In light of Fed Chairman Powell’s congressional testimony, we thought it relevant to revisit the inflation story and provide yet more evidence that the trend in inflation continues to be higher. For now, the Fed has assessed the risks to inflation and growth as balanced in both directions, which is Fed-speak for a policy that is on auto pilot. Yet, a number of indicators spanning the labor market to input costs suggest the risks to inflation, at least, remain squarely to the upside. Not that this will necessarily affect Fed policy. After all, the Fed has recently introduced the concept of inflation symmetry, which is the idea that if inflation ran below target for an extended period then perhaps it should run above target for an extended period as well. But a continued trend of higher inflation would surely inform asset allocation decisions of portfolio managers from the types of equities to be invested in to the magnitude of one’s commodity exposure. With that, let;s get to the charts.

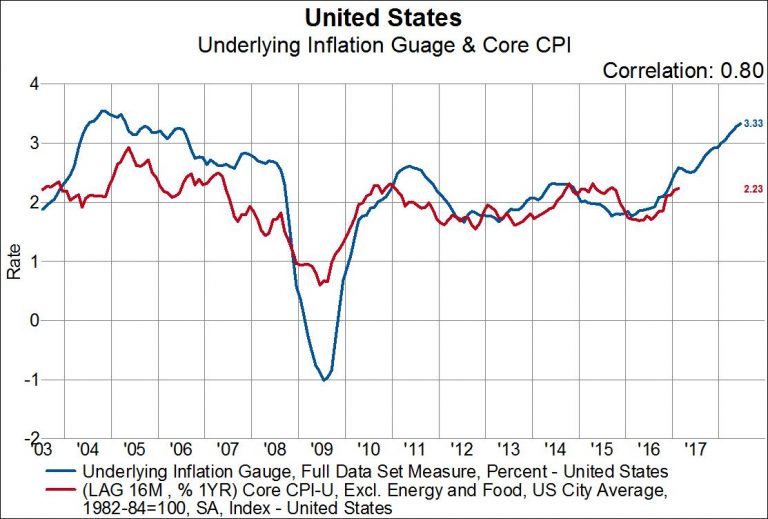

One of our favorite indicators of trend inflation is the New York Fed’s Underlying Inflation Gauge. It includes not only measures of prices, but also macroeconomic and financial market variables in order to capture the true trend of economic pricing pressure even more acutely than the Core CPI. Interestingly, the Underlying Inflation Gauge (blue line) leads Core CPI (red line) by 16 months and is doing nothing but going up and to the right. If this were a stock, you would want to own it.

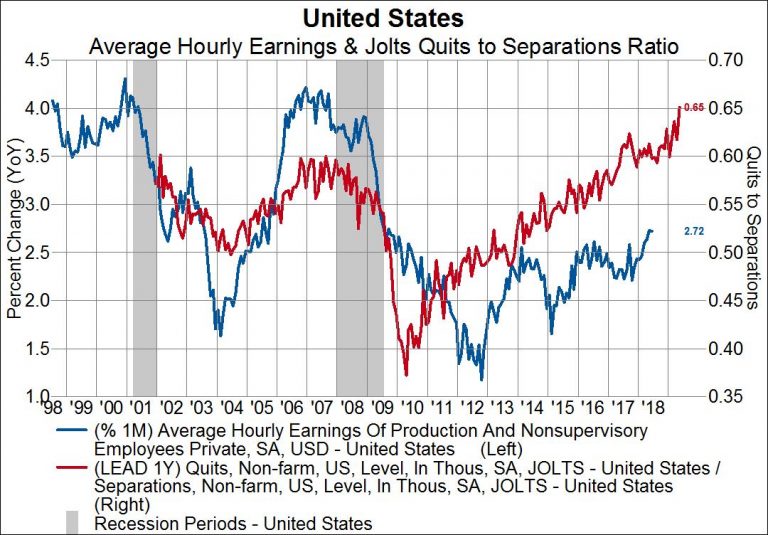

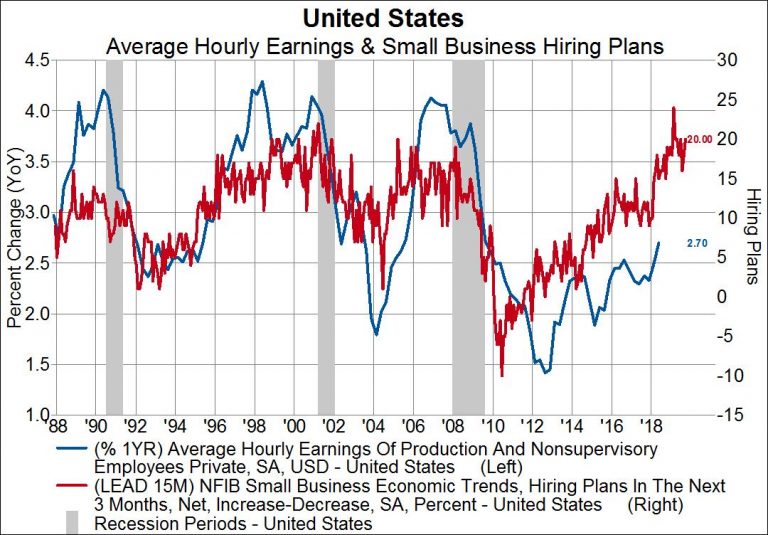

The long-awaited increase in wages also seems to be unfolding, and indicators suggest it has legs. The next chart below compares average hourly earnings (blue line, left axis) to the ratio of quits to total separations (red line, right axis), two components of the Job Openings and Labor Turnover Survey (JOLTS). Voluntary quits as a percent of total employment separations can be thought of as one measure of wage pressure, since people generally only voluntarily leave a job for another higher paying job. Therefore, the fact that this ratio has exploded higher so far in 2018 suggests that faster wage growth is not far behind. In fact, the quits to separations ratio leads wage growth by about one year.