Fed Chairman Jerome Powell will deliver his semi-annual monetary policy testimony to Congress on Tuesday and Wednesday, but he’s not expected to cover any new ground. In the past, this testimony was often a big deal for the financial markets. However, the Fed has become more transparent over the years. We have the Fed’s Monetary Policy Report in hand (released on Friday). We have the Fed’s Summary of Economic Projections (forecasts of growth, inflation, unemployment, and the revised dot plot). Powell delivered a post-FOMC press conference. He sat down for a Marketplace interview last Thursday, which provided a lot more insight into his approach. Still, there are a number of uncertainties in the outlook. For example, how much slack remains in the labor market? The bigger question is how the Fed views the risks from trade policy. To date, Powell has indicated that the Fed is watching things closely, but consumer and business concerns about trade policy are increasing rapidly.

As Powell noted in his post-FOMC press conference on June 13, “the economy is doing very well – most people who want to find jobs are finding them, and unemployment and inflation are low.” The Fed expects that fiscal policy (tax cuts and added spending) will continue to support economic growth this year and next.

In his Marketplace interview, Powell said that the Fed “doesn’t directly look so much at wages as we do price inflation,” but is “looking very carefully at maximum employment as one of the things that pushes up wage and price inflation.” Powell said it is “a bit of a puzzle” (not a “mystery”) why wages aren’t rising at a faster pace, but points to lackluster productivity growth as a possible culprit. Still, prices should go up as markets tighten, “and I think we’re starting to see that.”

The PCE Price Index rose 2.0% over the 12 months ending in May, matching the Fed’s goal. That estimate is subject to change when comprehensive benchmark revisions are released (July 27), but it’s too soon to declare victory according to Powell (“we want inflation to be symmetrically around 2% -- just reaching up and touching it once doesn’t fulfill that goal”).

Powell is aware of the risks of overshooting on monetary policy. “If we leave rates too low for too long, then we can have high inflation or we can have asset bubbles or housing bubbles. If we move too quickly, then we can unintentionally put the economy into a recession or cut off the return of inflation at 2%. So we’re always balancing those two things.” This balancing act wasn’t much of a concern for the last several years, but is more important as policy nears a neutral level.

The Fed’s Monetary Policy Report provides a comprehensive look at the overall economy. However two key themes, which were also included in the June 13 policy statement, stand out. The first is that Fed officials still see the stance of monetary policy as “accommodative” even after the June rate hike. That means there is a little more work to do to get to normal. The second is that conditions are expected to warrant only gradual increases in short-term rates. Officials still see some slack in the job market, which means that they can afford to take their time. However, as we saw in the revised dot plot, policymakers are divided on whether there will be one or two more rate increases in the second half of 2018.

The Fed normally refrains from taking a stand on fiscal policy, but has to take account of the impact. Powell believes that “the tax cuts and spending increases are very likely to support economic activity for at least the next few years.”Fiscal policy may also have long-term positive effects on the supply side (higher investment and productivity growth), but this is uncertain and “there’s a very wide range of perspectives on how that would happen,” according to Powell. Longer-term, “it is widely understood that the U.S. is on an unsustainable fiscal path,” largely due to the interaction of an aging population and rising health care prices.

The Fed also normally refrains for taking a stand on trade policy. The Fed is “hearing a rising level of concern about the effects of changes in trade policy.’ Powell noted that the post-war trading system “has served the global economy, and particularly the U.S., very well.” It has boosted productivity and incomes. However, “there are particular populations and geographies that are negatively affected” – and no country has done a good job of addressing those concerns.

Trade tensions have escalated sharply in recent weeks and are expected to have a much broader impact on the economy in the months ahead. It’s difficult to come up with precise estimates of the impact on growth and inflation, but increased tariffs add to costs and disrupt supply chains. The uncertainty is a negative for fixed investment at home and abroad. While the impact is uncertain, the Fed does not have a set of tools to deal with the fallout – it only has short-term interest rates.

Powell has been with the Fed for six years, but has generally kept a low profile. Powell’s Marketplace interview has helped to give us some insight into the man. While not an economist by training, he has had “an awful lot of time to learn the economics.” Much like Bernanke and Yellen, he appears to have an open mind and is willing to listen to a variety of views. That characteristic is likely to be important as the Fed attempts to balance growth, inflation, and trade policy uncertainty in the months ahead.

Data Recap – Once again, the economic data took a backseat to trade policy concerns. The year-over-year increase in the CPI increased, offset growth in average hourly earnings over the last year (implying limited firepower for consumer spending growth).

The Federal Reserve’s Monetary Policy Report repeated two key themes. The first is that (even after the June 13 rate hike) officials still viewed policy as “accommodative” – that is, not “neutral.” The second is that further gradual increases in short-term interest rates are expected. Policymakers generally see some remaining slack in the labor market, which allows the Fed to move gradually. The report mentioned trade policy uncertainty as a factor holding down long-term Treasury yields and restraining equity prices.

Trade Tensions escalated as China responded to U.S. tariffs (a 25% tariff on $34 billion in Chinese goods on July 6), with increased tariffs on $34 billion in U.S. exports. The U.S. indicated that it would retaliate against the Chinese retaliation (specifically, a 10% tariff on an addition $400 billion in Chinese goods). President Trump has also threatened to impose tariffs on $350 billion in imported motor vehicles and parts, which would bring the total to around $850 billion of U.S. imports (4.6% of GDP).

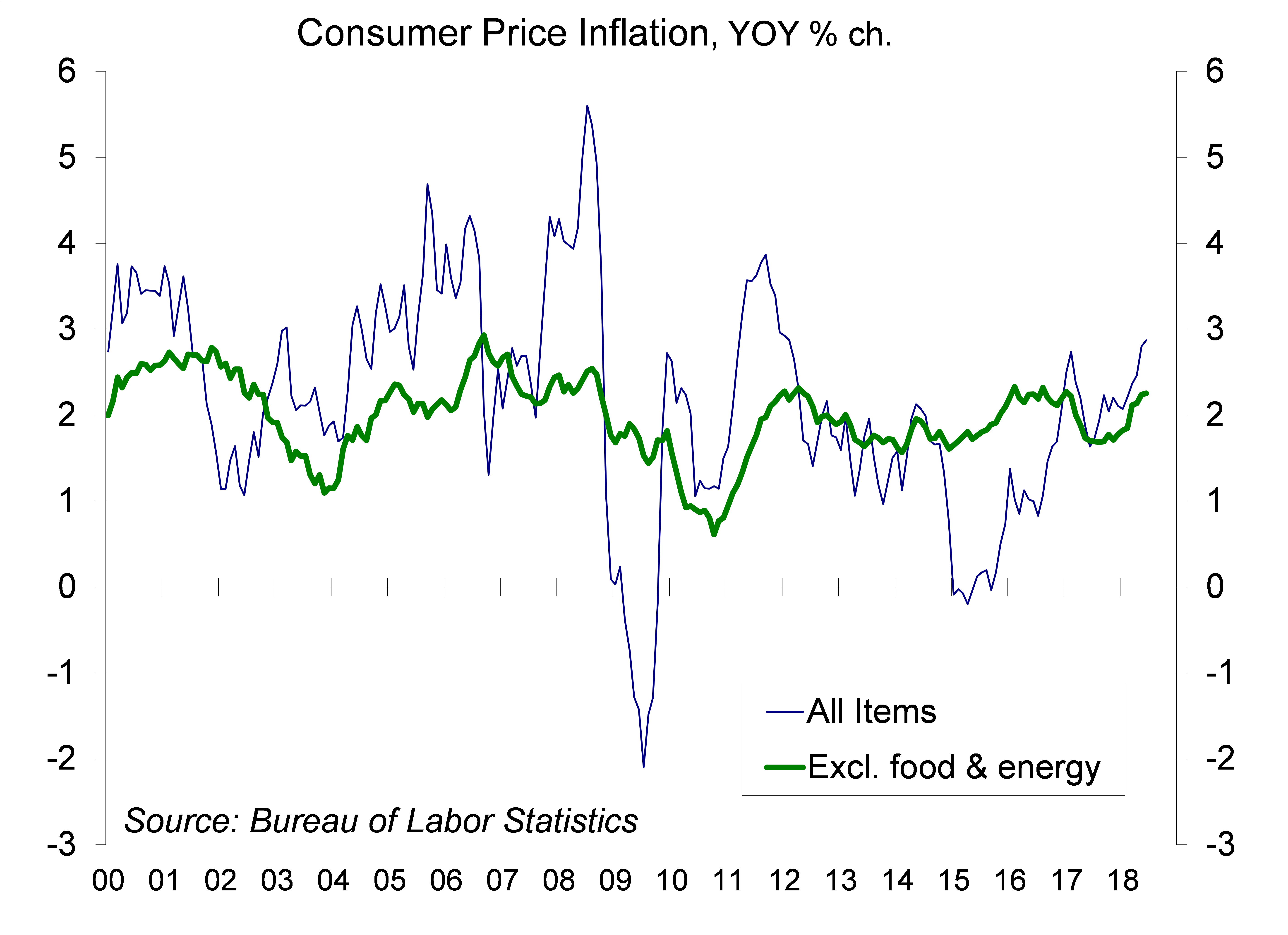

The Consumer Price Index rose 0.1% in June (+2.9% y/y), held down by a 1.5% drop in energy services. Food rose 0.2% (+1.4% y/y), with a y/y split between food at home (+0.4% y/y) and food away from home (+2.8% y/y). Gasoline (4.4% of the overall CPI) rose 0.5% (+0.3% before seasonal adjustment, and +24.3% y/y) and home fuel oil rose 2.9%, but those gains were more than offset by declines in electricity (-1.4%) and natural gas (-1.7%). Ex-food & energy, the CPI rose 0.2% (+2.3% y/y). Owners’ Equivalent Rent (23.5% of the CPI) rose 0.3% (+3.4% y/y), while rent (7.8% of the CPI) rose 0.3% (+3.6% y/y) and lodging away from home (1.0% of the CPI) fell 3.7% (-1.7% before seasonal adjustment, +1.5% y/y). New motor vehicle prices rose 0.4% (-0.9% y/y). Used motor vehicle prices rose 0.7% (-0.7% y/y). Laundry equipment rose 1.8%, up 19.9% over the last three months, reflecting the impact of tariffs. Note that the Fed uses the PCE Price Index as its official target, which has a smaller weighting on shelter, and the core PCE Price Index has been trending about 0.3 percentage point below the core CPI y/y in recent months.

Chart 1

Click here to enlarge

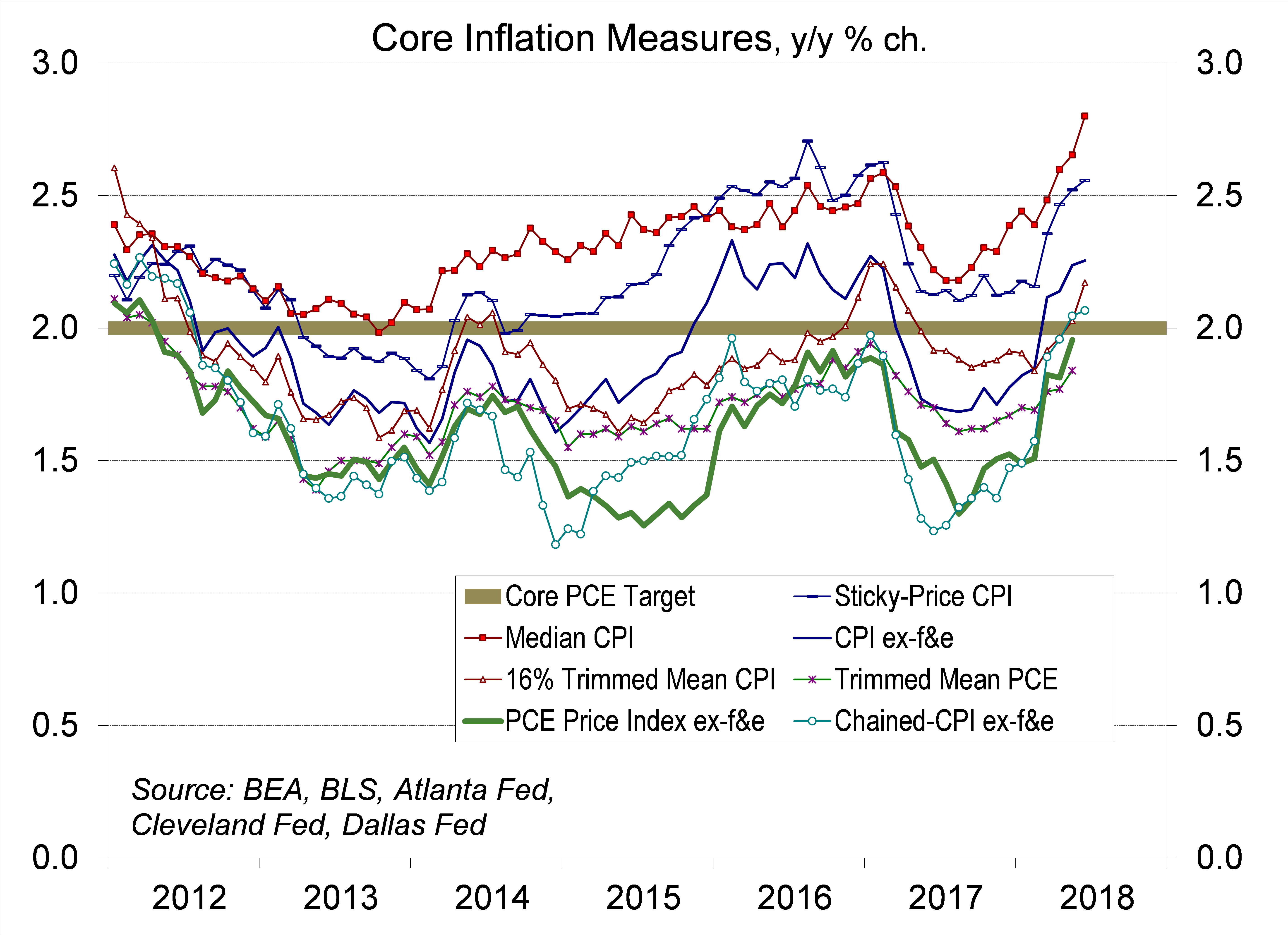

Chart 2

Click here to enlarge

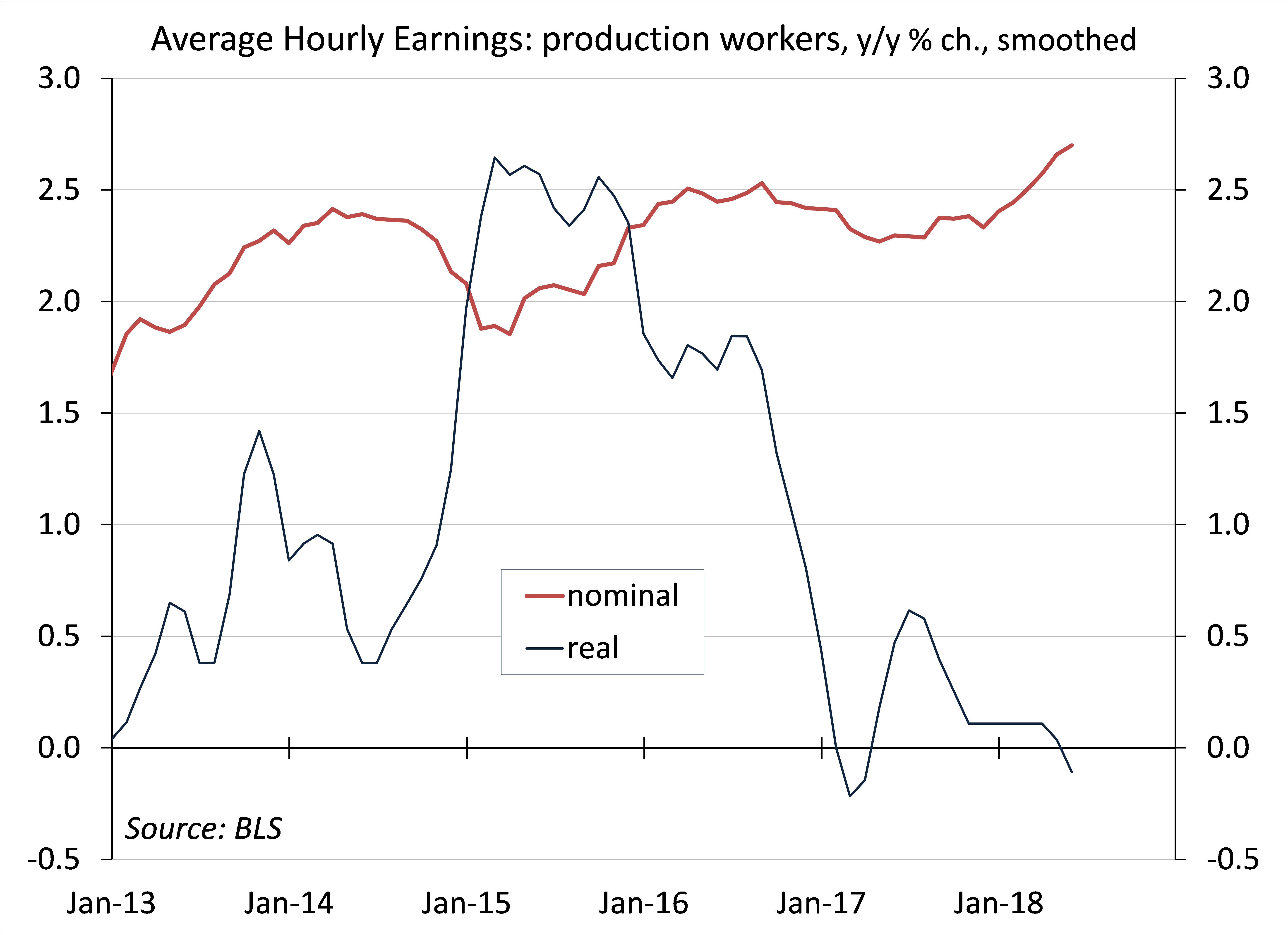

Real Hourly Earnings rose 0.1% in the initial estimate for June (unchanged y/y).

Chart 3

Click here to enlarge

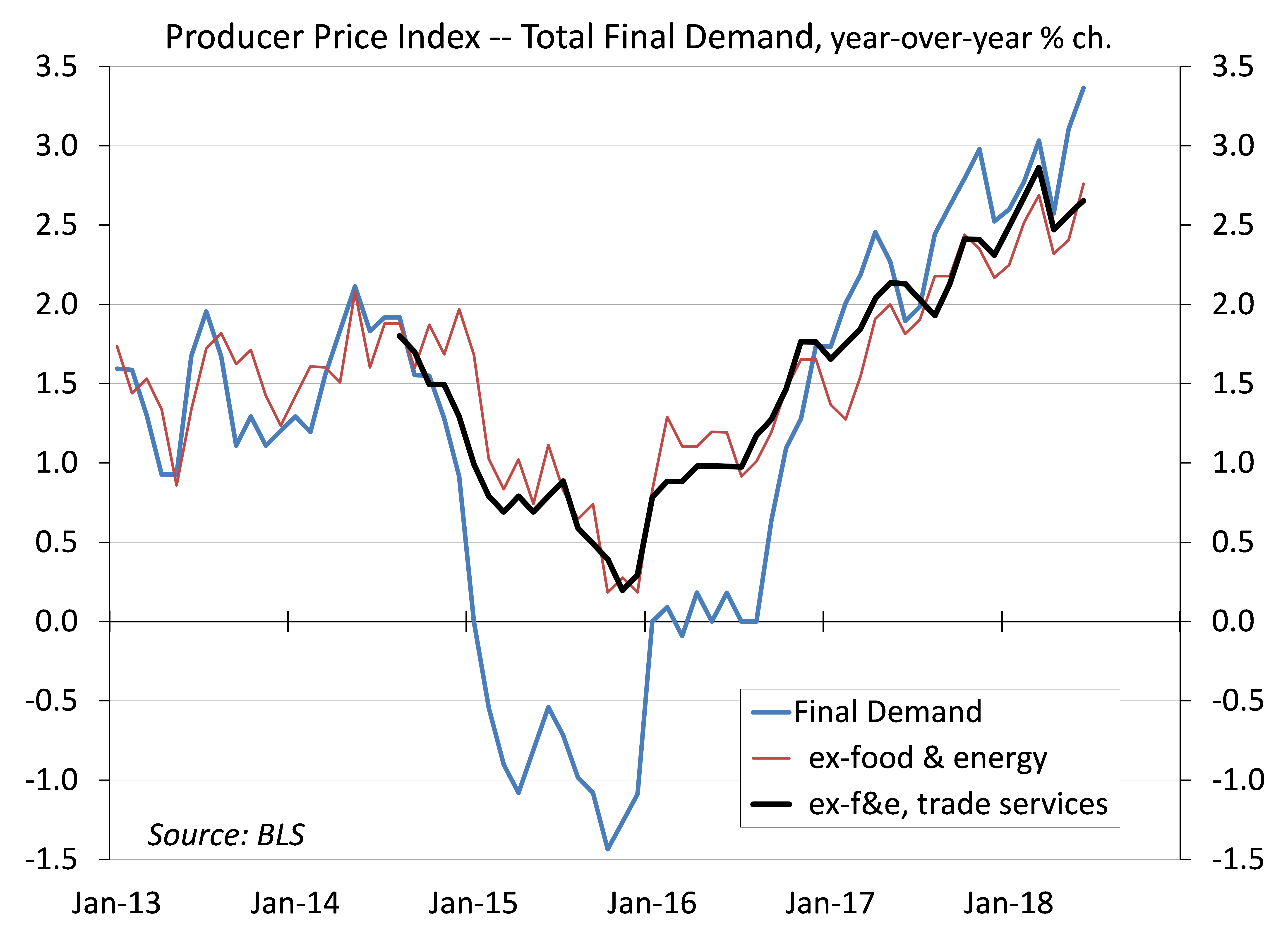

Chart 4

Click here to enlarge

The Producer Price Index rose 0.3% in June (+3.4% y/y). Food fell 1.1% (-1.0% y/y), while energy rose 0.8% (+17.2% y/y) and trade services rose 0.7% (+3.1% y/y). Ex-food, energy and trade services, the PPI rose 0.3% (+2.7% y/y).

Import Prices fell 0.4% in June (+4.3% y/y), reflecting a 2.6% drop in food, feeds, and beverages (-2.1% y/y). Petroleum fell 0.8% (+37.9% y/y), while natural gas fell 6.0% (-27.8% y/y). Ex-food & fuels, import prices edged down 0.1% (+1.8% y/y), with prices of industrial supplies and materials up 0.3% (+18.8% y/y). There was little or no inflation in finished imported goods. Capital goods slipped 0.1% (+0.6% y/y), autos edged down 0.1% (0.0% y/y), and consumer goods fell 0.3% (+0.3% y/y).

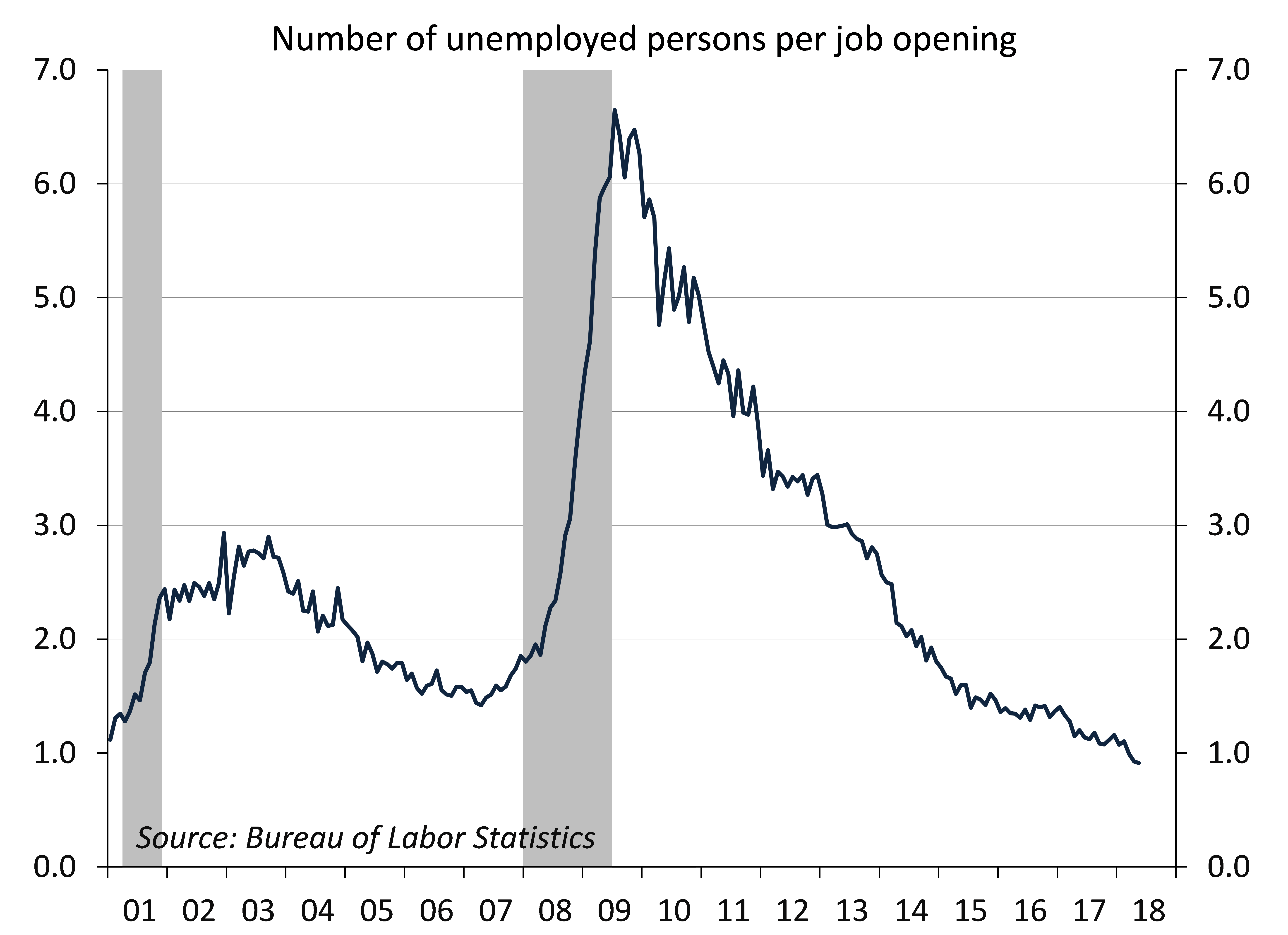

Jobless Claims fell 18,000 in the week ending July 7, but it’s not unusual for the figures to be distorted around major holidays. The four-week average was 223,000, consistent with a further tightening in labor market conditions.

Chart 5

Click here to enlarge

Chart 6

Click here to enlarge

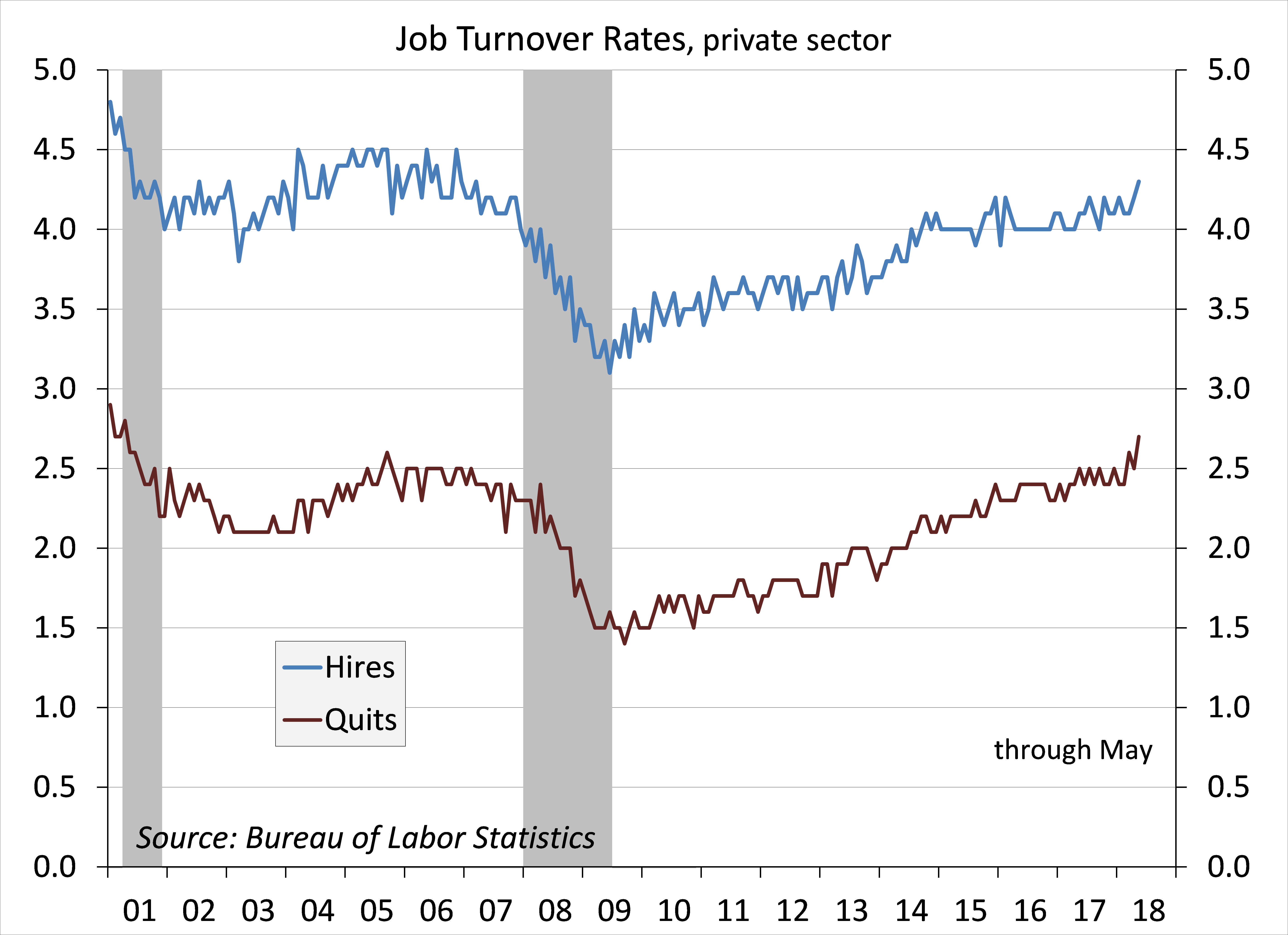

The Job Opening and Labor Turnover Survey (JOLTS) data for June were consistent with a further tightening of job market conditions. The hiring rate (for the private-sector) rose to 4.3%. In a strong job market, workers are more likely to quit to pursue employment elsewhere. The quit rate rose to 2.7% in May, the highest since April 2001.

Chart 7

Click here to enlarge

Chart 8

Click here to enlarge

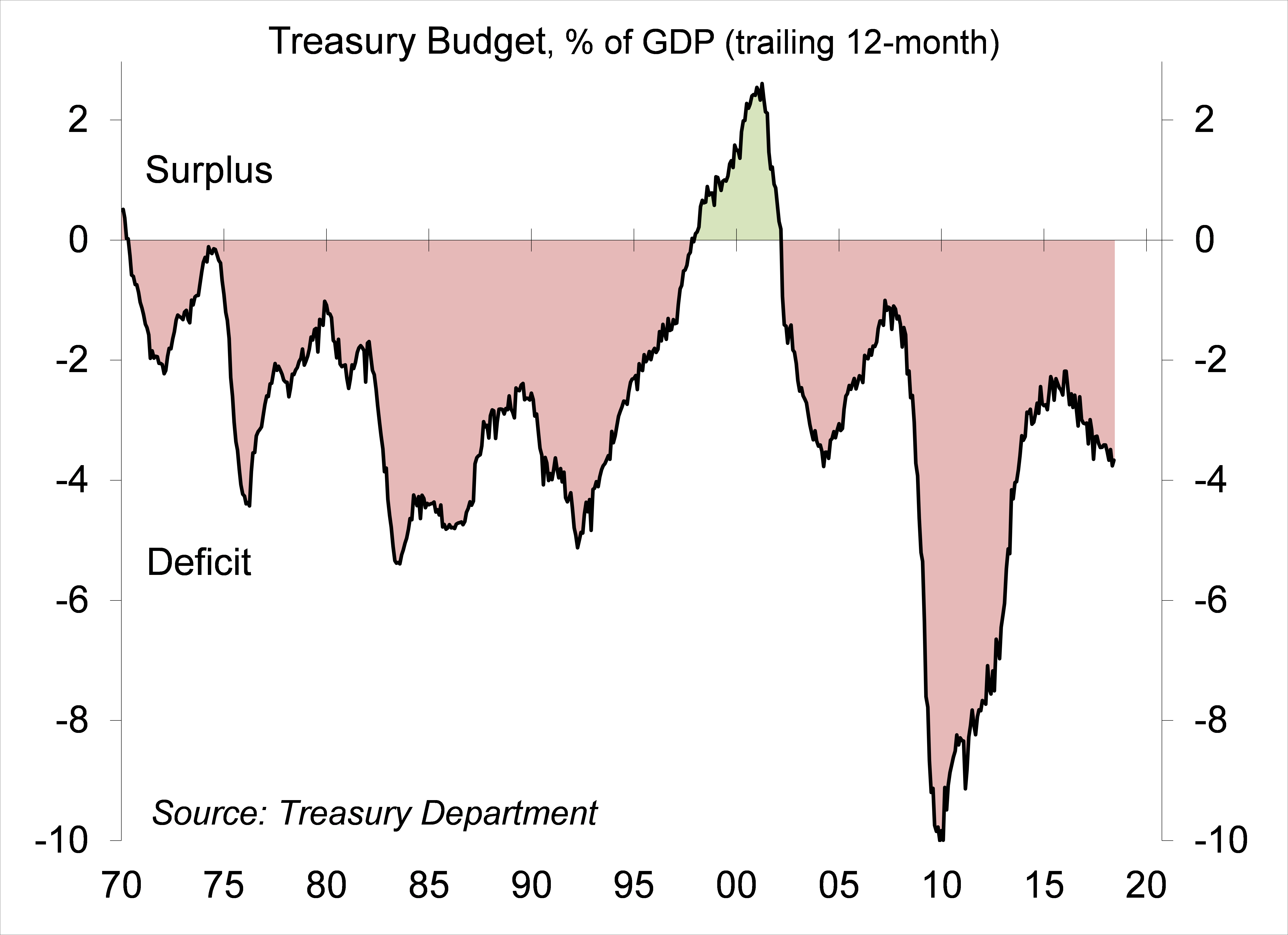

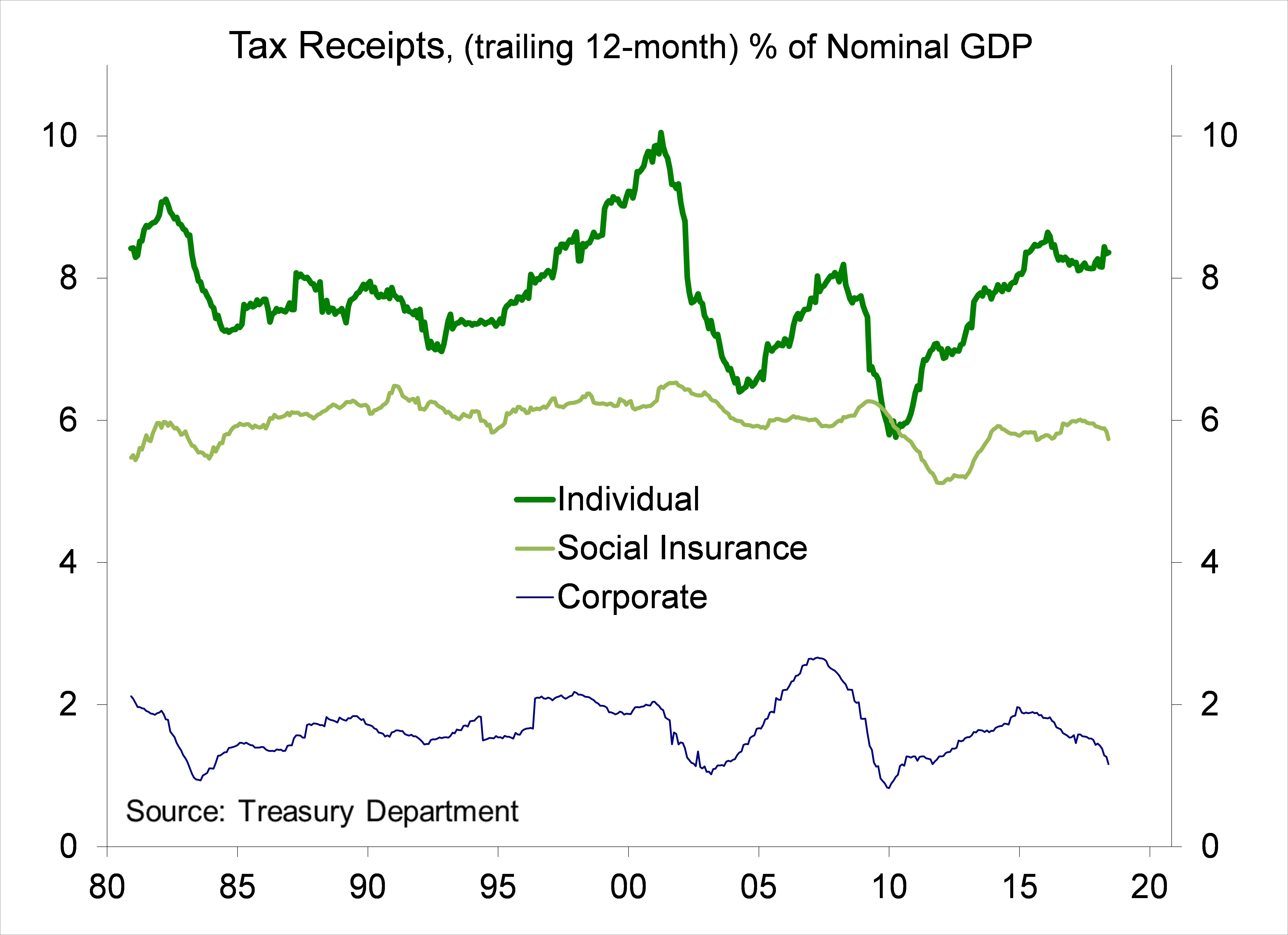

Treasury reported a $74.8 billion Budget Deficit for June (vs. $90.4 billion in June 2017). For the first nine months of FY18, the deficit totaled $608 billion, vs. $523 billion for the first nine months of FY17. Corporate tax receipts were down 27.6% y/y.

The University of Michigan’s Consumer Sentiment Index edged down to 97.1 in mid-July, vs. 98.2 in June, near the 12-month average (97.7). Sentiment continues to be supported by favorable job and income prospects, with those under the age of 45 anticipating the largest income gains since July 2000. The report also showed growing concerns about the potential negative impact of tariffs (“the primary concerns expressed by consumers were a decline in the future pace of economic growth and an uptick in inflation”). According to the report, “while consumers may not understand the intricacies of trade theory, they have substantial experience making decisions about the timing of discretionary purchases based on prospective trends in prices.”

The Index of Small Business Optimism edged down to 107.2 in June, vs. 107.8 in May, still elevated by historical standards.

The Bank of Canada raised its target for the overnight rate by 25 basis points, to 1.5%, noting that the economy was operating close to its capacity. The BOC expects that further gradual increases will be warranted.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James