There has been considerable discussion lately about the slowly inverting yield curve and what it may signal for growth prospects going forward. Commonly used as a proxy for the yield curve is the spread between 10-Year US Treasury yields and 2-Year US Treasury yields. As of this writing, the spread is 24bps, having compressed by 2bps today after Fed Chair Powell’s presentation.

Most observers look at the chart below and conclude the yield curve is on the cusp of inverting—after maybe one more rate hike in September—and from there the clock is ticking on when the economy goes into a recession.

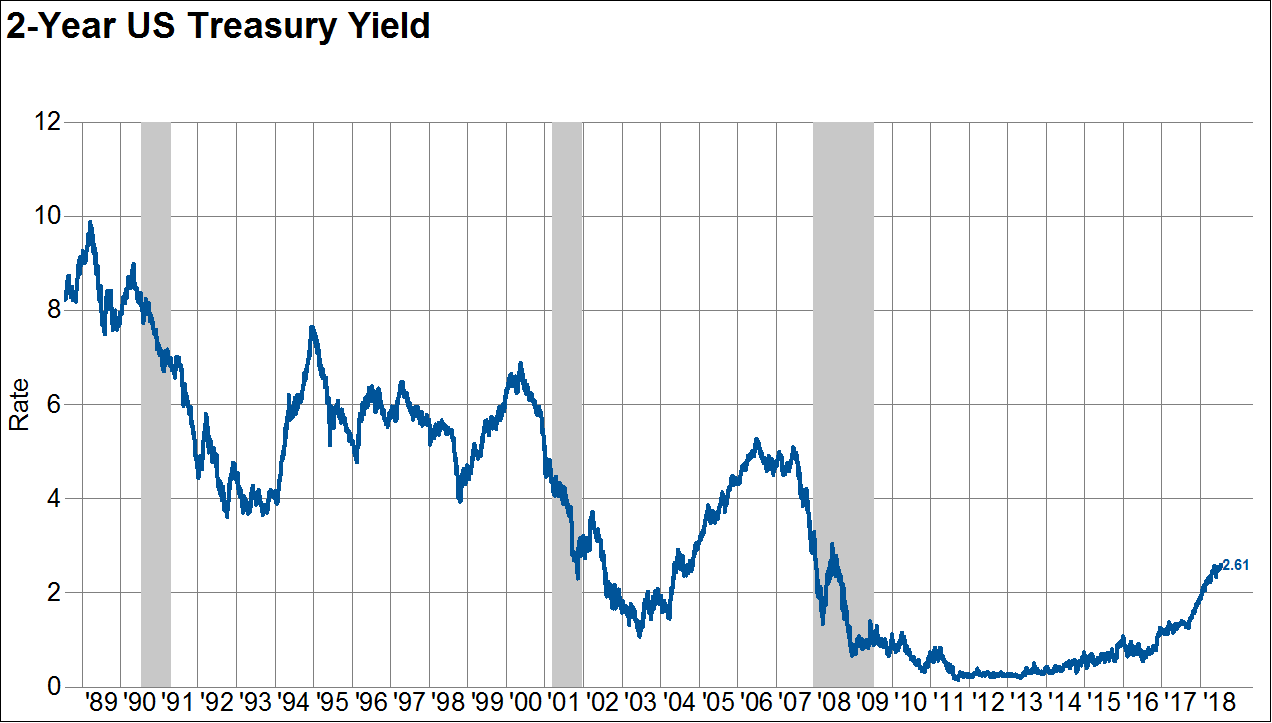

If there is one thing I’ve learned over the course of the last decade, it is that many things are not quite what they appear to be in the US Treasury market. In the next chart, I show the standard 2-Year US Treasury yield which has been rising since 2014 in anticipation the current tightening cycle.

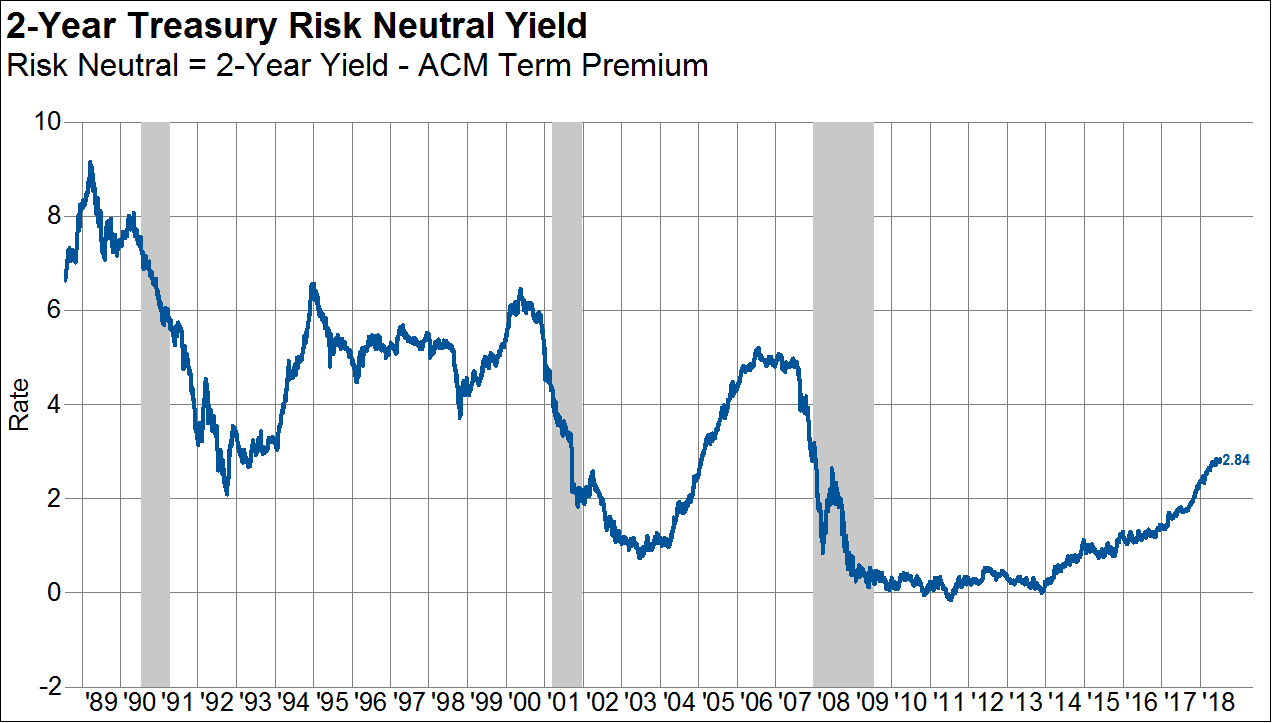

But, there is a key piece missing in this analysis. Term premiums—which historically are positive, compensating investors for unexpected pops in inflation—are negative after trillions of dollars of quantitative easing. In fact, this is the main channel through which Fed asset purchases have impacted the US Treasury market. In the chart below, I show the ACM term premium for the 2-Year Treasury, which is -28bps.

So, we need to adjust the observed yield on the 2-Year Treasury for a negative term premium. If we subtract a negative term premium from yields, we arrive at a “risk neutral” 2-Year US Treasury Yield. Note that by subtracting a negative term premium we end up adding the term premium to observed yields.

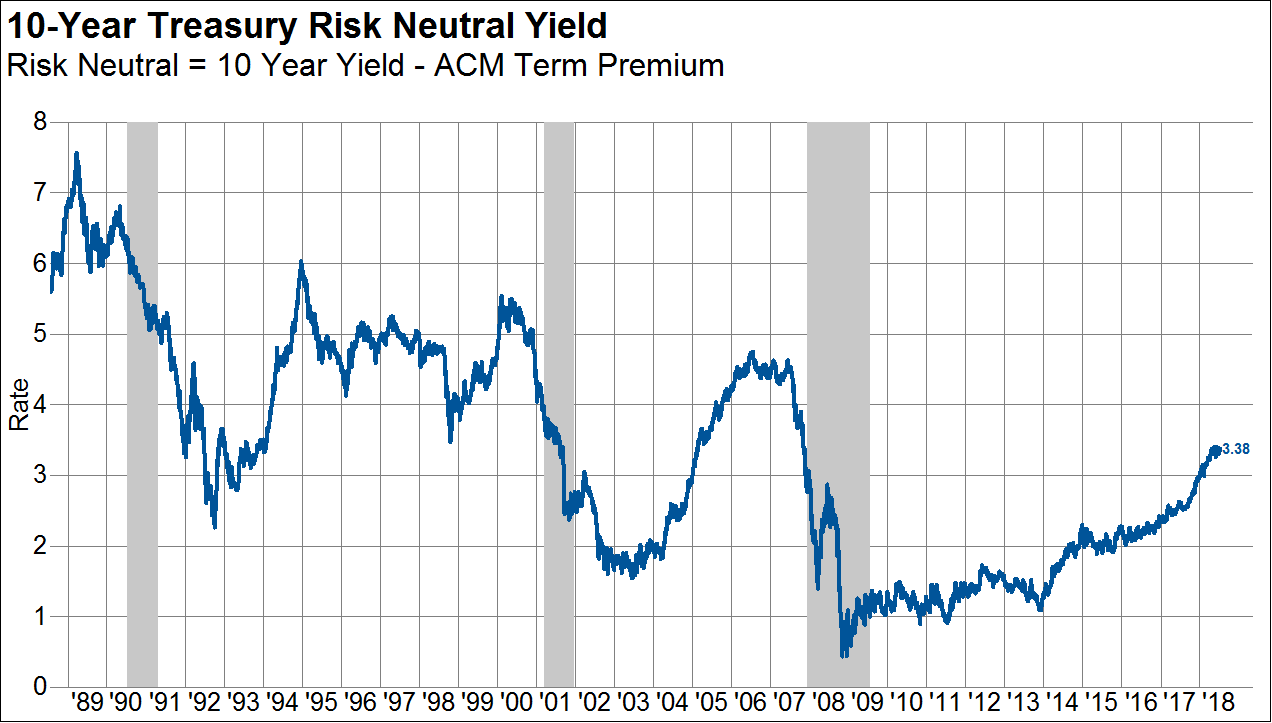

Moving on the to 10-Year yield, we can perform the same adjustment process. I begin with observed 10-Year yields of 2.86%.

Next, I chart the ACM term premium for 10-Year US Treasury yields. It is 52bps, so it is clear that there is a negative slope to the US Treasury term premium curve.

Again, by subtrcting the negative term premium from oberved 10-Year yields, we end up with a “risk neutral” 10-Year yield, which is considerably higher than observed yields. This risk neutral yield began steadily rising in 2014 from about 1% to the current reading of 3.38%.

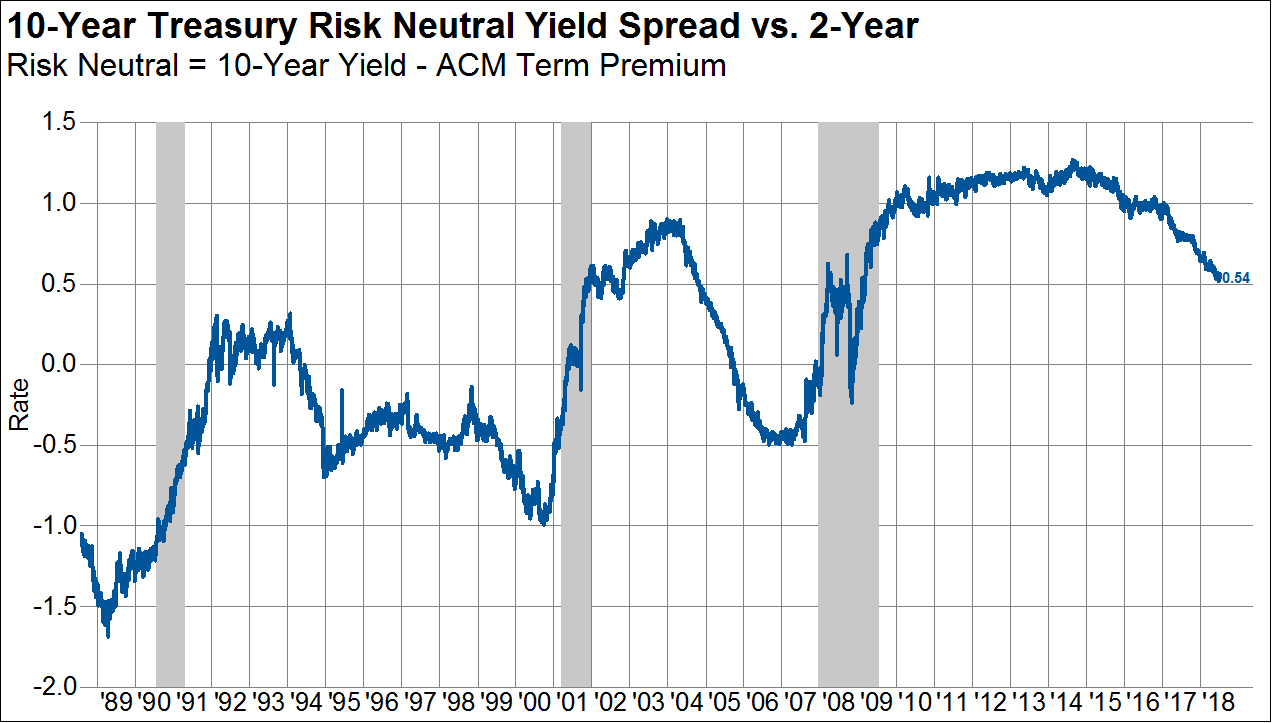

So, now that we have the pieces, I calculate the true yield curve adjusted for negative term premia. There are at least two interesting observations here: 1) the curve is nowhere near inverted and 2) current readings are consistent with many years of economic growth before the onset of recession. Today’s risk-neutral yield curve is steeper than any point in the 1990s expansion. At 54bps it is now where the curve was in 2004, four years before the 2008 recession. Historically this curve inverts deeply preceding a recession (-100bps in 2000 or -50bps in 2007).

I think there is more than meets the eye when thinking about the current state of the yield curve. Perhaps this is why Fed Chair Powell was somewhat dismissive of the yield curve in his testimony to Congress. The risk-neutral term structure seems to suggest that there are years left in this economic cycle before this curve inverts to a level that historically signals an impending recession.

To wrap up, I thought it would be interesting to look at the risk-neutral 10-Year to 3-Month US Treasury spread. It is 144bps, which is about six 25bps hikes away from inverting. This reinforces the message from the bond market that recession is still years away.

© Knowledge Leaders Capital

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital