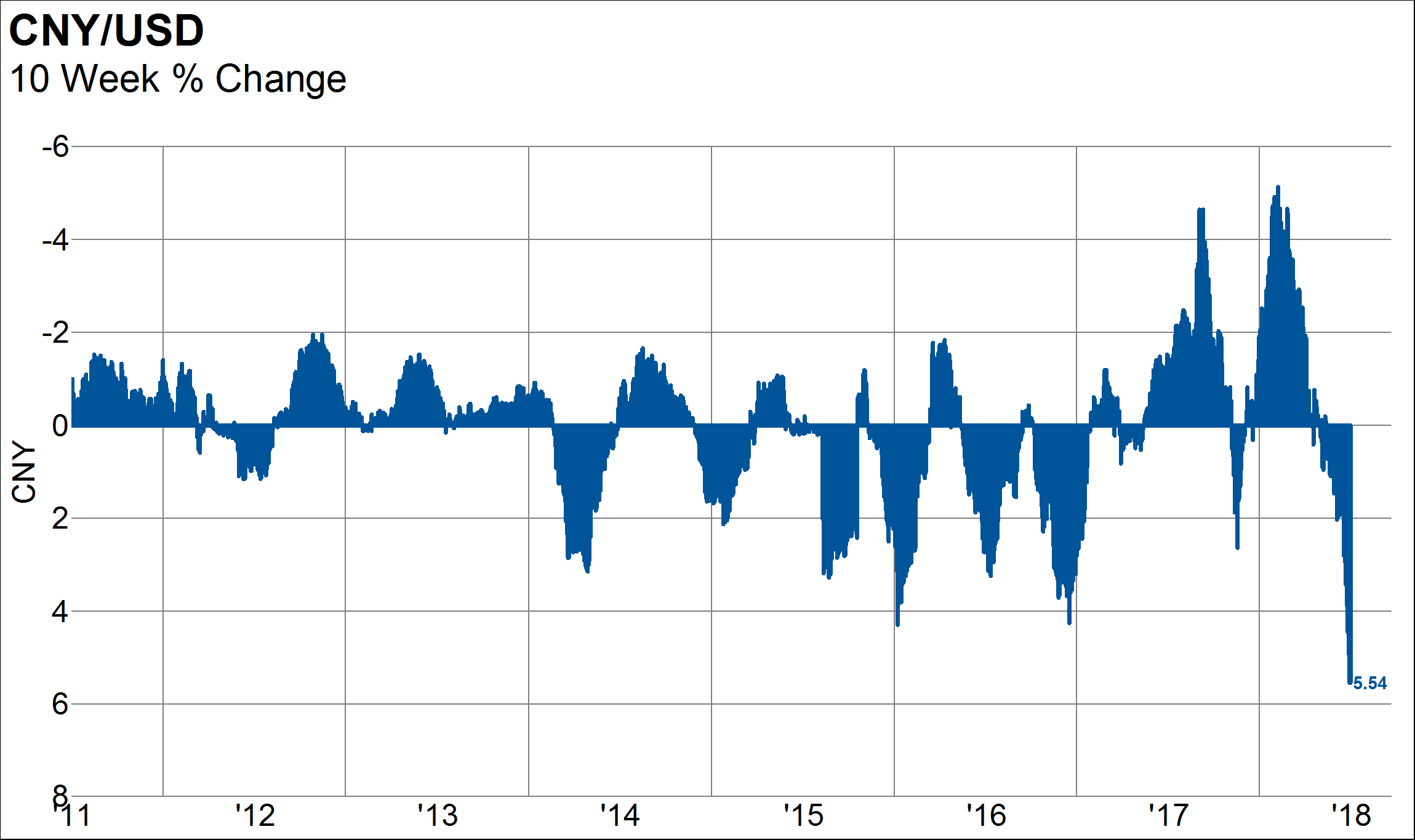

The Chinese Yuan has fallen precipitously in the last 10 weeks raising concerns of whether China was using the currency as a weapon to preemptively mitigate looming tariffs. A 6% devaluation over the last 10 weeks is a larger move than experienced in 2015/16. The timing and magnitude of the devaluation is suspicious to say the least, coming on the heels of President Trump’s ramping up trade war rhetoric.

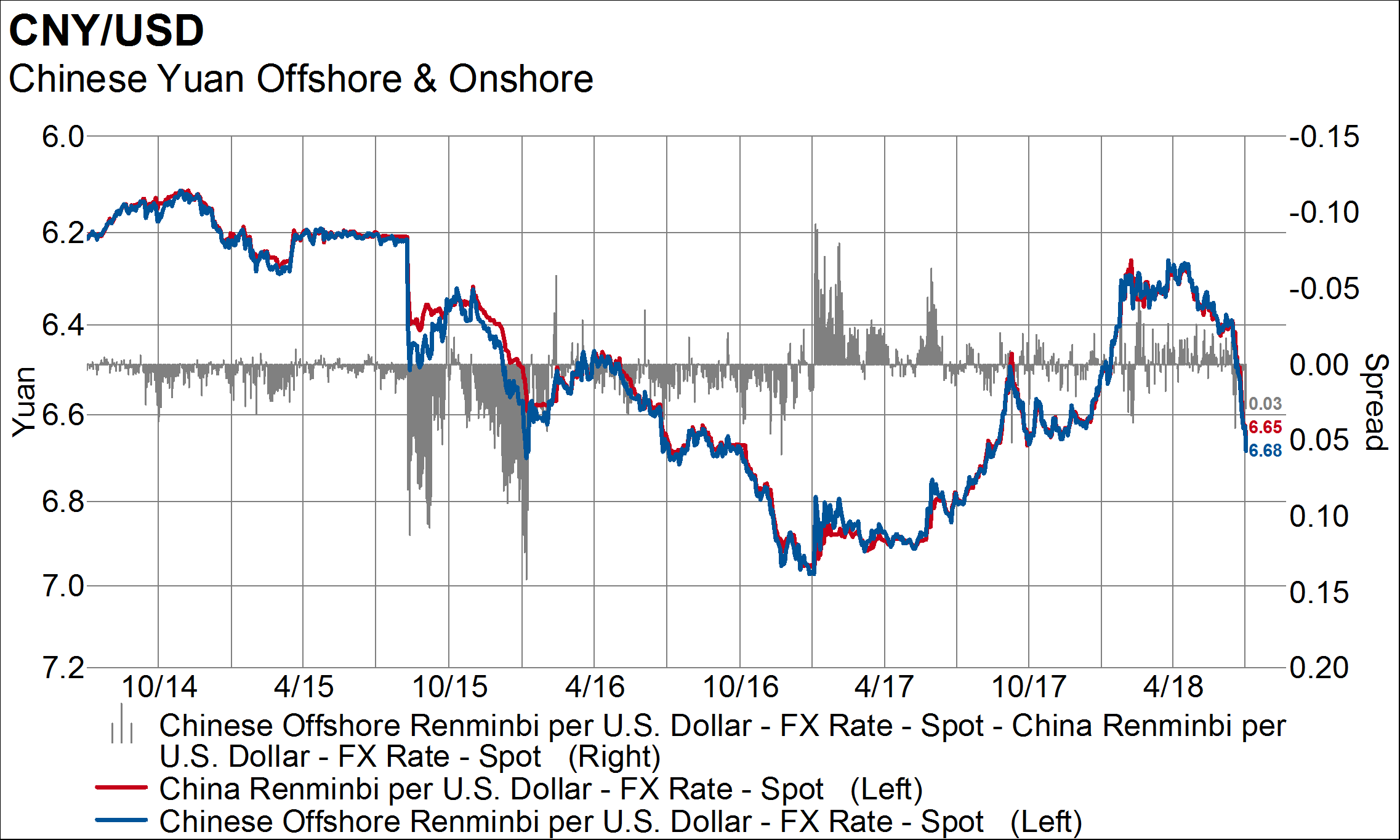

In this round of CNY/USD devaluation, there are some differences with the 2015/16 experience. First, there is little evidence that the devaluation has been driven by Chinese citizens trying to get money out of the country. The barometer we use to measure this is the spread between the onshore and offshore Yuan. When residents want to get money out of the country, a spread opens up between the two markets reflecting the acceptance of a discount to cash out. The CNY/CNH spread widened to .10-.15 in September 2015 and January 2016. Currently, the spread is about .03, well within the normal historic range.

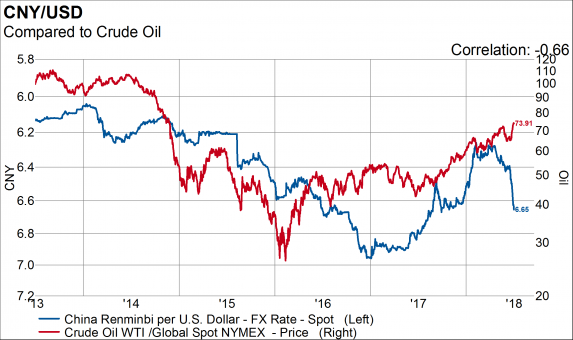

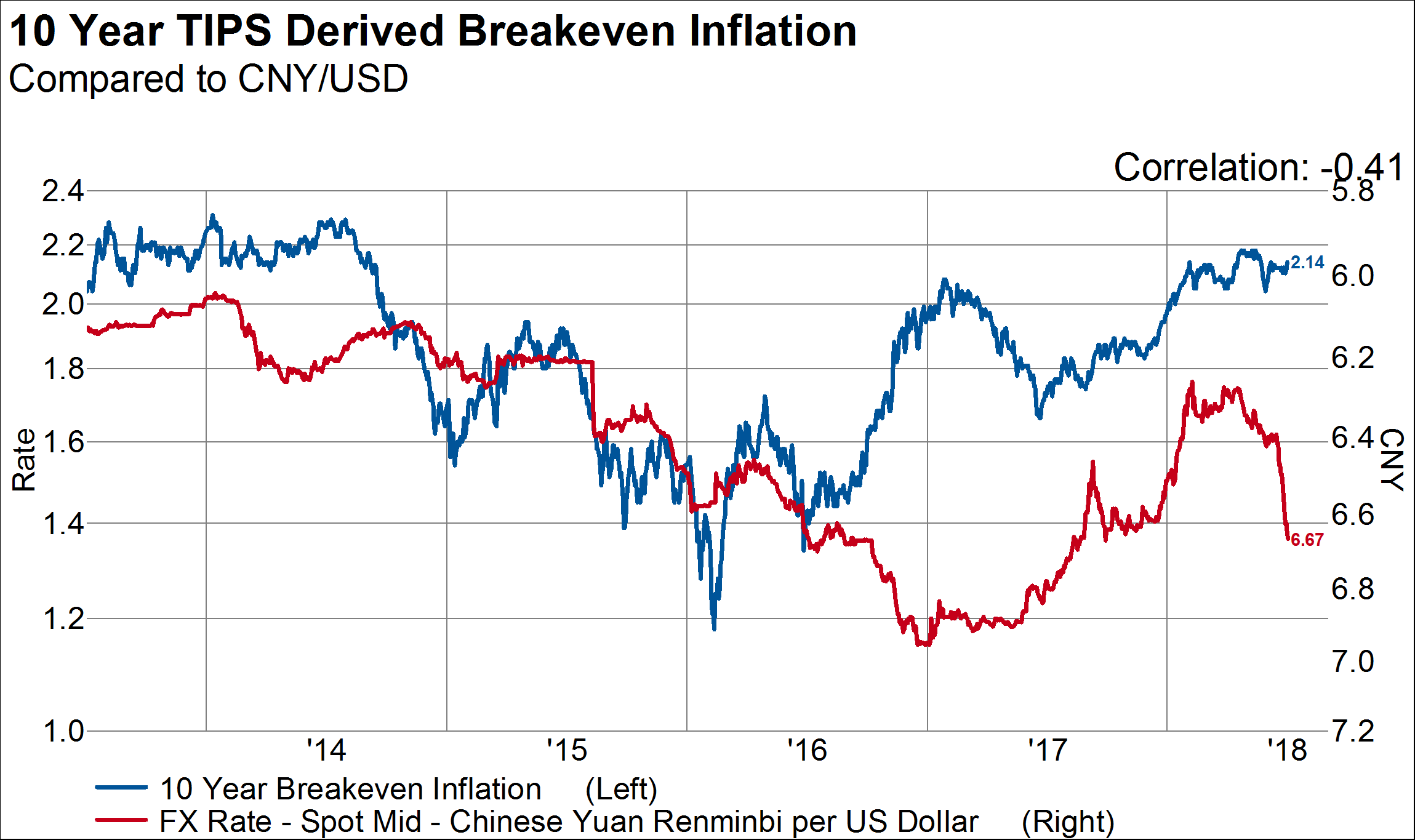

Second, in 2015/16 the CNY was falling alongside oil prices. In the September 2015 episode, oil fell almost a third and in the January 2016 episode, oil prices fell almost 50%. This time, oil prices have risen about 20% while the CNY has been falling. All else equal, rising oil prices should be the backdrop for the CNY to rise given that China is a huge oil importer.

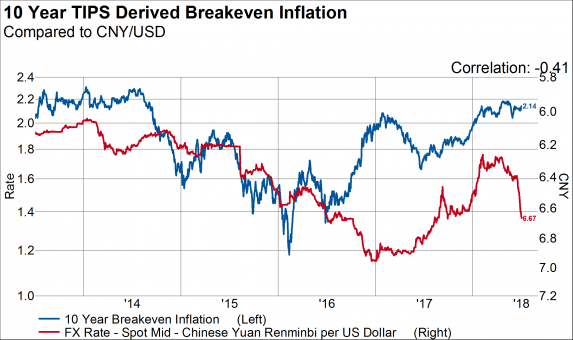

Third, inflation expectations are not collapsing like they did in 2015/16. From July 2015 to February 2016, inflation expectations fell from 1.9% to 1.2%. This time, inflation expectations have actually risen slightly since the CNY began depreciating.

I think these elements add up to a different kind of devaluation than we saw in 2015/16, one that may prove more temporary. Generally, oil prices move inversely to the USD broadly. Over the last five years, there is a 92% correlation between oil prices and the USD. While the CNY has been falling, a gap has opened between the USD and oil.

Oil prices have been driven by fundamental factors, crystallized by the days supply of crude oil inventory (inventory relative to demand). Over the last 18 months, as the global oil market has begun to come back into balance, the USD has been under pressure. As the USD has risen over the last few months, the crude oil market has gotten tighter.

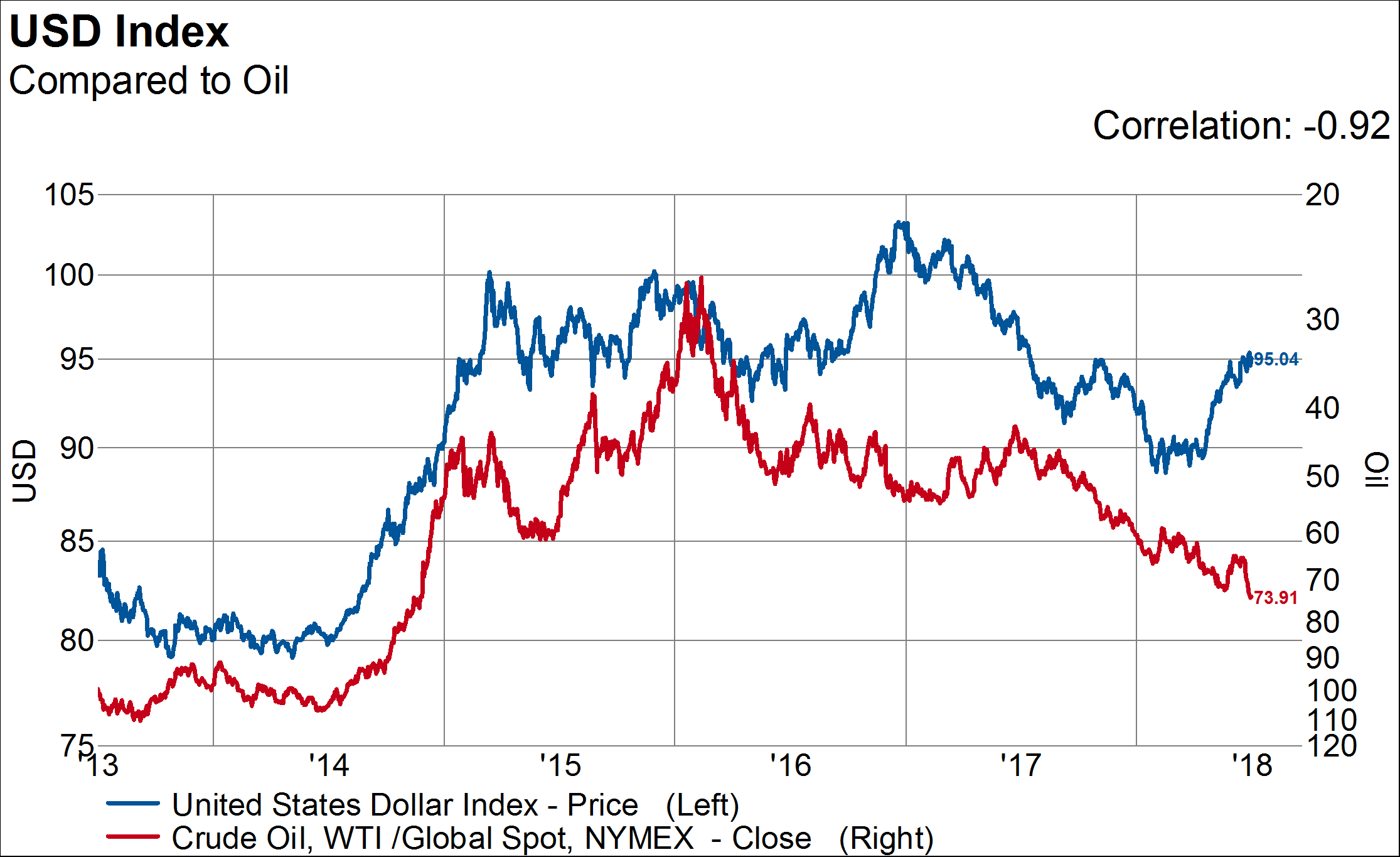

Higher oil prices are likely to push interest rates back up. With oil making new highs, not just for the year, but for the last four years, 30-Year US Treasury yields should push back to 3.2% and maybe higher.

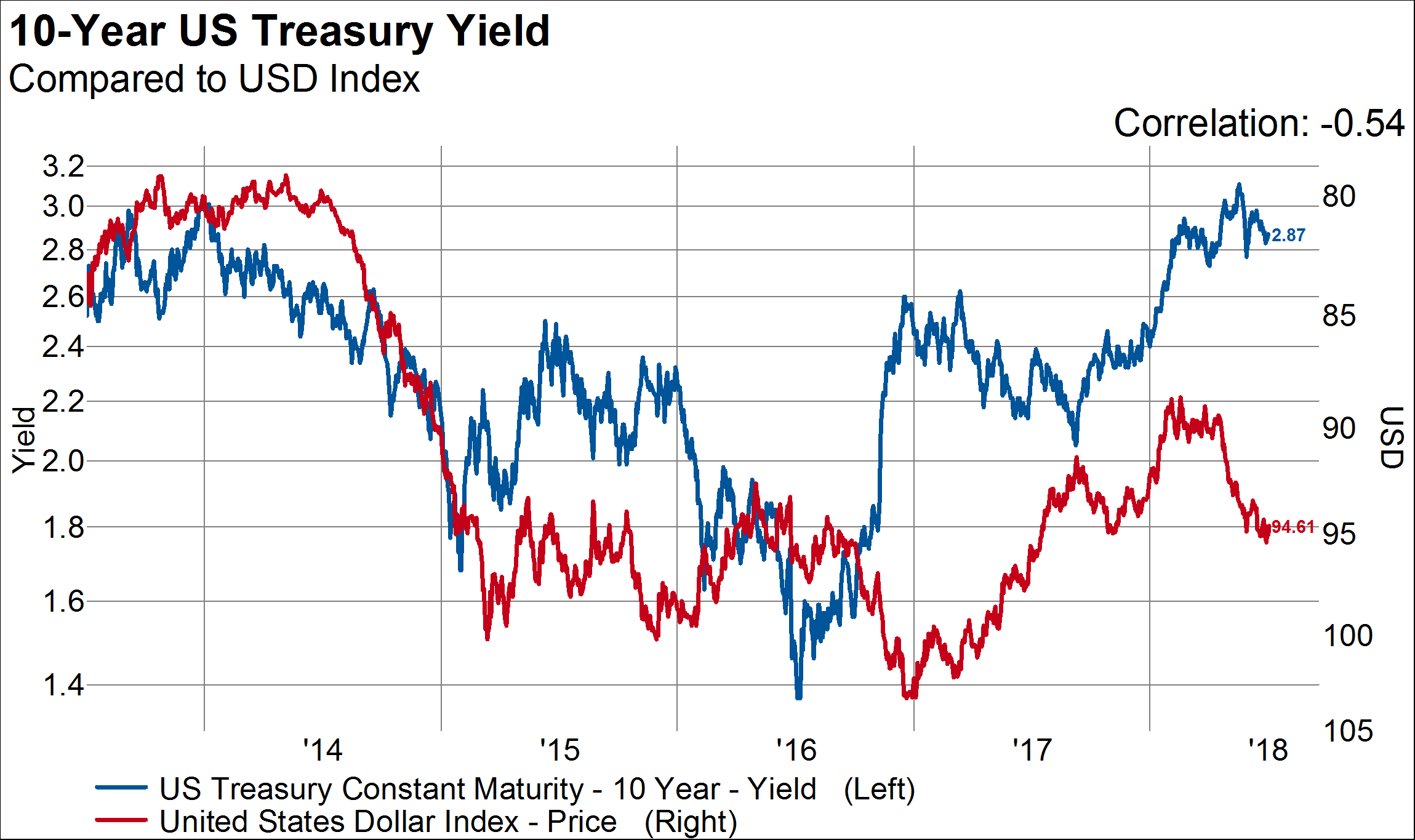

Despite many believing otherwise, the USD is negatively correlated to interest rates. Over the last five years, a weaker USD has been associated with higher interest rates.

So, is this CNY devaluation different? Yes, in many ways, that suggests the fundamental motivation is a top-down preemptive strike against looming US tariffs rather than a bottoms-up desire to liquidate CNY by Chinese residents. Economic fundamentals don’t seem to support a Chinese devaluation, which leaves only the conclusion that it is inspired by political motivations.

© Knowledge Leaders Capital

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital