The year began with two key themes. The first was that the economy ended 2017 with a good deal of momentum that should have continued into early 2018. The second was that the outlook for the second half of the year was considerably more clouded, reflecting fiscal stimulus, more binding constraints in the labor market, and tighter monetary policy. As is often the case, the economy was mixed in the first half of 2018, but remains in generally good shape. Growth is expected to slow in the second half of the year, but remain moderately strong. At the same time, the odds of recession for 2019 or 2020 have ticked up.

Comprehensive benchmark revisions to the National Income and Product Accounts are set to be released on July 27 (along with the advance GDP estimate for 2Q18). This revision will further address the issue of residual seasonality (the fact that first quarter GDP growth has been significantly less than the average for the other three quarters of the year), likely shifting recent GDP growth figures around. As usual, investors place far too much emphasis on the headline GDP figure. Focus on the meat and potatoes.

Consumer spending accounts for 69% of GDP. Quarterly figures are often lumpy – strong one quarter, softer the next. This appears to have been the case in recent quarters. “Soft” first quarter figures were widely expected to be followed by stronger second quarter numbers. Indeed, personal spending data through May suggest an inflation-adjusted annual rate of 2.5-3.0% in 2Q18 (vs.

+0.9% in 1Q18 and +4.0% in 4Q17). That’s relatively strong, but it’s less than earlier expectations of a sharper rebound. Nominal wage growth has picked up, but that has been largely offset by higher inflation over the last 12 months.

Chart 1

Click here to enlarge

Chart 2

Click here to enlarge

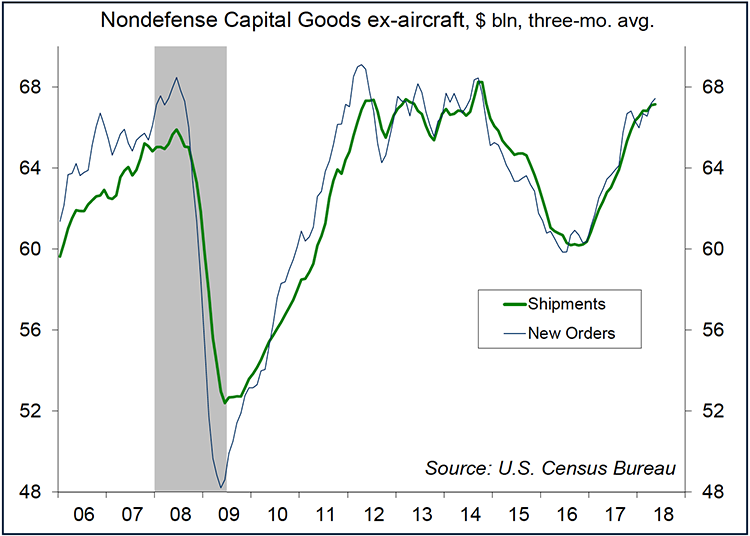

The corporate tax cut was supposed to lead to a significant increase in capital spending. Business fixed investment was strong in the first quarter, rising at a 10.4% annual rate (vs. 6.8% in 4Q17). However, strength was concentrated in structures (partly reflecting the further recovery in energy exploration) and intellectual property products (which may not be as strong in 2Q18). Spending on business equipment was moderate, but at the slowest pace since 4Q16. Moreover, shipments of nondefense capital goods ex- aircraft were on a slower trend in the first two months of 2Q18. Year-over-year gains in capital goods shipments still remain strong, reflecting robust growth in the second half of last year. Business sentiment remains enthusiastic, and new orders for capital goods appear to have accelerated into the second quarter (after slowing sharply in the first quarter).

There are increasing reports of a lack of skilled labor in a number of industries. The Fed’s most recent Beige Book noted that some firms are forgoing additional output because of labor shortages. The unemployment rate fell to 3.8% in May and measures of underemployment have continued to decrease. The second half GDP outlook rests partly on the issue of how much slack remains in the labor market. However, the demographics argue that labor force growth will be significantly slower than in previous decades.

The White House has launched a trade war on three fronts (China, Canada and Mexico, and the European Union). Trade policy conflicts are a major source of uncertainty for the economy and the financial markets. To date, increased tariffs should have only a minor impact on GDP growth. However, an escalation of tensions may lead to more significant disruptions in the months ahead.

Federal Reserve policymakers always face a difficult challenge in a late-cycle economy. There are clear risks of raising short-term interest rates either too rapidly or not rapidly enough (and having to raise rates more rapidly later). Fiscal stimulus is still expected to provide support, but officials will continue to monitor the economy for signs of softness in the quarters ahead.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James