1. The Treasury Yield Curve Has Narrowed Significantly

2. Why an Inverted Yield Curve is Bad For the Economy

3. Economists’ Survey: Next Recession in 2020 or 2021

Overview

The “yield curve” has been a popular topic of discussion this year. The yield curve is the spread between interest rates at various maturities, typically among Treasury securities. Normally, there is an interest rate premium the further you go out on the maturity scale (1-year, 2-year, 5-year, 10-year, 20-year and 30-year).

The reason the yield curve has been getting so much attention this year is because the spreads between short-term interest rates and longer-term maturities have been narrowing. Some forecasters fear that the yield curve could “invert,” meaning that short-term rates rise above longer-term rates.

The reason this is important is because historically the yield curve has inverted about a year in advance of recessions. Recessions, of course, are usually bearish for stocks. In particular, traders watch the spread between the 2-year and the 10-year Treasury Notes, which has narrowed considerably this year.

While the US economy looks quite strong and may register 4+% GDP growth in the second half of this year, this economic recovery is quite old compared to most past business cycles. So, a recession in the next few years would hardly be a surprise. This explains all the attention currently being paid to the yield curve. That’s what we’ll focus on today.

The Treasury Yield Curve Has Narrowed Significantly

The yield curve is a line on a graph plotting the difference between yields for debt of different maturities. Since investors typically demand a bigger premium to lend money over a longer period, the line usually curves upward.

The yield curve can vary significantly depending on a host of factors including the economy, interest rates, Fed monetary policy, bank lending trends, loan demand, savings rates, inflation, etc., etc. As noted above, there is normally a higher interest rate premium the farther you go out on the maturity scale.

For the last several years, the yield curve has been narrowing or flattening, meaning that the spread between the various maturities has gotten smaller. Currently, the yield on the 2-year Treasury Note is 2.53% (highest since 2008), the 10-year is at 2.82% and the 30-year is at 2.94%.

Although not inverted, these rates are very, very narrow. The spread between the 2-year and the 10-year fell below 30 basis points (0.29%) last week for the first time in 11 years, as you can see below.

Several factors are contributing to the narrowing of the yield curve, but chief among them is the Fed’s policy of “normalizing” short-term interest rates. The Fed Open Market Committee (FOMC) raised the Fed Funds rate a second time this year in June and signaled it will raise the rate two more times this year and 2-3 times in 2019.

The Fed Funds rate is the rate of interest banks charge each other for overnight lending of reserves. These increases in the Fed Funds rate tend to drive the short end of the yield curve higher while the longer maturities tend to rise less, stay flat or even decline in some cases.

As noted above, a growing number of forecasters believe the yield curve could invert before long with short-term rates rising above long-term rates. I’m not so convinced that will happen but with several more Fed rate hikes to come, we can’t rule it out.

Why an Inverted Yield Curve is Bad For the Economy

With the Fed’s confirmation last month that there will be two more rate hikes this year instead of just one and potentially several more next year, more investors are worrying that the Fed may be applying the brakes too hard. This is raising concerns that we could be headed for a recession.

History shows that inverted yield curves have often preceded financial crises, which was the case in 2001 and 2006 when recessions followed. In fact, in five of the past six times the yield curve inverted, a recession followed.

Of course, the yield curve is nowhere near inverting now, and economic growth is expected to be strong the rest of this year thanks to deregulation, tax cuts and increased federal spending.

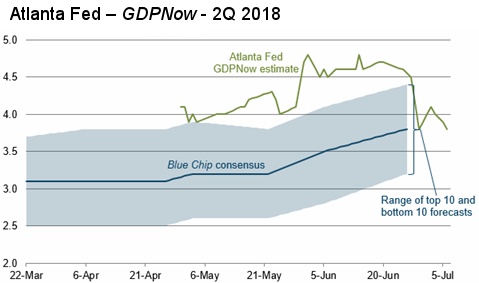

The Atlanta Fed now estimates that the economy is growing at a 3.8% pace in the 2Q, although that’s down from their 4.5% estimate on June 20. It will be interesting to see the government’s first estimate of 2Q GDP which will be out near the end of this month.

Economists believe an inverted yield curve is a harbinger of an economic slowdown for two reasons primarily. One, banks rely on short-term deposits to fund longer-term loans, harvesting the difference in interest rates. Because the net interest margin broadly correlates with the yield curve’s steepness, an inverted curve suggests banks would cut back on making loans, thus hurting business investment.

Two, a yield curve inversion confirms that Fed monetary policy has become very tight, with short-term yields rising much faster than the long-term yields.

An inverted yield curve can affect you in a number of different ways depending on your financial situation. For example, if you’re a long-term investor and have money tied up in long-dated bonds, you’re typically going to see interest rates for those bonds go lower than short-term ones. This can be alarming to investors.

Also, if you have an adjustable-rate mortgage, there’s a good chance your interest rate schedule is predicated on the current short-term bond interest rate. That means that if those rates are higher, you’re going to end up paying more in interest.

Interestingly, an inverted yield curve in the US is far more predictive of a recession than in most other countries. Analysts at AQR Capital Management found that the inverted yield curve’s prophetic reputation was either non-existent or weak in major economies from Australia to Germany.

In closing, there is growing concern about the yield curve inverting in the US later this year. As I was doing the research for this piece, I saw a couple of predictions that the curve could invert as early as September 26 when the Fed wraps-up its next major policy meeting.

It is widely expected that the FOMC will hike the Fed Funds rate another 25 basis points at that meeting. If rates stay roughly where they are today, that won’t be quite enough to invert the curve but it will make it even flatter. That does raise the odds that the curve could invert on December 19 when the FOMC is likely to raise the rate yet another 25 basis points.

In any event, I’ll keep you posted.

Economists’ Survey: Next Recession in 2020 or 2021 – Really?

The Wall Street Journal recently surveyed 60 well-known economists and asked when they expect the next US recession will come. Almost 60% of these supposedly learned economists predicted the next recession will come in 2020. Another 22% said it would come in 2021. So, over 80% of leading economists say the next recession is 2-3 years away.

I bring this to your attention only to make one point. I think it is ridiculous that these mainstream economists believe they can predict when the next recession will occur. I assure you they have no clue! No one knows when the next US recession will unfold.

Currently, it is widely believed that the US economy will accelerate in the second half of this year. Many forecasters have revised their estimates of second-half 2018 GDP to 4% or better. And the consensus is that this strong growth will continue at least into the first half of 2019. That has been my thinking as well.

But I can tell you that no one knows what will happen beyond a year from now. The global debt bubble could explode at any time, and a new financial crisis could be upon us. Maybe it happens late next year, or in 2020 or 2021, or maybe it’s several more years in the future. The point is, no one knows.

The most likely cause of the next recession cited by the economists surveyed in May was higher interest rates brought on by Fed tightening. While the Fed has made it clear it wants to raise short-term interest rates, it does not want to engineer a recession in doing so.

My point is, when you read these (stupid) surveys of leading economists predicting the future, take them with a grain of salt. No one knows when the next recession will unfold. No one knows when the debt bubble will explode. And anyone who says they do should be ignored.

I’ll leave it there for this week. Thanks as always for reading! I welcome your comments and suggestions, really I do.

All the best,

Gary D. Halbert

© Halbert Wealth Management

© Halbert Wealth Management

Read more commentaries by Halbert Wealth Management