1. Our Shrinking Middle Class

2. Energy Prices Have Soared Higher

3. Shortage Drives Home Prices Higher

4. Introducing Broadmark Capital

Overview

The US economy continues to gain momentum. More and more forecasters are predicting GDP growth of 4% or better for the second half of this year. Yet while the economy is strengthening, many Americans are not fully benefitting from the improvement. Today, we’ll take a look at some of the reasons why.

Following that discussion, I’ll introduce you to an exciting new investment opportunity – Broadmark Capital – which invests in short-term real estate loans to homebuilders and commercial real estate developers. As you will see below, Broadmark’s two real estate funds have delivered very attractive, consistent returns with low drawdowns.

Broadmark’s real estate Funds are restricted to “accredited investors.” An accredited investor is an individual with a net worth of at least $1,000,000 (excluding the value of one's primary residence), or have income of at least $200,000 each year for the last two years (or $300,000 combined income if married) and have the expectation to make the same amount this year.

Let’s get started.

Why Many Americans Are Not Benefitting From the Strong Economy

I have written a lot this year about how the economy is strengthening and how Americans have benefitted from it and will continue to as the recovery gains even more momentum just ahead. However, there are many Americans who are not benefitting as much from the economic recovery, and that’s what I want to talk about today.

Last week after the Fed raised interest rates another quarter point, new Fed Chairman Jerome Powell stated: The economy is doing very well… The outlook for growth is very favorable.” And it is. The unemployment rate has fallen to 3.8% – the lowest since the late 1960's. Cosumer confidence is way up and spending is strong. Household wealth is up. Taxes are down. Factories are busy. Demand for homes is strong.

While these numbers collectively paint a picture of a vibrant economy, they don't reflect reality for many Americans who still feel far from financially secure, even though we are nine years into the economic expansion.

From drivers paying more for gas and families bearing heavier childcare costs to workers still awaiting decent pay raises and couples struggling to afford a home, people throughout the economy are straining to succeed despite the economy's gains.

When analysts at Oxford Economics recently studied American spending patterns, they found that the bottom 60% of earners are essentially having to draw on their savings just to maintain their lifestyles. Their incomes weren't enough to cover expenses. Millions of families still live paycheck-to-paycheck.

Most economists describe the economy as fundamentally healthy, a testament to the durable recovery from the 2008 financial crisis. Yet they also note that even many people who have jobs and are in little danger of losing them feel burdened and uneasy.

Here are some reasons why.

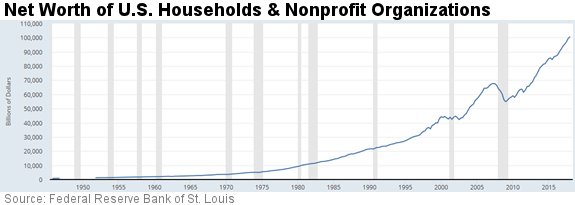

Our Shrinking Middle Class

The net worth of US households and nonprofit organizations rose to nearly $100 trillion in 2017, up $2 trillion last year alone and a new record, according to the Federal Reserve. The problem is, America's wealth is increasingly lopsided, with the affluent and ultra-wealthy amassing rising proportions of the total net worth and everyone else benefiting only modestly, if at all.

The top 10% of the country holds 73% of its wealth, a share that has crept steadily up since 1986, according to the World Inequality Database. The most sweeping gains are concentrated among the top 1%, which holds nearly 39% of the wealth, and they're arguably poised to become even more prosperous in the future.

Contrast that with the middle 40% of the country, a group that would historically be considered “middle class.” In 1986, they held 36% of the country's wealth; now, it's just 27%. So in terms of wealth, the middle class is shrinking. Worse off is the bottom 40% of Americans, most of whom have a negative net worth and almost no financial cushion in case of an emergency.

Most Americans can't draw on stocks, rental properties, capital gains or significant home equity to generate cash. They depend almost exclusively on wages. And after adjusting for inflation, the government reported that Americans' average hourly earnings have barely budged over the past 12 months, up only 2.7%.

Energy Prices Have Soared Higher

Even with inflation running at a relatively low 2.4%, one particular expense is weighing on anyone driving in traffic or commuting to work. Gasoline prices have surged 24% over the past year to a national average of $2.94 a gallon, according to AAA. That's the highest average since 2014.

Analysts at Morgan Stanley have estimated that the increase this year will likely eat away a third of people's savings from President Trump's tax cuts. While gas prices are still below their high reached roughly a decade ago, the increase this year represents an additional financial burden on consumers and businesses compared with a year ago.

Childcare Costs Are Accelerating

Children are immensely expensive. For nearly a third of families, the costs of childcare swallowed at least 20% of their annual income, according to a survey posted in March by the caregiver job site Care.com. Nearly a third of parents said they went into debt to cover childcare expenses.

When Care.com assessed how much its members were spending on daycare centers for infants yearly, the average cost was $10,486, and it ranged as high as $20,209. Nannies were even more expensive.

Some women remain outside the workforce because of the comparatively weak family leave and child care policies in the US relative to those in other developed economies. As a result, many families are forgoing income that would otherwise benefit them and the economy.

When the unemployment rate was last below 4%, the proportion of women who either had a job or were looking for one was peaking. For women ages 25 to 54, that proportion – called the labor force participation rate – was roughly 77% in 2000. It's now down to 74.8%.

Shortage Drives Home Prices Higher

A strong job market can actually be a curse for would-be homebuyers. With more people drawing paychecks and able to afford a home, demand has intensified. Yet the number of homes listed for sale is flirting with historic lows. The combination of high demand and low supply has driven prices to troubling high levels.

It's not just that home ownership is largely unobtainable in big cities. The real estate brokerage firm Redfin says the median sales price in the 174 markets it covers has jumped 6.3% over the past year to $305,600.

A general rule of thumb is that buyers can afford a home worth roughly three times their income. So, the median home sales price far exceeds what a typical US household earning a median $57,000 income can manage. As noted above, average hourly wages have risen just 2.7% over the past year.

On top of that, 30-year fixed-rate mortgages are growing costlier. The average interest rate on these mortgages jumped to 4.62% last month – up from 3.95% at the start of the year – according to mortgage buyer Freddie Mac.

These are just a few of the reasons why many Americans are not fully benefitting from the strong economic recovery.

All the best,

Gary D. Halbert

Forecasts & Trends E-Letter is published by Halbert Wealth Management, Inc. Gary D. Halbert is the president and CEO of Halbert Wealth Management, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgment of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, Halbert Wealth Management, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management

© Halbert Wealth Management

Read more commentaries by Halbert Wealth Management