The Federal Open Market Committee is widely expected to raise short-term interest rates by another 25 basis points following its June 12-13 policy meeting (bringing the target range for the federal funds rate to 1.75-2.00%). As with every other FOMC meeting, the Fed will release revised economic projections, including a new dot plot, and Chair Powell will conduct a post-meeting press conference. The key question for investors will be whether there will be one or two further rate increases by the end of the year. Market participants will look to the revised dot plot. However, the dots don’t tell the full story.

Click here to enlarge

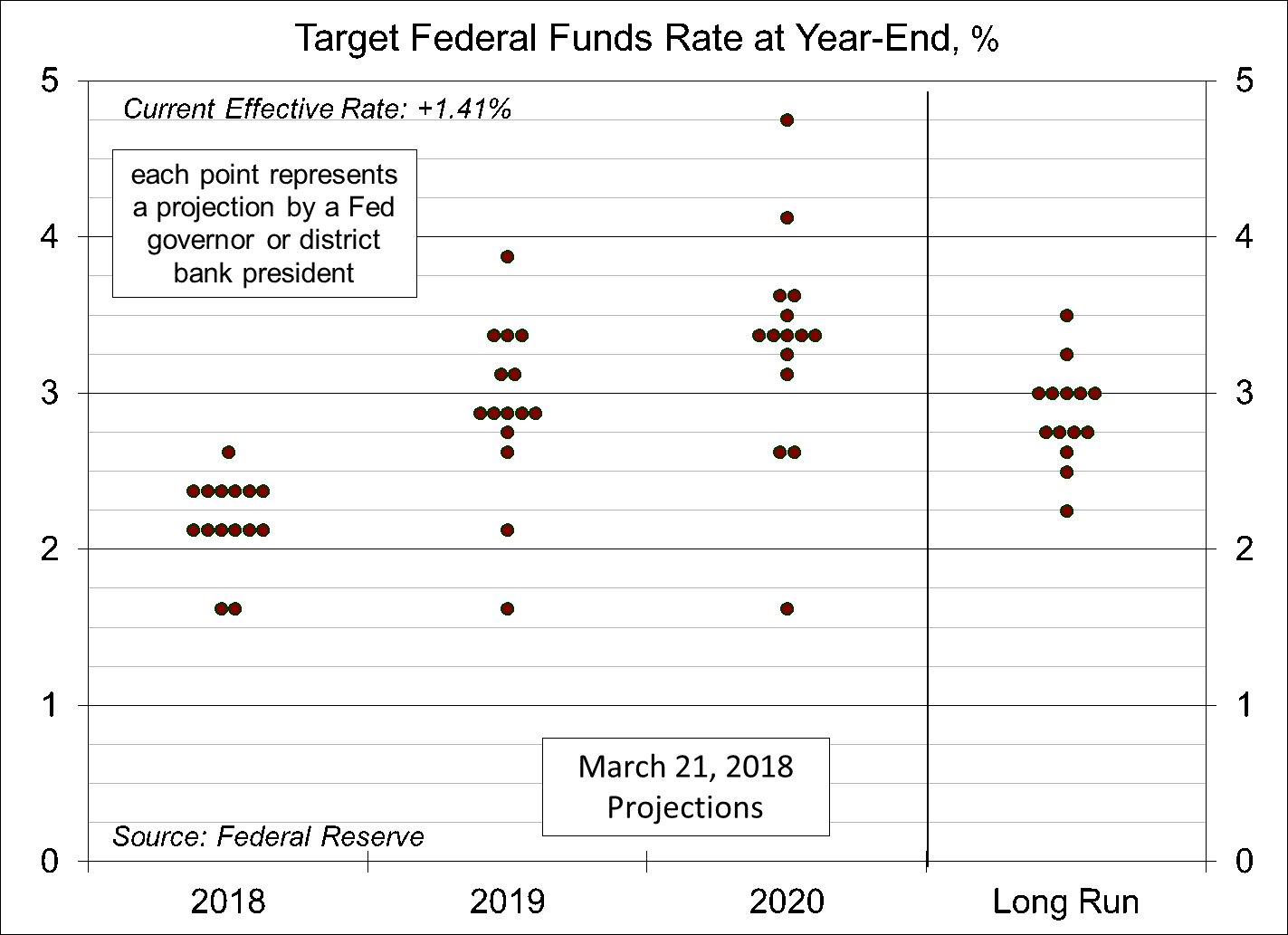

The Fed began publishing the dot plot in early 2012. The intent was to provide the public with the range of policy expectations. The dots represent senior Fed officials’ forecasts of the appropriate year-end federal funds rate. Only eight of the 15 dots are voting FOMC members (we don’t know which is which, and there are still four vacancies on the Fed’s Board of Governors). The Fed stressed that the dots “should not be viewed as unconditional pledges.”Rather, “these policy projections reflect the information available at the time of the forecast and are subject to future revisions in light of evolving economic and financial conditions.” Unfortunately, market participants have focused on the median of the dots, rather than on their range (in March, the median was for three rate increases this year, although the majority of the dots were evenly split between three and four).

During the financial crisis, the Fed began paying interest on bank reserves held at the Fed (something most other central banks had been doing for some time). Recall that the Fed requires banks to hold a certain portion of reserves at the Fed, but could hold more (these are “excess reserves”). The Fed pays the Interest on Required Reserves rate (IORR) on required reserves and the Interest on Excess Reserves rate (IOER) on the excess reserves (currently, both are 1.75%, the top of the federal funds target range). At this meeting, the Fed is expected to raise IOER by 20 basis points. This is a technical adjustment. The effective federal funds rate has drifted well above the Fed’s target range (currently 1.70%, vs. a target range of 1.50-1.75%).

The underlying rate of consumer price inflation has remained moderate. So why is the Fed raising rates? In the last couple of years, the Fed’s rate increases were about getting monetary policy back to a neutral position following an extended period of exceptionally low rates — taking the foot off the gas pedal. Now it’s about tapping the brakes in an attempt to get the economy to slow to a more sustainable pace. Growth has been strong, but that’s largely due to a declining unemployment rate – and the unemployment rate cannot fall forever. Soft landings are difficult to achieve – it’s difficult to gauge the amount of slack available – and the risks of a policy error (moving too rapidly or too slowly) naturally rise in a late-cycle economy. Personnel changes at the Fed have given a slightly more hawkish tilt to the FOMC this year, but the Fed’s approach to monetary policy is essentially the same as it was under Janet Yellen’s leadership. Some Fed officials believe that the economy has already exceeded its potential.

A number of emerging economies may face difficulties as the Fed raises short-term rates, but the Fed’s focus is on the domestic economy. Tighter monetary policy ought not to have a significant impact on the U.S. economy in the short term, but higher intermediate and long-term interest rates (a consequence of rising short-term interest rates) should dampen economic growth over time. There are no signs of a recession on the horizon, but the risks of a possible downturn are likely to rise as we head into 2019.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James