The Kansas City Fed’s annual monetary policy symposium begins later this week in Jackson Hole, Wyoming. Around 120 people attend the conference, including central bankers from around the world. In the past, the Fed chair’s speech has often been a big deal for the financial markets. This will be Powell’s first speech as Fed chair and the title (“Monetary Policy in a Changing Economy”) suggests the possibility of a change in the Fed’s approach or some modification in its thinking. However, whether Powell provides any new clues is an open question. Of greater interest will be the debates and discussions (the impact of trade policy uncertainty, full employment) in the hallways and around the grounds. Powell may even address these issues.

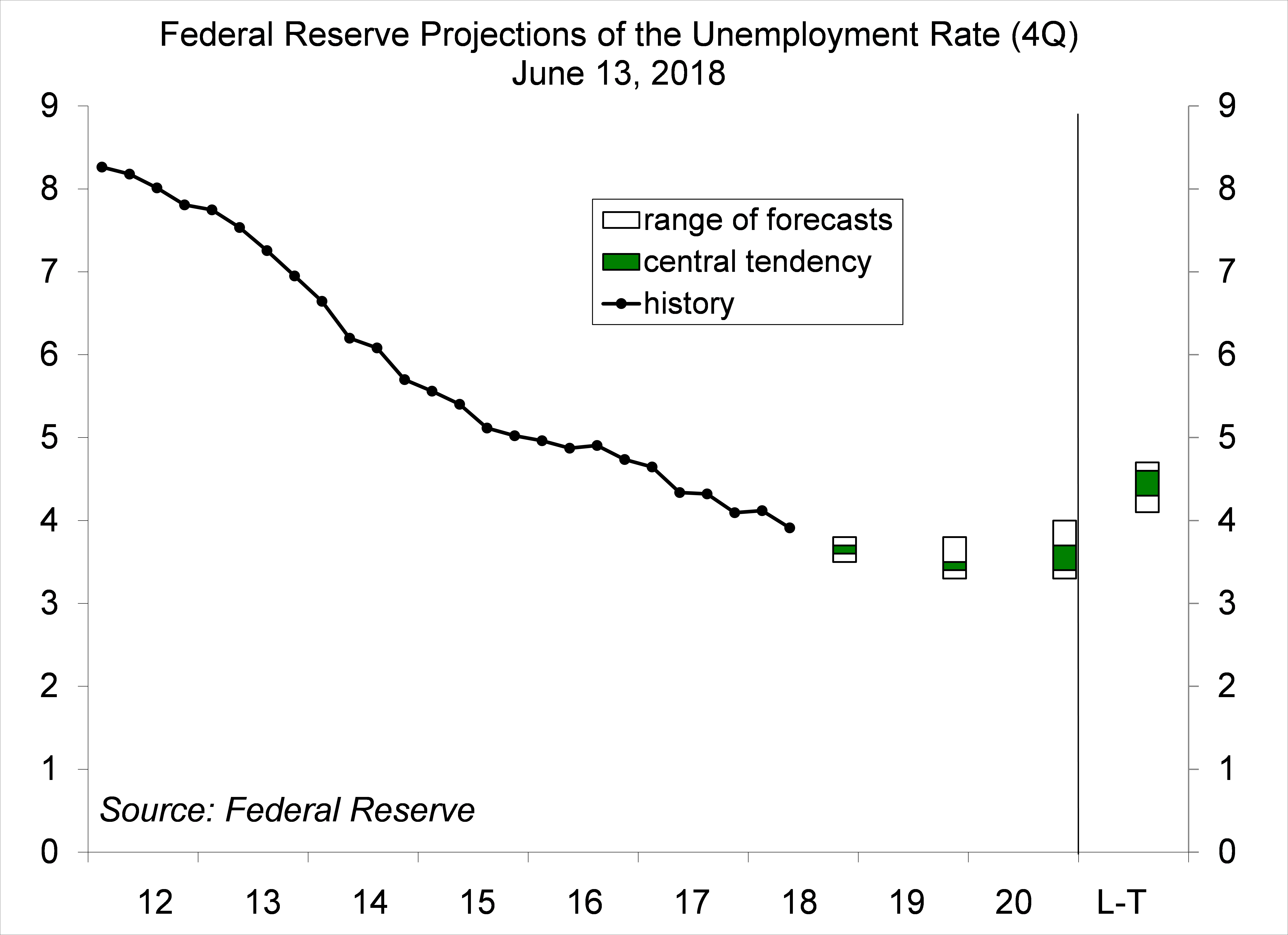

There were a few oddities in the June 13 Summary of Economic Projections (forecasts of senior Fed officials). The unemployment rate was expected to fall a bit further, averaging 3.6% in 4Q18 and 3.5% in both 4Q19 and 4Q20. However, the long-term average was seen as 4.3-4.6%, which implies that the economy would have to slow below its potential (the Fed sees the longer-term average of GDP growth at 1.8-2.0%). Job growth has remained relatively strong this year, well beyond a long-term sustainable pace (based on the demographics). At the same time, while wage growth has picked up, the pace is not especially strong (well below the kind of appreciation we’ve seen around low unemployment rates in the past). In hindsight, there was more slack in the job market than many had expected, but that slack is still declining. Labor costs are the widest channel for inflation pressure.

Chart 1

Chart 2

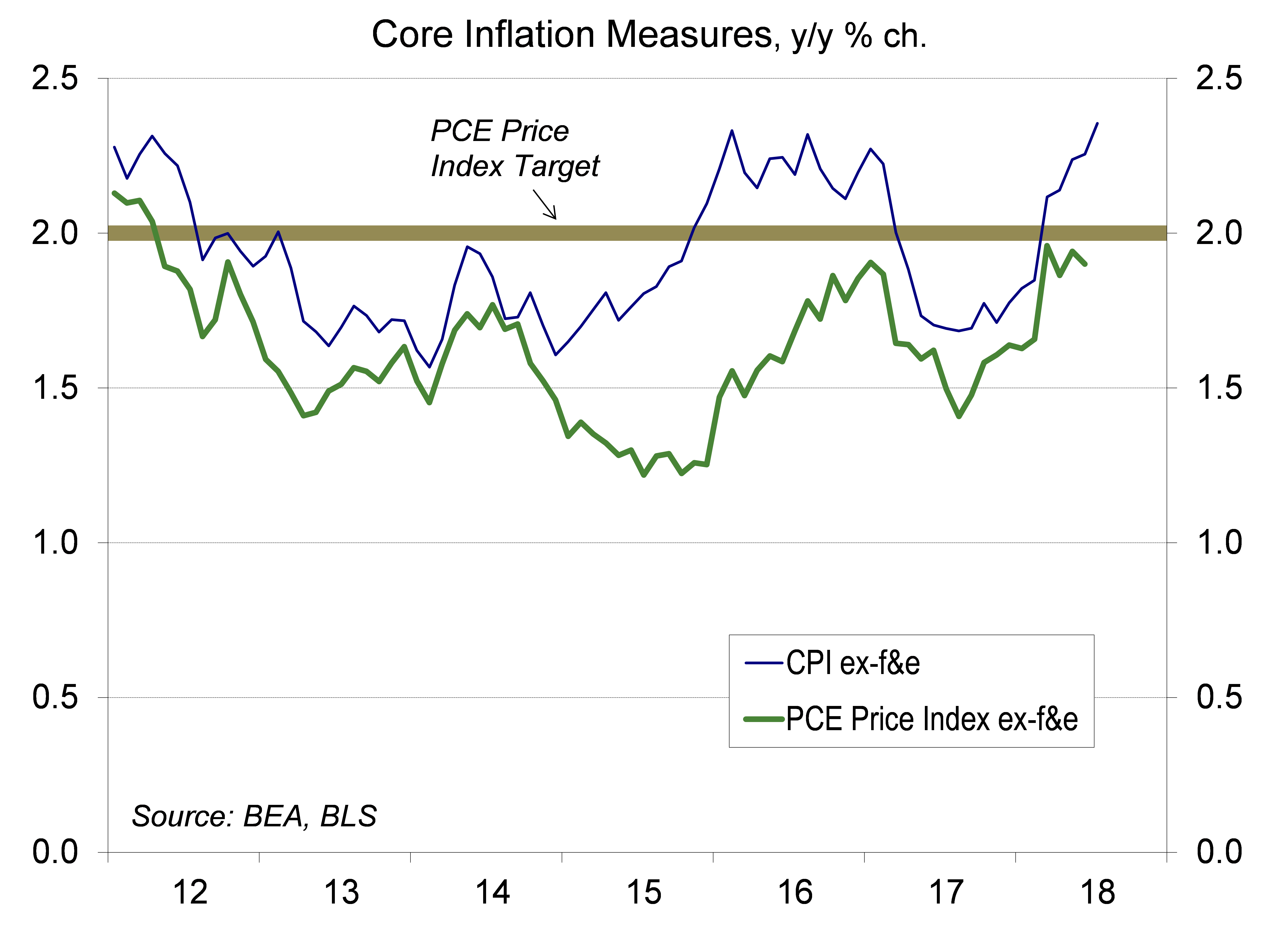

Inflation, as measured by the PCE Price Index excluding food and energy, is expected to match the Fed’s 2% goal for the 12 months ending in July (data due August 30). Fed officials have indicated a tolerance for having core inflation trend a bit above the 2% goal for a while. In this way, 2% becomes a target, rather than a ceiling (and in turn, inflation expectations should be anchored at 2%, rather than a bit below – that’s important for the Fed). With the exception of oil, commodity price pressures are not a major inflationary concern. It takes a gigantic increase in the prices of raw materials to have much of an impact at the consumer level. Increased tariffs have raised prices in some sectors (washing machines up 20%, lumber adding $9,000 to the average price of a new home), but have not been a significant factor in boosting overall inflation – at least, so far. However, the University of Michigan’s survey of consumer sentiment noted that recent data suggest that “consumers have become much more sensitive to even relatively low inflation rates than in past decades” and tariff concerns appear to have weakened buying perceptions for autos and new homes in early August (these are two of the most cyclically sensitive components of the economy).