Nonfarm payrolls rose more than expected in June, but the unemployment rate rose and average hourly earnings rose moderately. That’s a seemingly sweet combination for investors. The economy remains strong, but not so much that the Fed has to slam on the brakes. Still, the central bank is widely expected to raise short-term interest rates further and the broad range of labor market data paint a somewhat puzzling picture.

Recall that the employment report consists of two separate surveys. The establishment survey, which covers about 149,000 businesses and approximately 651,000 worksites, yields estimates of nonfarm payrolls, average weekly hours, and average hourly earnings. The household survey, which is based on a sample of 60,000 households, generates estimates of labor force participation and the unemployment rate. The size of the household survey is small, too small to give us accurate estimates of levels (such as the size of the labor force or total employment), but large enough to yield reasonably accurate measures of ratios (such as the unemployment rate and labor force participation). Still, statistical uncertainty and seasonal adjustment add noise to the job market figures. The monthly change in nonfarm payrolls is reported accurate to ±115,000 (that’s a 90% confidence interval for those of you who stayed awake in statistics class). The unemployment rate is reported accurate to ±0.2%.

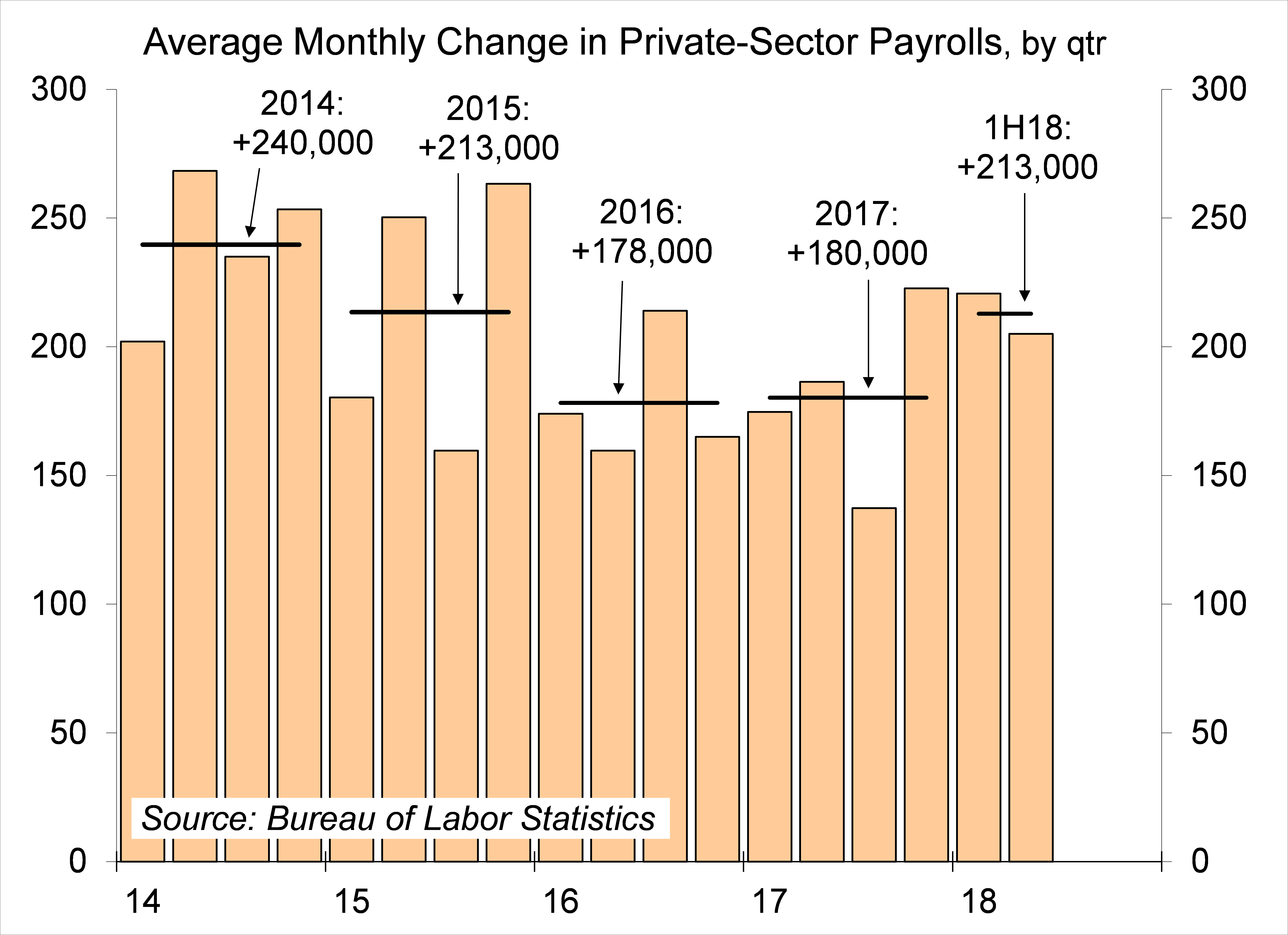

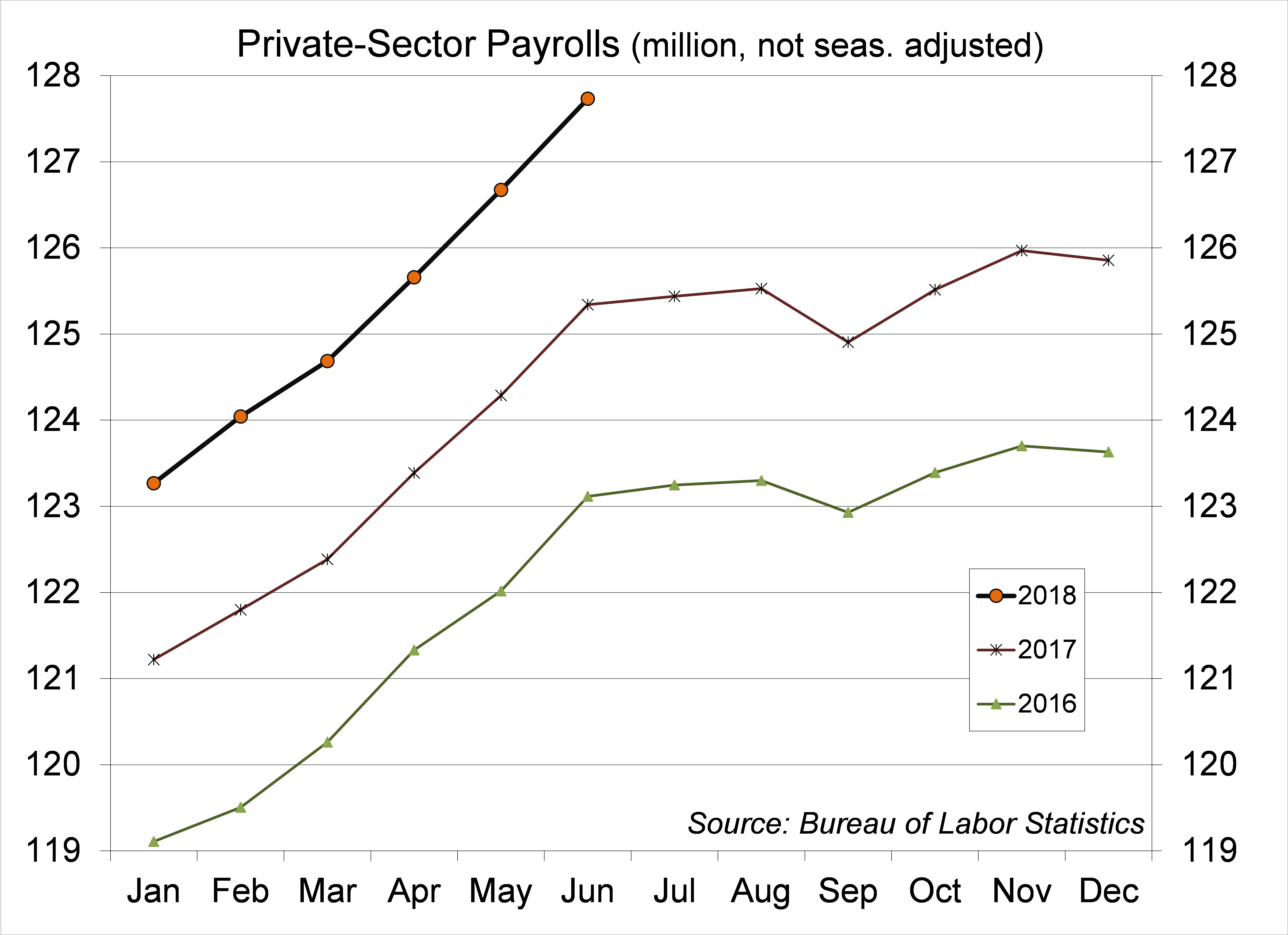

The impact of noise in the establishment data can be reduced by taking the three-month average. Private-sector payrolls averaged a 205,000 monthly gain in 2Q18, a bit less than the first quarter’s 218,000 pace, but higher than the average of the last two years. That may not mean much. These figures will be subject to annual benchmark revisions (derived from actual payroll tax receipts) next February, but the results are consistent with other indicators of labor market strength. We need a little less than 100,000 jobs per months to absorb new entrants into the workforce – so the recent pace of job growth is unsustainable over the long run.

Chart 1

Click here to enlarge

Chart 2

Click here to enlarge

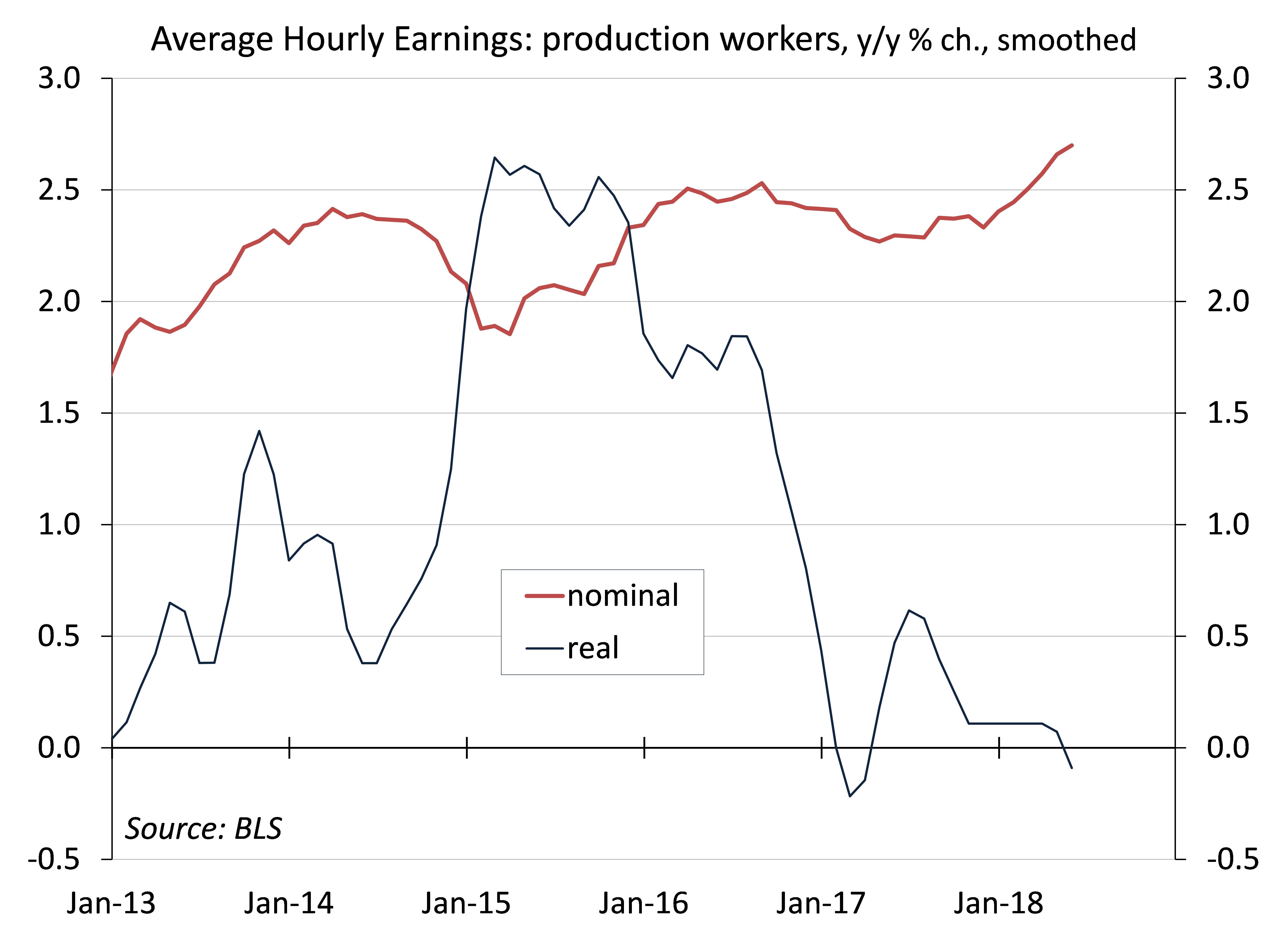

Tighter labor market conditions are making it more difficult for businesses to hire qualified workers. Normally, that would lead to a pickup in wage growth. Average hourly earnings are rising at a more rapid rate than in recent years, but far from the pace that we would normally associate with such a strong job market. There are a number of reasons for this. Union membership has fallen significantly in recent decades and we have a greater concentration of large firms, shifting the wage bargaining power away from labor and towards employers. There are also some business behavioral changes. Perhaps aware that we will run into a recession sooner or later, firms appear reluctant to make long-term commitments. In lieu of raising salaries for all workers, firms are attracting new workers by offering signing bonuses, more time off and other perks, and providing stipends to pay down student debt (this ought to show up in the more comprehensive Employment Cost Index (2Q data due July 31).

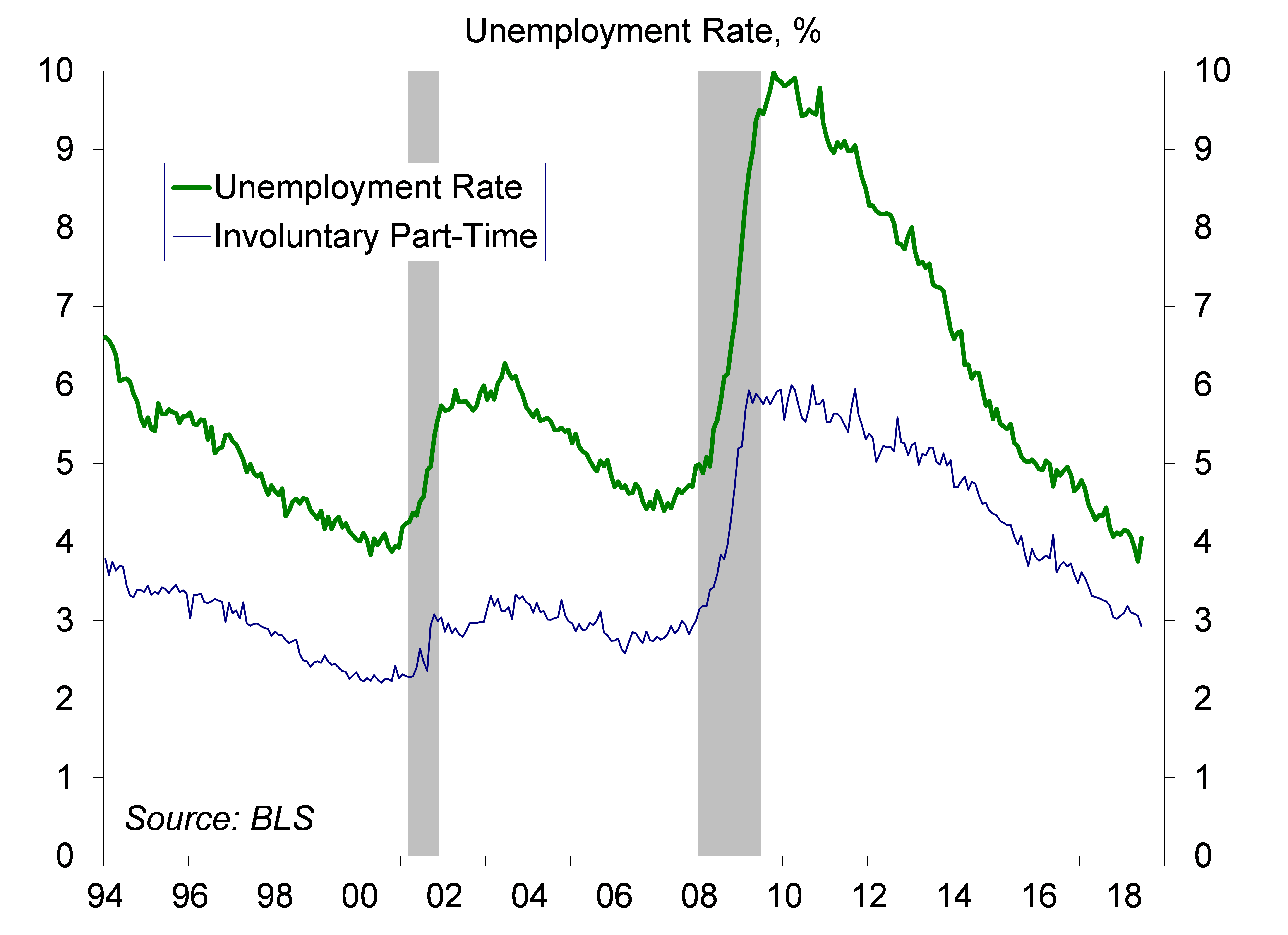

The unemployment rate rose to 4.0% in June, after dipping to 3.8% in May, but the difference is within the normal statistical uncertainty. Labor force participation is trending about flat, which is a sign of strength in the current environment (where the aging of the population should lead to a natural downtrend).

Trade policy conflicts have already had an impact on some industries, but the overall effect on the economy has been small. That will likely change as tensions escalate, mostly through higher input costs, supply chain disruptions, and greater uncertainty for fixed investment. Fed officials see trade policy as a risk to the economic outlook, but there’s no indication (so far) that the central bank will pause – and FOMC minutes confirmed that officials see the federal funds rate moving above a neutral level in 2019 or 2020.

Data Recap – The economic data reports were generally on the strong side of expectations. Financial market participants showed brief concern about escalating trade tensions.

The Trade War is officially underway, as the Trump administration imposed tariffs on $34 billion in Chinese goods, which is expected to be followed in a few weeks by increased tariffs on a further $16 billion of Chinese goods. China has indicated that it will retaliate with increased tariffs on U.S. exports, and the White House has indicated that it will retaliate against China’s retaliation, with additional tariffs on another $200 billion in Chinese goods.

The FOMC Minutes from the June 12-13 policy meeting showed that senior Fed officials saw “a number of factors supporting above-trend growth,” leading to the view that “it would likely be appropriate to continue gradually raising the target range for the federal funds rate to a setting that was at or somewhat above their estimates of its longer-run level by 2019 or 2020.” Officials felt that inflation was on track to reach the 2% goal, “although a number of participants noted that it was premature to conclude that the FOMC had achieved that objective.” Most meeting participants noted that “uncertainty and risks associated with trade policy had intensified and were concerned that such uncertainty and risks eventually could have negative effects on business sentiment and investment spending.”The slope of the yield curve was discussed, without any firm conclusions, but “several participants cautioned that yield curve movements should be interpreted within the broader context of financial conditions and the outlook, and would be only one among many considerations in forming an assessment of appropriate policy.”

The June Employment Report was mixed. Nonfarm payrolls rose by 213,000 in the initial estimate (median forecast: +195,000), with a net upward revision of 37,000 to April and May. Private-sector payrolls averaged a 205,000 monthly gain in 2Q18 (vs. +221,000 in 1Q18 and +180,000 in 2017). The unemployment rate rose to 4.0% (from 3.8%), but that likely reflects a rebound from a quirky drop in May. Average hourly earnings rose 0.2% (median forecast: +0.3%), leaving the year-over-year gain at 2.7% (in comparison, the Consumer Price Index 2.8% over the 12 months ending in May).

Chart 3

Click here to enlarge

Chart 4

Click here to enlarge

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James