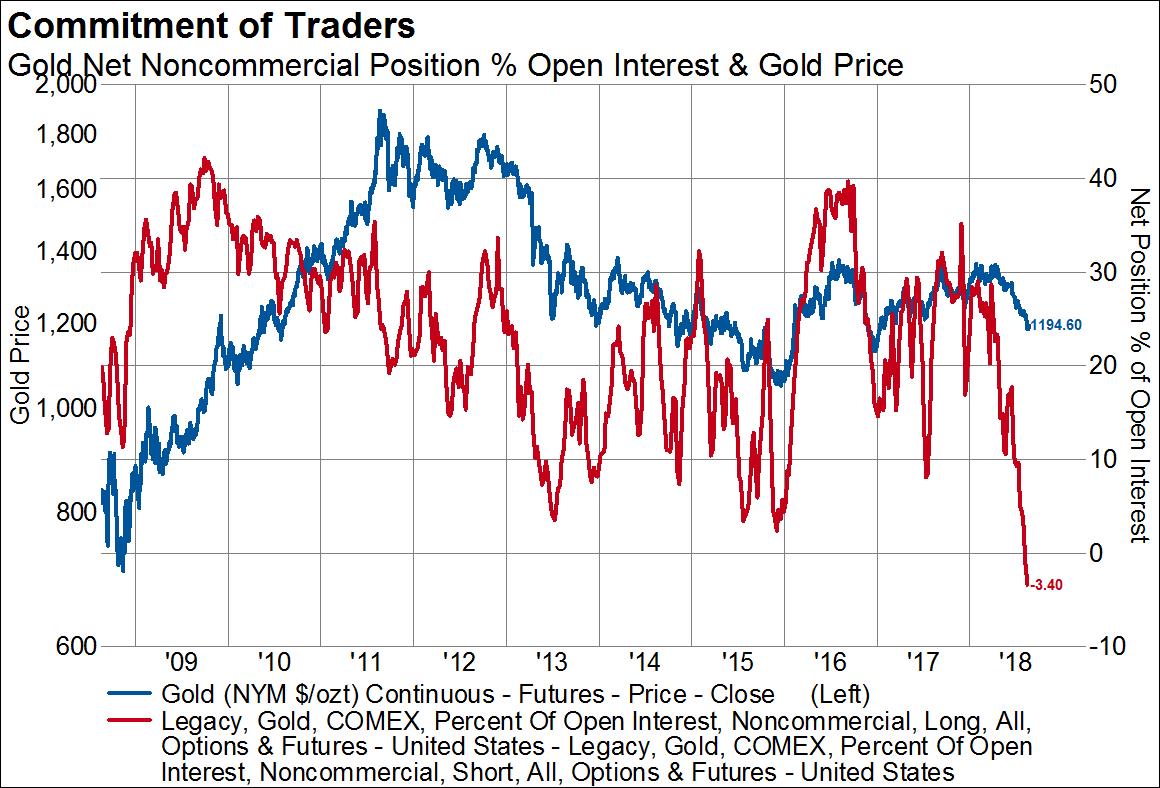

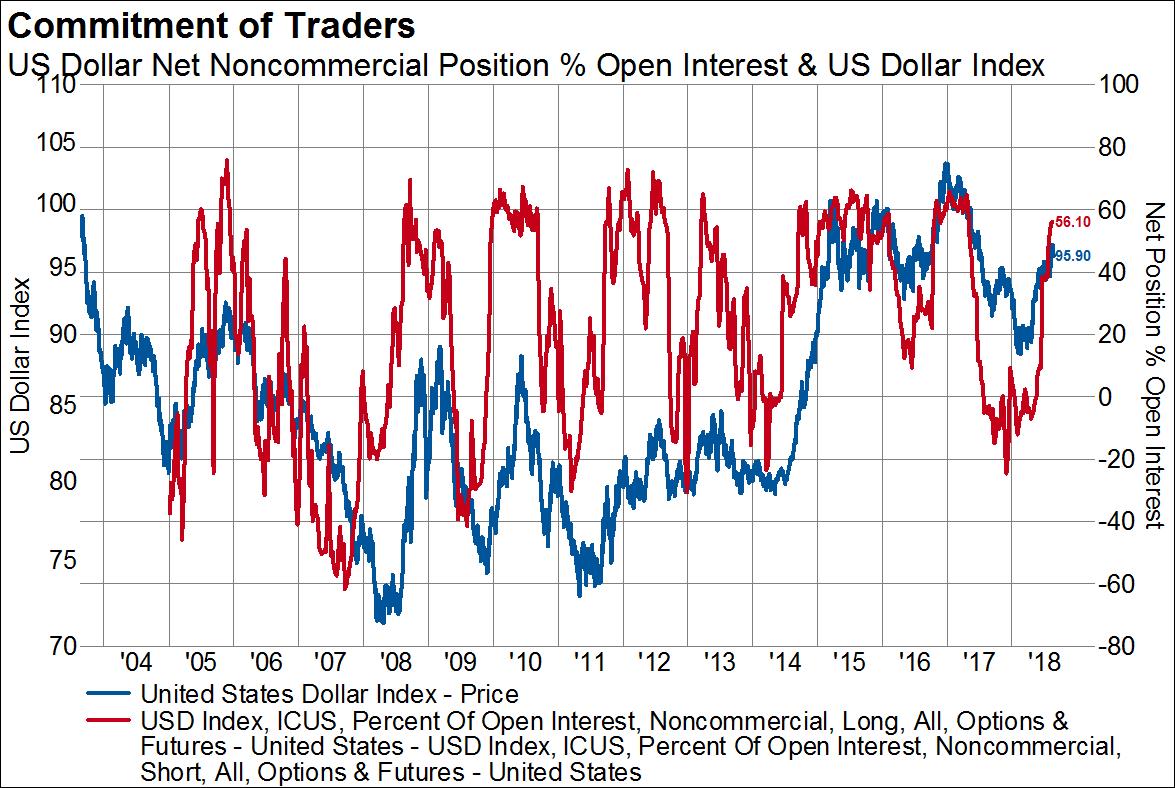

We are living through a period of extremely crowded trades at the moment, as Jeff Gundlach notably quipped several days ago. The risk in crowded trades is of course that what would otherwise be relatively minor risk reversals can cause massive covering of positions resulting in large moves in the underlying. Ditto when those positions are levered, like options or futures contracts. But right now we observe not only one crowded trade, but two (short gold, short treasury bonds) going on three (long the US dollar). As we will see, crowded trades eventually get reversed, which is what makes this extreme positioning trifecta so interesting. In all the charts below we plot the total speculative positioning in options and futures contracts as a percent of open interest as the red line on the right axis. We plot the underlying on the left axis with the blue line.

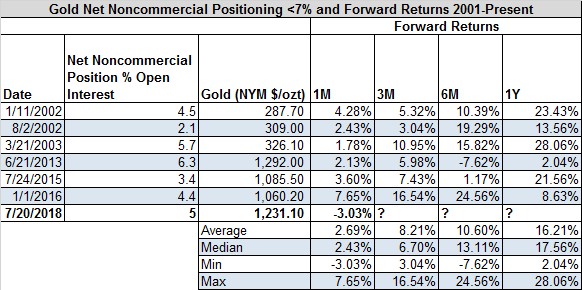

Starting with gold, we can see that speculators registered an extreme position in gold on July 20th and as of last week they became net short of gold for the first time this cycle, and indeed for the first time since 2001. Previous episodes of extreme gold positioning (which for speculators was actually just a very small long position) resulted in sharp price increase, averaging 10.6% over the next three months and 16.2% over the next year, as the first table below shows. What is interesting is that speculative positioning in gold right now is even more extreme than it was in late 2015, which resulted in a 21.6% jump in the price of gold over the next year. Though to be fair, the move didn’t begin in earnest until six months after the extreme in positioning was first registered.

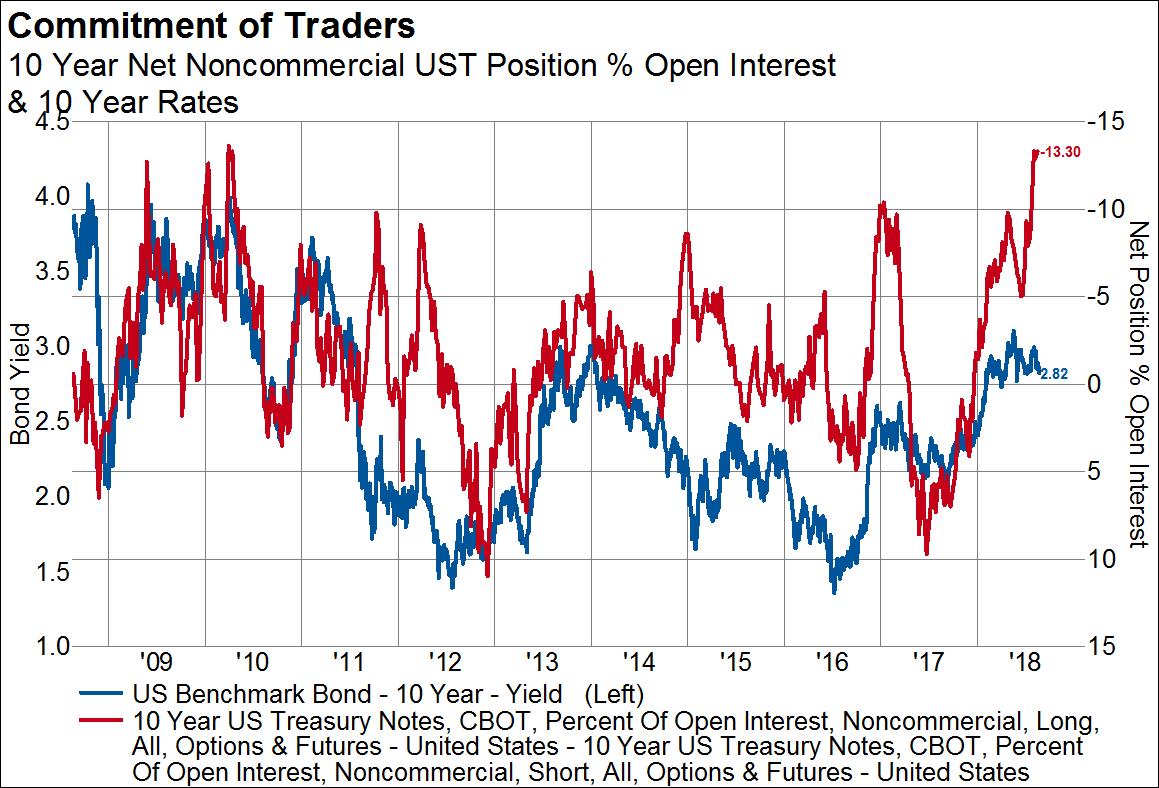

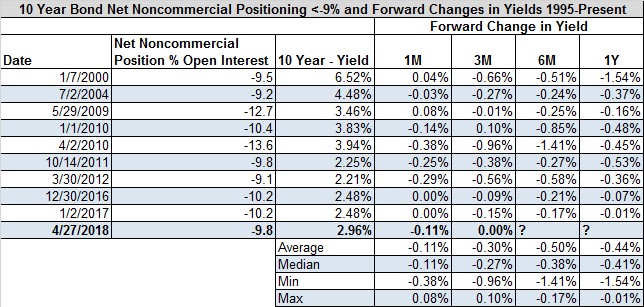

Next is bonds. Bond positioning reached an extreme short position on April 27th, and has since moved to the second most extreme net short position ever, only eclipsed in April of 2010. When bond shorts grow to extreme levels, interest rates have always fallen over the next six and twelve months. The only other time net shorts as a percent of open interest breached 13%, interest rates fell by 141 basis points six months later.

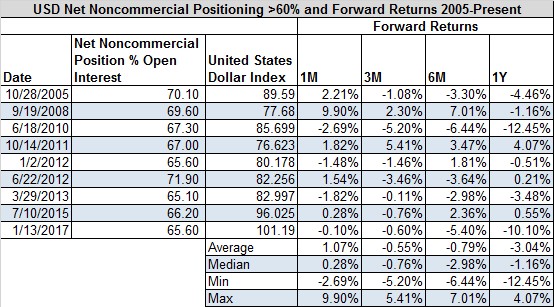

Finally, the US dollar. Speculative long positioning in the US dollar has not quite grown to extremes, statistically speaking, but it’s close. We view extreme positioning on the the long side of the US dollar at 60% of open interest and the current reading is 56%. Still, it’s worth considering the forward returns when positioning becomes extremely long the dollar. Generally speaking, positioning extremes lead to muted to slightly negative forward dollar returns. On average the dollar falls by 3% over the next year once an extreme reading is triggered, but the forward returns in the table below fail to account for multi-year periods of dollar weakness once positions start to be unwound and speculators move to becoming short.

Given that crowed trades always eventually get unwound, this setup in cross asset positioning is highly peculiar. For example, short covering in bonds may well cause the dollar to stumble as foreign bonds become relatively more attractive. A US dollar positioning unwind that sends the dollar lower may cause gold to scream higher. A trade war resolution that puts a floor under the Chinese yuan may induce gold speculators to cover their shorts, which in turn could cause dollar speculators to cover longs. In any case, it appears that simultaneously lower gold, higher rates and a higher dollar is possibly the lowest probability scenario of them all.

© Knowledge Leaders Capital

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital