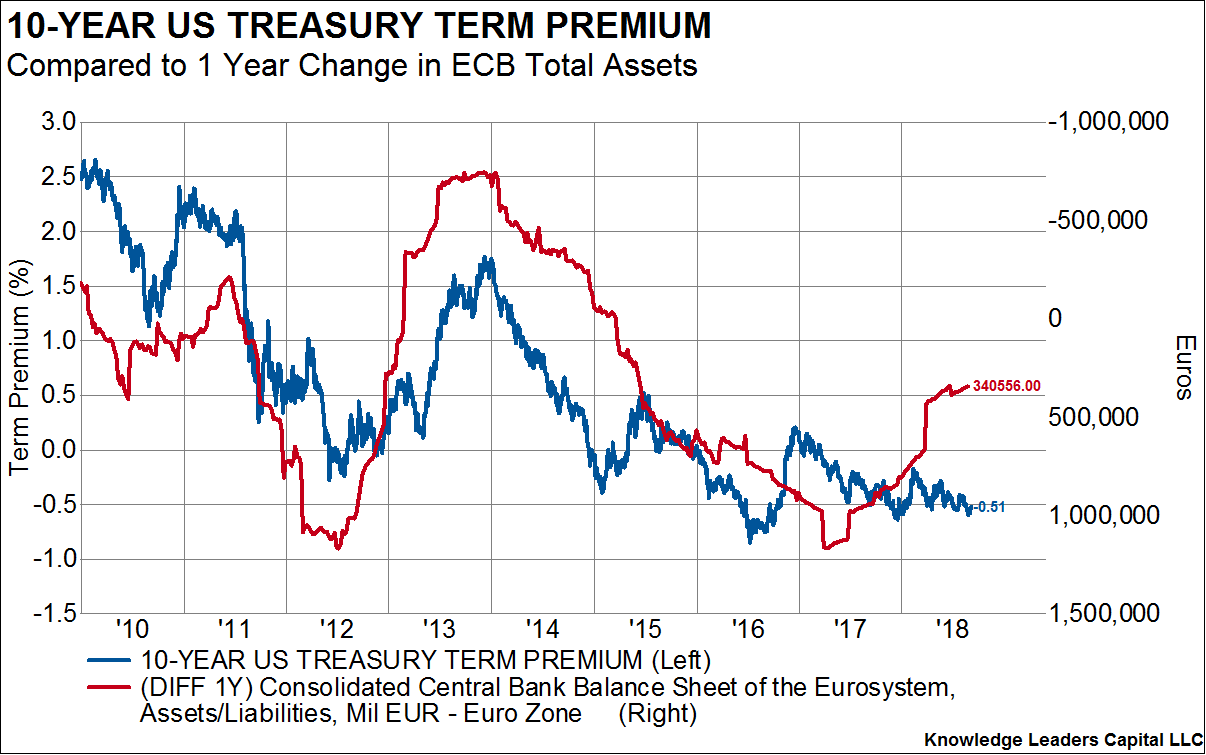

The momentum of asset purchases by the ECB has already slowed significantly. By December 2019, the one-year change in assets should rise to the zero line in the chart below.

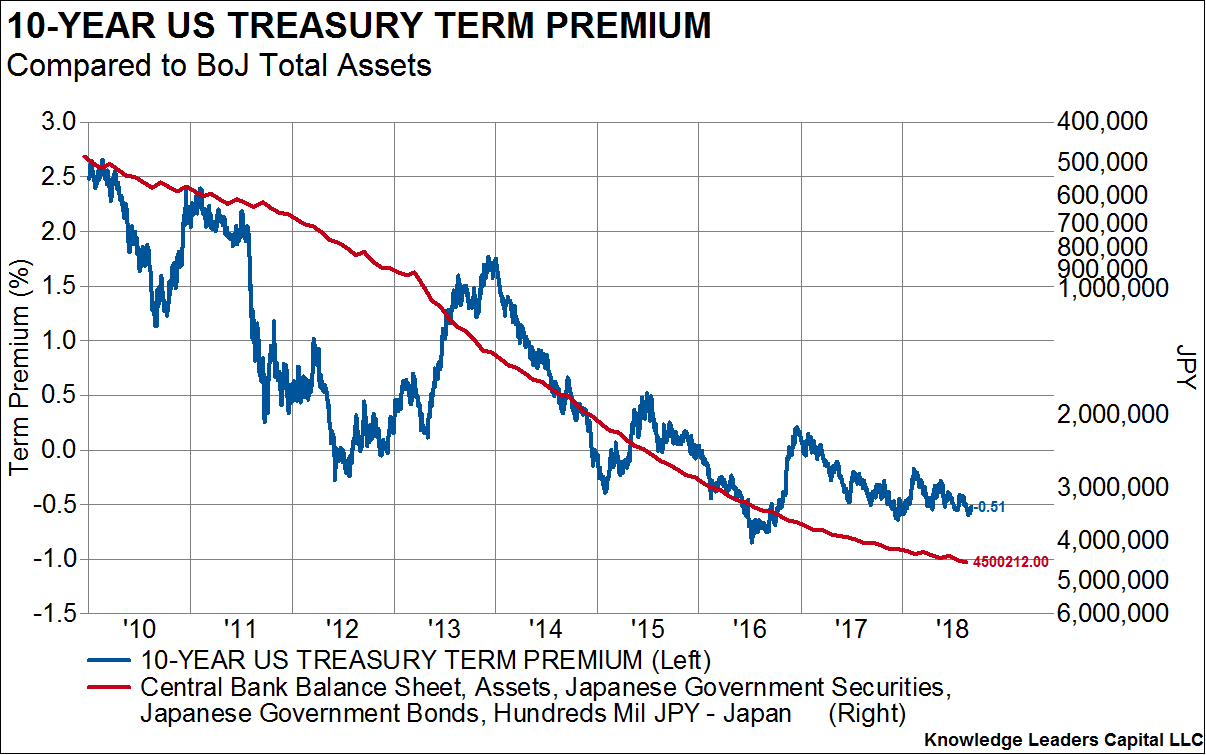

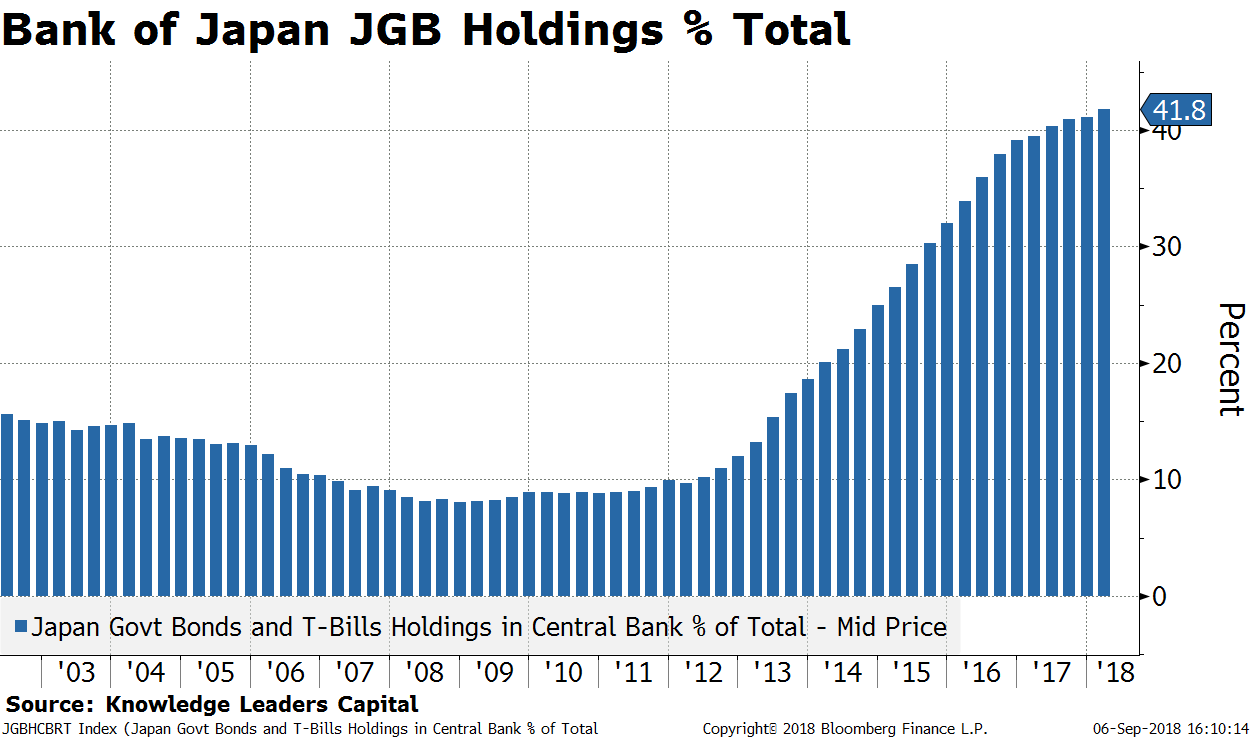

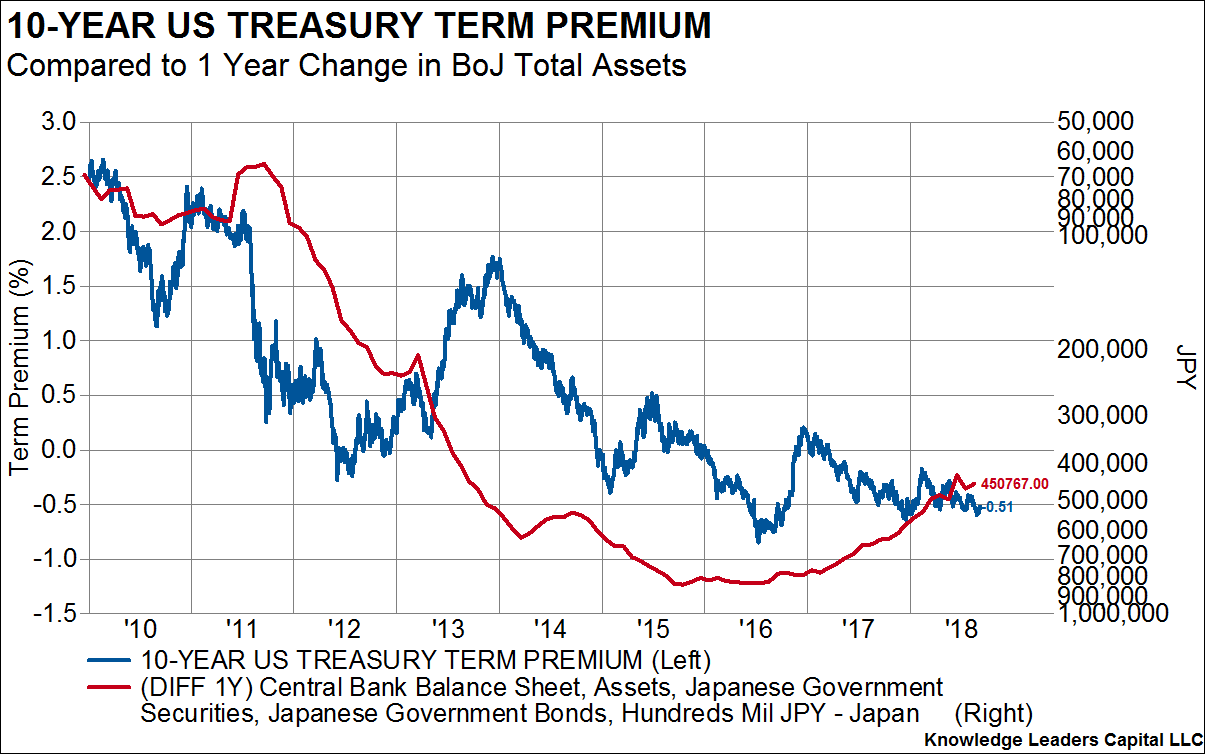

The Bank of Japan’s balance sheet has exploded by almost 10-fold in the last decade, imparting a third downward force on term premiums.

Japan may be getting to the end of the run-way in its purchases of government bonds. They own over 40% of the entire JGB market, the second largest single country bond market in the world (second only the US).

Likely as a result, the momentum of purchases has slowed here too in the last year. While still contributing to downward pressure on term premiums, the force is diminishing slowly.

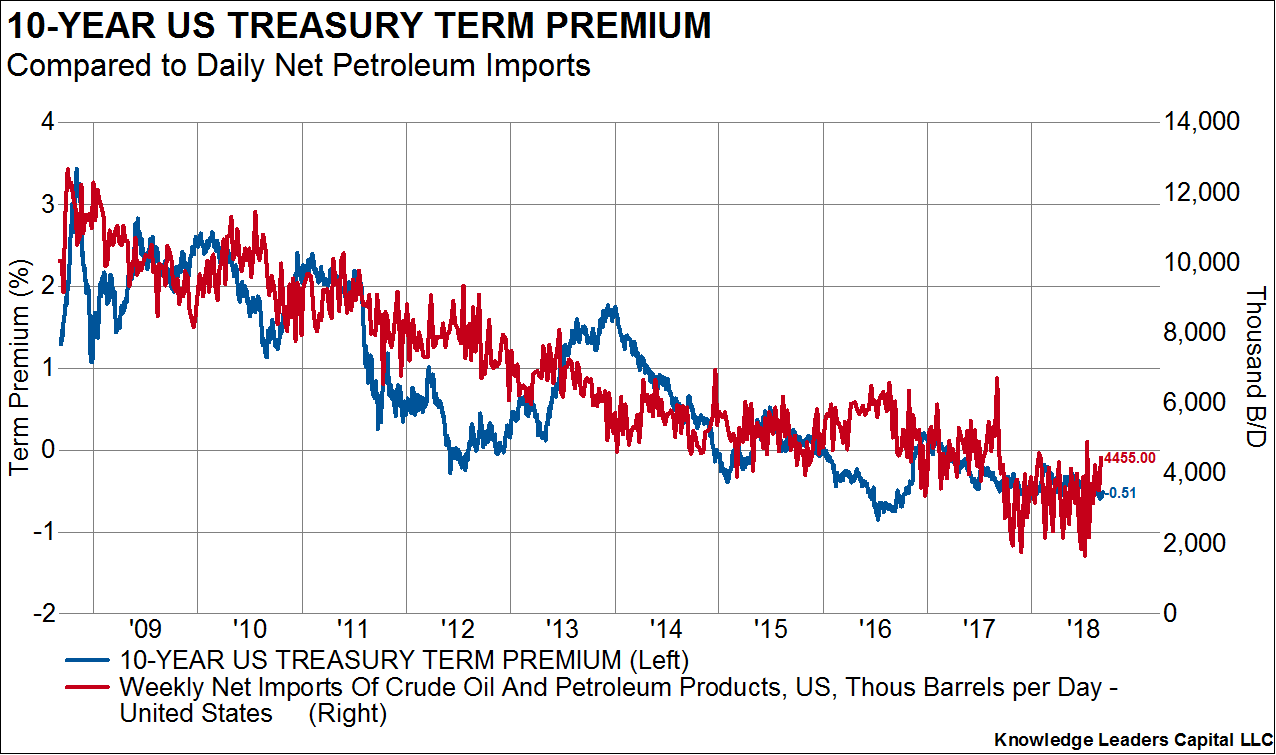

The above analysis suggests we should have begun to see a rise in the term premium by now, but instead it has remained stuck around -50bps recently.

Perhaps we can explain this divergence by bringing into consideration the energy boom we’ve seen in the US. Historically the term premium was pretty well related to oil prices because energy shocks were largely a function of America’s dependence of foreign oil. But, now the US net trade position in energy is almost in balance. The petroleum trade deficit is down to about 25bps. While the US is still a net importer of crude oil, it is a net exporter of refined product. Combined the total petroleum net deficit is down to 2-4 million barrels/day over the last year. This is down from 12 million barrels/day in 2009. With American trade in petroleum almost in balance, the possibility of an oil price shock leading to an inflation shock is greatly reduced. Even if oil prices rise significantly, the result will be an internal redistribution of income rather than an external deficit.

In the last year US crude oil production has increased by about 1.5 million barrels/day to about 11.1 million barrels/day. If this pace continues, the US will be completely energy independent in less than three years. A simple extrapolation of the above graph would suggest that complete energy independence would be associated with a roughly -2% term premium.

It is worth considering that term premiums going forward will be driven less by central bank actions than by American petroleum exploration and production companies.

© Knowledge Leaders Capital

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital